Navigating Medicare Supplement Plans N & G: What You Need to Know

🔑 Key Takeaways

1. Plan Standardization: All Medicare Supplement plans are standardized, but premiums can vary, so shopping around is crucial.

2. Enrollment Timing: Enroll during your Medigap Open Enrollment Period to avoid medical underwriting and guarantee coverage.

3. Financial Stability: Choose insurers with strong financial ratings to ensure long-term stability and reliable service.

4. Independent Agents: Utilize independent agents to compare plans, save time, and ensure you get the best value.

As we navigate the intricate world of Medicare, it’s essential to understand the supplemental plans that can help cover gaps in Original Medicare (Parts A and B). Among these, Medicare Supplement Plans N and G are popular choices. Here, we will dive into the details of these plans, including enrollment guidelines, underwriting issues, and the importance of financial stability. We’ll also highlight why these plans might be ideal for you and how an independent agent can be a valuable resource.

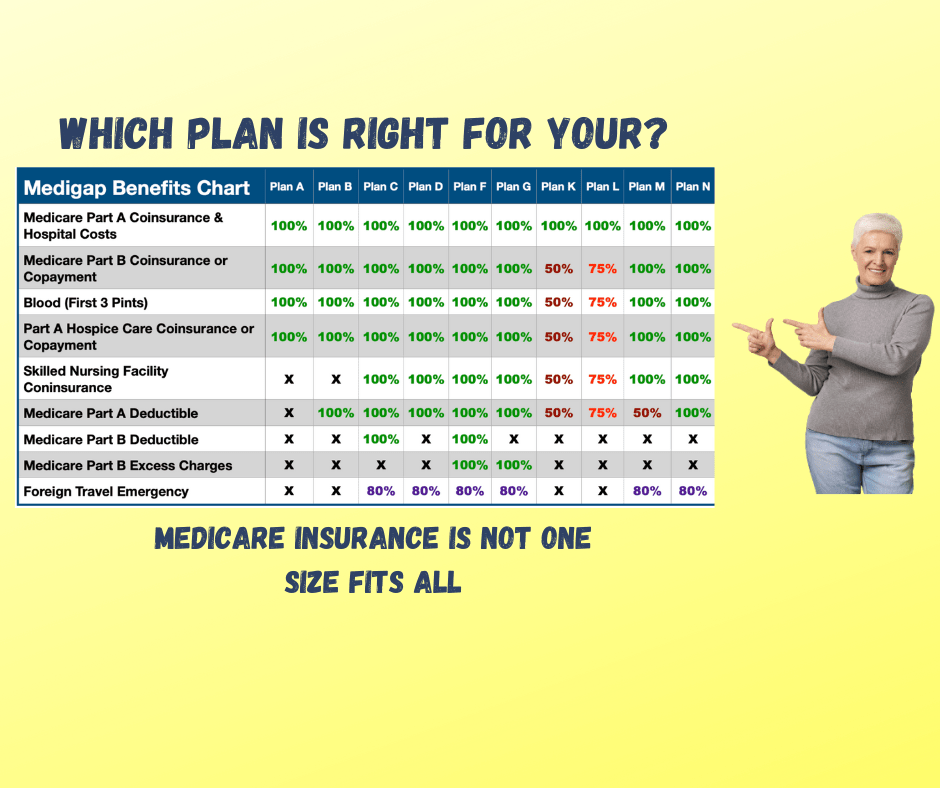

Navigating Medicare Supplement Plans Standardization

Before we explore Plans N and G, it’s crucial to understand that Medicare Supplement plans, also known as Medigap, are standardized. This means that regardless of the insurer, each plan must offer the same basic benefits. For example, Plan G from one company offers the same coverage as Plan G from another. However, premiums can vary widely between insurers, making it essential to shop around.

Plan G: Comprehensive Coverage

Medicare Supplement Plan G is often favoured for its comprehensive coverage. It covers all the gaps in Original Medicare except for the Part B deductible. This includes:

– Part A deductible

– Part A coinsurance and hospital costs

– Part B coinsurance or copayment

– Blood (first 3 pints)

– Part A hospice care coinsurance or copayment

– Skilled nursing facility care coinsurance

– Foreign travel emergency (up to plan limits)

Plan G is an excellent choice for those who want minimal out-of-pocket expenses after paying the Part B deductible.

Plan N: Lower Premiums, Slightly More Out-of-Pocket Costs

Medicare Supplement Plan N is designed to offer lower premiums in exchange for slightly higher out-of-pocket costs. It covers most of what Plan G does, but with some differences:

Part B coinsurance is covered, except for a $20 copayment for office visits and a $50 copayment for emergency room visits.

Part B deductible is not covered.

Part B excess charges are not covered.

Plan N is ideal for individuals willing to handle small copayments in exchange for lower premiums.

Enrollment and Underwriting Guidelines

When to Enroll:

The best time to enrol in a Medicare Supplement plan is during your Medigap Open Enrollment Period. This period lasts for six months, starting when you turn 65 and are enrolled in Part B. During this time, you have guaranteed issue rights, meaning insurers cannot deny you coverage or charge you more due to pre-existing conditions.

**Underwriting Guidelines:**

Outside the Open Enrollment Period, you may be subject to medical underwriting. Insurers can evaluate your health history and current health status, which might result in higher premiums or denial of coverage. However, some states offer additional guaranteed issue rights or special enrollment periods.

Importance of Financial Stability

Financial stability is crucial when choosing a Medicare Supplement plan. Insurers with strong financial ratings are more likely to offer stable premiums and reliable service over time. Look for ratings from agencies like A.M. Best, Moody’s, or Standard & Poor’s to gauge an insurer’s financial health.

Top 3 Reasons to Choose Navigating Medicare Supplement Plans N or Plan G

1. Comprehensive Coverage: Plan G offers almost complete coverage with predictable costs, making it an excellent choice for those who want to avoid unexpected medical expenses.

2. Cost Savings: Plan N’s lower premiums can save money in the long run for those who don’t mind occasional copayments.

3. Freedom to Choose Providers: Both plans allow you to see any doctor or specialist who accepts Medicare, offering more flexibility than Medicare Advantage plans.

The Role of an Independent Agent

An independent agent or broker can be an invaluable resource. They:

1. Provide Objective Comparisons: Independent agents can compare plans from multiple insurers, ensuring you get the best coverage at the best price.

2. Save Time: They handle the legwork of researching and comparing plans, saving you time and effort.

3. Offer Expertise: With their knowledge of Medicare and the insurance market, they can help you navigate complex decisions and avoid common pitfalls.

Conclusion

Navigating the complexities of Medicare can be daunting, but understanding the ins and outs of Medicare Supplement Plans N and G can significantly ease the process. These plans offer valuable options for covering gaps in Original Medicare, each tailored to different financial preferences and healthcare needs. By enrolling during your Medigap Open Enrollment Period, you can secure coverage without the hurdles of medical underwriting. Additionally, considering an insurer\’s financial stability ensures you choose a plan that offers long-term reliability.

Leveraging the expertise of an independent agent can save you time and money, providing objective comparisons and personalized recommendations. Remember, the goal is to find a plan that offers comprehensive coverage, fits your budget, and grants you peace of mind. With the right information and guidance, you can confidently choose the best Medicare Supplement plan to meet your needs, ensuring a smoother and more secure healthcare journey.