Original Medicare is defined as the federal health insurance program comprising Medicare Part A and Part B, covering hospital stays, doctor visits, and outpatient medical services for Americans aged 65 and older, as well as certain individuals with disabilities or End-Stage Renal Disease. Getting original medicare explained correctly from the start matters because enrollment mistakes, especially around drug coverage and supplemental plans, cost beneficiaries real money. Part A covers inpatient care. Part B covers outpatient and medical services. Together, they form the foundation of federal Medicare coverage, but they leave meaningful gaps that every new enrollee must plan around.

What original medicare covers and what it leaves out

Original Medicare covers two distinct categories of care, each governed by its own rules, deductibles, and cost-sharing structure.

Medicare Part A: Hospital Insurance pays for inpatient hospital stays, care in a skilled nursing facility following a qualifying hospital stay, hospice care, and some home health services. Most people think of Part A as their hospital coverage, which is accurate. What surprises many new enrollees is that Part A does not cover custodial long-term care, meaning the kind of ongoing personal assistance you might need in a nursing home if you cannot perform daily activities independently.

Medicare Part B: Medical Insurance covers outpatient care, including visits to your primary care doctor and specialists, preventive services like annual wellness visits and certain screenings, mental health services, and durable medical equipment such as wheelchairs or blood glucose monitors. Part B also covers medically necessary ambulance services and some home health care. For beneficiaries managing diabetes, understanding diabetic supply coverage under Part B is worth reviewing separately.

What Original Medicare does not cover is just as important as what it does. The three most significant exclusions are:

- Prescription drugs: Original Medicare excludes drug coverage; most beneficiaries must enroll separately in a Part D plan to get prescription benefits.

- Dental, vision, and hearing: Routine dental cleanings, eyeglasses, and hearing aids are not covered under Parts A or B.

- Out-of-pocket maximum: There is no annual spending cap under Original Medicare, which means a serious illness could expose you to unlimited cost-sharing without supplemental coverage.

These gaps are not accidental. They are the reason Medigap policies and Medicare Advantage plans exist. Understanding the gaps is the first step toward deciding whether you need additional coverage.

Pro Tip: If you take prescription medications regularly, enroll in a Part D plan during your Initial Enrollment Period. Delaying Part D enrollment when you have no other creditable drug coverage triggers a permanent late enrollment penalty.

How enrollment works for Original Medicare Parts A and B

Enrollment in Original Medicare is not one-size-fits-all. The rules differ for Part A and Part B, and the timing of your enrollment has lasting financial consequences.

-

Automatic enrollment: If you are already receiving Social Security or Railroad Retirement Board benefits when you turn 65, you are automatically enrolled in both Part A and Part B. Your Medicare card arrives in the mail about three months before your 65th birthday.

-

Manual enrollment: If you are not yet receiving Social Security at 65, you must actively sign up through the Social Security Administration, either online at SSA.gov, by phone, or in person at a local office.

-

Premium-free Part A: Most people qualify for premium-free Part A if they or their spouse paid Medicare payroll taxes for at least 40 quarters, which equals 10 years of work. If you have fewer than 40 quarters, you pay a monthly premium for Part A.

-

Part B is voluntary: Part B requires a monthly premium and you can choose to decline it, particularly if you have employer-sponsored coverage through an active job. Puerto Rico residents are automatically enrolled in Part A but must actively enroll in Part B even if they receive Social Security.

-

Initial Enrollment Period (IEP): Your IEP spans seven months, starting three months before the month you turn 65, including your birthday month, and ending three months after. Enrolling during the first three months of your IEP means your coverage starts on the first day of your birthday month.

-

General Enrollment Period (GEP): If you miss your IEP, you can enroll during the GEP, which runs January 1 through March 31 each year, with coverage beginning July 1. A late enrollment penalty on Part B applies in most cases.

-

Special Enrollment Period (SEP): If you delayed Part B because you had employer group coverage, you qualify for an SEP when that coverage ends, allowing you to enroll without penalty.

Pro Tip: Do not decline Part B simply to save on the monthly premium if you do not have other creditable coverage. The late enrollment penalty adds 10% to your Part B premium for every 12-month period you were eligible but did not enroll, and it lasts for as long as you have Part B.

What does Original Medicare cost in 2026?

Original Medicare’s cost structure involves premiums, deductibles, and coinsurance. None of these are fixed or capped without supplemental coverage, which makes budgeting a critical exercise before you retire.

| Cost Component | 2026 Amount | Notes |

|---|---|---|

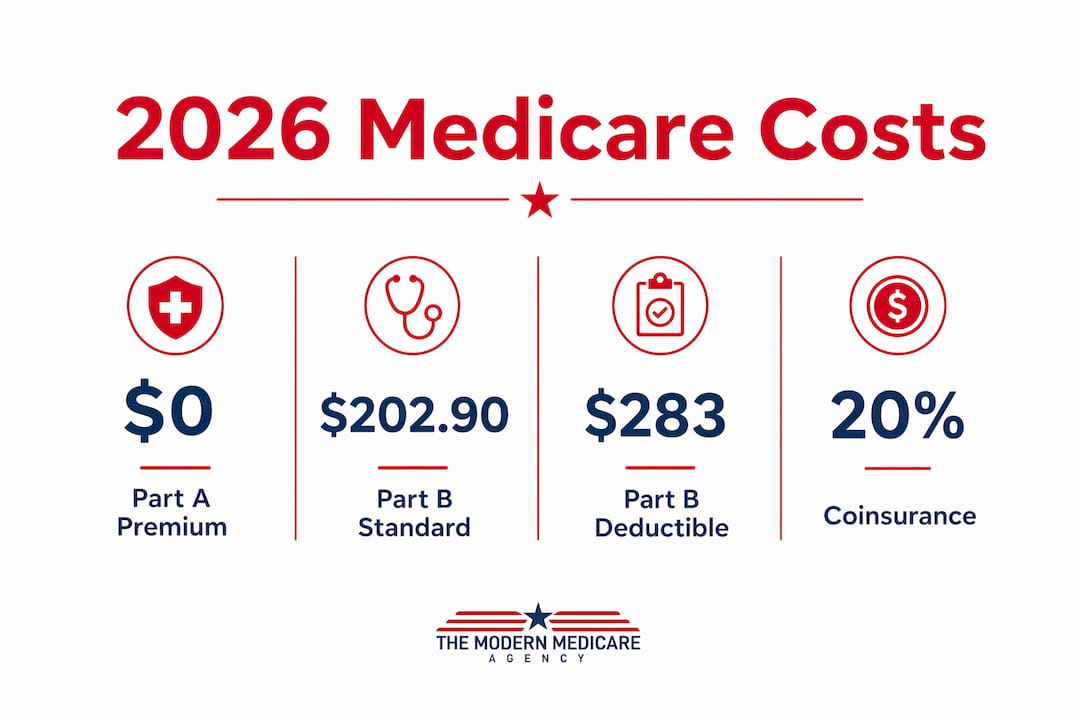

| Part A premium (most enrollees) | $0 | Requires 40+ quarters of Medicare taxes |

| Part A inpatient deductible | $1,676 per benefit period | Applies each new benefit period, not annually |

| Part B standard monthly premium | $202.90 | Largest increase since 2022 |

| Part B annual deductible | $283 | Paid once per calendar year |

| Part B coinsurance | 20% of approved amount | Applies after deductible is met |

| Annual out-of-pocket maximum | None | No spending cap without supplemental coverage |

The 2026 Part B standard premium rose to $202.90 per month, up $17.90 from 2025. That increase reflects rising healthcare costs and signals that premiums will likely continue climbing in future years, making long-term budget planning essential.

The 20% coinsurance under Part B deserves special attention. After you meet the $283 annual deductible, you pay 20% of every Medicare-approved service for the rest of the year. There is no out-of-pocket maximum under Original Medicare, meaning a major surgery or extended treatment could cost you tens of thousands of dollars in coinsurance alone.

One factor many new enrollees overlook is whether their provider accepts Medicare assignment. Providers who accept assignment agree to charge only the Medicare-approved amount. Non-participating providers can charge up to 15% above that amount, increasing your out-of-pocket costs further.

Higher-income beneficiaries face an additional cost called the Income-Related Monthly Adjustment Amount, or IRMAA. IRMAA surcharges range from an extra $81.20 to over $487 per month depending on your modified adjusted gross income from two years prior. If your income dropped significantly after retirement, you can request a reconsideration through the Social Security Administration using Form SSA-44.

Key cost factors to track every year:

- Part B premium changes announced each fall by CMS

- IRMAA thresholds, which adjust annually for inflation

- Part A benefit period deductibles, which reset with each new hospital admission after a 60-day gap

How does Original Medicare compare to Medicare Advantage and Medigap?

Understanding original medicare vs medicare advantage is one of the most consequential decisions you will make at 65. Both options provide Parts A and B coverage, but they work very differently.

| Feature | Original Medicare | Medicare Advantage | Medigap + Original Medicare |

|---|---|---|---|

| Provider network | Any Medicare-accepting provider nationwide | Usually restricted to plan network | Any Medicare-accepting provider nationwide |

| Out-of-pocket maximum | None | Required by law | Depends on plan; can cover most costs |

| Prescription drug coverage | Not included | Usually bundled | Requires separate Part D plan |

| Monthly premium | Part B premium only | Often low or $0 (plus Part B) | Part B premium plus Medigap premium |

| Referrals required | No | Often yes (HMO plans) | No |

Medicare Advantage plans bundle Parts A, B, and usually Part D into a single plan offered by a private insurer. They are required by law to cap your annual out-of-pocket spending, which is a meaningful protection that Original Medicare does not provide. The trade-off is network restrictions. Most Medicare Advantage plans are HMOs or PPOs that require you to use in-network providers or pay significantly more.

Medigap, also called Medicare Supplement Insurance, works alongside Original Medicare rather than replacing it. A Medigap policy pays some or all of the costs that Original Medicare leaves behind, including the 20% coinsurance, Part A deductibles, and in some plans, foreign travel emergency care. You keep full provider flexibility because any doctor who accepts Medicare accepts your Medigap coverage. The cost is a separate monthly premium on top of your Part B premium, but it creates predictable, capped expenses.

Pro Tip: The best time to buy a Medigap policy is during your six-month Medigap Open Enrollment Period, which starts the month you are both 65 and enrolled in Part B. During this window, insurers cannot deny you coverage or charge more based on pre-existing conditions. After it closes, medical underwriting applies in most states.

Whether Original Medicare with a Medigap plan or Medicare Advantage fits you better depends on your health, your preferred doctors, how much you travel, and your tolerance for variable costs. Neither is universally superior. They serve different needs.

Key takeaways

Original Medicare provides essential hospital and medical coverage through Parts A and B, but its lack of an out-of-pocket maximum and exclusion of prescription drugs, dental, vision, and hearing make supplemental planning a necessity, not an option.

| Point | Details |

|---|---|

| Two-part structure | Original Medicare consists of Part A (hospital) and Part B (medical), each with separate costs. |

| No spending cap | Without supplemental coverage, there is no annual limit on what you can owe under Original Medicare. |

| 2026 Part B premium | The standard monthly premium is $202.90, with a $283 annual deductible and 20% coinsurance. |

| Enrollment timing matters | Missing your Initial Enrollment Period triggers permanent late penalties on Part B and Part D. |

| Supplemental options exist | Medigap fills cost gaps; Medicare Advantage bundles coverage with a network and an out-of-pocket cap. |

What I’ve learned after nearly two decades of Medicare counseling

I have been helping people navigate Medicare since 2007, and the single most common mistake I see is treating Medicare as one thing. People turn 65, they hear “Medicare,” and they assume they are covered. They are not fully covered. They have a foundation, and what they build on top of that foundation determines whether a health crisis becomes a financial one.

The absence of an out-of-pocket maximum under Original Medicare is not a minor detail. I have seen clients face $30,000 or more in coinsurance after a serious hospitalization because they assumed Medicare covered everything. It does not. That risk is real, and it is avoidable.

Part B being voluntary also catches people off guard. I have spoken with retirees who declined Part B at 65 because they felt healthy and wanted to save $200 a month. Years later, they paid permanent penalties and faced underwriting hurdles when trying to add Medigap. The short-term savings rarely justify the long-term cost.

My honest advice: do not make enrollment decisions based on what you think Medicare covers. Make them based on what it actually covers, what it costs, and what your specific health situation requires. Reviewing your Medicare supplement options before your Initial Enrollment Period closes is one of the highest-value decisions you can make for your retirement finances.

— Paul

Get personalized Medicare guidance from Paulbinsurance

Paulbinsurance specializes in helping Medicare consumers make confident, informed decisions. Paul Barrett and his team of independent agents have been doing this since 2007, and the approach has always been education first.

Whether you are sorting through 2026 Medicare coverage options for the first time or comparing Original Medicare against Medicare Advantage and Medigap plans, Paulbinsurance offers no-pressure, personalized guidance at no cost to you. The team covers Medicare supplements, Part D drug plans, dental, hospital indemnity, and more. Reach out today to get clarity on your options before your enrollment window closes.

FAQ

What is Original Medicare in simple terms?

Original Medicare is the federal health insurance program made up of Part A (hospital coverage) and Part B (medical coverage), administered by the Centers for Medicare and Medicaid Services. It covers hospital stays, doctor visits, and outpatient services but does not include prescription drugs, dental, or vision.

Does Original Medicare cover prescription drugs?

No. Original Medicare excludes prescription drugs, so most beneficiaries enroll separately in a Medicare Part D plan to get drug coverage. You can learn more in the Part D guide from Paulbinsurance.

What is the out-of-pocket maximum for Original Medicare?

Original Medicare has no annual out-of-pocket maximum. Beneficiaries pay 20% coinsurance on Part B services with no spending cap, which is why many enrollees add a Medigap policy or choose Medicare Advantage to limit their financial exposure.

When can I enroll in Original Medicare?

Your Initial Enrollment Period spans seven months centered on your 65th birthday. If you miss it without qualifying for a Special Enrollment Period, you can enroll during the General Enrollment Period from January 1 through March 31, but late penalties may apply to Part B.

How much does Part B cost in 2026?

The standard Part B premium for 2026 is $202.90 per month, with a $283 annual deductible. Higher-income beneficiaries pay additional IRMAA surcharges ranging from $81.20 to over $487 per month above the standard premium.