What if the person helping you choose your Medicare plan was more like a personal protector than a salesperson? In 2026, the flood of insurance marketing is louder and more confusing than ever. We know the stress of trying to understand how the new $2,100 out-of-pocket cap for prescriptions affects your wallet, or why the Part B premium rose to $202.90 this year. It’s natural to worry about losing access to a doctor you’ve trusted for decades. You deserve a guide who removes that anxiety rather than adding to it.

We want to help you move from this state of uncertainty to a place of total peace of mind. By learning the exact questions to ask a medicare broker, you can identify a dedicated advocate who puts your health and budget above a commission check. We’ll show you how to find a professional who will verify your specific medications against the latest negotiated drug prices and ensure you never overpay. This guide outlines the clear, logical steps to finding an expert who will truly work for you.

Key Takeaways

- Understand how a broker’s independence impacts your options and why we believe having access to multiple carriers is vital for your 2026 coverage.

- Identify the specific questions to ask a medicare broker to confirm they are a true advocate who will protect your interests year-round.

- Learn the “Big Three” verification process to ensure your doctors, specialists, and prescriptions are all handled correctly within your new plan.

- Discover why the most valuable part of a broker relationship happens after you sign up, especially when dealing with complex billing or claim issues.

- Gain the clarity you need to move past the noise of 2026 marketing and find a plan that provides genuine peace of mind.

Why You Need a Medicare Broker in 2026

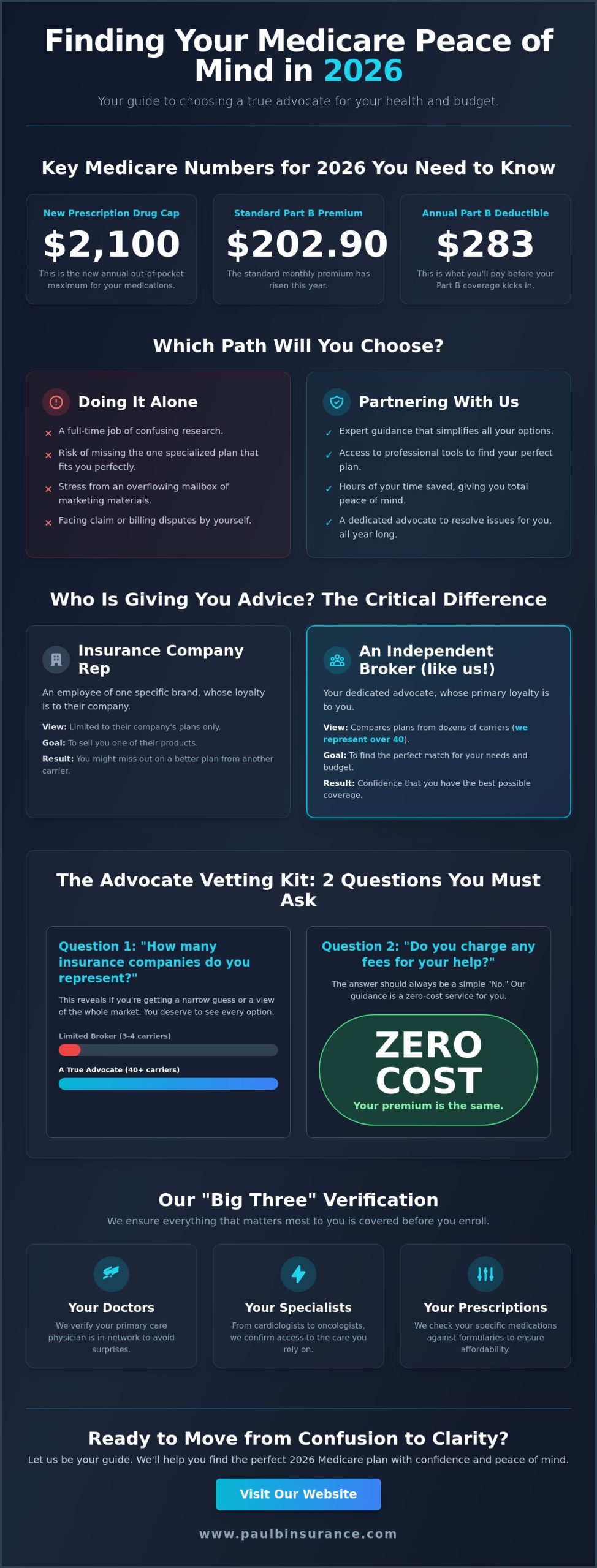

Your mailbox is likely overflowing with shiny flyers and confusing letters right now. It is a lot to handle, and we understand why you might feel stressed. In 2026, Medicare feels more complex because the rules have changed significantly. Between the new $2,100 prescription drug out-of-pocket cap and the standard Part B premium rising to $202.90, there are many moving parts. The transition into 2026 also brings a Part B annual deductible of $283. Understanding these shifts is exactly why knowing the right questions to ask a medicare broker is so essential for your financial security. We see our role as your professional guide. We take that mountain of marketing and simplify it into a clear, manageable plan.

One of the first things we want you to know is that working with us costs you exactly zero dollars. We are compensated by the insurance companies, so your premium stays the same whether you sign up through us or try to do it yourself. This “Zero Cost” reality means you get an expert advocate without any added financial burden. Our goal is to move you from feeling overwhelmed by 2026 mailers to having total peace of mind. We want you to feel protected and empowered throughout this journey.

The Difference Between “Doing it Alone” and Having an Advocate

Trying to research every plan on your own is a full-time job. With the average number of Medicare Advantage plans dropping slightly this year, the options that remain are more specialized. We use professional comparison tools to filter out the noise of TV commercials and junk mail. We save you hours of research by focusing only on what fits your specific needs. If an insurance company says “no” to a claim or makes a billing error in the middle of the year, you don’t have to fight them alone. You call us, and we step in to resolve the issue. Having an advocate means you never have to face the system by yourself.

The Broker vs. The Insurance Company Representative

It’s important to understand who you are talking to. An insurance company representative is an employee of that specific brand. They can only tell you about their own plans. If you’re looking for a deep dive into What is Medicare? or need to compare a Medigap plan against a different carrier, they have a limited view. We are independent brokers. This means we compare options from dozens of different carriers to find your perfect match. An independent broker is a dedicated consumer advocate whose primary loyalty is to you, not a corporate brand. When you prepare your questions to ask a medicare broker, remember that their independence is the foundation of the trust you are building together.

Vetting the Expert: Questions to Ask About Their Independence

Before we dive into plan details, we must talk about the person sitting across from you or on the other end of the phone. The plan you choose is only as good as the advice behind it. If the advice is biased, your coverage will be too. This is why the very first questions to ask a medicare broker should focus on their independence and their loyalty. You need to know if they are working for a giant insurance corporation or if they are truly working for you. This “independence test” protects you from being steered toward a plan that benefits the agent’s commission rather than your health needs.

One of the most vital questions you can pose is: “How many insurance companies are you appointed with?” In 2026, the average number of available Medicare Advantage plans has dipped slightly to 32 per enrollee. If your agent is only appointed with three or four companies, they are essentially guessing with your health. They can’t see the whole picture. We represent over 40 carriers because we believe you deserve to see every option available in your zip code. You should also ask if they charge any fees. The answer should always be a simple “no.” While programs like SHIP offer free, unbiased Medicare counseling, we provide that same zero-cost expertise while also handling the complex paperwork of your enrollment.

The Power of Choice: Why “40+ Carriers” Matters

We shop the entire market to find your specific needle in a haystack plan. A broker with limited options might miss the best Medicare Advantage plan for your unique situation. When an agent only represents two or three companies, they are forced to make your needs fit their limited inventory. We do the opposite. We look at your needs first and then scan our massive list of partners to find the one that fits you perfectly. If you want to see how this variety can work for you, our team is ready to help you compare these options side by side.

Understanding How Your Broker is Licensed

Professionalism in 2026 requires more than just a friendly smile. Ask your broker if they are AHIP certified for the current 2026 plan year and if they are licensed in your specific state. We maintain licenses in 34+ states to serve our clients wherever they go. However, local expertise still matters deeply. For our neighbors in Melville, NY, we understand the local hospital networks and doctor groups in a way a national call center never could. This community trust ensures that when we say a doctor is in-network, we’ve done the local legwork to prove it.

Plan-Specific Questions: Ensuring Your Doctors and Drugs are Covered

Once you feel confident in your broker’s independence, it is time to look at the plans themselves. We focus on what we call the Big Three: Doctors, Drugs, and Dollars. These three pillars determine if a plan will actually work for your daily life. When preparing your questions to ask a medicare broker, make sure these are at the top of your list. You need to know if your specific specialists are in-network for 2026. You also need to understand how the new prescription rules affect your wallet. Finally, you must know the absolute maximum you might pay in a worst-case scenario. In 2026, the maximum out-of-pocket limit for in-network Medicare Advantage services is $9,250. Knowing this number gives you a ceiling on your financial risk.

Protecting Your Doctor-Patient Relationships

We don’t just look at a printed directory and hope for the best. We use the carrier’s internal tools to verify that your specific cardiologist and primary care doctor are still participating in the plan for the 2026 calendar year. This is vital because 2026 introduces a new special enrollment period for people who join a plan based on inaccurate provider lists. If you love a plan but your doctor is out-of-network, we can help you weigh the costs. In simple terms, an HMO usually requires you to stay within a strict network and get referrals. A PPO gives you the freedom to see doctors outside the network, though you will likely pay more for that privilege. We help you decide which level of freedom fits your budget.

Navigating the 2026 Prescription Drug Landscape

The rules for Medicare Part D have changed for the better this year, but they still require careful planning. The most significant change in 2026 is the $2,100 out-of-pocket cap on covered prescriptions. This means once you spend $2,100 on your medications, you won’t pay another penny for covered drugs for the rest of the year. However, you still need to ask: “Is my pharmacy considered a preferred pharmacy for this plan?” Using a non-preferred pharmacy can cause your costs to spike even with the new cap. We also check the $615 maximum deductible to see how it affects your initial costs. Drug formularies change every single year and require an annual review to ensure your specific medications are still covered at the lowest possible price. We perform this review for you to remove the guesswork and keep your costs predictable.

Beyond Enrollment: Questions About Long-Term Support

Most people think the journey ends when their new Medicare card arrives in the mail. We believe that is exactly when the most important part of our job begins. Your health needs don’t stay the same forever, and the insurance system certainly doesn’t either. When you are finalizing your list of questions to ask a medicare broker, you must look past the initial enrollment date. You need an advocate who stays by your side throughout the entire year, not just during the busy autumn months. We want you to have a single point of contact who knows your history and cares about your future.

One of the most critical questions you should pose is: “What happens if I have a billing error or a claim is denied in July?” You should never have to spend your afternoon waiting on hold with a giant insurance company. That is our responsibility. We step in to resolve disputes and clarify confusing paperwork so you can focus on your health. We also help you look at the bigger picture. This includes checking if you need additional protection like dental insurance or vision coverage to fill the gaps in your basic plan.

The “Year-Round” Promise

We are committed to being your advocate 365 days a year. Life happens. You might move to a new zip code, or a doctor might suggest a new medication that isn’t on your current list. In 2026, we are paying very close attention to the new $2,100 out-of-pocket cap for prescriptions. If there is ever a question about whether a specific drug is counting toward that limit, we are the ones who dig into the details for you. We handle these life changes with you so your coverage never skips a beat. If you want a partner who stays committed long after the paperwork is filed, contact our team today to start a lifelong relationship.

Preparing for the Annual Review

The plans available in 2026 will likely look different by 2027. We proactively track these changes so you don’t have to. Every autumn, we reach out to our clients to perform a comprehensive drug list review. We check your current medications against the upcoming year’s formularies and negotiated prices. This ensures your plan is always up to date and you are never surprised by a sudden price hike in January. This proactive approach is the difference between a seasonal salesperson and a true advocate. You deserve the certainty that comes from knowing someone is always looking out for your best interests.

Finding Your Peace of Mind with The Modern Medicare Agency

We believe that finding the right health coverage should not feel like a battle. It should feel like a relief. Throughout this guide, we have explored the technical side of 2026 coverage, from the $283 Part B deductible to the complex new drug price negotiations. However, the most important part of this journey is the relationship you build with your advocate. As you finalize your list of questions to ask a medicare broker, remember that the best answer is one that makes you feel heard and protected. We embody the independent advocate model because we know that your peace of mind is worth more than any single insurance brand.

Our founder, Paul Barrett, started this agency with a very specific mission. He saw a “sales” culture in the insurance industry that often left seniors feeling like nothing more than a number. He wanted to create a sanctuary from that high-pressure environment. Our process is simple and methodical: we listen first, we educate second, and we enroll last. We don’t start by talking about plans. We start by talking about you. This approach ensures that we move from a state of 2026 marketing confusion to a place of total certainty together.

A Personal Approach in a Digital World

We use a “we” philosophy in everything we do. This means we are in this with you every step of the way. While we use modern technology to scan the market and compare dozens of carriers, we never lose sight of old-fashioned empathy. We know that behind every medication list is a person who just wants to stay healthy without going broke. Our team knows the 2026 regulations inside and out, including how the new Part B immunosuppressive drug premium of $121.60 might affect specific beneficiaries. We combine this high-level expertise with a gentle, patient guidance that removes the anxiety from the process.

Your Next Steps to Clarity

If you are ready to move forward, your first conversation with us will be completely stress-free. There is no pressure to sign anything. We simply want to help you organize your “Medicare Homework.” Before we speak, try to gather a complete list of your current medications and the names of any specialists you see regularly. This allows us to hit the ground running and provide the clear answers you deserve. You have worked hard for your retirement, and you deserve a plan that works just as hard for you. Schedule your stress-free Medicare consultation with our team today and let us help you find the security you’ve been looking for.

Step Into Your Medicare Future With Certainty

You now have a clear roadmap to navigate the 2026 Medicare landscape with confidence. By knowing the right questions to ask a medicare broker, you’ve moved from a state of information overload to a position of true control. We’ve explored why working with an independent advocate who compares 40+ carriers is the only way to ensure you see every option available. We have also covered the vital importance of verifying your specific doctors and medications against the significant 2026 Part D legislative changes.

Our team is proud to serve as independent brokers licensed in 34+ states, including New York, Florida, and California. We provide the expert guidance you need to manage the rising Part B premiums and the new prescription out-of-pocket caps. You don’t have to face these complex systems alone. We are here to protect your health and your budget every day of the year, ensuring you never overpay for the coverage you deserve. Let’s start your journey to total peace of mind together.

Get Expert Medicare Help & Peace of Mind Today

Frequently Asked Questions

Do I have to pay a Medicare broker for their help in 2026?

No, you do not pay us a single penny for our services. We are compensated directly by the insurance companies we represent, so your premium remains exactly the same as if you signed up alone. This allows you to receive expert guidance and personal advocacy without any added financial burden.

Can a Medicare broker help me switch from Medicare Advantage to a Medigap plan?

Yes, we can certainly help you navigate a move from a Medicare Advantage plan to a Medigap (Medicare Supplement) plan. It is important to remember that in most states, this switch may require medical underwriting to determine eligibility. We will guide you through the timing and health requirements to ensure a smooth transition without a gap in your coverage.

What is the difference between a captive agent and an independent broker?

A captive agent works for one specific insurance carrier and can only offer you their specific products. An independent broker represents dozens of different companies and shops the entire market to find your best fit. This distinction is one of the most important questions to ask a medicare broker because independence ensures you see every available option in your area.

How do Medicare brokers get paid if the service is free to me?

We receive a commission from the insurance company once you are successfully enrolled in a plan. These payments are regulated by the government and do not change based on which plan you choose. This system allows us to focus entirely on finding the right fit for your health needs rather than pushing a specific brand.

Should I ask my broker about the 2026 Part D “Donut Hole” changes?

Yes, you should definitely ask how the latest prescription rules affect your specific costs. The old “donut hole” concept has been replaced by a clear $2,100 out-of-pocket maximum for covered drugs in 2026. We will explain how this cap and the new $615 maximum deductible work together to protect your finances throughout the year.

Can a broker help me if I already have a Medicare plan?

Absolutely, we help many people who already have existing coverage. We can review your current plan to see if it still meets your needs or if 2026 changes, such as the $202.90 Part B premium, make a different plan more attractive. You don’t have to wait for a problem to arise to benefit from a professional review of your current benefits.

How often should I meet with my Medicare broker to review my coverage?

We recommend a formal review at least once every year during the Annual Enrollment Period. Since drug formularies and plan networks change every single year, a quick check-in ensures your doctors and medications remain covered. We also suggest reaching out whenever you experience a major life change, such as moving to a new home or receiving a new diagnosis.

Is it better to call the insurance company directly or use a broker?

Using a broker is almost always better because we offer an impartial comparison across multiple companies. When you call a carrier directly, they will only tell you why their own plan is the best choice. We provide a broader view of the market and remain your personal advocate if you ever face a denied claim or a billing error later in the year.