What if the mountain of insurance mailers on your kitchen table is actually hiding the best plan for your budget? It’s 2026, and with the new $2,100 out-of-pocket limit for Part D prescriptions, the stakes for your healthcare have never felt higher. You’re likely wondering, “should I use a medicare broker or enroll myself” as you try to figure out which plans still include your specific doctors. It’s completely normal to feel a sense of anxiety over these changes or worry about choosing a plan that leaves you with unexpected costs.

We understand how confusing this process feels when you’re bombarded with conflicting information. Our goal is to replace that stress with total clarity. You deserve to feel certain that your medications are covered and your doctors are in-network without having to become an insurance expert yourself. This guide breaks down the critical differences between DIY enrollment and working with an independent professional. You’ll discover how to secure the best possible coverage for 2026 while keeping the entire process simple, free, and error-free.

Key Takeaways

- Learn how the 2026 Part D changes and the new $2,100 out-of-pocket limit make plan selection more complex than ever.

- Understand the trade-offs to help you decide, “should I use a medicare broker or enroll myself,” based on your specific health and budget needs.

- Discover how an independent broker provides access to over 40 carriers at no cost to you, offering options a single-brand agent cannot.

- Identify the “Independence Test” to find a trustworthy advocate who prioritizes your peace of mind over insurance company commissions.

- Find out why professional guidance acts as “insurance for your insurance” by providing year-round support even after your enrollment is complete.

The 2026 Medicare Landscape: Why Enrollment Feels Different This Year

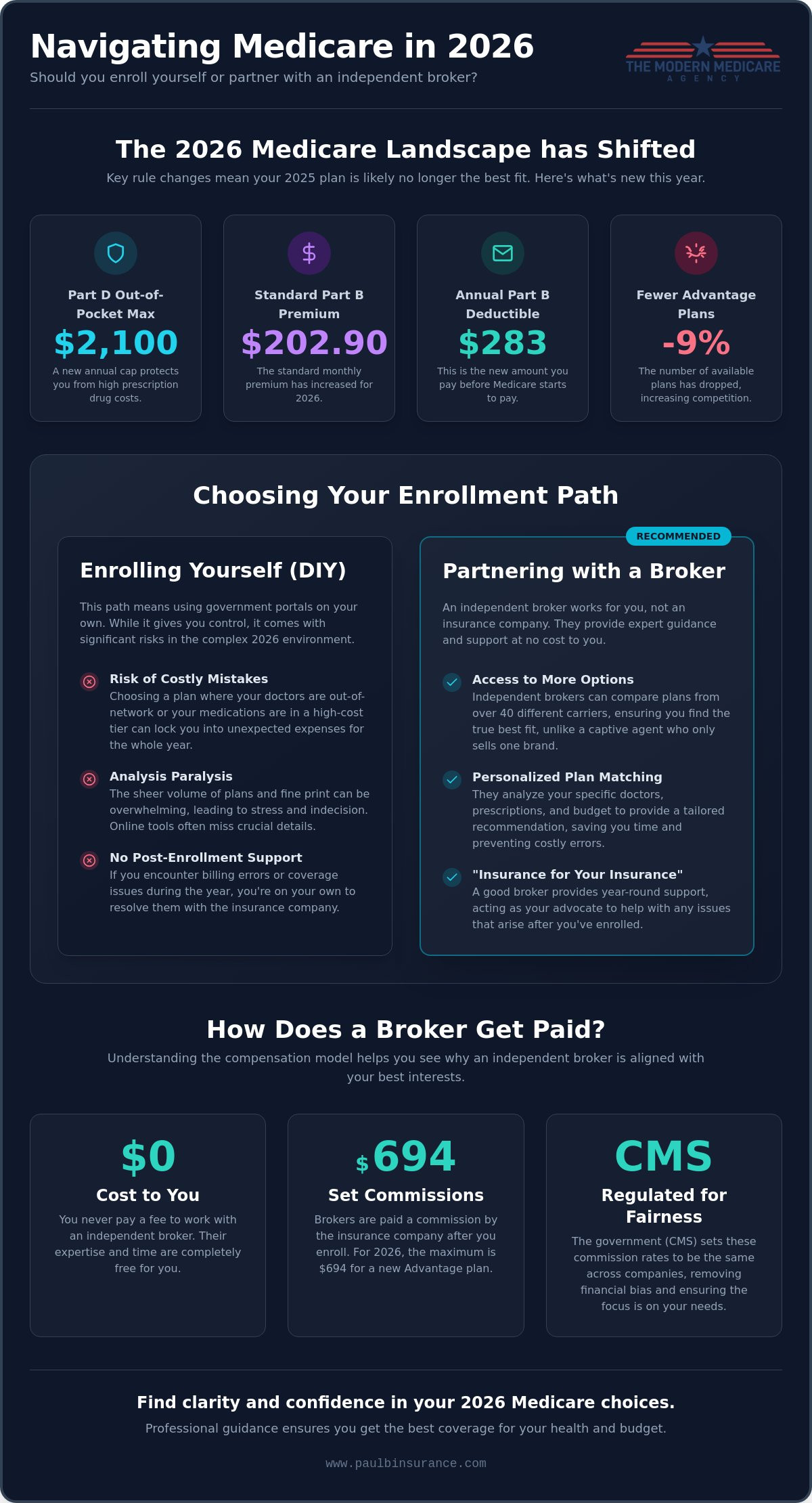

It is 2026, and your mailbox is likely overflowing with glossy flyers and urgent notices. This “Mailbox Blizzard” is happening because the number of available Medicare Advantage plans has dropped by 9% this year, leaving a total of 3,373 plans nationwide. Insurance companies are competing harder than ever for your attention. As you sort through the stack, you might be asking yourself, “should I use a medicare broker or enroll myself” to find the right path forward. The truth is that the rules have changed significantly since last year.

The 2026 landscape is unique because the Inflation Reduction Act is now in full effect. For the first time, beneficiaries are seeing the benefits of newly negotiated prices for high-cost prescription drugs. While this is a major win for your wallet, it has caused insurance companies to completely redesign their Medicare Part D offerings. Relying on the standard Plan Finder tool might give you a list of prices, but it often misses the nuances of how these new drug price structures affect your specific pharmacy choices.

Making a mistake during this window is a heavy burden. If you choose a plan that doesn’t include your primary doctor or moves your most important medication to a higher cost tier, you are generally locked into that choice for the entire year. Before you dive into the specifics, it helps to have some foundational information on Medicare to understand how these different parts connect. Understanding the basics makes it much easier to see why a wrong choice can be so costly.

New 2026 Rules You Need to Know

The most important change is the new $2,100 out-of-pocket maximum for prescription drugs. While this protects you from astronomical costs, many carriers have adjusted their “extra benefits” to compensate. You may notice that dental, vision, or gym perks look different than they did in 2025. Additionally, the standard Part B monthly premium has increased to $202.90, and the annual deductible is now $283. Your 2025 plan was designed for a different set of regulations, so it likely isn’t the most efficient fit for the 2026 environment.

The Emotional Toll of Medicare DIY

Trying to manage this process alone often leads to “analysis paralysis.” It is one thing to find a plan that looks good on paper, but it is another thing entirely to ensure your specific doctors are actually in the network. The stress of second-guessing your choice can be exhausting. There is a profound difference between simply “finding a plan” and securing a solution that protects your health and your savings. Because of these massive regulatory shifts, 2026 requires a much more strategic approach to enrollment than we have seen in previous years.

Medicare Broker vs. DIY: Understanding Your Options

When you sit down to make your healthcare choices for the coming year, you generally have three main paths to follow. An independent Medicare broker acts as your personal advocate. They don’t work for one specific insurance company; they work for you. This is a vital distinction compared to a “captive agent” who is employed by a single carrier and can only show you that company’s specific plans. If you’re currently asking, “should I use a medicare broker or enroll myself,” keep in mind that an independent broker has the freedom to compare over 40 different companies to find your best fit.

The DIY enrollment path involves using the government portal to select a plan on your own. Some people also reach out to SHIP volunteers. These are helpful individuals who provide free government counseling. While they are a great resource for general questions, they aren’t licensed brokers. They can explain how the system works, but they cannot give you specific plan recommendations or step in to help you resolve billing issues with an insurance company later in the year.

How Independent Brokers Are Compensated

Working with an independent broker costs you exactly zero dollars. You never pay them a fee for their time or expertise. Instead, the insurance companies pay the broker a commission after you enroll. The Centers for Medicare & Medicaid Services (CMS) regulates these payments very strictly to prevent bias. In 2026, the maximum commission for a Medicare Advantage plan is $694 in most states. Because these rates are set by the government, a broker’s main goal is to keep you happy so you stay with them year after year. Learning how to choose a Medicare advisor who prioritizes your needs is the first step toward a stress-free experience.

The Role of the Medicare Plan Finder Tool

The official Medicare Plan Finder is the primary tool for those who choose to enroll themselves. It’s a useful website for seeing a broad list of available options. However, it’s also very easy to make a small data entry error that can lead to incorrect drug cost estimates. A broker uses professional software that often catches these tiny details. This software can cross-reference your specific doctors and medications across dozens of carriers in a matter of seconds. If you want to see how this professional comparison looks for your specific situation, you can reach out to a dedicated advocate who can run these reports for you at no cost.

The Pros and Cons of Enrolling Yourself vs. Using a Broker

Many people value the feeling of total autonomy. They want to see every option for themselves without feeling like they are being sold something. This is the primary appeal of the DIY approach. If you are weighing whether you should I use a medicare broker or enroll myself, it often comes down to how much value you place on your own time and the security of a professional second opinion. In 2026, that sense of control comes with a heavy research burden. What used to take a few hours of reading now requires a deep dive into hundreds of pages of plan data.

A significant benefit of working with an independent expert is the sheer amount of time you save. Most people spend roughly 20 hours researching plans, checking doctor networks, and comparing drug costs. A broker can often condense that entire process into a 30-minute conversation. Beyond the initial signup, a broker serves as your post-enrollment advocate. If a claim is denied or your favorite doctor suddenly leaves a network mid-year, you have a direct line to someone who can help resolve the issue. When you go it alone, those phone calls to the insurance company become your responsibility.

DIY Enrollment: The Risks and Rewards

The reward for self-enrollment is the peace of mind that you’ve seen every detail with your own eyes. However, the risks in 2026 are higher than in previous years. It’s easy to overlook the fine print in the “Summary of Benefits” for Medicare Advantage plans. With the new $2,100 out-of-pocket cap on prescription drugs, carriers have changed how they cover certain medications to balance their costs. Missing a critical enrollment deadline can also trigger lifetime late-enrollment penalties that stay with you forever.

Working with a Broker: The Expert Advantage

The “Expert Advantage” is about precision. A broker performs a personalized formulary analysis to ensure every one of your 2026 medications is covered at the lowest possible cost tier. They don’t just look at a digital list; they often call your doctors’ offices directly to confirm they still accept the plan you’re considering. This creates a “Safety Net” for your healthcare. You gain a dedicated partner whose job is to protect your budget and your access to care, ensuring that your transition into the 2026 plan year is smooth and certain.

How to Identify a Trustworthy Medicare Broker in 2026

Finding the right partner to help you through this transition is just as important as the plan itself. If you’re still weighing whether you should I use a medicare broker or enroll myself, the quality of the broker you choose will likely be the deciding factor. A trustworthy broker acts as a shield between you and the aggressive marketing tactics of big insurance companies. They should be willing to show you every option, even the ones that don’t pay them a commission. This level of transparency is the hallmark of a true advocate who prioritizes your peace of mind.

The first thing you should check is the “Independence Test.” Ask them how many carriers they represent. If they only work with five or six companies, you’re missing out on a huge portion of the market. An independent expert who represents over 40 carriers can provide a much broader perspective. It’s also helpful to find someone who understands the local nuances of your area, such as the provider networks in Melville, NY or other local market specifics. Certain doctors may only participate in specific local plans, and a national call center agent likely won’t know that.

Questions You Must Ask Before Enrolling

Before you commit to a partnership, have a candid conversation. You want to know that they’ll be there for the long haul, not just for the initial signup. Make sure to ask these specific questions:

- “How many different insurance carriers are you appointed with?” Look for a broker with access to 40+ carriers to ensure you’re seeing the full market.

- “Will you help me if I have a billing issue six months from now?” A dedicated advocate provides year-round support, not just during the enrollment window.

- “Can you explain the trade-offs between a Medicare Supplement and an Advantage plan for my specific health needs?”

Red Flags to Watch Out For

In 2026, the Centers for Medicare & Medicaid Services (CMS) has updated its marketing rules. While some guardrails have shifted, certain behaviors remain major red flags. Be wary of anyone using high-pressure tactics or claiming there are “limited time offers” that don’t actually exist in the Medicare world. A professional should always insist on looking at your specific medication list before making a recommendation. Finally, remember that unsolicited phone calls are a significant compliance violation. If someone calls you out of the blue without your permission, they aren’t following the rules designed to protect you.

If you want to experience the difference that a dedicated, local advocate can make, you can schedule a clear, no-pressure consultation with our team today.

Conclusion: Making the Right Choice for Your Peace of Mind

We have traveled through a lot of information together. From the “Mailbox Blizzard” of advertisements to the significant new $2,100 out-of-pocket drug cost cap, it is clear that 2026 is a landmark year for your healthcare. Deciding whether you should I use a medicare broker or enroll myself is the most important choice you will make this season. While the government website offers a path to do it yourself, the complexity of these new regulations means that even a small oversight can lead to a year of frustration. You deserve to move from a state of uncertainty to a state of total confidence.

Think of professional guidance as the ultimate “insurance” for your insurance. It is a safety net that ensures the plan you pick today actually works for you in July or October. At The Modern Medicare Agency, we provide unbiased and deeply empathetic support to help you find that perfect fit. We understand the stress of worrying if a doctor will leave a network or if a medication tier will change. Your Medicare plan is a 12-month commitment. Because you generally cannot change plans mid-year, making the right choice now is vital for your financial and physical health.

Ready to Simplify Your 2026 Medicare Journey?

Our team at The Modern Medicare Agency is here to take the weight off your shoulders. We don’t just look at one or two companies. We compare over 40 different carriers to find the specific plan that fits your life and your budget. Our process is designed to be simple and methodical. We start with a personalized 2026 plan review where we cross-reference your specific doctors and medications. You get a clear, side-by-side comparison of your best options without any high-pressure sales tactics. If you are ready for a clearer path, you can schedule your free, no-obligation Medicare consultation today to get started.

Your Advocate for 2026 and Beyond

Our commitment to you does not end when your application is submitted. Medicare rules change every single year, and your health needs can shift just as quickly. We take pride in being a long-term partner for our clients. This includes performing Medicare Part D reviews every year to ensure your drug coverage remains the most cost-effective option available. Whether you are navigating the local networks in Melville or managing coverage across state lines, we handle the claims issues and network changes so you don’t have to. We are proud to serve as your calm, patient guide through every twist and turn of this complex system.

Secure Your 2026 Peace of Mind Today

Your health and financial security in 2026 are too important to leave to chance or a confusing website. You’ve seen how the new drug cost caps and shifting plan structures have made the system more complex than ever before. The final decision of whether you should I use a medicare broker or enroll myself really comes down to how much you value your own time and certainty. Choosing a plan is just the start. Having a dedicated advocate who stands by you when a claim is questioned or a provider network changes is what provides true peace of mind.

Paul Barrett and his expert team are licensed in 34+ states and represent over 40 carriers to give you an unbiased, wide-reaching perspective. We’re here to provide the year-round support you deserve at no cost to you. Get your free 2026 Medicare plan comparison from a trusted independent broker and step into the new year with total confidence. We’re ready to help you navigate this journey with ease and clarity. You don’t have to face these changes alone; we’re here to protect your health and your budget every step of the way.

Frequently Asked Questions

Is it truly free to use a Medicare broker in 2026?

Yes, it is completely free for you. Brokers receive compensation directly from the insurance carriers they represent. CMS strictly regulates these commissions to ensure you receive the same price whether you work with an expert or go it alone. This allows you to get professional guidance without any added financial burden.

Will a broker show me every plan available in my zip code?

Most independent brokers represent a vast majority of the market, though they might not have every single niche plan. By law in 2026, brokers must tell you if they don’t offer every plan in your area. However, an independent broker representing 40+ carriers gives you a much broader view than a captive agent who only shows one brand.

Can I change my mind after enrolling through a broker?

You can certainly change your mind, provided you are within a valid enrollment period. For example, the Medicare Advantage Open Enrollment Period runs from January 1 to March 31 in 2026. If you’re asking “should I use a medicare broker or enroll myself,” remember that a broker can help you navigate these specific windows if you realize a plan isn’t the right fit.

Does a broker make my monthly premiums more expensive?

No, a broker never adds a penny to your monthly premium. Insurance companies set the rates, and those rates are filed with the government. Whether you enroll on the official Medicare website or through a professional advocate, the cost of the plan remains exactly the same for you.

What is the difference between a Medicare broker and a SHIP counselor?

SHIP counselors are volunteers who offer general education and cannot recommend specific plans. Medicare brokers are licensed professionals who can perform deep research into your medications and doctors. Brokers also provide year-round support, whereas SHIP volunteers generally only provide information during the initial decision-making process.

Why should I use a local broker instead of a national 1-800 number?

Local brokers understand the specific doctor networks and hospital reputations in your community. A national call center agent might not know that a certain local specialist just left a network. Using a local expert ensures your plan works at the pharmacy and clinic you already visit every month.

Can a broker help me with both Medigap and Medicare Advantage?

Yes, an independent broker can help you compare both Medicare Supplement and Medicare Advantage plans. They can explain the trade-offs between the higher monthly premiums of Medigap and the lower premiums of Advantage plans. This helps you decide if you should I use a medicare broker or enroll myself based on your specific health budget.

What happens to my broker if I move to a different state in 2026?

If you move, your broker can often continue to serve you if they are licensed in your new state. Paul Barrett and his team are licensed in over 34 states, including NY, FL, and CA. If you move to a state where they aren’t licensed, they will help you find a trusted professional so your coverage doesn’t skip a beat.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com