When it comes to Medicare, one of the biggest head-scratchers is Medicare Supplements — also called Medigap plans. I can’t tell you how many times I hear things like, “I thought Plan G was better with Company A than Company B,” or “I can just switch anytime, right?”

Here’s the real story: Medicare Supplements are actually one of the most straightforward and reliable parts of Medicare — but only if you know how they work. So, let’s pull back the curtain together.

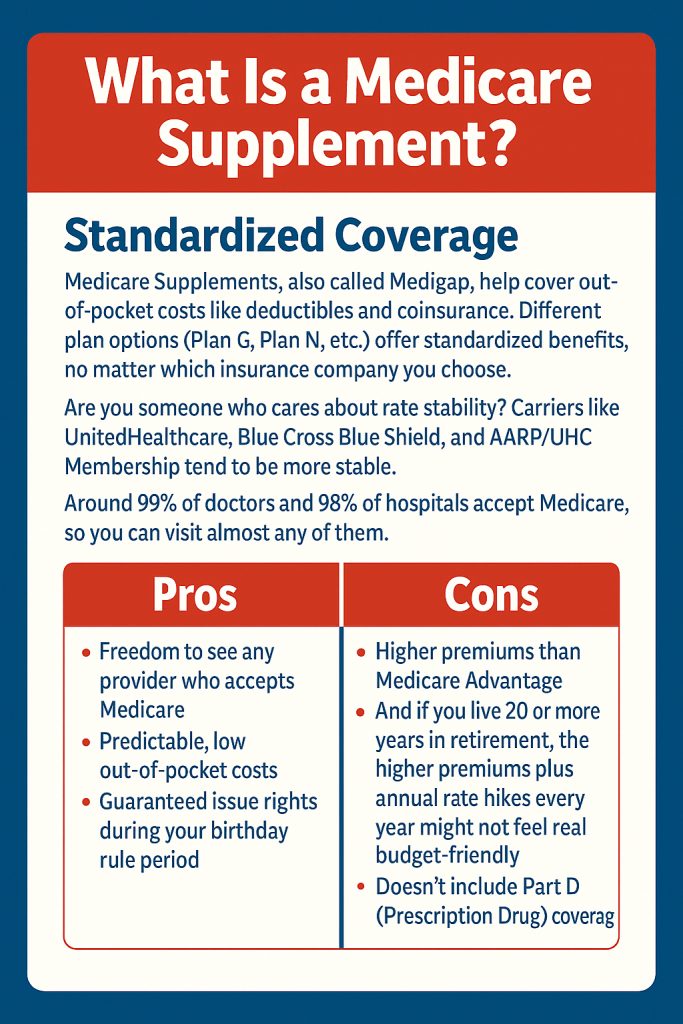

What a Medicare Supplement Really Is

Think of a Medicare Supplement as a safety net for your wallet. It works hand-in-hand with Original Medicare (Parts A & B) to cover the gaps: deductibles, copays, and coinsurance.

The #1 reason people love Medigap? Freedom. If a doctor takes Medicare, you’re in. Period. No networks, no referrals, no “is this hospital covered?” headache.

How big is that network?

- About 98% of U.S. doctors : accept Medicare.

- Nearly 9 out of 10 doctors : are still taking new Medicare patients.

- Over 4,600 hospitalsnationwide are Medicare-certified.

- Medicare/Medicaid account for roughly two-thirds of all U.S. hospital discharges.

Translation: with a Supplement, you can go almost anywhere. That’s peace of mind.

Standardized Coverage: Same Benefits, Different Price Tags

Here’s the part most people don’t realize. Every Medigap plan is standardized by the federal government. A Plan G is a Plan G. That means the coverage is identical no matter what company sells it.

So why do prices vary so much? Because what you’re really shopping for is the price and stability of the company. Some charge $120 a month, others $180 — for the exact same benefits. Of course, if you’re in New York, expect those premiums to be closer to double due to state rules on community rating and guaranteed acceptance.

Let’s talk stability. Carriers set premiums in one of three ways:

- Community-Rated:Everyone pays the same, regardless of age.

- Issue-Age-Rated: Your premium is based on the age you were when you signed up. Younger = cheaper, and it stays that way.

- Attained-Age-Rated:Starts lower, but climbs as you age. (This is the most common method.)

And yes — rates go up. In fact, the average Medigap increase in 2024 was 7.8%, compared to a long-term average closer to 3.8% a year. Larger carriers with more policyholders, like UnitedHealthcare or Blue Cross Blue Shield, can sometimes smooth out those bumps, but no company is immune.

Quick tip to protect yourself: Before you sign, ask:

- Is this plan community, issue-age, or attained-age rated?

- What have the last 3–5 years of rate increases been in my ZIP code?

A year with no increase is a unicorn. Don’t expect it.

The Medical Underwriting Puzzle

Here’s where a lot of folks get burned. When you first sign up for Medicare Part B, you get a six-month Medigap Open Enrollment Period. In that window, you can choose any Medigap plan, from any company, with no health questions asked.

After that? You may have to pass medical underwriting to switch. That means answering health questions, and yes, you can be denied or charged more.

This is why many people stay locked into an overpriced plan — they didn’t realize switching later might require approval.

Birthday & Anniversary Rules: Special Shortcuts

The good news? Some states have rules that give you a “get out of underwriting free” card:

- Birthday Rule (CA, OR, ID, NV, IL, LA, OK): Around your birthday, you get a window (30–90 days) to switch to a plan of equal or lesser benefits without underwriting.

- Missouri’s Anniversary Rule: During your Medigap policy anniversary month, you can swap carriers for the same plan letter — no health questions.

Not every state offers this, but if yours does, it’s worth knowing.

Why Prices Differ Between Companies

If coverage is identical, why the price gap? Because each company:

- Uses different rating systems.

- Files different rate increases with your state.

- Offers (or doesn’t offer) things like household discounts.

- Manages risk pools differently.

Bottom line: same Plan G, wildly different cost. I’ve helped clients save $1,000+ a year by simply switching carriers for the exact same benefits.

The Pros and Cons of Medicare Supplements

Pros:

- Go anywhere Medicare is accepted (98% of doctors, 4,600+ hospitals).

- Predictable, low out-of-pocket costs.

- No network stress, no referrals.

Cons:

- Higher monthly premiums compared to Medicare Advantage.

- Doesn’t cover extras like dental, vision, or prescriptions (Part D sold separately).

- The long game is expensive. That $164/month Plan G? Over 20–25 years, after annual rate hikes, it could cost:

- $57k–80k at a modest 3.8% increase.

- $72k–108k at 6%.

- $88k–140k at 7.8%.

It’s not a deal-breaker — many gladly pay for the predictability and freedom. But you deserve to know the math.

The Bottom Line

Medicare Supplements can bring incredible peace of mind in retirement. But they come with rules, costs, and fine print most people never hear about.

Remember:

- Remember:

- All Plan G’s (or N’s, or F’s) are the same.

- Underwriting matters once your initial window closes.

- Rates go up — always.

- Some states give you a second chance with Birthday or Anniversary Rules.

Confused? Overpaying? Just want the truth without the sales pitch? That’s what I’m here for.

Call me at 631-358-5793

I’ll help you cut through the noise, compare your options, and walk away feeling confident. Because Medicare is complicated enough — your Supplement doesn’t have to be.