What if you could lower your monthly expenses in 2026 without cutting back on the things you love? Many people see commercials promising extra money in their Social Security checks and wonder if it’s just another gimmick. You might be asking, what is the medicare part b give back benefit, and is it a legitimate way to save? With the standard Part B premium sitting at $202.90 this year, it’s completely natural to look for some breathing room in your budget.

We agree that the rising cost of living makes every dollar count, and the confusion surrounding these plans only adds to the stress. This guide will show you exactly how these premium reductions work so you can decide if they fit your specific health needs. We’ll walk through the trade-offs you should watch for and how to identify a plan that offers real security. By the end, you’ll feel confident choosing a plan that puts money back in your check while keeping your healthcare protected.

Key Takeaways

- Understand exactly what is the medicare part b give back benefit and how it can help lower your 2026 monthly expenses.

- Check your eligibility to ensure you’re able to receive this premium reduction in your Social Security check.

- Learn how to spot the trade-offs so you don’t end up paying more in doctor copays than you save on premiums.

- Discover how we look at over 40 different carriers to find the specific plan that fits your unique health needs.

Understanding the Medicare Part B Give Back Benefit in 2026

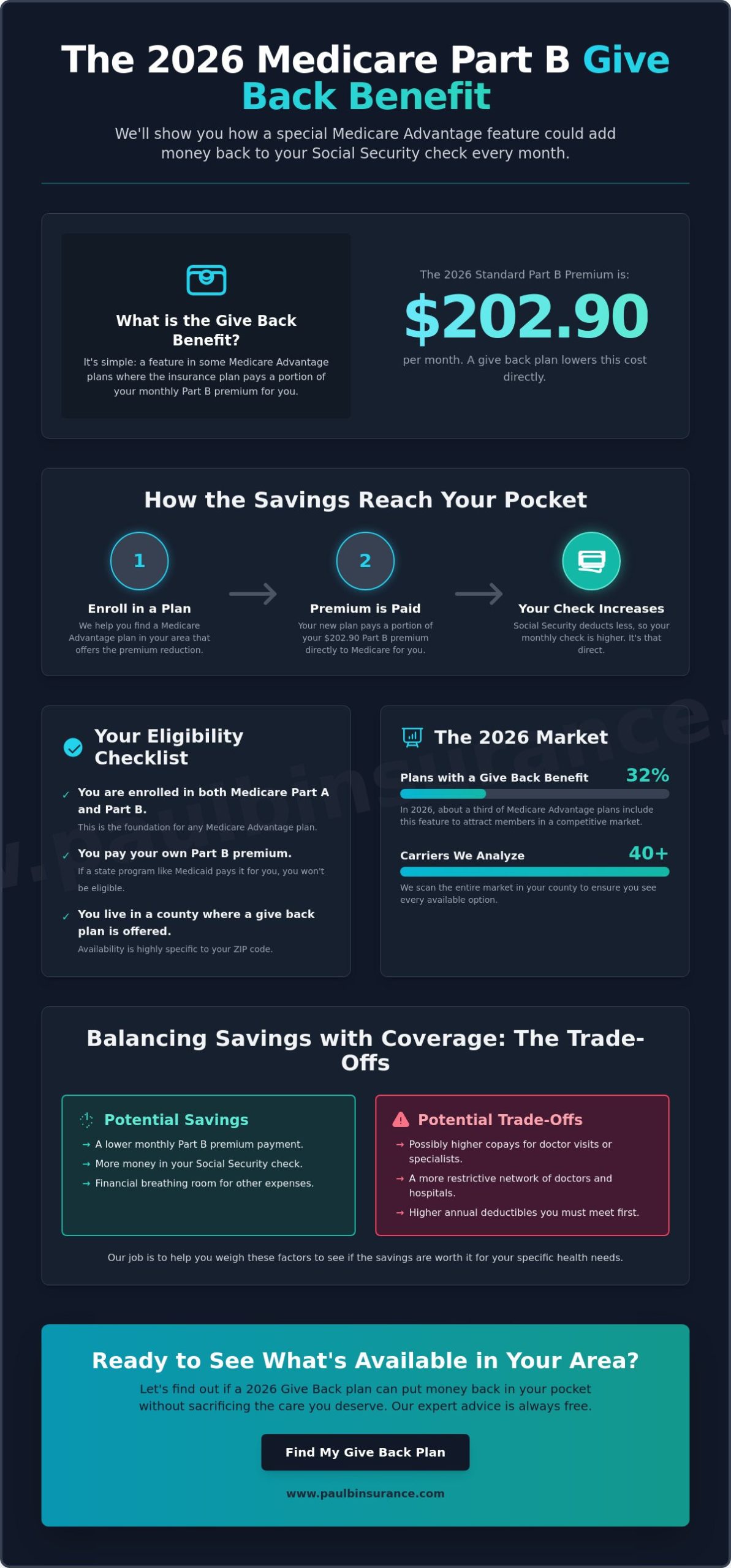

Many people ask us, what is the medicare part b give back benefit, especially when they see ads promising “extra money” in their Social Security check. We understand that these claims can feel confusing or even too good to be true. Simply put, this benefit is a feature found in certain Medicare Advantage plans where the insurance carrier pays a portion of your monthly Medicare Part B premium for you. In 2026, the standard Part B premium has reached $202.90. For many of our neighbors living on a fixed income, that is a significant monthly expense. Reducing that cost can provide a much-needed financial cushion during a time when the cost of living continues to rise.

You might hear this benefit called by a few different names, such as a “Part B Premium Reduction” or even a “Social Security Giveback.” Regardless of the name used in a brochure, the core concept remains the same: it’s a way to lower your out-of-pocket healthcare costs. We often describe this as a potential win-win for those on a strict budget. It allows you to keep more of your hard-earned money while still maintaining the comprehensive coverage you need to stay healthy. Our mission is to help you find that balance without the typical stress of navigating insurance alone.

How the Give Back Appears in Your Budget

The benefit is defined as a contractual reduction of your Part B obligation. It doesn’t arrive as a separate check in the mail; instead, it changes how much you pay at the source. If you’re already receiving Social Security benefits, the “give back” usually shows up as a direct increase in your monthly check. This happens because the government simply deducts less for your Part B premium. If you aren’t on Social Security yet and pay Medicare directly, your monthly or quarterly bill will be lower. It’s a straightforward way to see a positive change in your household budget every single month, helping you feel more in control of your finances.

Why Insurance Companies Offer This Benefit

You might wonder why a private company would offer to pay your premium. It’s not magic; it’s based on how the Medicare system is funded. Carriers receive rebates from the government when they manage care efficiently. They can then use these rebates to offer extra incentives to members. In 2026, the market is more competitive than ever. Research shows that roughly 32% of plans now include this feature to attract new members. We help you look past the flashy marketing to see the actual value of these offers. Our role is to ensure you don’t sacrifice essential coverage or access to your favorite doctors just to save a few dollars on your premium. You can explore more about these options in our Medicare Advantage guide. We’re here to make sure you have the clarity and peace of mind you deserve.

Eligibility and How the Premium Reduction Works

Understanding who qualifies for this reduction is the next step in your journey toward lower monthly costs. While the idea of getting money back sounds simple, there are specific rules you need to follow to participate. First, you must be enrolled in both Medicare Part A and Part B. This is because the benefit is tied directly to your Part B premium. Second, you must be the one responsible for paying that premium. If you receive state assistance like Medicaid that already covers your costs, you won’t be eligible for this specific feature. We often see neighbors get frustrated when they realize they can’t double dip on these savings, so we want to be clear about that from the start. You can find more details in this Medicare Giveback Benefit Explained article, which highlights how these rules protect the system’s integrity.

Determining what is the medicare part b give back benefit for your specific situation starts with your home address. You must choose a Medicare Advantage plan that specifically includes this reduction feature. It isn’t a standard part of every plan, so you have to look for it during your search. If you’re feeling overwhelmed by the hundreds of options for 2026, you can always reach out to us for a quick chat to see what is available in your neighborhood.

The Role of Your Zip Code

Location is one of the biggest factors in whether you can access these savings. A plan available to someone in Melville, NY, might offer a significant give back, while a plan just across a state line might not offer one at all. These benefits are determined at the county level. We use our specialized database to scan every available plan in your specific county to ensure you don’t miss out. It’s also vital to remember that plan details can change every year. The options you see during the annual Medicare enrollment period might be different from what was available last year. We stay on top of these changes so you don’t have to worry about the details.

Timeline: When Will You See the Money?

Once you’ve selected a plan, you might expect to see the change immediately, but it takes a little patience. There is usually a one to three month delay while the Social Security Administration processes the update. If you switch plans in January, your first check of the year might still show the old deduction. This is normal. The reduction will eventually kick in and often includes a catch up payment for the months you missed. If your give back doesn’t appear by the end of the third month, we recommend checking your plan’s Summary of Benefits or giving us a call. We’re here to help you track down those answers and ensure you’re getting exactly what was promised. Understanding what is the medicare part b give back benefit means knowing that the wheels of government move slowly, but the savings are real.

Evaluating the Trade-offs: Is a Give Back Plan Right for You?

We know that seeing an extra $50 or $77 in your monthly Social Security check feels like a major victory. However, it’s vital to look at the whole picture to understand what is the medicare part b give back benefit in terms of total value. Insurance companies have a set budget for your care. If they choose to use those funds to pay your Part B premium, they often have to adjust other parts of the plan to balance the books. This can lead to what we call ‘hidden costs’ that aren’t always obvious when you first see the advertisement.

One common trade-off is higher copays for routine doctor visits or specialist consultations. You might also find that the Maximum Out-of-Pocket (MOOP) limit is higher on these plans. For example, a standard plan in 2026 might cap your yearly spending at $4,500, while a give back plan in the same area might set that cap at $6,500. If you have a significant health event, like a hospital stay, that $50 monthly saving could be quickly overshadowed by a $500 higher hospital copay. We always encourage you to check your specific prescriptions in the plan’s drug formulary as well. Some give back plans might have different coverage levels for the medications you take every day.

Rebate vs. Richer Benefits

We often help clients decide between a premium rebate and richer medical benefits. For some, having lower copays for dental or vision care is more valuable than a monthly check. It’s also helpful to see how these plans compare to Medicare Supplement Insurance, which works differently by covering your cost-sharing gaps rather than giving a rebate. We focus on the ‘Total Cost of Care.’ This means looking at your premium savings alongside your potential medical bills to find the true winner for your wallet. If a plan saves you $600 a year in premiums but costs you $800 more in dental work, it isn’t actually saving you money.

Who Benefits the Most?

Who is the ideal candidate for these plans? They usually work best for individuals who rarely visit the doctor and want to maximize their monthly cash flow. We generally find these plans are a good fit for:

- Healthy seniors who only go to the doctor for annual wellness visits.

- Individuals who have a strong emergency fund to cover a higher MOOP if needed.

- Those who prioritize having more liquid cash in their Social Security check each month to cover daily expenses.

On the other hand, if you manage chronic conditions or visit specialists frequently, a standard plan might be a safer choice. We help you run a ‘stress test’ on any plan you are considering. We look at your medical usage from last year and calculate if you would have come out ahead or behind with the give back feature. Knowing what is the medicare part b give back benefit requires looking at the math, not just the marketing. Our goal is to move you from a state of uncertainty to one of total clarity about your coverage.

How to Find and Compare Give Back Plans in 2026

Finding the right plan shouldn’t feel like a part-time job. While the official Medicare Plan Finder is a helpful public tool, it often lacks the nuance needed to see the full picture of your healthcare costs. We use our own specialized tools to filter through dozens of carriers at once, saving you the stress of manual searching. When you are looking at a specific option, you need to find the document called the Summary of Benefits. This is where the plan must clearly state what is the medicare part b give back benefit in actual dollars. It is usually listed under a section called Part B Premium Buy-Down or Premium Reduction.

To see the real details, you should also ask for the Evidence of Coverage. This is a much longer document, but it contains the fine print about how and when the reduction applies to your Social Security check. We also want to warn you about cold calls. Ethical professionals don’t call you out of the blue to push a specific plan. If a stranger calls you promising free money, please be careful. It is always safer to do your own research or work with an advocate you trust who can show you all your options side by side.

Step-by-Step Comparison Strategy

We suggest a simple three-step approach to keep your search organized and logical. First, check your doctors. A give back is useless if your primary physician or specialist isn’t in the plan’s network. Second, check your medications. You can read more about how this works in our guide to Medicare Part D. Third, calculate your annual Net Benefit. Take the monthly give back amount and multiply it by 12. Then, subtract your estimated annual copays for visits and prescriptions. If the number is still positive, the plan might be a winner. If you’d like a hand with this math, you can compare 2026 plans with us to find your best fit.

Common Marketing Scams to Avoid

Television ads in 2026 often use high-pressure tactics to get your attention. You might see celebrities promising $200 back every month. While the standard Part B premium is $202.90, getting the full amount back is very rare. These plans often come with extremely high medical costs in other areas. CMS rules for 2026 now restrict how these plans are advertised. Companies aren’t supposed to lead with the give back as the only reason to join. They must present a balanced view of the coverage. If an ad sounds like it’s only about the money, it’s probably leaving out the most important details about your healthcare. We are here to help you see through the noise and find the truth about what is the medicare part b give back benefit for your specific needs.

Why Working With an Independent Broker Makes the Difference

Finding the right health plan shouldn’t feel like a solo mission through a maze. When you speak with a “captive” agent, you’re only seeing one side of the story because they only represent a single insurance company. We do things differently. We compare over 40 carriers to give you a complete, honest view of the 2026 market. This unbiased approach is essential when you’re trying to understand what is the medicare part b give back benefit and how it varies between different companies. We don’t have a favorite plan. Our only goal is to find the one that fits your life perfectly and protects your hard-earned savings.

Our support doesn’t stop once you sign your enrollment forms. If your plan changes its rules or the give back amount next year, we’ll be right here to help you adjust and find a better fit if needed. This year-round commitment is how we move you from a state of confusion to one of absolute certainty. You deserve to feel like you have a dedicated advocate in your corner. We take pride in being the champion of the consumer, ensuring you’re never pushed into a plan that doesn’t serve your best interests.

The Advantage of Choice

We often find “hidden” give back plans that don’t spend millions of dollars on flashy television ads. These smaller plans sometimes offer the best value because they focus their budget on member benefits instead of celebrity endorsements. You can explore a broader view of these options in our Medicare Advantage Plans: A Simple Guide. Best of all, our service comes at no cost to you. The insurance carriers pay us for our expertise, so you get professional guidance without adding another bill to your monthly budget. It’s a simple, ethical way to ensure you’re seeing every option available in your specific county.

Ready for a Clear Path Forward?

Starting your journey to better coverage is a straightforward process. We recommend having a list of your current doctors and medications ready before we talk. This allows us to run a precise check against every plan available in 2026. We’ll look at the provider networks, the drug costs, and exactly what is the medicare part b give back benefit for each specific option. We’ll help you weigh the premium savings against the potential out-of-pocket costs we discussed earlier. When you’re ready to move forward with confidence, let’s find the right plan for your budget and your health together. We’re here to be your guide every step of the way.

Take the Next Step Toward Financial Certainty

You now have the tools to understand exactly what is the medicare part b give back benefit and how it impacts your monthly budget in 2026. We’ve explored how these plans can lower your Part B costs while also highlighting the critical trade-offs you must consider, such as out-of-pocket maximums and doctor networks. Saving money on your premium is a wonderful goal, but protecting your access to quality care remains the top priority. You deserve a plan that balances both your health needs and your wallet without the typical stress of insurance shopping.

You don’t have to navigate these complex choices alone. We compare over 40 carriers and are licensed in 34+ states to provide you with truly independent, unbiased guidance. Since our inception, we’ve focused on moving our neighbors from a place of stress to a state of total confidence. Schedule your free 2026 Medicare plan review with a trusted expert today. We are ready to help you find the security and peace of mind you deserve for the years ahead. You’ve worked hard for your benefits, and we’re here to help you protect them.

Frequently Asked Questions

Is the Medicare Part B Give Back benefit a scam?

No, this benefit is a legitimate insurance feature. It’s a contractual reduction of your Part B premium obligation offered by private companies. We know the flashy TV ads can feel suspicious or even predatory. While the benefit is real, you must be careful about the trade-offs. It’s a legal way to lower your costs, but you should always verify the plan details with a trusted advocate to ensure you don’t lose important coverage.

How much money can I actually get back in 2026?

In 2026, the amount can range from $0.10 to the full premium of $202.90 per month. Most people don’t receive the full amount. In recent years, the average benefit was approximately $77 each month. The exact figure depends on the specific plan and your zip code. We help you look at the official Summary of Benefits for each plan to find the precise dollar amount available in your local area.

Do I have to be on Social Security to get the give back?

You don’t need to be receiving Social Security checks to qualify for this reduction. If your premium is normally deducted from your monthly check, the deduction simply becomes smaller. If you pay Medicare directly through a bill, your monthly or quarterly statement will show a lower balance. Either way, the savings stay in your pocket. It’s a flexible benefit that applies regardless of how you handle your monthly Medicare payments.

Will I lose my current doctors if I switch to a give back plan?

You might lose access to your current doctors if they aren’t in the new plan’s network. Give back plans are a type of Medicare Advantage plan, which means they use specific groups of providers. We always recommend checking the plan’s directory before you make any changes. We can help you verify if your favorite physicians and hospitals are included so you don’t have to sacrifice your care for a lower premium.

Can I get a give back if I have a Medicare Supplement (Medigap) plan?

No, you cannot get this benefit with a Medigap plan. When asking what is the medicare part b give back benefit, it’s important to remember it’s exclusive to Medicare Advantage. Medigap plans focus on covering your out-of-pocket costs like deductibles and coinsurance. You have to choose between the predictable costs of a Supplement plan or the monthly premium reduction offered by certain Advantage plans. We can help you compare these two paths.

What happens to my give back if I move to a different zip code?

Your benefit will likely change or disappear if you move. These plans are tied to specific counties. If you move to a new area, you’ll need to join a plan available in that specific location. Some counties have dozens of give back options, while others have none at all. Moving usually triggers a Special Enrollment Period, giving you the chance to find a new plan that fits your new neighborhood.

Is the give back benefit available in every state?

No, these plans aren’t available in every state or every county. While the number of plans offering this feature has grown to about 32% recently, availability depends on the private insurers in your area. Some regions have very competitive markets with many options, while others are more limited. We can scan your specific zip code to see exactly what is offered in your part of the country for 2026.

How does the give back affect my taxes?

Generally, this reduction isn’t considered taxable income. It’s a lower cost for your insurance premium rather than a direct payment or prize. Because it’s technically a “buy-down” of an expense, it doesn’t usually count toward your adjusted gross income. However, every financial situation is unique. We always suggest you speak with a qualified tax professional to be absolutely certain about how what is the medicare part b give back benefit might impact your personal tax return.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com