Medicare does not cover routine dental care, vision exams, hearing aids, long-term custodial care, or most outpatient prescription drugs under Original Medicare Parts A and B. These are not minor gaps. They represent the healthcare services most people over 65 actually need and use. The Centers for Medicare and Medicaid Services (CMS) governs Medicare under a “reasonable and necessary” standard that excludes entire benefit categories regardless of medical need. AARP reports that 1 in 5 adults of Medicare age faced over $2,000 in out-of-pocket costs annually from services Original Medicare simply will not pay for. That number should reset your expectations before you turn 65.

What Medicare does not cover: the major exclusions

Understanding the full list of medicare exclusions is the first step to protecting your finances. Original Medicare was built as a base insurance program, not a comprehensive safety net. These are the categories where it falls short:

-

Routine dental care: Medicare does not cover routine dental exams, cleanings, fillings, dentures, or tooth extractions. A single set of dentures can cost $1,500 to $3,000 out of pocket. Medicare only covers dental work that is directly tied to a covered medical procedure, such as jaw reconstruction after an accident.

-

Routine vision care: Eye exams for glasses or contact lenses are not covered. Eyeglasses and contacts are not covered either. Medicare Part B does cover one annual eye exam for diabetic retinopathy and cataract surgery, but standard vision correction falls entirely outside the program.

-

Hearing aids and exams: Hearing aids are among the most expensive non-covered items, often running $3,000 to $7,000 per pair. Routine hearing exams to fit or adjust those aids are also excluded. Medicare covers diagnostic hearing tests only when a physician orders them to evaluate a medical condition.

-

Long-term custodial care: This is the exclusion that surprises people most. Medicare does not pay for help with daily activities such as bathing, dressing, or eating in a nursing home or at home. That is custodial care. Medicare only covers skilled nursing facility care for up to 100 days per benefit period, and only after a qualifying 3-day inpatient hospital stay.

-

Most outpatient prescription drugs: Original Medicare Parts A and B do not cover drugs you take at home. Medicare Part D is a separate, standalone plan that covers outpatient prescriptions. Without it, you pay full retail price.

-

Cosmetic surgery: Procedures performed for appearance rather than medical necessity are excluded under CMS rules. Reconstructive surgery following a covered medical event, such as a mastectomy, is a different matter and may be covered.

-

Most alternative medicine: Medicare covers chiropractic care only for manual spinal manipulation to correct a subluxation. It does not cover chiropractic X-rays, diagnostic exams, or maintenance therapy visits. Acupuncture is covered only for chronic lower back pain under specific conditions. Naturopathy, massage therapy, and homeopathy are not covered at all.

How do Medicare coverage gaps affect your out-of-pocket costs?

The financial impact of medicare coverage gaps is not theoretical. Original Medicare has no annual out-of-pocket maximum. That means if you need repeated hospitalizations or ongoing Part B services, your liability has no ceiling. A Medigap policy addresses some of that exposure, but Medigap does not cover routine dental, vision, or hearing services. Those gaps remain open regardless of which supplement plan you hold.

Consider a realistic scenario: a 67-year-old needs two hearing aids, a dental crown, and new eyeglasses in a single year. That combination could easily exceed $6,000 in costs that neither Original Medicare nor a Medigap plan will touch. Multiply that across a retirement that may last 20 or 30 years, and the cumulative exposure is significant.

The 3-day inpatient hospital stay rule for skilled nursing facility coverage catches many beneficiaries off guard. If your hospital stay is classified as “observation status” rather than inpatient admission, those days do not count toward the 3-day requirement. You can spend four nights in a hospital bed and still receive no skilled nursing coverage because of how the stay was coded. This distinction costs some beneficiaries thousands of dollars.

Pro Tip: Ask your hospital billing department directly whether you are admitted as an inpatient or under observation status. You have the right to know, and the answer changes your Medicare coverage entirely.

Medicare Advantage plans cap annual out-of-pocket costs, which Original Medicare does not. In 2026, the maximum out-of-pocket limit for Medicare Advantage plans is set by CMS. That ceiling provides a financial floor that Original Medicare simply cannot offer on its own.

Original Medicare vs. Medicare Advantage: how do they compare on coverage gaps?

The choice between Original Medicare and Medicare Advantage is largely a decision about how you want to manage the services not covered by medicare. Here is a direct comparison:

| Feature | Original Medicare | Medicare Advantage |

|---|---|---|

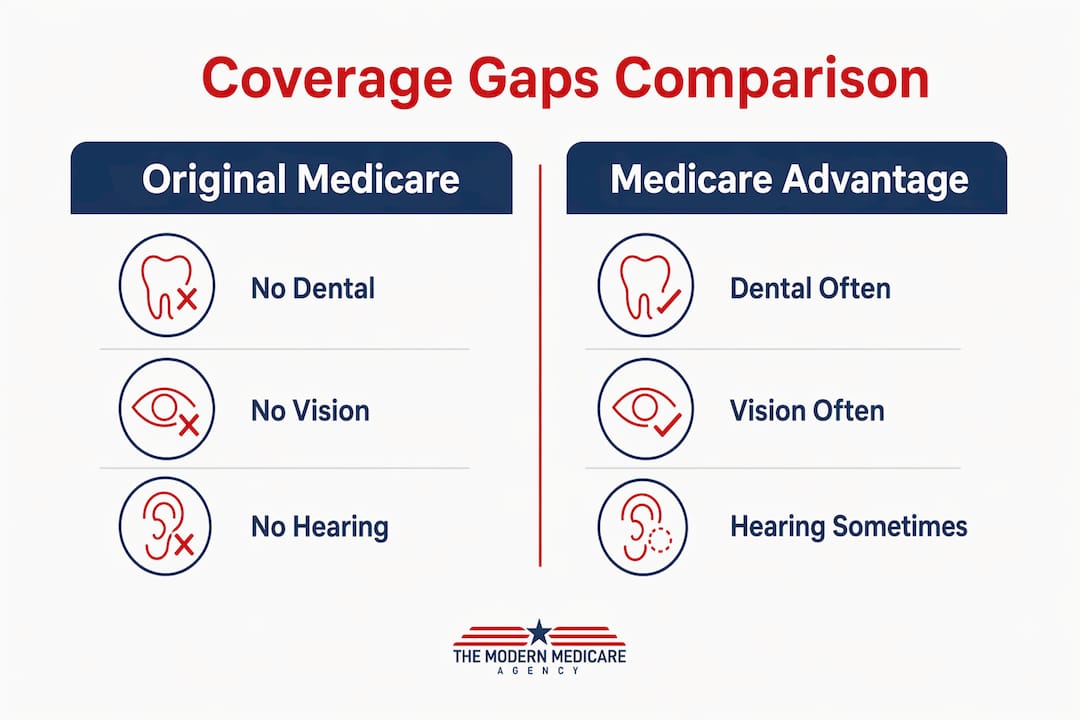

| Routine dental coverage | Not covered | Often included as supplemental benefit |

| Routine vision coverage | Not covered | Often included as supplemental benefit |

| Hearing aids | Not covered | Sometimes included, with limits |

| Out-of-pocket maximum | None | Annual cap set by CMS |

| Provider network | Any Medicare-accepting provider | Restricted network (HMO or PPO) |

| Prior authorization | Rarely required | Commonly required for specialist care |

| Prescription drugs | Requires separate Part D plan | Usually bundled (MAPD plans) |

Medicare Advantage plans are offered by private insurers and may include supplemental benefits like routine dental and vision care. That sounds like the obvious solution to Medicare’s exclusions. The trade-off is real, though. These plans typically restrict you to a defined provider network, and prior authorization requirements can delay or deny care that Original Medicare would cover without question.

The supplemental dental and vision benefits in Medicare Advantage plans are also not unlimited. A plan might cover $1,000 per year in dental benefits, which covers a cleaning and an X-ray but falls short of a crown or implant. Reading the Evidence of Coverage document before enrolling tells you exactly what the plan pays and what it does not. The pros and cons of Medicare Advantage depend heavily on your specific health needs and how often you use specialists.

What strategies can you use to cover what Medicare does not pay for?

Closing the gaps in Medicare coverage requires a deliberate plan built around your actual health needs. These are the most effective approaches:

-

Buy a Medicare Supplement (Medigap) policy. Medigap plans sold by private insurers cover costs like Part A and Part B coinsurance, hospital deductibles, and excess charges. Plan G is currently the most popular option for new enrollees. Medigap does not cover dental, vision, or hearing, but it eliminates most of the financial unpredictability in Original Medicare.

-

Add a standalone Part D plan. If you choose Original Medicare plus Medigap, you need a separate Part D prescription drug plan for outpatient medications. Skipping Part D when you are first eligible triggers a permanent late enrollment penalty, even if you take no drugs today.

-

Purchase long-term care insurance. Medicare’s exclusion of custodial care is one of the most expensive gaps in the program. Long-term care insurance covers nursing home stays, assisted living, and in-home personal care. Premiums are significantly lower when you buy before age 60, making pre-retirement planning the right time to act.

-

Use a Health Savings Account (HSA) before you enroll. If you are still on a high-deductible employer plan before turning 65, contribute the maximum to your HSA. Once you enroll in Medicare, you can no longer contribute, but you can spend existing HSA funds tax-free on Medicare premiums, dental care, vision, hearing aids, and long-term care insurance premiums.

-

Consider a Medicare Advantage plan for bundled supplemental benefits. If your priority is dental and vision coverage and you are comfortable with a provider network, a Medicare Advantage plan may deliver more value than Original Medicare plus separate supplemental policies. Compare total annual costs, not just premiums.

Pro Tip: Do not wait until you are sick to review your coverage. The best time to evaluate Medigap versus Medicare Advantage is before you turn 65, when Medigap guaranteed issue rights protect you from medical underwriting.

What I’ve learned after nearly two decades helping people navigate Medicare gaps

Most people I talk to at Paulbinsurance arrive with the same assumption: Medicare is like the employer coverage they are leaving. It is not. Employer plans are designed to be comprehensive. Medicare was designed in 1965 as a hospital and physician insurance program. The world has changed. The program has not kept pace with what people actually need.

The exclusion that causes the most financial harm in my experience is not dental or vision. It is the skilled nursing facility rule. I have seen families blindsided by a $10,000 bill because a loved one spent four days in the hospital under observation status and did not qualify for skilled nursing coverage. That distinction between inpatient and observation is buried in the fine print, and hospitals are not always proactive about explaining it.

My honest advice: treat Medicare as a foundation, not a finish line. Original Medicare covers serious acute care well. It covers the rest poorly. The gap between what Medicare covers and what you actually need in retirement is real, and it is measurable. Build your supplemental coverage around your specific health history, your preferred doctors, and your realistic budget. Review your plan every year during Annual Enrollment, because plan benefits and costs change. The people who do that work upfront are the ones who avoid the expensive surprises.

— Paul

How Medicare Supplement plans can help you fill the gaps

Understanding what Medicare does not cover is only half the equation. The other half is knowing how to protect yourself from those costs.

At Paulbinsurance, we work with individuals approaching Medicare eligibility every day to build coverage that actually fits their lives. A Medicare Supplement plan eliminates most of the financial unpredictability in Original Medicare by covering coinsurance, deductibles, and hospital costs that would otherwise come out of your pocket. Our independent agents compare plans across multiple carriers to find the right fit for your health needs and budget. If you want a clear picture of your options before you enroll, we are here to help you get it right the first time.

FAQ

Does Medicare cover routine dental care?

Medicare does not cover routine dental exams, cleanings, fillings, or dentures under Original Medicare Parts A and B. Some Medicare Advantage plans include limited dental benefits, but coverage amounts vary widely by plan.

What is the skilled nursing facility rule under Medicare?

Medicare covers skilled nursing facility care for up to 100 days per benefit period, but only after a qualifying 3-day inpatient hospital stay. Time spent under observation status does not count toward that 3-day requirement.

Does Medicare cover hearing aids?

Original Medicare does not cover hearing aids or the routine exams needed to fit them. Some Medicare Advantage plans offer hearing aid benefits, though coverage limits typically apply.

What does Medicare not pay for regarding prescription drugs?

Original Medicare Parts A and B do not cover most outpatient prescription drugs. A standalone Medicare Part D plan is required to get outpatient drug coverage, and skipping it at initial eligibility triggers a permanent late enrollment penalty.

Can Medigap cover all of Medicare’s gaps?

Medigap policies cover costs like coinsurance, deductibles, and hospital charges but do not cover routine dental, vision, or hearing services. Those services require separate insurance or a Medicare Advantage plan with supplemental benefits.

Key takeaways

Medicare’s most consequential exclusions are routine dental, vision, hearing, long-term custodial care, and outpatient prescription drugs, and none of these gaps are closed by Original Medicare alone.

| Point | Details |

|---|---|

| Dental, vision, hearing excluded | Original Medicare covers none of these routine services; separate coverage is required. |

| No out-of-pocket maximum | Original Medicare has no annual spending cap, creating unlimited financial liability without a supplement. |

| Skilled nursing facility rule | Coverage requires a 3-day inpatient stay; observation status does not qualify, catching many beneficiaries off guard. |

| Medigap fills financial gaps, not service gaps | Medigap covers coinsurance and deductibles but still leaves dental, vision, and hearing uncovered. |

| Plan before age 65 | HSAs, long-term care insurance, and Medigap guaranteed issue rights are most valuable before Medicare enrollment begins. |