Are you nearing 65 and trying to navigate the confusing maze of Medicare rules? Do you find yourself wondering if your work history is enough, or if a disability might qualify you early? You’re not alone. The fear of making a costly mistake or missing a critical deadline is a common stressor for many Americans. This feeling of uncertainty is exactly why we created this guide. The question of who is eligible for medicare shouldn’t be a source of anxiety, and with the right information, it doesn’t have to be.

We’re here to provide simple, clear answers. This guide is designed to cut through the jargon and give you the straightforward guidance you deserve. We will walk you through the different paths to eligibility-whether by age, through a disability, or due to specific health conditions. Our goal is to replace your confusion with confidence, giving you the peace of mind that comes from knowing exactly where you stand and how to prepare for your healthcare future.

Key Takeaways

- Discover the straightforward eligibility rules for U.S. citizens and legal residents turning 65.

- Learn how you may qualify for Medicare benefits before age 65 if a disability prevents you from working.

- Understand the special health conditions that can grant you immediate Medicare eligibility, bypassing standard waiting periods.

- Get a clear, simple answer to the question of who is eligible for medicare by understanding the three main pathways.

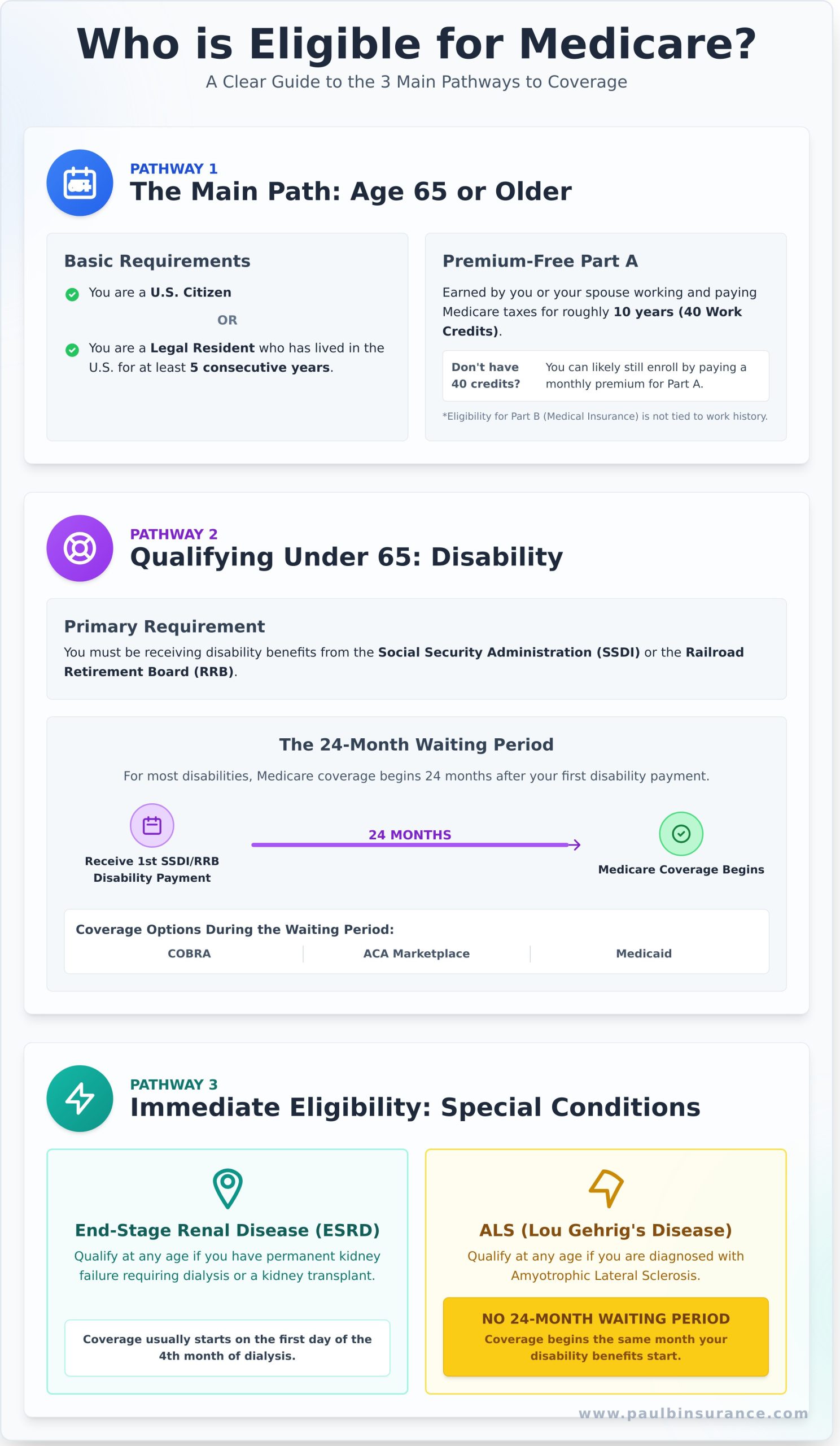

The Main Path to Medicare: Eligibility at Age 65 or Older

For most Americans, turning 65 is the key that unlocks Medicare eligibility. This is the most common path to enrollment, but understanding the specific rules is the first step toward gaining confidence in your coverage. Navigating the question of who is eligible for medicare can feel overwhelming, but we are here to provide simple, clear guidance. To qualify at age 65, you must first meet two basic residency requirements:

- You are a U.S. citizen, OR

- You are a legal resident who has lived in the United States for at least 5 consecutive years.

If you meet this standard, your eligibility generally begins on the first day of the month you turn 65. From there, your work history determines whether you will pay a monthly premium for certain parts of the coverage. For a complete Medicare Overview, it’s helpful to understand how these parts work together.

The 40-Credit Rule for Premium-Free Part A

Most people receive Medicare Part A (Hospital Insurance) without paying a monthly premium. This benefit is earned by working and paying Medicare taxes. To qualify for premium-free Part A, you or your spouse must have accumulated at least 40 work credits. This is roughly equal to 10 years of work. You earn credits based on your annual income; for example, in 2024, you receive one credit for every $1,730 in earnings, up to a maximum of four credits per year.

What if You Don’t Have 40 Work Credits?

If you don’t have the required 40 credits, please don’t worry-you can still get coverage. You will likely have the option to buy into Part A by paying a monthly premium. It’s important to know that your eligibility for Medicare Part B (Medical Insurance) is not tied to your work history. As long as you meet the age and residency requirements, you can enroll in Part B by paying the standard monthly premium.

Qualifying Through Your Spouse’s Work History

Many people who haven’t worked or have an insufficient work history can still get premium-free Part A. You may be eligible based on the work record of your current, divorced, or deceased spouse. If your spouse is at least 62 and has earned 40 or more credits, you can typically qualify. This is a crucial pathway that provides peace of mind, especially for spouses who stayed home to manage the household and raise a family.

Qualifying Under 65: Medicare Eligibility Through Disability

One of the most common questions The Modern Medicare Agency hears is, “Can I get Medicare before I’m 65?” The answer is yes, but this path is not based on age. It’s designed for individuals who are unable to work due to a significant medical condition or disability. This is a critical factor in understanding who is eligible for medicare beyond the standard age requirement.

If you have a disability, you may qualify for Medicare early. The primary pathway is through receiving disability benefits from either the Social Security Administration (SSDI) or the Railroad Retirement Board (RRB). However, simply receiving these benefits doesn’t grant you immediate Medicare coverage. There is a crucial waiting period involved, which can be a source of stress and confusion if you aren’t prepared for it.

The Social Security Disability Insurance (SSDI) Connection

Your journey to Medicare coverage under 65 begins with being approved for Social Security Disability Insurance (SSDI) benefits. Once you are approved, there is a mandatory 24-month waiting period before your Medicare eligibility begins. This clock starts from the month you receive your first disability payment, not from the date your disability began. According to the official Social Security Administration Medicare Eligibility guidelines, this two-year period is a firm requirement for most recipients.

Let’s use a simple example to make this clear: If your SSDI payments begin in January 2024, you will automatically be enrolled in Medicare Parts A and B starting in January 2026.

What Happens During the 24-Month Waiting Period?

We understand that a two-year gap in health coverage can feel overwhelming. Planning for this period is essential for your peace of mind and financial security. While you wait for your Medicare benefits to start, you may have other options to stay covered:

- COBRA: If you recently left a job, you might be able to continue your employer’s health plan for a limited time.

- Affordable Care Act (ACA) Marketplace: You can shop for an individual health plan through the official ACA Marketplace. You may qualify for subsidies to lower your monthly premium.

- Medicaid: Depending on your income and resources, you may be eligible for your state’s Medicaid program.

Once you complete the waiting period and your Medicare coverage begins, you’ll have important decisions to make. This is when you can explore your options beyond Original Medicare, such as Medicare Advantage plans, to find coverage that best fits your specific health needs.

Immediate Eligibility: Special Health Conditions (ESRD & ALS)

While most people think of Medicare as a health benefit for those 65 and older, there are critical exceptions for individuals facing specific, severe health challenges. Navigating a serious diagnosis is overwhelming enough without having to worry about healthcare coverage. Fortunately, Medicare has provisions for two conditions that allow you to enroll regardless of your age, providing a vital lifeline when you need it most. Understanding these exceptions is a key part of knowing who is eligible for medicare.

These special enrollment rules are designed to offer immediate support and peace of mind to individuals and their families during an incredibly difficult time. Let’s look at these two conditions and how they work.

Eligibility with End-Stage Renal Disease (ESRD)

End-Stage Renal Disease (ESRD) is a medical condition in which your kidneys have permanently failed, requiring you to receive regular dialysis or a kidney transplant to live. If you are diagnosed with ESRD, you can qualify for Medicare at any age, provided you or your spouse have paid Medicare taxes for a certain amount of time.

Typically, your Medicare coverage will begin on the first day of the fourth month of your dialysis treatments. However, it can start sooner in specific situations, such as if you are participating in a home dialysis training program. This ensures you get the care you need without a long, stressful wait.

Eligibility with Amyotrophic Lateral Sclerosis (ALS)

Amyotrophic Lateral Sclerosis (ALS), often known as Lou Gehrig’s disease, is a progressive neurodegenerative disease. For those with a diagnosis of ALS, the path to Medicare is immediate. You become eligible for Medicare coverage the very same month your Social Security Disability Insurance (SSDI) benefits begin.

This is a crucial distinction: There is no 24-month waiting period for individuals with ALS. This immediate eligibility provides fast, essential relief, removing a significant barrier to care. The rules are designed to give you and your family one less thing to worry about, allowing you to focus on your health.

Navigating these special circumstances can feel complex, but they are clearly outlined in the Official Medicare Eligibility Rules from the Social Security Administration. If you or a loved one are facing one of these situations, you don’t have to figure it out alone. Getting trusted, unbiased guidance is essential for making confident decisions. We are here to help you understand your options with clarity and compassion.

Putting It All Together: Your Medicare Eligibility Checklist

Navigating the question of who is eligible for medicare can feel overwhelming. To simplify things, we’ve created this quick checklist to help you see exactly where you stand. Think of this as your first step from confusion to clarity. Use these simple questions to confirm your path forward.

Check Your Age and Residency Status

This is the most common path to Medicare. Ask yourself:

- Are you age 65 or older?

- Are you a U.S. citizen or a legal resident who has lived in the U.S. for at least five consecutive years?

If you answered “yes” to both, you meet the basic requirements. You are eligible to enroll in Medicare Part B and likely Part A.

Review Your Work History (or Your Spouse’s)

Your work history determines whether you get hospital insurance (Part A) for free. Have you or your spouse worked and paid Medicare taxes for at least 10 years (which equals 40 credits)? If so, you will qualify for premium-free Part A. If not, don’t worry-you can still purchase Part A. Many people find that Original Medicare leaves gaps, which is why they add a Medigap plan to help cover out-of-pocket costs like deductibles and coinsurance.

Consider Any Disability or Health Conditions

You don’t have to be 65 to qualify for Medicare. You may be eligible earlier if you have a specific disability or health condition. This applies if you:

- Have been receiving Social Security Disability Insurance (SSDI) benefits for 24 months.

- Have been diagnosed with End-Stage Renal Disease (ESRD) or Amyotrophic Lateral Sclerosis (ALS).

If you qualify early, it’s also crucial to plan for prescription drug coverage (Part D) to ensure your medications are covered from day one.

Confirming your eligibility is a huge first step-congratulations! But understanding who is eligible for medicare is only half the journey. The next, and most critical, step is choosing the right coverage for your needs. Original Medicare was never designed to cover everything, leaving you exposed to significant costs.

Making the right choices during your enrollment period is key to protecting your health and savings for years to come. For trusted, unbiased guidance in navigating your options, The Modern Medicare Agency is here to make it simple. Visit us at themodernmedicareagency.com to connect with an expert who can help you navigate your choices with confidence.

Your Path to Medicare Clarity and Confidence

Navigating your Medicare eligibility doesn’t have to feel like solving a puzzle. As we’ve covered, the path to qualification is clear: most people become eligible when they turn 65, while others can qualify sooner based on a disability or with specific health conditions like ESRD and ALS.

However, simply understanding who is eligible for Medicare is only the first step on your journey. The real challenge often comes when choosing the right plan from a sea of confusing options. This is where costly mistakes can happen, but you don’t have to face it alone. As your trusted, independent broker, we provide the personalized, unbiased guidance you deserve, comparing plans from over 40+ carriers to find the perfect fit for your needs and budget.

Feeling overwhelmed? Let’s clarify your Medicare options together.

Let us help you move from confusion to confidence. You can take the next step with peace of mind, knowing a dedicated expert is on your side.

Frequently Asked Questions About Medicare Eligibility

Can I get Medicare if I never worked?

Yes, you can still qualify for Medicare even if you have never worked. If your spouse is at least 62 and worked for 10 years or more while paying Medicare taxes, you can be eligible for premium-free Part A based on their record. Navigating these spousal rules can feel confusing, but we are here to provide simple, clear guidance to ensure you receive all the benefits you are entitled to, giving you complete peace of mind.

Do I have to be a U.S. Citizen to be eligible for Medicare?

To qualify for Medicare, you must be a U.S. citizen or a legal resident who has lived in the United States for at least five consecutive years. This is a core requirement, along with meeting the age or disability criteria. Verifying your status is a simple but essential first step in the process. We can help you confirm your eligibility and walk you through the next steps with confidence, ensuring there are no surprises along the way.

Am I automatically enrolled in Medicare when I turn 65?

This is a common point of confusion. You are only automatically enrolled in Medicare if you are already receiving benefits from Social Security or the Railroad Retirement Board before you turn 65. If not, you must actively sign up during your Initial Enrollment Period. Missing this crucial window can result in lifelong late enrollment penalties. We help you steer clear of these costly mistakes by providing timely, expert guidance on when and how to enroll.

Can I have Medicare and private insurance at the same time?

Yes, it is very common to have both. Many people use private insurance to work with Medicare and cover costs that Original Medicare (Parts A and B) does not. This can include an employer plan if you’re still working, a Medicare Supplement (Medigap) plan, or a Medicare Advantage (Part C) plan. Our unbiased advice helps you understand how these options fit together, so you can build a coverage plan that truly protects you.

What happens if I’m still working at 65? Do I need to sign up?

The answer depends on your employer’s size. If your company has 20 or more employees, you may be able to delay enrolling in Medicare Part B without a penalty. For smaller companies, you will likely need to sign up when you turn 65 to avoid gaps in coverage. Knowing who is eligible for Medicare while working is tricky, but we simplify the rules for you so you can make the right decision with complete confidence and avoid penalties.

Does Medicare eligibility mean my healthcare will be free?

While you have earned your Medicare benefits through years of paying taxes, it is not entirely free. Most people receive Part A (hospital insurance) without a monthly premium. However, Part B (medical insurance) requires a monthly premium. You will also face out-of-pocket costs like deductibles and copayments. A big part of our job is to provide clarity on these costs and help you find a plan that fits your budget and health needs perfectly.