An independent Medicare agent is defined as a licensed insurance professional who represents multiple insurance carriers, giving you access to a broad range of Medicare plan options rather than a single company’s offerings. Choosing the right Medicare advisor matters more than most people realize. The difference between a plan that fits your health needs and budget and one that leaves you with unexpected costs often comes down to who helped you enroll. Paulbinsurance has been helping Medicare consumers make that distinction since 2007, and the education-first approach makes all the difference.

Why choose an independent Medicare agent over other options

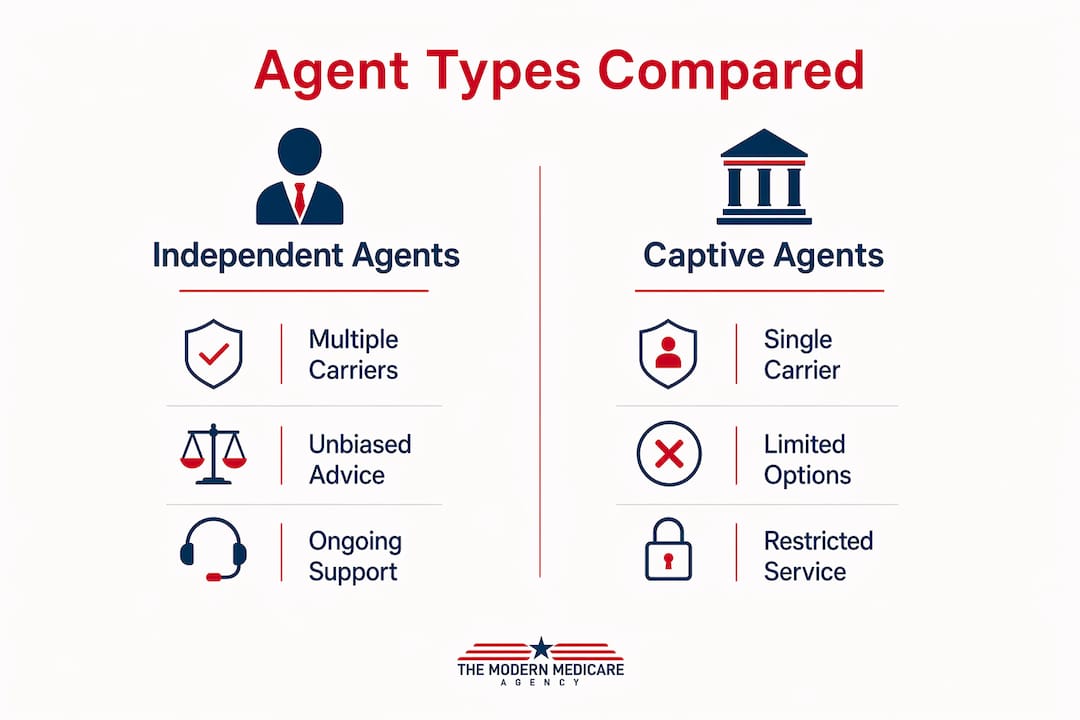

Independent agents represent multiple insurance carriers, which means they can compare plans across the entire market on your behalf. A captive agent, by contrast, works for a single insurer and can only offer that company’s plans. That restriction limits your choices before the conversation even begins.

The practical impact is significant. If the one carrier a captive agent represents does not have a plan that covers your doctors, your prescriptions, or your preferred hospital, you are out of options with that agent. An independent Medicare broker has no such constraint. They can shop across carriers to find the plan that actually fits your life.

Personalized advice from a local agent consistently outperforms what online quoting tools or call centers deliver. Many people who enroll through digital platforms end up with generic plans that miss important coverage details. A local independent agent asks the right questions first.

Independent agent vs. captive agent: key differences

| Feature | Independent agent | Captive agent |

|---|---|---|

| Carrier access | Multiple carriers | Single carrier |

| Plan variety | Medicare Advantage, Medigap, Part D | Limited to one insurer’s lineup |

| Advice bias | Impartial, client-focused | Tied to employer carrier |

| Ongoing support | Incentivized by renewal commissions | Varies by employer |

| Best for | Clients wanting full market comparison | Clients loyal to one specific insurer |

The captive vs. independent distinction is not just technical. It directly shapes how many real choices you get when you sit down to pick a plan.

How agent commissions work and why they benefit you

Independent Medicare agents are compensated through commissions paid by insurance carriers, not by you. 2026 CMS guidelines set the maximum initial commission at $694 and the renewal commission at $347 for Medicare Advantage and Part D (MAPD) plans. That structure matters because it means your agent earns less if you leave a plan than if you stay satisfied with it.

Renewal commissions create a direct financial incentive for agents to keep you in the right plan year after year. An agent who places you in a poor fit loses that renewal income when you switch. That alignment of incentives is one of the clearest structural reasons to work with a licensed agent rather than enrolling alone.

Many independent agents also work through Field Marketing Organizations, known as FMOs. FMOs provide agents with sales tools, compliance support, and carrier contract access. That back-end infrastructure means your agent has more resources to serve you, not fewer.

Key questions to ask any agent about compensation:

- Do you receive the same commission regardless of which plan I choose?

- Are you contracted with multiple carriers in my area?

- Will you contact me before the Annual Enrollment Period each year?

- Do you earn a renewal commission if I stay in my current plan?

Pro Tip: Ask your agent to show you at least three plan options side by side before you decide. An agent who only presents one option without explanation may not be shopping the full market for you.

How independent agents help disabled and underserved clients

Independent Medicare agents serve more than adults turning 65. People under 65 who qualify for Medicare due to disability represent a high-need population with specific plan requirements. Dual Eligible Special Needs Plans, known as D-SNPs, are designed for people who qualify for both Medicare and Medicaid. These plans coordinate care across both programs, reducing gaps and out-of-pocket costs for some of the most vulnerable enrollees.

D-SNPs account for 35.7% of Medicare Advantage enrollments. That share reflects how many people genuinely need specialized plan access, not just standard coverage. An independent agent who understands D-SNPs can connect disabled clients to benefits that a generic enrollment process would miss entirely.

The benefits of working with an independent Medicare advisor for this population include:

- Access to D-SNPs that bundle Medicare and Medicaid benefits into one coordinated plan

- Help identifying extra benefits like transportation, meal delivery, and over-the-counter allowances

- Guidance on Medicare supplement options for under-65 clients who face limited Medigap availability in some states

- Ongoing advocacy when coverage disputes or care coordination issues arise

- Enrollment support during Special Enrollment Periods triggered by disability status

Independent agents who specialize in this market understand the regulatory differences between states. That local knowledge is something no national call center can replicate.

How to work effectively with an independent Medicare agent

Choosing a Medicare advisor is not a one-time transaction. The relationship should extend through every Annual Enrollment Period and any major life change that affects your coverage. Knowing how to select and work with the right agent saves you money and frustration for years.

Step 1: Verify carrier access. Ask the agent how many carriers they are contracted with in your county. More carriers mean more real options. An agent contracted with only two or three carriers in a market with ten available plans is not giving you a full picture.

Step 2: Confirm Medicare specialization. Medicare rules, plan structures, and enrollment windows are specific and change annually. An agent who also sells auto and home insurance may not track CMS updates closely enough to serve you well. Paulbinsurance focuses exclusively on Medicare and senior insurance products, which means the team stays current on every rule change.

Step 3: Ask about ongoing service. A good agent contacts you before the Annual Enrollment Period each october to review your plan. Agents earn renewal commissions for keeping clients in suitable plans, so proactive outreach is both a service standard and a business incentive.

Step 4: Understand your plan options. A qualified independent agent explains the differences among Medicare Advantage, Medigap (Medicare Supplement), and Part D prescription drug plans clearly. Each serves a different need. Medicare Advantage bundles hospital, medical, and often drug coverage into one plan. Medigap covers the gaps in Original Medicare. Part D covers prescriptions as a standalone policy.

Step 5: Use local resources. Finding a trusted local agent in your area gives you someone who knows the carriers, hospitals, and provider networks in your region. National tools cannot account for local network differences that affect whether your doctor is covered.

Pro Tip: Bring a list of your current medications and your primary care doctor’s name to your first meeting. An agent who does not ask for this information before recommending a plan is not doing a thorough job.

Key Takeaways

An independent Medicare agent gives you broader plan access, unbiased advice, and ongoing support that captive agents and online tools cannot match.

| Point | Details |

|---|---|

| Independent agents shop the full market | They represent multiple carriers, giving you real plan comparisons instead of a single insurer’s options. |

| Commission structure rewards good service | CMS caps renewals at $347 for MAPD plans, incentivizing agents to keep you in the right plan long-term. |

| D-SNPs serve disabled and dual-eligible clients | Independent agents can connect under-65 disabled clients to coordinated care plans that generic enrollment misses. |

| Specialization matters | An agent focused exclusively on Medicare tracks annual CMS rule changes that affect your coverage and costs. |

| Ongoing relationship beats one-time enrollment | The best agents review your plan before every Annual Enrollment Period and contact you proactively. |

What 17 years of Medicare advising taught me

Most people come to me thinking Medicare is a one-time decision. Pick a plan, done. That misunderstanding costs them money every single year. Plans change their formularies, their networks, and their premiums every january. A plan that was perfect in 2024 may be a poor fit by 2026.

The agents who serve clients well are the ones who treat enrollment as the beginning of a relationship, not the end of a transaction. I have seen people stay in plans that no longer covered their primary doctor simply because no one called to review their options. That is a failure of service, not a Medicare problem.

One thing I tell every person I work with: an independent agent who is doing their job will never pressure you toward a specific plan. They will show you options, explain the tradeoffs, and let you decide. If an agent is pushing hard for one plan without asking about your doctors, your medications, or your budget, that is a red flag worth taking seriously. You can spot those warning signs early if you know what to look for.

The clients I have served since 2007 are not just policyholders. They are people who trusted me with a decision that affects their health and their finances. That responsibility does not end at enrollment.

— Paul

Paulbinsurance: independent Medicare guidance you can count on

Paulbinsurance is a team of independent Medicare agents led by Paul Barrett, who has been helping Medicare consumers since 2007. The team is contracted with multiple carriers and specializes in Medicare Advantage, Medigap, Part D, dental insurance, and long-term care products.

Every client gets a personalized plan review based on their doctors, medications, and budget. No scripts, no pressure, and no single-carrier bias. Whether you are turning 65, transitioning from employer coverage, or reviewing your current plan, the team at Paulbinsurance walks you through every option clearly. Start with a full breakdown of your Medicare Advantage plan options or get a complete picture of your Medicare eligibility and coverage before your next enrollment window opens.

FAQ

What is an independent Medicare agent?

An independent Medicare agent is a licensed professional who represents multiple insurance carriers, allowing them to compare and recommend Medicare plans across the full market rather than from a single insurer.

How does an independent agent differ from a captive agent?

A captive agent works for one insurance company and can only offer that company’s plans. An independent agent has contracts with multiple carriers and provides unbiased recommendations based on your specific needs.

Do I pay extra to use an independent Medicare agent?

No. Independent Medicare agents are compensated through commissions paid by insurance carriers. The cost to you is the same whether you enroll through an agent or directly with the insurer.

Can an independent agent help if I am under 65 and on Medicare due to disability?

Yes. Independent agents can access Dual Eligible Special Needs Plans (D-SNPs) and other specialized options for disabled clients under 65, including coordinated care plans that combine Medicare and Medicaid benefits.

How often should I meet with my Medicare agent?

You should review your plan with your agent at least once a year before the Annual Enrollment Period, which runs from october 15 through december 7. Any major health or financial change is also a good reason to reconnect.