You see the ads everywhere: $0 premiums, gym memberships, and all-in-one convenience. It sounds almost too good to be true, and a part of you might be worried that it is. This constant marketing can leave you feeling overwhelmed, and it’s why so many people search for answers about why medicare advantage plans are bad. They’ve heard stories from friends or neighbors who were suddenly denied necessary care or discovered their trusted doctor was no longer covered. The fear of making a costly, long-term mistake with your health is completely understandable.

The truth is, these plans have significant trade-offs that are often buried in the fine print. This article isn’t meant to scare you; it’s here to give you the clear, unbiased guidance you deserve. We will calmly walk through the real disadvantages and potential risks of Medicare Advantage plans. Our goal is to cut through the confusion and empower you with straightforward information, so you can look past the sales pitches and choose the right coverage for your future with complete confidence.

Key Takeaways

- Understand the most significant risk of an Advantage plan: being restricted to a specific network of doctors and hospitals, which can limit your access to care.

- Learn how the cost structure of Advantage plans differs from Original Medicare and discover the potential for frequent, unexpected out-of-pocket copays.

- Discover the role of “prior authorization” and how this requirement can create frustrating delays or even denials for necessary medical treatments.

- The real answer to why medicare advantage plans are bad often comes down to a mismatch; learn how to assess your own health needs to avoid choosing the wrong coverage for you.

The Truth Behind the ‘Bad’ Reputation: Why Are You Hearing So Many Negatives?

If you feel like you’re getting mixed signals about Medicare Advantage, you are not alone. One minute, you see an advertisement promising $0 premiums, dental coverage, and free gym memberships. The next, you hear a friend’s frustrating story about a denied claim or a favorite doctor who is suddenly out-of-network. It is perfectly reasonable to be cautious and ask the important question: why are Medicare Advantage plans bad for some beneficiaries?

The reality is that these plans operate on a fundamental trade-off. While millions of Americans are happy with their coverage, the negative experiences you hear almost always stem from this core exchange: you receive lower (or no) monthly premiums in return for agreeing to receive your care within a managed system. To fully grasp this, it helps to review a comprehensive overview of Medicare Advantage, which details how these plans are structured differently from Original Medicare.

The ‘Too Good to Be True’ $0 Premium

That $0 premium is the most heavily advertised feature, but it’s crucial to understand it isn’t truly “free.” Here’s how it works: instead of you paying a hefty premium, the government pays a fixed monthly amount to a private insurance company to manage your healthcare. The insurer’s challenge is to cover all your care within that budget. Your “cost” isn’t in the premium but in the potential restrictions and out-of-pocket expenses you may face, like deductibles, co-pays, and strict provider networks.

Understanding the Business Model

Medicare Advantage plans are administered by private, for-profit insurance companies. Their goal is to manage healthcare costs for a large group of members while staying profitable. This “managed care” approach is the source of nearly every major complaint. To control costs, insurers create rules that can include:

- Requiring you to use doctors and hospitals within a specific network.

- Needing a referral from your primary care physician to see a specialist.

- Requiring prior authorization from the plan before they will cover a service or procedure.

This business model is the primary reason why Medicare Advantage plans are bad when a member’s healthcare needs clash with the plan’s cost-saving rules.

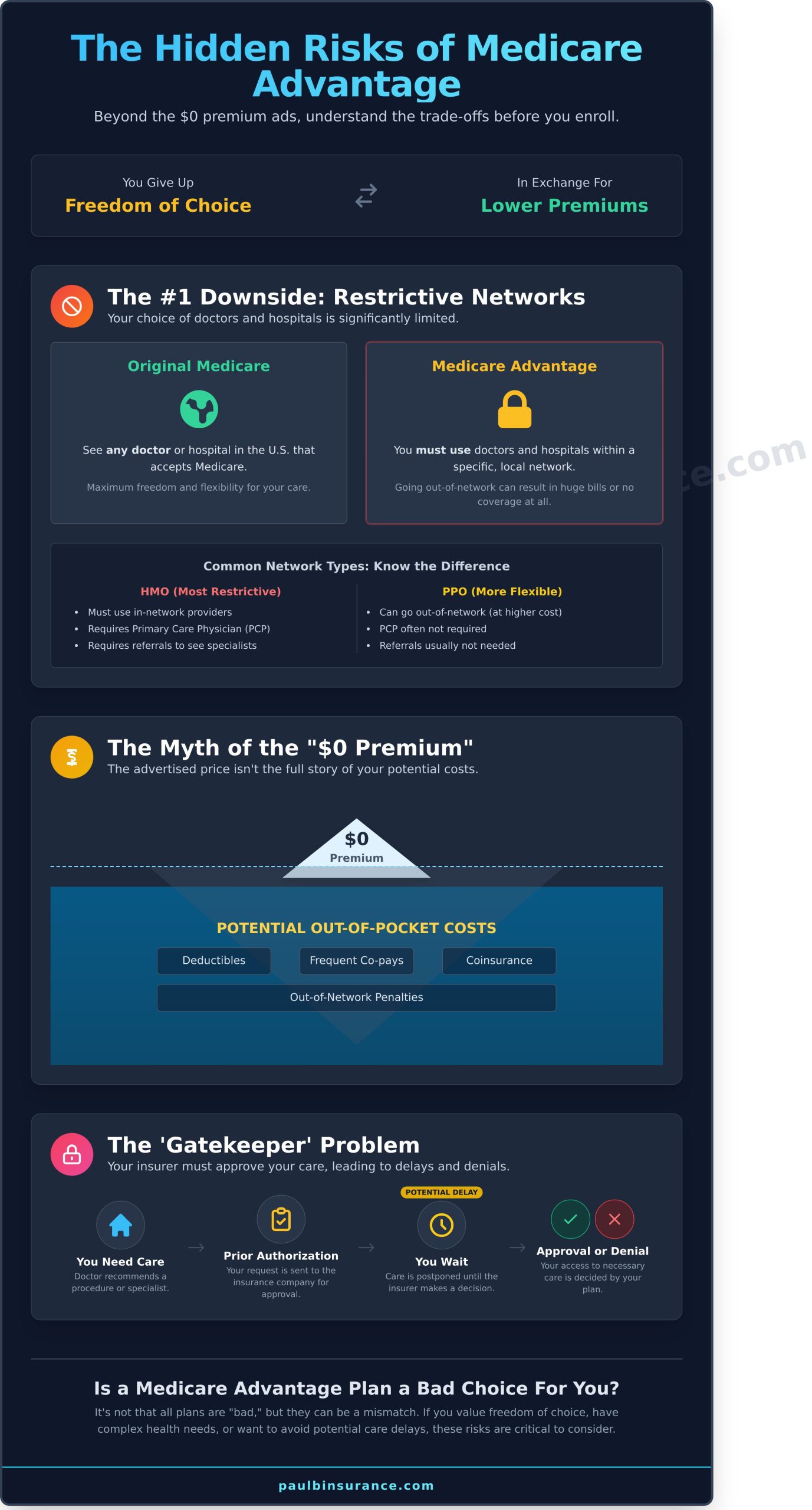

The #1 Downside: Limited Doctor and Hospital Networks

When clients ask us for an honest answer about why Medicare Advantage plans are bad for some individuals, the conversation almost always begins here: restrictive networks. While the low premiums are attractive, they come at the cost of your freedom to choose your healthcare providers. This is, without a doubt, the single most significant risk you take when enrolling in a Medicare Advantage (MA) plan.

Unlike Original Medicare, which allows you to see any doctor or visit any hospital in the U.S. that accepts Medicare, MA plans operate with specific, local networks. To receive care at the lowest cost, you must use doctors, specialists, and hospitals that are “in-network.” Going “out-of-network” can lead to staggering bills or, in many cases, the plan may not cover the service at all. Even more unsettling is that doctors and entire hospital systems can-and do-leave these networks, sometimes even in the middle of the year, leaving you scrambling to find new providers.

HMO vs. PPO: Understanding Your Freedom of Choice

Not all networks are created equal. The two most common types are HMOs and PPOs, and understanding the difference is crucial for your care.

- HMO (Health Maintenance Organization): These plans are typically the most restrictive. You must use doctors within their network (except for true emergencies), and you usually need to select a Primary Care Physician (PCP) to coordinate your care.

- PPO (Preferred Provider Organization): These plans offer more flexibility. You can see out-of-network doctors, but you will pay significantly more to do so. A PCP is not always required.

Before you even consider a plan, it is essential to confirm that your trusted doctors, preferred hospitals, and necessary specialists are all part of the network.

The Hassle of Specialist Referrals

Another major frustration with many MA plans, particularly HMOs, is the requirement to get a referral from your PCP before seeing a specialist. This creates an extra step-and an extra appointment-that can delay access to necessary care. This “gatekeeper” system is a core reason why medicare advantage plans are bad for those with complex health needs. When this process is combined with a high volume of prior authorization denials by insurance carriers, patients can find themselves waiting weeks or even months for an approved visit with a cardiologist or oncologist. This is in stark contrast to Original Medicare, where you can make an appointment with any specialist who accepts Medicare without needing permission first.

What About Traveling?

If you love to travel or spend part of the year in another state, a Medicare Advantage plan can be a serious liability. Most plans are built around regional networks, meaning your coverage is tied to a specific service area (like a county or group of counties). Outside of this area, your plan will typically only cover true medical emergencies. Routine check-ups, specialist visits, or pharmacy refills in another state are generally not covered. This is a major drawback for “snowbirds” and anyone who doesn’t want their healthcare choices limited by their zip code.

Beyond the Premium: Uncovering Potential Out-of-Pocket Costs

The allure of a $0 monthly premium is powerful, but it often masks a more complicated and potentially expensive reality. One of the primary reasons why medicare advantage plans are bad for many retirees is that they replace Original Medicare’s straightforward cost structure with a complex system of pay-as-you-go fees. While you might save on your monthly premium, you could face a steady stream of bills every time you see a doctor, visit a hospital, or receive a medical service.

This is a stark contrast to pairing Original Medicare with a Medigap (Medicare Supplement) plan, which is designed to cover most, if not all, of your out-of-pocket costs for a predictable monthly premium. With an Advantage plan, your healthcare costs can become highly unpredictable, especially during a year when you need significant medical care.

Copays, Coinsurance, and Deductibles

Understanding an Advantage plan’s cost-sharing is crucial. These private insurance plans are designed to be profitable, and one way they manage this is through cost-sharing. In fact, a major investigation by The New York Times revealed allegations that some large insurers have exploited Medicare for billions, which highlights the focus on profits over patient costs. Here’s what you’ll typically encounter:

- Copayments (Copays): A fixed dollar amount you pay for a service. For example, you might pay $20 for a primary care visit or $50 for a specialist.

- Coinsurance: A percentage of the cost of a service you are responsible for. You might pay 20% for durable medical equipment or certain outpatient procedures.

- Deductibles: The amount you must pay out-of-pocket before your plan begins to cover costs. Some plans have separate deductibles for medical services and prescription drugs.

Imagine a short hospital stay. You could face a daily copay for the first several days, separate copays for each doctor who sees you, and coinsurance for diagnostic tests. These small amounts add up with frightening speed.

The Maximum Out-of-Pocket (MOOP) Limit

Every Medicare Advantage plan must include a Maximum Out-of-Pocket (MOOP) limit. This is a critical safety net that caps how much you will spend on medical services in a calendar year. Once you hit this limit, the plan pays 100% of your covered in-network costs.

However, this “safety net” can be set very high. For 2025, plans can have a MOOP as high as $8,850 for in-network services. For many retirees on a fixed income, facing nearly $9,000 in medical bills during a serious illness is a devastating financial blow. This potential for high spending is a significant factor in understanding why medicare advantage plans are bad for those seeking financial predictability in retirement.

Prior Authorization: The ‘Gatekeeper’ Problem

If there is one aspect of Medicare Advantage that causes the most stress and confusion for members, it is prior authorization. This process can feel like a major roadblock standing between you and the care your doctor recommends. So, what is it?

Simply put, prior authorization (or pre-approval) is a requirement from the insurance company to approve a medical service, procedure, or medication before you receive it. While insurers use this as a tool to manage costs, for a patient, it can mean frustrating delays or even outright denials of necessary care. This ‘gatekeeper’ model is a fundamental reason many people question if these plans are the right choice for their health.

Why Do Plans Require Prior Authorization?

From the insurance company’s perspective, prior authorization serves two main purposes: to verify that a service is medically necessary and to control spending by ensuring a more expensive treatment isn’t used when a less costly, effective alternative is available. However, this process puts a third party-the insurer-directly in the middle of the trusted relationship between you and your doctor, potentially overriding their expert medical opinion.

The Risk of Denials and Appeals

While many prior authorization requests are eventually approved, denials are a real and frightening possibility. When a service is denied, you have the right to appeal, but this process can be slow, complicated, and incredibly stressful-especially when you are ill and waiting for treatment. This uncertainty is a core reason why Medicare Advantage plans are bad for those who want predictability and control over their healthcare.

This is where the freedom of Original Medicare combined with a Medigap plan truly shines. With that combination, if a treatment is medically necessary and covered by Medicare, you receive the care. There is no private insurance company acting as a gatekeeper to deny your doctor’s orders for common services like:

- Complex imaging (MRIs, CT scans, PET scans)

- Major inpatient or outpatient surgeries

- Stays in a skilled nursing facility

- Expensive medications administered by a doctor

Navigating these complex rules can feel overwhelming. If you’re looking for clear, unbiased guidance to understand which path is right for you, our team at Paul B Insurance is here to help you move from confusion to confidence.

Are They All Bad? How to Avoid a ‘Bad’ Medicare Advantage Plan

After reviewing the potential drawbacks, it’s easy to understand the concern. But are Medicare Advantage plans inherently bad? The straightforward answer is no. For many seniors, they are an excellent and affordable choice. The real danger isn’t in the plans themselves, but in choosing a plan that is a fundamental mismatch for your personal health needs, budget, and lifestyle.

The reason so many people ask why medicare advantage plans are bad is often because they or someone they know ended up in a plan that wasn’t right for them. A relatively healthy individual who wants to keep monthly costs low may love the $0 premium and bundled dental and vision benefits. In contrast, someone managing multiple chronic conditions may find the network restrictions and prior authorization requirements to be a constant, unacceptable barrier to care.

Who Might Be a Good Fit for an MA Plan?

A Medicare Advantage plan could be an ideal solution if you:

- Are in good health and don’t anticipate needing frequent specialist care.

- Are comfortable receiving your care from a specific network of doctors and hospitals.

- Prioritize a low (or $0) monthly premium and value the convenience of all-in-one coverage that often includes prescription drugs, dental, vision, and hearing benefits.

The Key to Choosing Wisely: Work With an Unbiased Expert

The potential for a mismatch is precisely why you shouldn’t have to navigate this complex decision alone. The stakes are simply too high to risk making a costly mistake. Working with an independent Medicare broker provides a crucial layer of protection. Unlike a captive agent who only represents one company, an independent expert represents you.

Our goal is to provide trusted, personalized guidance. We take the time to understand your health, your doctors, and your priorities. Then, we can compare dozens of plans from various insurance carriers to find the one whose network, costs, and rules align perfectly with your life. This is how you move from confusion to confidence. Let us help you compare your options with confidence.

Making an Empowered Choice for Your Healthcare

Navigating the world of Medicare can feel overwhelming, especially with so many conflicting stories. As we’ve explored, the real risks often lie in restrictive doctor networks, unpredictable out-of-pocket costs, and frustrating prior authorization hurdles. The core reason why medicare advantage plans are bad for some beneficiaries is a mismatch-a plan’s rigid structure clashing with their unique healthcare needs and budget.

But a potential pitfall for one person can be a perfect fit for another. The key is finding the right match without the stress and guesswork. This is where trusted, professional guidance becomes invaluable, ensuring you avoid a ‘bad’ plan and choose one that truly supports your well-being.

You don’t have to make this critical decision alone. With unbiased advice on over 40 insurance carriers and a history of serving 5,000+ clients with confidence, our mission is to provide the patient, expert guidance you need. Schedule your free, unbiased Medicare plan review today and move from confusion to confidence in your healthcare journey.

Frequently Asked Questions

Can I switch back to Original Medicare if I don’t like my Advantage Plan?

Yes, but it can be complicated. You can switch during specific times, like the Annual Enrollment Period (Oct. 15 – Dec. 7). However, if you’ve been on your Advantage Plan for more than a year, you may have to go through medical underwriting to qualify for a Medigap plan. This means you could be denied coverage based on your health, which is a significant risk to consider before leaving Original Medicare in the first place.

What is the difference between an HMO and a PPO network?

Think of it as a choice between cost and flexibility. An HMO (Health Maintenance Organization) plan requires you to use doctors within its network and get a referral to see a specialist. In contrast, a PPO (Preferred Provider Organization) plan offers more freedom, allowing you to see out-of-network doctors (for a higher cost) without needing referrals. Your choice depends on whether you prioritize lower costs (HMO) or greater access to providers (PPO).

What is the Maximum Out-of-Pocket (MOOP) on Medicare Advantage Plans?

The MOOP is a crucial safety net that limits what you spend on co-pays and deductibles in a year. For 2024, this limit can be as high as $8,850 for in-network services. While it protects you from unlimited costs, this figure is still very high for many seniors on a fixed income. It represents a significant financial risk you must be prepared for, especially if you have a serious health event during the year.

Do Medicare Advantage plans really deny a lot of claims?

It’s a common and valid concern. Because these plans are managed by private insurers, they often require prior authorization for tests, procedures, and specialist visits. This process can lead to delays or denials of care that your doctor deems necessary. This hurdle is a primary reason why medicare advantage plans are bad for individuals with complex or chronic health conditions who require consistent, predictable access to medical care without administrative roadblocks.

How can an independent Medicare broker help me avoid these problems?

An independent broker provides unbiased, expert guidance because we work for you, not a single insurance company. We can compare dozens of plans from different carriers to find one whose network truly includes your trusted doctors and whose rules fit your lifestyle. Our goal is to provide personalized support, helping you understand the fine print and steer clear of restrictive plans that could cause problems for you down the road. We help you move from confusion to confidence.

Are the extra benefits like dental and vision on Advantage plans any good?

While appealing on the surface, these “extra” benefits often come with significant limitations. The dental coverage may only include cleanings, or the network of approved dentists could be very small and inconvenient. It’s important to look past the advertising and examine the details. Your core medical coverage and doctor network should always be your top priority, as these “free” extras rarely provide the comprehensive coverage you might expect.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com