Choosing a Medicare Supplement plan can feel like a monumental decision for your retirement. You’re looking for long-term security, but the fear of being locked into a policy with huge, unexpected rate increases is real. It’s confusing why two companies can charge vastly different prices for the exact same government-standardized plan, making it difficult to spot a potential problem. This uncertainty is what separates a reliable partner from the worst medicare supplement companies that could jeopardize your financial peace of mind.

Our goal is to move you from that confusion to complete confidence. In this straightforward guide, we will pull back the curtain on the Medigap industry. You will discover the critical red flags that signal trouble, from a history of drastic rate hikes to poor customer service ratings. We’ll look at which companies have a pattern of issues and, most importantly, empower you with the tools to research any insurer. You’ll gain the clarity needed to choose a stable, trustworthy company that you can count on for years to come.

Key Takeaways

- Understand that while Medigap plans are standardized by law, the company behind the plan is what truly matters for your financial security and peace of mind.

- Learn the common warning signs of unstable providers to help you identify and steer clear of the worst medicare supplement companies before you enroll.

- Discover a simple 15-minute process to research any insurer’s financial health and customer service record, giving you confidence in your choice.

- Your best protection against future rate hikes and service issues is choosing the right company from day one, a decision just as crucial as picking the right plan.

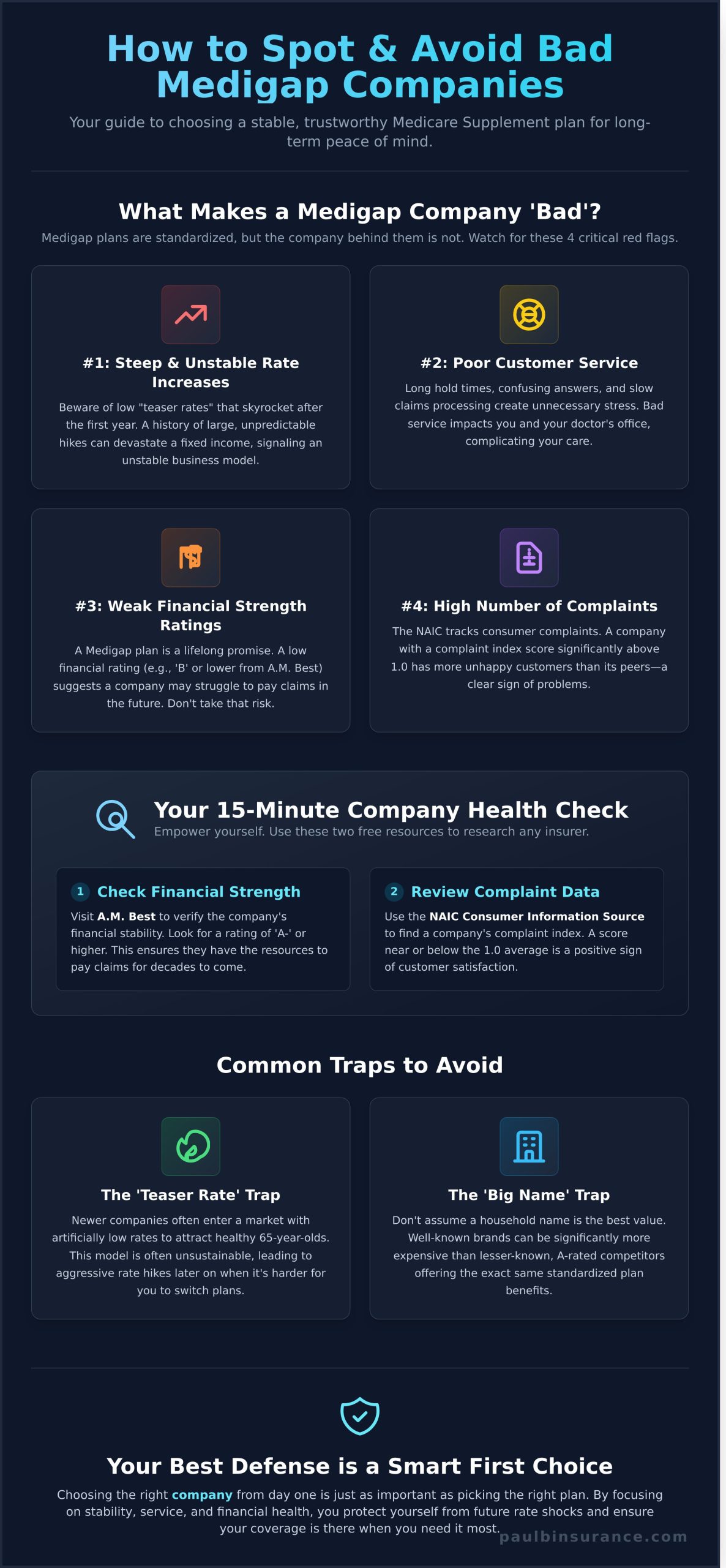

What Really Makes a Medigap Company ‘Bad’? 4 Critical Red Flags

Navigating the Medicare maze can feel overwhelming, and choosing the right supplement plan is a critical decision for your financial and physical health. It’s a common point of confusion, but by law, Medigap plans are standardized. This means a Plan G from Company A offers the exact same medical benefits as a Plan G from Company B. If you’re new to this concept, a great neutral resource on What is Medigap? can provide more background. The real difference isn’t the coverage-it’s the company standing behind it.

So, what separates a reliable partner from one of the worst medicare supplement companies? It comes down to stability, service, and integrity. To protect your peace of mind, use the following four red flags as your personal checklist. This simple guidance will help you avoid future regret and secure a plan you can count on for years to come.

Red Flag #1: A History of Steep and Unstable Rate Increases

For seniors on a fixed income, a sudden, sharp premium increase can be devastating. This is the most common issue we see. Many companies use an ‘Attained-Age’ pricing model, where your premium rises as you get older. Some lure you in with a low “teaser rate” that skyrockets after the first year. A company with a history of large, unpredictable rate hikes is a major warning sign.

Red Flag #2: Poor Customer Service and Claims Processing

Your Medigap coverage is only as good as the company’s ability to pay claims efficiently and answer your questions. Long hold times, confusing answers, and a difficult claims process create unnecessary stress when you should be focused on your health. Remember, it’s not just you who suffers-your doctor’s billing staff has to deal with these companies, too, which can add another layer of frustration to your care.

Red Flag #3: Weak Financial Strength Ratings

A Medicare Supplement plan is a long-term promise. You need to be confident that your chosen company will be around to pay its bills for the rest of your life. Independent agencies like A.M. Best grade insurance carriers on their financial stability. A low rating (such as B or lower) can signal that a company may struggle to meet its obligations in the future, making it a risk you shouldn’t take.

Red Flag #4: High Number of Official Complaints

The National Association of Insurance Commissioners (NAIC) tracks consumer complaints against insurance companies. They publish a Complaint Index, which creates a level playing field by comparing companies of different sizes. A score of 1.0 is the national average. A company with a score significantly above 1.0 receives more complaints than its peers, which is a clear indicator of customer dissatisfaction.

Which Companies Have a Reputation for Problems?

Navigating the Medicare Supplement market can feel overwhelming, especially when you hear stories about bad experiences. It’s important to understand that no single company is the “worst” for everyone. A carrier’s performance, rates, and customer service can change over time and vary significantly from one state to another. The information below is based on historical data, public records, and common patterns we’ve observed over years of helping clients. When people search for the worst medicare supplement companies, they are typically trying to avoid specific problems like these.

Companies Known for Aggressive ‘Teaser’ Rates

Some companies, particularly those newer to a state’s Medigap market, may use a strategy of offering incredibly low introductory rates to attract healthy 65-year-olds. While appealing at first, this business model often leads to steep and frequent rate increases down the line. This can make your once-affordable plan a significant financial burden in your late 70s or 80s, precisely when you need it most and switching plans is more difficult.

Carriers With Lower Financial or Customer Service Ratings

A stable company is a reliable one. That’s why we pay close attention to two key metrics: financial strength and customer complaints. Companies that consistently receive lower ratings from A.M. Best (such as B or lower) may pose a future risk. More importantly, the National Association of Insurance Commissioners (NAIC) tracks consumer complaints. As part of our commitment to providing trusted guidance, we always research Medigap company complaints to identify carriers with a high complaint ratio. A high number of complaints relative to a company’s size is a major red flag that requires extra scrutiny.

The ‘Big Name’ Trap: Why Brand Recognition Isn’t Enough

It’s easy to assume a household name offers the best product, but that’s not always true in the Medigap world. For example, AARP/UnitedHealthcare is one of the most recognized brands available. While they are a stable company with a strong reputation, their premiums often start significantly higher than those of lesser-known but equally A-rated competitors. You could end up paying hundreds of dollars more per year for the exact same standardized benefits. The biggest name doesn’t always equal the best value for your unique situation.

How to Research Any Medigap Company Yourself (in 15 Minutes)

Knowledge is your best defense against making a poor choice. Instead of just taking our word for it, we want to empower you with the tools to become a confident, informed shopper. This simple, three-step process is the same one we use to vet insurers, and it will help you spot red flags and steer clear of the worst medicare supplement companies on your own.

Follow these steps to put any insurer under the microscope in about 15 minutes.

Step 1: Check Financial Strength with A.M. Best

A Medigap plan is a long-term promise that the company will be there to pay its claims for decades. A company’s financial stability is non-negotiable. The gold standard for rating an insurer’s financial health is A.M. Best. You can look up any company on their website to see its rating.

- What to look for: A rating of ‘A-‘ (Excellent) or better.

- How to interpret it: An ‘A’ rating signifies that, in A.M. Best’s opinion, the insurer has an excellent ability to meet its ongoing insurance obligations. This gives you peace of mind that your claims will be paid without issue.

Step 2: Look Up the NAIC Complaint Index

How does a company actually treat its policyholders? The National Association of Insurance Commissioners (NAIC) provides the answer by tracking official consumer complaints. You can research any company’s complaint history using the official NAIC Consumer Insurance Search tool on their website. The key metric is the complaint index. A score of 1.0 is the national average. A score below 1.0 is great, but a score significantly above 1.0 is a major red flag, indicating more complaints than expected for its size.

Step 3: Ask About Rate Increase History

This is the most critical piece of information and the hardest to find on your own. A low introductory premium means nothing if the company has a history of aggressive rate hikes. This is where the value of a truly independent broker shines. You should ask any agent you speak with this direct question:

“What has been this company’s average rate increase history in my state for the last 3-5 years?”

If the agent dodges the question or says they don’t know, you should walk away. A trustworthy, experienced agent will have this data and share it transparently. This is the kind of unbiased guidance that helps you avoid the worst medicare supplement companies and secure stable, long-term coverage.

Your Best Defense: How to Avoid a Bad Company from Day One

Navigating the world of Medicare Supplements can feel overwhelming, especially after learning about the pitfalls of choosing the wrong carrier. The truth is, selecting the right company is just as vital as choosing the right plan letter. Trying to vet dozens of insurers on your own is a time-consuming and risky process, filled with confusing marketing and data that doesn’t tell the whole story. This is where an expert guide can make all the difference.

Why ‘Cheapest’ Today is Rarely ‘Best’ Tomorrow

A rock-bottom premium at age 65 is often a ‘teaser rate’ designed to attract new customers. The real measure of a good company is its rate stability over time. A carrier with a history of responsible pricing might cost a few dollars more upfront, but it can save you from the drastic, unaffordable rate hikes that are common with less stable insurers. The goal is long-term affordability, not just a cheap first year.

The Independent Broker Advantage: We Do the Research For You

An independent broker is your best defense against the worst medicare supplement companies because we work for you, not a single insurance carrier. We provide unbiased, expert analysis based on data that isn’t readily available to the public. We help you make an informed decision by evaluating:

- Rate Increase Histories: We track which companies have a record of stable, predictable rate adjustments over many years.

- Financial Stability: We review A.M. Best ratings to ensure a company has the financial strength to pay claims for decades to come.

- Market Insights: We know which new carriers are using aggressive, unsustainable pricing to gain market share, a classic red flag.

Gain Confidence and Lifelong Support

Our mission is to move you from confusion to confidence. Working with an expert guide removes the fear of making a costly mistake and ensures you choose a reliable company from the start. We don’t just help you enroll; we provide lifelong support for any questions or needs that arise. Ready to find a stable, reliable plan without the stress and guesswork? Schedule your free, no-obligation consultation today to get trusted guidance.

Choose Your Medigap Plan with Confidence

Navigating the world of Medicare Supplements can feel overwhelming, but you now have the tools to make an informed choice. Remember, the best defense is recognizing the red flags-like unstable finances and a history of aggressive rate hikes-before you enroll. Empowering yourself with a simple research process is the most effective way to steer clear of the worst medicare supplement companies and protect your financial future.

But you don’t have to do this complex research alone. An experienced, independent expert can provide the clarity you need. With 18+ years of dedicated experience, we offer completely unbiased guidance by comparing plans from over 40 trusted insurance carriers. We work for you, not the insurance companies, ensuring your needs always come first.

Get free, unbiased help comparing top-rated Medigap companies. Let us help you move from confusion to confidence and find the peace of mind you deserve.

Frequently Asked Questions

Are all Medicare Supplement Plan G policies the same?

Yes, the medical benefits for every Plan G are standardized by the government. This means a Plan G from one company must offer the exact same coverage as a Plan G from any other carrier. The only differences are the monthly premium you pay and the company’s reputation for customer service and rate stability. This is why it’s so important to choose a company with a history of fair, stable rate increases to avoid overpaying for identical benefits.

Can I switch Medigap companies if I’m unhappy with mine?

You can apply to switch Medigap companies at any time, but it’s not always simple. Outside of specific guaranteed issue periods, you will likely have to answer health questions, a process called medical underwriting. An insurance company can deny your application based on your health history. This is why making a confident, well-researched choice from the beginning is so crucial to ensure you have stable, long-term coverage without future complications.

Why do Medigap premiums increase every year?

Medigap premiums typically increase due to two key factors: your age and medical inflation. Most plans are “attained-age rated,” meaning the premium rises as you get older. Additionally, as the overall cost of healthcare services goes up, insurance carriers adjust their rates to cover those higher expenses. A company with a history of large, unpredictable rate hikes is a major red flag, as this can quickly make an affordable plan unmanageable.

Is a company that isn’t on a ‘worst’ list automatically a good choice?

Not necessarily. While steering clear of the worst medicare supplement companies is an essential first step, it doesn’t mean every other option is the right fit for you. A company might simply be average, not terrible. The best choice depends on factors like long-term rate stability, financial strength, and customer service in your specific area. Our guidance helps you move beyond just avoiding the bad and confidently select the truly excellent options.

How do I find the best Medicare Supplement company for my specific state?

The “best” company can change dramatically depending on your state and even your zip code. Insurance carriers price their plans differently across the country. The most effective way to find your ideal fit is to work with an independent broker. We provide a personalized comparison of all the top-rated carriers available where you live, analyzing their rates, rate histories, and financial ratings to give you a clear and simple recommendation.

Why does it cost me nothing to use an independent Medicare broker?

Our expert guidance and year-round support come at no cost to you. This is because we are compensated directly by the insurance company if you decide to enroll in a plan through us. Your premium is the exact same price whether you use our service or go directly to the carrier. This allows us to provide completely unbiased advice focused on finding the perfect plan for your needs, not on selling a particular product.