The most expensive monthly premium on your desk right now might actually be the most affordable way to protect your retirement in 2026. It sounds backwards, but paying more upfront often prevents the $2,500 surprise hospital bills that catch so many seniors off guard. We understand the immediate sticker shock you feel when comparing these rates to “zero premium” alternatives. It leads many to ask the logical question: why doesn’t everyone get a Medigap plan if it offers such total peace of mind? You aren’t alone in feeling overwhelmed by the alphabet soup of plans or the fear of being locked into a monthly cost that only goes up.

We’re here to pull back the curtain on why Medigap isn’t the right fit for every person and help you decide if that premium is a smart investment for your specific future. We’ll simplify the jargon and show you the long-term ROI of these plans versus the 20% coinsurance risks of original Medicare. You’ll finish this guide with a clear path from confusion to confidence, knowing exactly how to protect your savings without the pressure of a sales pitch.

Key Takeaways

- Understand why Medicare Advantage enrollment is hitting record highs in 2026 and how to decide if Medigap’s “bridge” coverage is worth the monthly premium for your peace of mind.

- We answer the big question, “Why doesn’t everyone get a Medigap plan,” by breaking down the financial trade-off between predictable monthly bills and the risk of high out-of-pocket costs.

- Learn about the “Lock-In” effect and why your initial 6-month window is a critical, one-time opportunity to secure coverage without being denied for health reasons.

- Discover how to maintain total freedom over your healthcare by choosing a path that lets you see any doctor in the country who accepts Medicare, without the stress of network restrictions.

- Find out how we act as your personal advocate to help you navigate over 40 carriers, moving you from confusion to confidence as you choose your best fit for 2026.

The Medigap Mystery: Why Isn’t It the Universal Choice?

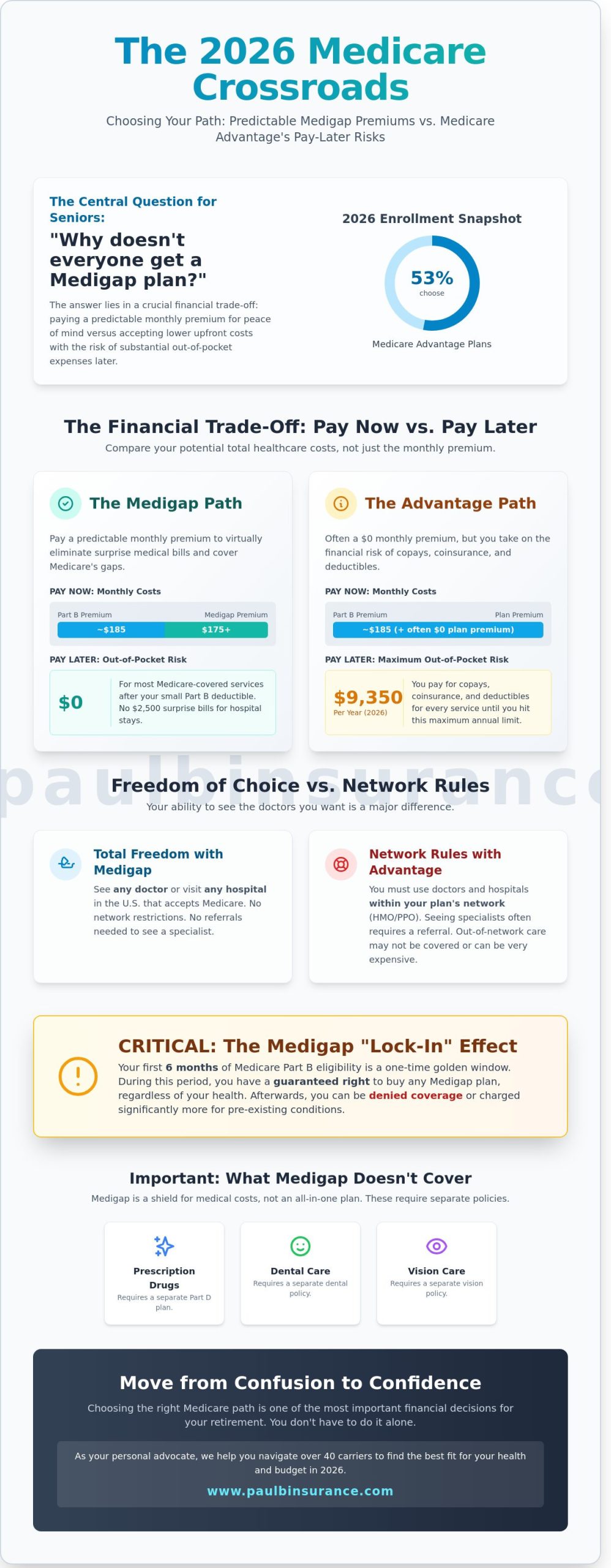

We know how overwhelming the mailbox can be during enrollment season. Between the glossy brochures and the constant television ads, it’s easy to feel like you’re lost in a maze. One of the most common questions we hear in our office is, “Why doesn’t everyone get a Medigap plan?” It’s a fair question. If Medigap covers the 20% gap that Original Medicare leaves behind, why do so many people choose a different path? As of January 2026, over 53% of Medicare beneficiaries have opted for Medicare Advantage plans instead. This shift happens because people often prioritize their immediate monthly budget over potential future costs. For a comprehensive overview of Medigap, you can see how these plans were standardized to provide predictable support. However, the choice often comes down to a simple trade-off between paying now or paying later.

We see our role as your guide to help you move from confusion to confidence. Medigap acts as a bridge. It connects the coverage gaps that can otherwise lead to financial ruin if a major health event occurs. Even so, the 2026 trend shows that many seniors are attracted to the “all-in-one” feel of other options. They see the $0 premium stickers and wonder why they should pay for a supplement. We want to validate that feeling of hesitation. It’s a lot of money to commit to every month, and we’re here to help you decide if that commitment is actually a smart investment for your specific health needs.

The “Sticker Shock” Factor

The biggest hurdle for most folks is the monthly bill. When you choose a Medigap plan, you pay a set premium every month to a private insurance company. This is in addition to your standard Medicare Part B premium, which in 2026 sits at a projected $185 per month for most people. Adding a Plan G premium of $175 or $210 on top of that can feel like a lot for someone on a fixed income. Many people see the $0 premium marketing for Advantage plans and feel that it’s the only affordable way to survive. We understand that stress. It’s hard to look ten years down the road when you’re trying to balance your checkbook today. This immediate cost is the primary reason why doesn’t everyone get a Medigap plan right away.

What Medigap Does (and Doesn’t) Cover

Medigap is designed to be a shield. It steps in to pay for the “big three” costs that usually fall on your shoulders:

- Your Part A hospital deductibles: Which can cost over $1,700 per benefit period in 2026.

- Part B outpatient coinsurance: That 20% of the bill for doctor visits and surgeries.

- Copays: Those small charges that add up quickly during a long recovery.

But it’s not a catch-all solution. A common point of confusion we clear up is that Medigap doesn’t include Medicare Part D for your prescriptions. You also won’t find the “extras” that Advantage plans use to attract members. If you want dental and vision insurance, you’ll typically need to set those up as separate policies. This lack of bundling is another reason why some people look elsewhere. We believe in being honest about these gaps so you can make a choice with your eyes wide open.

The Financial Trade-off: Premiums vs. Out-of-Pocket Risks

When we talk to folks about their options, one question comes up often: Why doesn’t everyone get a Medigap plan if the coverage is so good? The answer usually comes down to the monthly premium. It’s easy to look at a $0 premium Advantage plan and think it’s the better deal. However, we encourage you to look at the total cost of your care, not just the monthly bill. Choosing a plan is a balance between what you pay now and what you might owe later. This is the “Pay Now vs. Pay Later” philosophy that defines senior financial planning in 2026.

Some people believe that healthy people don’t need supplements. We’ve seen how quickly that can change. A single diagnosis or an unexpected fall can turn a “low-cost” plan into a major financial burden overnight. We want to help you move from confusion to confidence by looking at the hard numbers. If you’re healthy today, you’re in the best position to secure coverage before you actually need it.

Calculating Your “Maximum Exposure”

In 2026, the out-of-pocket (OOP) maximum for many Medicare Advantage plans has reached $9,350 for in-network services. That’s a significant amount of money to have “at risk” every year. If you have a major health event, you’re responsible for co-pays and co-insurance until you hit that limit. In contrast, a Medigap Plan G leaves you with almost zero exposure after you meet your small Part B deductible.

Consider a typical 5-day hospital stay. Under many 2026 Advantage plans, you might pay a $400 daily co-pay. That’s $2,000 for one stay. For most retirees, that $2,000 alone exceeds an entire year’s worth of Medigap premiums. The “break-even” point usually happens after just one or two moderate medical events. We believe it’s better to have a plan that protects your savings rather than one that asks you to gamble on your health.

Budgeting for Predictability

Many of the seniors we serve prefer a fixed monthly cost they can set their watch by. They don’t want to open the mailbox and fear a surprise $500 bill for a specialist visit or a diagnostic test. Medigap eliminates “medical bill anxiety” because the insurance company pays its share automatically. You can find more details on how these specific levels of coverage work on our Medigap overview page.

Waiting until you’re sick to buy a supplement is a risky strategy. Because of the official Medigap enrollment rules, you may not be able to switch into a Medigap plan later if you have a pre-existing condition. This “lock-in” effect is a primary reason why doesn’t everyone get a Medigap plan at first; they don’t realize that the door might close later. We’re here to make sure you understand these timelines so you don’t face a penalty or a denial of coverage down the road.

Our goal is to make this process simple and stress-free. If you’re feeling overwhelmed by the different price points, we can help you compare costs and benefits to see which path fits your specific budget. We take the time to listen to your concerns because we believe you deserve a plan that offers both clarity and peace of mind.

The “Lock-In” Effect: Why You Can’t Always Get Medigap Later

Your 65th birthday brings a wave of mail and a massive decision. This choice is often permanent because of the Medigap Open Enrollment Period. This is a one-time, six-month window that begins the month you turn 65 and enroll in Medicare Part B. During these 180 days, insurance companies must sell you any policy they offer at the best available rate, regardless of your health. We call this your “golden ticket” because it is the only time you are guaranteed acceptance without a single health question. You can find more Official Medigap Information regarding these protections on the government website.

Why doesn’t everyone get a Medigap plan during this window? Usually, it comes down to the monthly premium. In 2026, many seniors feel tempted by the $0 premium options found in Medicare Advantage. They think they can simply enjoy the lower costs now and switch to Medigap if they get a serious diagnosis later. This is the most dangerous misconception in the Medicare system. In about 46 states, once your initial six-month window closes, you lose your power. If you try to buy a Medigap plan later, you must go through a process that could leave you stranded without the coverage you need.

Medical underwriting is the process where insurers use your health history to set prices or deny coverage after your initial enrollment. In 2026, insurance companies are looking for specific “knock-out” conditions. If you have been treated for things like chronic obstructive pulmonary disease, insulin-dependent diabetes, or congestive heart failure, most carriers will simply say “no.” They aren’t required to take you. We have seen too many people stuck in plans they no longer want because their health changed before they tried to switch.

Guaranteed Issue Rights vs. Medical Underwriting

There are a few “safety valves” known as Guaranteed Issue rights. If you chose Medicare Advantage when you first became eligible for Part B, you have a 12-month “Trial Right.” This allows you to taste-test the Advantage system. If you decide it isn’t for you within that first year, you can switch back to Medigap without answering health questions. We also help clients who lose coverage because they move out of their plan’s service area or because their current plan leaves the Medicare program. Outside of these specific scenarios, pre-existing conditions like a recent cancer diagnosis or an upcoming knee surgery will likely prevent you from getting a new policy. We work to ensure you don’t miss these critical deadlines so you never have to worry about a denial.

The Risk of the “One-Way Door”

Choosing your Medicare path at 65 is often a 20-year decision. We view it as a “one-way door” because while it’s easy to walk from Medigap to Medicare Advantage, the door often locks behind you if you try to walk back. Why doesn’t everyone get a Medigap plan right away? They often don’t realize that the $270 Part B deductible or the monthly premium is a small price to pay for the “all-access pass” to any doctor in the country. Our team helps you look past the immediate cost to see the long-term security. We take you from confusion to confidence by showing you how these choices impact your bank account at age 75 or 85. We simplify the jargon so you know exactly how the system works. Our goal is to protect you from the stress of being “locked out” of the best healthcare options when you need them most.

Freedom of Choice: Why “Any Doctor” is a Powerful Benefit

When we sit down with clients to map out their future, they often ask us a very logical question: Why doesn’t everyone get a Medigap plan? It’s a fair point, especially when you consider the sheer level of control these plans provide over your healthcare. The primary reason people look elsewhere is usually the monthly premium cost, but for many of our clients, the price of freedom is worth every penny. If you value the ability to choose your own medical team without a corporate middleman, this is where Medigap truly shines.

The core rule of Medigap is refreshingly simple: if a doctor or hospital accepts Original Medicare, they must accept your Medigap plan. There are no “in-network” or “out-of-network” lists to check. This is a massive departure from the Medicare Advantage model, where you are often restricted to a specific zip code or a limited group of providers. This freedom is why travelers and “snowbirds” almost always lean toward Medigap. If you spend your winters in Arizona and your summers in Michigan, you don’t want to spend your vacation hunting for a doctor who is “in-network.” With Medigap, your coverage travels with you to every corner of the United States.

Network Narrowing in 2026

As we move through 2026, we’ve seen a significant shift in how private insurance networks operate. Many Medicare Advantage networks have become smaller over the last 24 months. Recent data from early 2026 suggests that some regional networks have shrunk by as much as 12 percent to manage rising costs. This means your favorite specialist might be in-network today but gone tomorrow.

We believe you deserve more stability than that. Medigap provides the peace of mind that comes from knowing you can visit top-tier cancer centers or renowned specialists nationwide without a second thought. You won’t be told that the best surgeon for your condition is “off-limits” because of a contract dispute. For a deeper look at how these network restrictions can impact your care, feel free to reference our Medicare Advantage guide.

The Prior Authorization Headache

One of the biggest stressors we see in 2026 is the rise of prior authorizations. This is the process where an insurance company must give you “permission” before you can receive a specific treatment or surgery. It’s an administrative hoop that can lead to delays when you are already feeling vulnerable. On a Medigap plan, this headache simply doesn’t exist. If Medicare says a procedure is medically necessary and covers it, your Medigap plan pays its portion automatically.

We also love that Medigap removes the “gatekeeper” model. You don’t need to visit a primary care doctor just to get a referral for a dermatologist or a cardiologist. You have the autonomy to manage your own health. It leads back to that core question: why doesn’t everyone get a Medigap plan when the lack of red tape is so clear? For those who want to avoid the stress of insurance company denials, the answer is usually to stick with Original Medicare and a solid supplement.

We are here to help you move from confusion to confidence. If you want to ensure you never have to ask an insurance company for permission to see your doctor, we can guide you through the process. Schedule a call with us today to find the right fit for your lifestyle.

Finding Your Balance: How We Help You Choose the Right Path

Choosing a Medicare path in 2026 feels like trying to solve a puzzle where the pieces keep changing shape. There is no single “best” plan that works for every senior in America. Instead, there is only the specific plan that fits your 2026 lifestyle, your doctor list, and your monthly budget. You might ask, why doesn’t everyone get a Medigap plan when it covers so many out-of-pocket costs? For 14 million Americans, the answer often comes down to the monthly premium versus the perceived risk. While a Medigap Plan G might cost $185 a month in 2026, some prefer the lower upfront cost of an Advantage plan despite the higher potential copays.

Our role at The Modern Medicare Agency is to help you see through the marketing noise. We act as independent brokers, which means we represent you rather than the 43 insurance carriers we currently work with. If a carrier raises their rates by 12 percent next year, we are the ones who call you to find a more stable option. We don’t have a quota to fill for any specific company. Our only goal is to ensure you don’t feel like just another policy number in a database. We want you to feel empowered by your choices.

The Unbiased Advantage

Talking to an independent broker is fundamentally different from calling a single insurance company. A captive agent at a large carrier can only tell you why their specific plan is the best, even if it doesn’t cover your specific 2026 medications. We simplify the jargon so you know exactly how your plan works before you ever sign a document. Our promise is simple: we are never rushed, never pressured, and always focused on your protection. We help you understand why doesn’t everyone get a Medigap plan by showing you the math behind the premiums versus the 2026 Part B deductible of $257.

We move you from a state of confusion to a place of total confidence. This isn’t a one-time transaction that ends when you get your card in the mail. We provide year-round support to handle billing errors or network changes that might occur mid-year. If your favorite specialist leaves a network on October 12, 2026, we are here to help you find the next best step. We stay by your side through every season of your retirement.

Next Steps: Your 5-Step Path to Peace of Mind

We invite you to take a breath and let us handle the heavy lifting. Your journey to clarity starts with a personalized review of your current health needs and your financial goals for the coming years. We follow a methodical process to protect your future:

- Step 1: We analyze your 2026 prescription drug costs using current pharmacy data.

- Step 2: We verify that your current doctors and specialists accept the plans we are considering.

- Step 3: We compare the 5-year rate increase history of our top-rated carriers.

- Step 4: We explain the “fine print” in plain English so there are no surprises at the doctor’s office.

- Step 5: We complete the enrollment paperwork together to ensure zero mistakes.

You don’t have to do this alone. We invite you to Schedule a Call with The Modern Medicare Agency for a no-obligation strategy session. We will look at your specific situation and give you an honest assessment of your options. We are here to make the complex simple and ensure you feel protected every single day of the year. Let us help you find the path that leads to true peace of mind.

Moving From Confusion to Confidence in Your Medicare Journey

Deciding on your coverage for 2026 shouldn’t feel like a gamble. We’ve explored the vital balance between predictable monthly premiums and the risk of high out-of-pocket costs. You now understand the “lock-in” effect where waiting too long can limit your future options due to medical underwriting rules that apply in most states. You also know that the freedom to see any of the 900,000 physicians who accept Medicare nationwide is a massive benefit for those who value choice. So, why doesn’t everyone get a Medigap plan if the perks are so clear? Often, it’s because the monthly costs don’t fit every budget or the complex rules create unnecessary fear. We’re here to replace that fear with absolute clarity. Our team provides unbiased guidance from 40+ different carriers across more than 34 states. We’ve maintained a 5-star rating by making sure you never feel pressured or rushed. We’ll help you navigate the 2026 landscape to find a path that protects both your savings and your health. Let’s turn your Medicare confusion into total confidence today.

Schedule a Call With Paul to Find Your Perfect Plan

Frequently Asked Questions

Is it true that I can be denied for a Medigap plan if I wait too long?

Yes, you can be denied coverage or charged more if you apply after your six month Medigap Open Enrollment Period ends. In 2026, 47 states still allow insurance companies to use medical underwriting to screen applicants who miss this initial window. We help you avoid these stressful denials by ensuring you enroll when your acceptance is legally guaranteed. Taking action early is the best way to secure your peace of mind.

Does Medigap cover prescription drugs in 2026?

No, Medigap plans do not cover outpatient prescription drugs in 2026. You must enroll in a separate Part D plan to get coverage for your medications. Under the updated 2026 guidelines from the Inflation Reduction Act, your out of pocket drug costs are capped at $2,000 per year. We simplify this process by helping you coordinate a standalone drug plan alongside your Medigap policy so you stay protected.

Can I switch from Medicare Advantage back to a Medigap plan during Open Enrollment?

You can apply to switch during the Annual Enrollment Period, but you will likely need to pass a health background check to qualify for Medigap. Many people find this process confusing, which is one reason why doesn’t everyone get a Medigap plan; they realize too late that their health history might block a switch. We provide unbiased guidance to help you determine if you can realistically move back to Original Medicare without facing a rejection.

Why are Medigap premiums different depending on where I live?

Premiums vary by location because insurance companies set rates based on local healthcare costs and state specific regulations. For example, a 65 year old in Miami might pay $285 for Plan G while someone in rural Iowa pays $145 for the exact same benefits. We look at the data in your specific zip code to find the most competitive rates. This ensures you aren’t overpaying for the security you deserve.

Do I still need to pay my Medicare Part B premium if I have a Medigap plan?

Yes, you must continue to pay your monthly Part B premium to keep your Medigap coverage active. In 2026, the standard Part B premium is projected to be $195.40 for most beneficiaries. Medigap is designed to work as a secondary payer to Medicare, so your primary coverage must stay in place. We make sure you understand your total monthly budget so there are no surprises or hidden costs.

What is the most popular Medigap plan in 2026?

Plan G remains the most popular choice for our clients in 2026 because it offers the highest level of protection for new enrollees. It covers all your Medicare gaps once you pay the annual Part B deductible, which is $275 this year. Over 60% of people entering Medicare choose Plan G to eliminate the fear of unpredictable hospital bills. It is the gold standard for anyone seeking a simple, “set it and forget it” solution.

Is Medigap better than Medicare Advantage if I have a chronic condition?

Medigap is often the preferred choice for chronic conditions because it allows you to see any specialist in the country who accepts Medicare. You won’t have to worry about restrictive provider networks or getting referrals to see a doctor at a facility like the Cleveland Clinic. This freedom is a major factor in why doesn’t everyone get a Medigap plan; some prefer lower premiums, but those with health concerns usually value this total flexibility.

Can I have both a Medigap plan and a Medicare Advantage plan at the same time?

No, it is actually illegal for an agent to sell you a Medigap policy if they know you are enrolled in a Medicare Advantage plan. These two types of insurance do not work together and you can only use one at a time. We help you navigate this “crazy maze” by comparing both options side by side. Our goal is to move you from confusion to confidence so you choose the single path that fits your life.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com