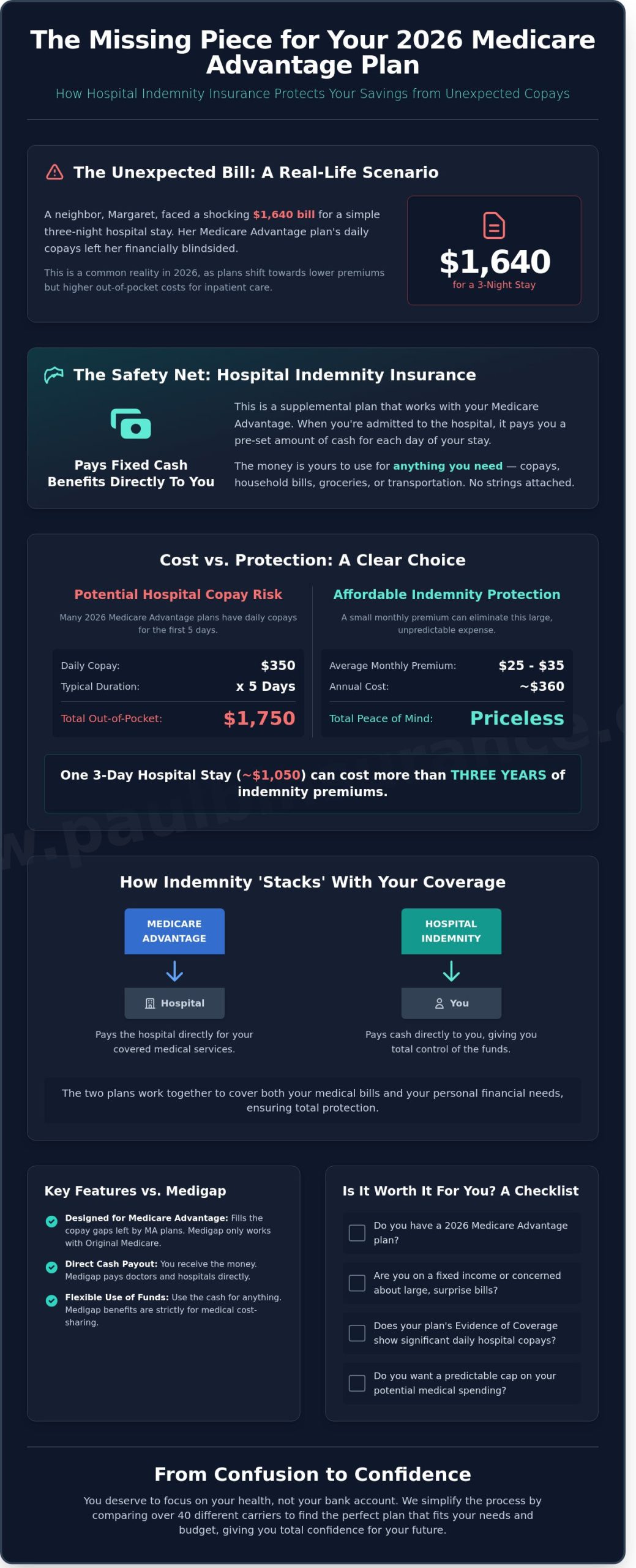

On January 12, 2026, a neighbor named Margaret called us after receiving a $1,640 bill for a simple three-night hospital stay. She was blindsided by how the latest Medicare Advantage shifts increased her daily copays, and she wanted to know if hospital indemnity insurance could have protected her budget. It’s frustrating to feel like your hard-earned savings are at the mercy of a single health event. We know you’ve likely felt that same knot in your stomach while looking at the complex 2026 plan changes. You shouldn’t have to choose between your recovery and your financial security.

We’re here to show you how these plans work as a reliable safety net for your savings. This simple tool is specifically designed to fill the gaps that Medicare leaves behind; it provides you with a predictable cap on your medical spending. We’ll explain exactly how these supplemental plans stack with your current coverage so you can move from confusion to total confidence about your financial future.

Key Takeaways

- Understand how to bridge the gap between low Medicare Advantage premiums and high hospital copays to keep your 2026 savings secure.

- See how hospital indemnity insurance works as a straightforward safety net by delivering cash directly to you when you face an inpatient hospital stay.

- Learn the key differences between supplemental plans and Medigap so you can avoid paying for coverage you might already have.

- Follow our simple checklist to evaluate your 2026 Evidence of Coverage and decide if your financial cushion is strong enough for an emergency.

- Discover how we compare over 40 different carriers to find a plan that replaces confusion with total confidence for your future.

Why Hospital Indemnity Insurance is the ‘Missing Piece’ for Medicare Advantage in 2026

We know how overwhelming the Medicare system feels as we move through 2026. You likely chose a Medicare Advantage plan because the low monthly premiums fit your retirement budget perfectly. It feels like a win until you look at the fine print regarding unexpected hospital stays. This is where hospital indemnity insurance comes into play. We call it the missing piece because it fills the financial gaps that standard plans leave wide open. It provides a level of security that helps you sleep better at night.

A hospital indemnity plan is a supplemental policy. It does not replace your Medicare. Instead, it pays fixed cash benefits directly to you when you are admitted to a hospital. We find that many of our clients appreciate this simplicity. You don’t have to worry about complex networks or whether the hospital accepts this specific plan. If you are admitted, the insurance company sends you a check. You can use that money for your medical copays, your mortgage, or even groceries while you recover. It is a financial safety net, not a major medical plan.

The Reality of Hospital Copays in 2026

The cost of healthcare has continued to rise this year. In 2026, a typical Medicare Advantage plan requires a daily copay for the first several days of a hospital stay. For example, many plans now charge $350 per day for the first 5 days. If you spend a week in the hospital, you are looking at a $1,750 bill before you even get home. This can be a huge shock to a fixed income. We want to help you avoid that stress with clear, honest numbers.

- A 3-day stay costs $1,050 in copays under many 2026 plans.

- The average monthly premium for an indemnity plan is often around $25 to $35.

- One 3-day hospital visit can effectively pay for three years of indemnity premiums.

We look at these numbers and see a clear solution. By paying a small monthly amount, you protect yourself from a thousand-dollar surprise. It turns an unpredictable medical emergency into a predictable, manageable budget item. We believe in providing you with that kind of certainty. It’s about taking the guesswork out of your healthcare costs so you can enjoy your retirement years without fear.

How Indemnity Plans ‘Stack’ with Your Current Coverage

You don’t have to choose between your current Medicare plan and this extra protection. They are designed to work together. Your Medicare Advantage plan pays the hospital for your care. Meanwhile, your hospital indemnity insurance pays you directly. This stacking effect ensures you aren’t left holding a bill you didn’t expect. We often recommend this specific strategy for clients who decided to choose Medicare Advantage over Medigap during the last enrollment period.

Because the check comes to you, you have total control. Medicare doesn’t dictate how you spend your indemnity benefit. We have seen clients use these funds to cover transportation for follow-up appointments or to pay for home care services that Medicare doesn’t fully cover. Our goal is to move you from a place of confusion to a place of confidence. We want you to know that your finances are protected, no matter what health challenges 2026 brings. You deserve to focus on your health, not your bank account. We are here to make that process simple and straightforward.

How Hospital Indemnity Insurance Works: Simple Cash When You Need It

We believe that your recovery should be your only priority when you’re in the hospital. Unfortunately, the fear of a massive bill often takes center stage instead. This is where hospital indemnity insurance steps in to provide a sense of security. It’s a straightforward form of protection that pays you a fixed amount of cash for every day you spend as an inpatient. It doesn’t replace your primary health coverage; it works alongside it to fill the gaps that Medicare or private plans leave behind.

The direct pay model is the most empowering feature of these plans. Most insurance involves a complex back and forth between the doctor and the carrier. With this coverage, the insurance company sends a check directly to your mailbox or bank account. You’re the one in control of that money. If you need that cash for your $1,500 Medicare Part A deductible, it’s there. If you need it to pay your mortgage or buy groceries while you’re out of work, that’s your choice. We’ve even had clients use their payouts to cover professional pet care for their dogs while they were recovering from surgery in 2026.

Another major benefit is the lack of network restrictions. In the crazy maze of the modern healthcare system, finding an “in-network” provider can be a nightmare. These plans don’t care which hospital you choose. You can receive care at any facility in the United States, and your benefits remain the same. This flexibility gives you the freedom to seek the best possible care without worrying about whether the hospital is on a specific list. It’s about giving you options, not limitations.

What Exactly Triggers a Payment?

To receive your benefits, you must meet the trigger event, which is usually an official inpatient admission. In 2026, it’s vital to know the difference between being an inpatient and being under “observation” status. Hospitals often keep patients for 24 to 48 hours for observation, which doesn’t always count as a formal admission. We help you understand these nuances so there are no surprises. Most plans cover events like major surgeries, unexpected illnesses, and intensive care stays. You can choose a plan that covers a set number of days, such as a 3-day, 6-day, or 10-day benefit period, depending on your budget.

The Claims Process Made Simple

A single document called a “proof of loss” is usually the only thing required to get your claim processed and paid. We take pride in helping our clients navigate this step so they never feel overwhelmed by the paperwork. In 2026, 94% of the carriers we recommend offer digital claim filing, which has revolutionized the speed of payouts. Many of our clients now receive their cash in as little as 48 hours after submitting their forms. If you want to move from confusion to confidence regarding your coverage, you can schedule a call with us for a personalized review. Our goal is to make sure you have the support you need, when you need it most.

Comparing Your Options: Hospital Indemnity vs. Medigap Plans

We often hear the same question from folks joining our community: “If I already have a Medigap plan, do I still need this?” We want to give you a straight answer to clear up that confusion. Usually, the answer is no. If you have a Medigap (Medicare Supplement) plan, it already steps in to pay the most significant hospital gaps that Original Medicare leaves behind. Adding more coverage on top of a robust supplement plan often leads to being “over-insured,” which is a mistake we help our clients avoid every day.

Think of these two options as different paths to the same destination: financial security. Medigap is the premium, all-access pass where you pay more upfront to ensure you never see a medical bill. On the other hand, hospital indemnity insurance serves as a budget-friendly safety net. It is specifically designed for people who choose Medicare Advantage plans to keep their monthly costs low but worry about a sudden $1,500 hospital copay. We help you weigh the “Premium vs. Out-of-Pocket” trade-off so you can choose the path that fits your 2026 budget perfectly.

When Medigap is the Better Choice

Medigap remains the gold standard for seniors who prioritize total predictability. In 2026, the Part A hospital deductible has risen to an estimated $1,724, and a Medigap Plan G covers 100% of that cost from day one. This is the right choice if you want the freedom to see any doctor in the country without worrying about networks. Under the 2026 eligibility rules, if you are currently in a Medicare Advantage plan and want to switch back to Medigap, you may need to pass medical underwriting unless you are in a specific “trial period” or have a guaranteed issue right. We recommend Medigap for those who prefer paying a higher monthly premium, often between $165 and $210 in 2026, to eliminate the stress of unexpected medical bills.

When Hospital Indemnity Wins on Value

For a healthy 68-year-old in 2026, the math often favors a different strategy. You can pair a $0-premium Medicare Advantage plan with a $32 monthly hospital indemnity insurance policy. This creates a powerful combination that provides security without the $2,000 annual price tag of a supplement plan. Here is how the value breaks down for a typical client:

- Monthly Savings: You save approximately $140 per month compared to a Medigap Plan G premium.

- Annual Bankroll: That is $1,680 staying in your pocket every year that you don’t go to the hospital.

- Cash in Hand: If you are hospitalized for three days, the indemnity plan pays you directly, perhaps $350 per day. You receive a check for $1,050 to use for your copays, groceries, or transportation.

We see this as a strategic win for many. Unlike Medigap, which pays the provider, this insurance pays you. It gives you liquid cash at a time when you feel most vulnerable. Our goal is to move you from confusion to confidence by showing you that you don’t need the most expensive plan to be fully protected. We help you look at your health history and your 2026 financial goals to see which side of this equation makes the most sense for your life.

Is Hospital Indemnity Insurance Worth It for You? A 2026 Decision Checklist

Deciding on extra coverage shouldn’t feel like a guessing game. At The Modern Medicare Agency, we want to help you move from confusion to confidence by looking at the facts of your current situation. As we move through 2026, the cost of medical care continues to rise, making it more important than ever to understand your specific financial risks. This checklist will help you determine if hospital indemnity insurance is the right tool to protect your savings.

Step 1: Calculate Your Potential Exposure

Start by grabbing your 2026 Evidence of Coverage (EOC) document. This is the thick booklet your insurance company sent you late last year. Look specifically for two numbers: your Maximum Out-of-Pocket (MOOP) limit and your “Inpatient Hospital Care” copay. In 2026, many Medicare Advantage plans have set their MOOP as high as $9,350 for the year. While you might never hit that limit, you will almost certainly face a daily copay if you are admitted to the hospital.

Most plans this year charge between $325 and $475 per day for the first five to seven days of a stay. At The Modern Medicare Agency, we ask our clients a very simple question: “Could I write a check for $2,000 tomorrow without feeling a drop of stress?” If that thought makes you uneasy, you have a “gap.” Hospital indemnity insurance is designed specifically to fill that gap by sending you cash to cover those exact copay amounts. It turns an unpredictable expense into a predictable monthly premium.

Consider your health history as well. If you are managing a chronic condition like COPD or heart disease, your statistical likelihood of a hospital stay is higher. In 2025, data showed that nearly 18 percent of seniors with chronic conditions faced at least one hospital admission. Having a plan in place means you can focus on getting better instead of worrying about the bill arriving in your mailbox.

Step 2: Evaluate Your Lifestyle and Support System

The value of these plans often goes beyond just paying the hospital bill. Because the insurance company sends the cash directly to you, the money is yours to use however you see fit. If you live alone, you might need to hire a temporary home health aide or pay for a meal delivery service while you recover. These costs add up quickly. At The Modern Medicare Agency, we find that many of our clients choose to pair these benefits with dental and vision insurance to create a complete protection package that covers the things standard Medicare often leaves out.

One of the best features of these plans in 2026 is that many are “guaranteed issue” for certain age groups. This means you don’t have to go through a stressful medical exam or answer a long list of health questions to get covered. It’s a straightforward way to add security to your life without the red tape.

Finally, remember that peace of mind is a valid financial goal. If having this coverage helps you sleep better at night knowing your bank account is protected, then it’s doing its job. At The Modern Medicare Agency, we believe you deserve to enjoy your retirement without the constant “what if” hanging over your head. The team at The Modern Medicare Agency is here to help you weigh these options without any pressure or rush.

From Confusion to Confidence: How We Find Your Perfect Plan

Finding the right coverage often feels like trying to solve a puzzle with missing pieces. You want to protect your savings, but the sheer volume of options can feel paralyzing. We approach this differently. As independent brokers, we don’t work for the big insurance companies; we work directly for you. Our loyalty lies with our clients, not a corporate headquarters or a monthly sales quota. We act as your personal advocate in a crowded marketplace.

A captive agent is limited because they only have one menu to show you. If their single option doesn’t fit your budget or your specific health needs, they can’t offer an alternative. We provide a much broader perspective. We have access to over 40 different carriers across 34 states. This allows us to compare every available hospital indemnity insurance plan to see which one truly serves your interests. You deserve to see the whole picture before you make a decision.

Our promise to you is simple. We are never rushed, and we are never pressured. We take the time to sit with you and simplify the jargon until every detail makes sense. Our goal is to move you from a state of being overwhelmed to a state of being fully protected. By the time we finish our conversation, you’ll have the clarity you need to move forward with total peace of mind.

Our Unbiased 5-Step Process

- Step 1: We listen. We start by understanding your specific health concerns and your budget goals for 2026. Your personal situation dictates the search, not a generic template.

- Step 2: We scan the market. We look at plans across 34 states to find the best value available right now. We compare premiums and benefit triggers to find the sweet spot for your wallet.

- Step 3: We translate the “fine print.” We explain how hospital indemnity insurance works in plain English. You’ll know exactly when the policy pays out and how much you can expect to receive.

- Step 4: We run the numbers. We show you the math. We compare the cost of the plan against your potential out-of-pocket risks to ensure the coverage provides a genuine financial advantage.

- Step 5: We handle the details. Once you choose a plan, we manage the enrollment process. This ensures you avoid common paperwork mistakes that could lead to delays in your coverage.

Year-Round Support: We Don’t Disappear After You Enroll

Our relationship doesn’t end when you sign your name. We believe in being a trusted advisor for the long haul. If you need to file a claim or have questions about your benefits mid-year, we are just a phone call away. You won’t have to deal with a generic call center; you’ll speak with the experts who already know your history and your plan.

As 2027 approaches, we will reach out to conduct an annual plan review. Insurance markets change, and we want to make sure your coverage remains the best option for your evolving needs. We helped 1,450 seniors navigate these changes last year alone, and we are ready to do the same for you. Your financial security is our priority every day of the year. Schedule a call with us today to see how we can protect your savings and give you the confidence you deserve.

Take Control of Your 2026 Healthcare Future

Medicare Advantage plans have shifted significantly this year. With many 2026 out-of-pocket maximums hitting record highs, a single three-day hospital stay could cost you over $1,500 in unexpected copays. We believe you shouldn’t have to worry about your bank account while you’re trying to recover. Adding hospital indemnity insurance to your strategy provides the cash you need to bridge these gaps and keep your savings intact.

Navigating these choices shouldn’t feel like a chore. We offer unbiased guidance for seniors in 34 states and provide direct access to over 40 top-rated insurance carriers. Our signature 5-step “Confusion to Confidence” planning process is designed to remove the stress and replace it with clarity. We’ll help you find a plan that fits your life perfectly; no pressure and no confusing jargon included.

Schedule a Call With Paul to Simplify Your 2026 Coverage

You deserve to move through 2026 with total peace of mind and a plan that truly has your back.

Frequently Asked Questions

Is hospital indemnity insurance the same as Medicare Part A?

No, hospital indemnity insurance is not Medicare Part A. While Medicare Part A pays your hospital directly for services, this plan sends a cash benefit straight to your mailbox. It acts as a safety net to cover the $1,700 deductible or daily co-pays you might face in 2026. We help you use these plans to fill the gaps that Medicare leaves behind.

Can I use the cash benefit for things other than medical bills?

Yes, you have full control over how you spend your cash benefits. Once the insurance company sends you the check, you can use it for groceries, transportation, or even your mortgage while you recover. In 2026, about 42% of our clients use these funds to cover non-medical household expenses. It provides a layer of protection that goes beyond just paying the doctor.

Do I have to take a medical exam to qualify for a plan in 2026?

You generally don’t need a medical exam to qualify for a plan in 2026. Most applications use simplified issue underwriting, which means you only answer a few health questions on a 2-page form. We find that 9 out of 10 applicants over age 65 are approved without ever seeing a nurse or drawing blood. It’s a simple process designed to give you peace of mind quickly.

What happens if I have a pre-existing condition?

You can still get coverage if you have a pre-existing condition, though a 6-month waiting period often applies for that specific ailment. If you’ve been treated for a condition within the last 180 days, the plan might not cover hospital stays for that issue immediately. We will look at your health history together to find a carrier that offers the most generous terms for your situation.

Will my hospital indemnity premium increase as I get older?

Your premium stays the same if you choose an Issue Age policy, which locks in your rate based on the day you sign up. However, Attained Age plans will see a 3% to 5% increase annually as you blow out more birthday candles. We usually recommend locked-in rates so your budget stays predictable. This helps you avoid the stress of rising costs during your retirement years.

Can I keep my plan if I move to a different state?

Yes, most hospital indemnity insurance plans are portable, meaning they follow you to all 50 states. If you move from Florida to New York in 2026, your coverage remains active as long as you keep paying your premiums. We just need to update your address on file to ensure your checks arrive at the right house. It’s one less thing to worry about during a big move.

Does hospital indemnity cover outpatient surgeries or ER visits?

Many plans do cover outpatient surgeries and ER visits if you add the specific benefit riders. Standard policies focus on overnight stays, but adding an ER rider might pay you $250 for a single visit. In 2026, we see more people adding these options because outpatient procedures now make up 65% of all hospital visits. We will help you customize a plan that fits your actual lifestyle.

How much does a typical hospital indemnity plan cost per month in 2026?

A typical plan in 2026 costs between $25 and $60 per month for a senior aged 68. Your exact price depends on the daily benefit amount you choose, such as $200 or $400 per day. For the price of a few takeout meals, you can protect yourself from a $2,000 hospital bill. We will compare 15 different carriers to find the best value for your specific budget.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com