What if the most expensive mistake your parents make this year isn’t a bad investment, but a simple misunderstanding of the 2026 Medicare enrollment windows? We know you want the best for your mom and dad, but looking at the maze of Part B premiums that rose to $202.90 this year and the $283 deductibles can feel completely overwhelming. It’s stressful to worry about them losing their trusted doctors or getting hit with lifetime late enrollment penalties because a form wasn’t signed correctly.

If you feel like you’re drowning in jargon, you aren’t alone. This guide provides the help for parents with medicare enrollment you need to move from confusion to confidence, ensuring they have the right coverage without the headache. We will walk you through the legal authorizations you need, the 2026 cost changes you must know, and a simple checklist to protect their health and your peace of mind.

Key Takeaways

- Learn why starting the conversation at age 64 is the best way to avoid stress and ensure your parents are ready for the 2026 enrollment deadlines.

- Discover which specific legal forms, such as the CMS-10106, give you the authority to advocate for your parents’ health coverage and speak with Medicare directly.

- Get a simple guide on performing a “Health Audit” to ensure your parents’ favorite doctors and medications are fully protected in the coming year.

- See how an independent broker provides the help for parents with medicare enrollment by comparing dozens of plans to find an unbiased, perfect fit for your family.

- Clearly weigh the benefits of Medigap versus Medicare Advantage so you can choose the path that offers your parents the most confidence and peace of mind.

Understanding the Basics: How We Start the Medicare Conversation

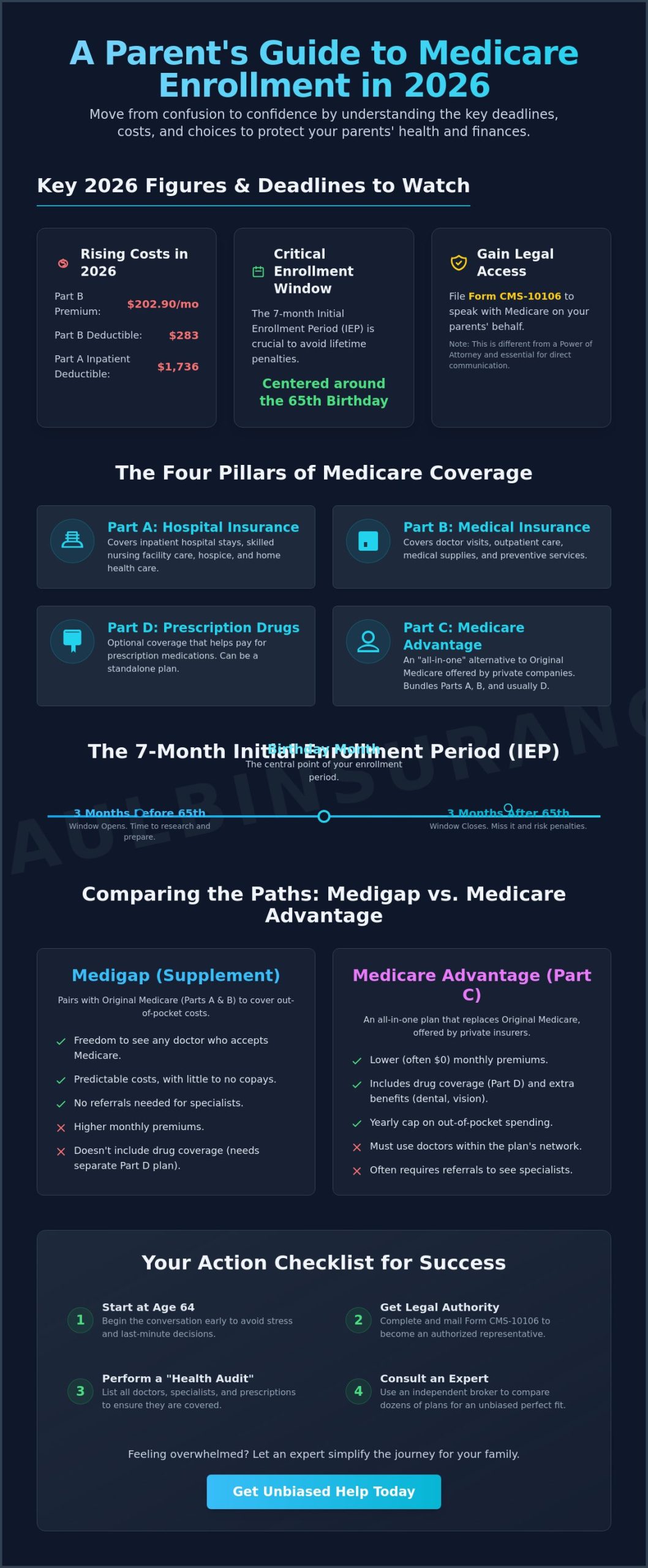

Helping your parents with Medicare isn’t just about filling out forms; it’s about becoming their most trusted advocate. We believe the best way to provide help for parents with medicare enrollment is to start the conversation when they turn 64. This early start removes the pressure and gives your family time to understand the system before the official clock starts ticking. In 2026, with the standard Part B premium sitting at $202.90 and the Part B deductible reaching $283, a single missed deadline or misunderstood benefit can be costly. We are here to help you move from confusion to confidence by breaking down these complex pieces into a simple plan.

The Four Pillars of Medicare Coverage

We find it easiest to view Medicare as a puzzle with four main pieces. At its core, Understanding Medicare Basics means looking at Part A for hospital insurance and Part B for medical services. These two parts form the foundation of their coverage, often called Original Medicare. However, they don’t cover everything. We often see families surprised by the $1,736 inpatient deductible for Part A in 2026. This is where the other pieces come in. You might consider Medicare Part D for prescription drugs or look into Medicare Advantage (Part C) as an all-in-one alternative. We view Medigap as the essential bridge that covers the out-of-pocket costs that Original Medicare leaves behind.

Approaching the Topic with Empathy

Discussing health and money can be delicate. If your parents say “I can handle it,” reassure them that you just want to be their organized backup. We suggest focusing on their specific needs, like keeping their current doctors. In 2026, some insurance companies are reducing their service areas or exiting markets entirely, so checking their provider list is more important than ever. Start by gathering their current insurance cards and a list of their medications. This simple act of organization provides a clear path forward without making them feel overwhelmed or rushed.

The Initial Enrollment Period (IEP) is your primary window for action. It’s a seven-month period that includes:

- The three months before their 65th birthday month.

- The month they turn 65.

- The three months following their birthday month.

Missing this window can lead to permanent late enrollment penalties and gaps in coverage. By acting as the researcher and organizer now, you ensure your parents stay protected and that their transition into Medicare is as smooth as possible.

Taking the Reins: Legal Authorization and HIPAA Forms

One of the most frustrating moments for adult children happens when they call Medicare to resolve a billing error or check a claim, only to be told the representative cannot speak with them. Even if you have the best intentions, privacy laws are designed to protect your parents’ data. This wall can feel like a major roadblock when you are trying to provide help for parents with medicare enrollment. To advocate effectively, you must have the proper legal permissions in place before a crisis occurs. We believe that securing this access is the single most important step in your journey as a caregiver.

The primary tool you need is the “Medicare Authorization to Disclose Personal Health Information” form, also known as CMS-10106. This document allows Medicare to share your parents’ protected health information with you. It is different from a Power of Attorney (POA). While a POA gives you the legal right to make decisions, the CMS-10106 is the specific “key” that opens the door to Medicare’s customer service. We suggest having both. A healthcare POA is vital for long-term planning, but the disclosure form is what makes daily management possible. You can find more details on the mechanics of these forms in the Official Medicare Enrollment Guide provided by the government.

Step-by-Step: Getting Legally Authorized

First, download the CMS-10106 form from the official Medicare website. Your parents must sign it, and you will need to specify how long the authorization lasts. In 2026, Medicare typically takes 14 to 21 days to process these forms once they are mailed. We recommend keeping a scanned copy for your records. If your parents have already chosen a private plan, such as those discussed in our Medicare Advantage guide, you must contact that specific insurance carrier separately. Private companies have their own proprietary HIPAA release forms that they require before they will discuss plan details with a family member.

Managing Digital Access Safely

Digital tools make tracking claims and costs much simpler. We encourage you to help your parents set up a secure “MyMedicare.gov” account. This portal allows you to see their Part B deductible status, which reached $283 in 2026, and track their recent doctor visits. Keep a central “healthcare folder” either physically or in a secure digital vault. This folder should hold their Medicare ID number, portal logins, and copies of all signed authorizations. If you ever feel overwhelmed by these technical hurdles, you can always reach out to us for a clear explanation of how to organize your parents’ files for maximum security and ease of use.

The Medicare Audit: Evaluating Doctors, Drugs, and Dollars

Before you look at a single plan brochure, we recommend performing a complete “Health Audit” for your parents. Most people make the mistake of choosing a plan based on a recognizable brand name or a neighbor’s suggestion. We take a different approach. A thorough audit ensures that the coverage fits your parents’ actual lives, not a generic template. This personalized look is where we provide the most effective help for parents with medicare enrollment, moving your family from a state of worry to a position of total control.

Start by gathering three pieces of information: a list of every medication they take, the names of every specialist they see, and their preferred local hospital. In 2026, many insurers have shifted their provider networks, meaning a doctor who was “in-network” last year might not be today. We help you look at the real numbers, comparing the standard $202.90 Part B premium against the potential out-of-pocket costs of each plan. This step prevents the “sticker shock” that often happens when a parent realizes their favorite cardiologist is no longer covered.

The Prescription Drug Checkup

The year 2026 brings a major relief for families managing high medication costs. Thanks to recent changes, the “donut hole” is a thing of the past. There is now a hard cap of $2,100 on total out-of-pocket drug costs for the entire year. Additionally, insulin copays remain capped at $35 per month. Even with these protections, every plan has a different “formulary,” which is just a list of the drugs they cover and what they charge for them. We suggest using our Medicare Part D guide to see how different plans rank the specific medications your parents need.

- Check if their pharmacy is “preferred” to keep copays at their lowest.

- Verify if any drugs require “prior authorization” before the plan will pay.

- Look for mail-order options that might save your parents a trip to the store.

Provider Network Verification

There is a big difference between a doctor who “accepts Medicare” and one who is “in-network” for a specific plan. If your parents choose a Medicare Advantage plan, they must stay within a specific network to keep costs low. We always recommend calling your parents’ must-have specialists directly. Ask the office manager specifically: “Will you be participating in this specific 2026 plan?” This simple phone call is an essential part of our help for parents with medicare enrollment strategy. It protects the long-term relationships your parents have built with their doctors, ensuring they don’t have to start over with a stranger just because of a plan change.

We believe that your parents deserve to keep the doctors they trust. By verifying these details now, you remove the anxiety of the unknown and replace it with the confidence that their healthcare team remains intact for the coming year.

Comparing the Paths: Medigap vs. Medicare Advantage for Parents

Choosing between Medicare Supplement (Medigap) and Medicare Advantage is the biggest decision you will face. We see many families struggle here because both paths have clear benefits. The right choice depends entirely on your parents’ health needs and your family’s budget. To provide the best help for parents with medicare enrollment, you have to look past the marketing and focus on how they actually use healthcare. In 2026, we are seeing a clear divide in how these plans handle costs and doctor access.

Medigap plans allow your parents to see any doctor in the country who accepts Medicare. There are no networks and no referrals required. Medicare Advantage plans, on the other hand, are often $0 premium options in Georgia for 2026, but they limit your parents to a specific network of providers. While Advantage plans include “extras” like gym memberships, they also come with a Maximum Out-of-Pocket (MOOP) limit that can reach $9,250 this year. We want to make sure you understand the trade-off between low monthly premiums and potential high costs during a health crisis.

Why Medigap is Often the Caregivers Choice

We often recommend Medigap for adult children who live in a different state than their parents. It offers total predictability. If your mom has Medigap Plan G, which 39% of new enrollees chose in early 2026, you know her only major out-of-pocket medical cost is the $283 Part B deductible. After that is met, the plan covers the rest. This makes budgeting simple and removes the stress of unexpected medical bills. You can explore the specific levels of coverage in our Medicare Supplement guide. For many caregivers, the “freedom of choice” to see any specialist without a gatekeeper is worth the monthly premium.

When Medicare Advantage Makes Sense

Medicare Advantage might be the right fit if your parents are relatively healthy and value bundled benefits. These plans often include dental and vision benefits that Original Medicare simply doesn’t provide. However, you must be diligent. In 2026, some insurers are exiting specific counties, which can disrupt care for over a million people nationwide. We suggest reading our Medicare Advantage guide to learn how to spot these changes before they happen. Always verify that their primary hospital is in-network, or they could face massive bills for “out-of-network” care.

If you feel stuck between these two very different paths, we can help you run a side-by-side comparison for your parents’ specific situation. Schedule a consultation with us to find the path that offers your family the most security.

How an Independent Broker Simplifies the Journey for Your Family

We understand that after reviewing the 2026 premiums and the choice between Medigap and Advantage, you might feel like you have taken on a part-time job as an insurance agent. This is exactly where we step in to provide the help for parents with medicare enrollment that makes the process simple again. Unlike a captive agent who only represents one company, we are independent brokers. We compare over 40 different carriers to find the specific plan that fits your parents’ unique health needs and budget. Our goal is to be your unbiased advocate, ensuring your parents never lose their options or their peace of mind.

Our relationship doesn’t end when the enrollment form is signed. Every September, your parents will receive an Annual Notice of Change (ANOC). In 2026, with over a million people facing plan disruptions due to insurers exiting certain markets, this document is more important than ever. With 180 Medicare Advantage plans available in Georgia alone this year, the maze can get crowded. We review these changes for you every year. If a plan is no longer the best fit, we help you pivot before the January 1st deadline. Our “never rushed, never pressured” approach ensures you always have the time to make the right decision for your family.

Moving From Confusion to Confidence

We specialize in translating complex “Medicare-speak” into plain, simple English. Our 5-step process is the core of how we provide help for parents with medicare enrollment, ensuring no detail is missed. We look at everything from verifying doctor networks to checking the 2026 Part D drug formularies for cost savings. We take the burden of enrollment paperwork off your plate entirely. By handling the administrative heavy lifting, we allow you to focus on being a supportive child rather than an unpaid insurance administrator.

Your Next Steps with Paul

You don’t have to spend your weekends reading plan brochures. A simple 15-minute discovery call with us can often save you 15 hours of frustrating research. To prepare for our talk, just have your parents’ current medication list and their preferred doctors ready. We will listen, answer your questions, and start building a clear path forward. If you are ready to move from a state of overwhelm to total confidence, we invite you to Schedule a Call With Paul today. We are here to protect your parents and simplify your life.

Move Toward a Stress-Free Medicare Future for Your Family

You have taken a big step today by learning how to protect your parents’ health and finances. From securing legal authorization to performing a thorough health audit, you now have the tools to ensure they aren’t surprised by the $283 Part B deductible or the $9,250 out-of-pocket limits seen in 2026. This journey doesn’t have to be a solo mission. We provide the help for parents with medicare enrollment that turns a confusing maze into a clear, manageable plan.

Paul Barrett and our team offer personalized, unbiased guidance backed by access to 40+ insurance carriers. We are licensed in over 34 states and dedicated to finding the perfect fit for your family’s specific needs. Schedule a Free Medicare Consultation for Your Parents today. You’ve done the hard work of researching; now let us handle the heavy lifting so you can focus on being a supportive child rather than an admin. We look forward to helping you move from confusion to confidence with a plan you can trust.

Frequently Asked Questions

Can I sign my parents up for Medicare without them being present?

No, you cannot sign them up without their consent or legal authorization like a Power of Attorney or a signed CMS-10106 form. Even with these documents, the Social Security Administration often requires the parent’s signature on the actual application. We help you navigate these legal hurdles so you have the right permissions ready when the enrollment window opens.

What happens if my parents miss their Medicare enrollment deadline in 2026?

Missing the deadline triggers lifetime late enrollment penalties and delays coverage until the next General Enrollment Period, which runs from January 1 to March 31, 2026. For Part B, your parents will pay an extra 10% on their premium for every 12-month period they were eligible but not enrolled. We provide the help for parents with medicare enrollment needed to avoid these permanent costs.

Is there a fee to work with an independent Medicare broker?

We don’t charge a fee for our services because we are compensated by the insurance companies. This allows us to provide unbiased, expert guidance at no cost to your family. You get access to our comparison of 40+ carriers while your parents’ premiums remain exactly the same as if they had signed up alone.

How do I know if my parents’ doctors will accept their new Medicare plan?

You must check the plan’s specific 2026 provider directory or call the doctor’s office directly to confirm they are in-network. While Original Medicare is accepted by 98% of doctors nationwide, Medicare Advantage plans have restricted networks that can change annually. We assist you by running a provider search to ensure their must-have specialists are included.

What is the best Medicare plan for a parent with many prescriptions?

The best plan is one that includes their specific medications on its “preferred” list at a pharmacy they find convenient. In 2026, the $2,100 out-of-pocket cap makes Part D more affordable than ever. We help for parents with medicare enrollment by analyzing their current prescriptions to find the plan with the lowest total annual cost.

Does Medicare cover long-term nursing home care for my parents?

Medicare doesn’t cover long-term custodial care, but it does cover up to 100 days of skilled nursing care following a hospital stay. In 2026, the first 20 days are covered at 100%, while days 21 through 100 require a $217 daily coinsurance. For true long-term care, we can discuss separate insurance options that protect your parents’ assets.

Can I change my parents’ Medicare plan later if their health needs change?

Yes, you can change their coverage during the Annual Election Period, which occurs every year from October 15 to December 7. If they have a Medicare Advantage plan, they also have a second window from January 1 to March 31, 2026, to switch plans or return to Original Medicare. We provide year-round support to ensure their coverage evolves with their health.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com