Last Tuesday, Margaret sat at her kitchen table surrounded by 14 different glossy mailers, feeling more lost than when she started. She wanted to know how to create a medicare comparison spreadsheet to make sense of the new 2026 Part D cost-sharing caps, but the mountain of paperwork made her feel anything but safe. We know how overwhelming it is to stare at a pile of brochures while trying to guess if a lower premium is worth a higher out-of-pocket maximum. You shouldn’t have to be a math expert to get the healthcare you deserve.

We are going to show you exactly how to build a custom tool that cuts through the noise and brings you peace of mind. We’ll help you compare Medigap and Medicare Advantage side-by-side, ensuring you don’t miss a single detail about the 2026 benefit structures. This guide provides a simple, step-by-step process to help you find the clear winner for your health and your budget. You will finish with a shareable document that proves you are choosing your 2026 coverage with total confidence.

Key Takeaways

- We help you navigate the 40+ carriers and hundreds of plan combinations available this year so you can move from confusion to complete confidence.

- Learn exactly how to create a medicare comparison spreadsheet to organize premiums and deductibles, making it easy to see which 2026 plans truly protect your savings.

- We show you how to compare the predictable fixed costs of Medigap against the variable expenses of Advantage plans to find your perfect financial fit.

- Discover why the 2026 Part D cap is a game-changer for your budget and how to factor this new limit into your side-by-side analysis.

- Understand why a spreadsheet is just the first step and how we help you spot “fine print” issues like doctor network stability that data alone might miss.

Why You Need a Custom Medicare Comparison Spreadsheet in 2026

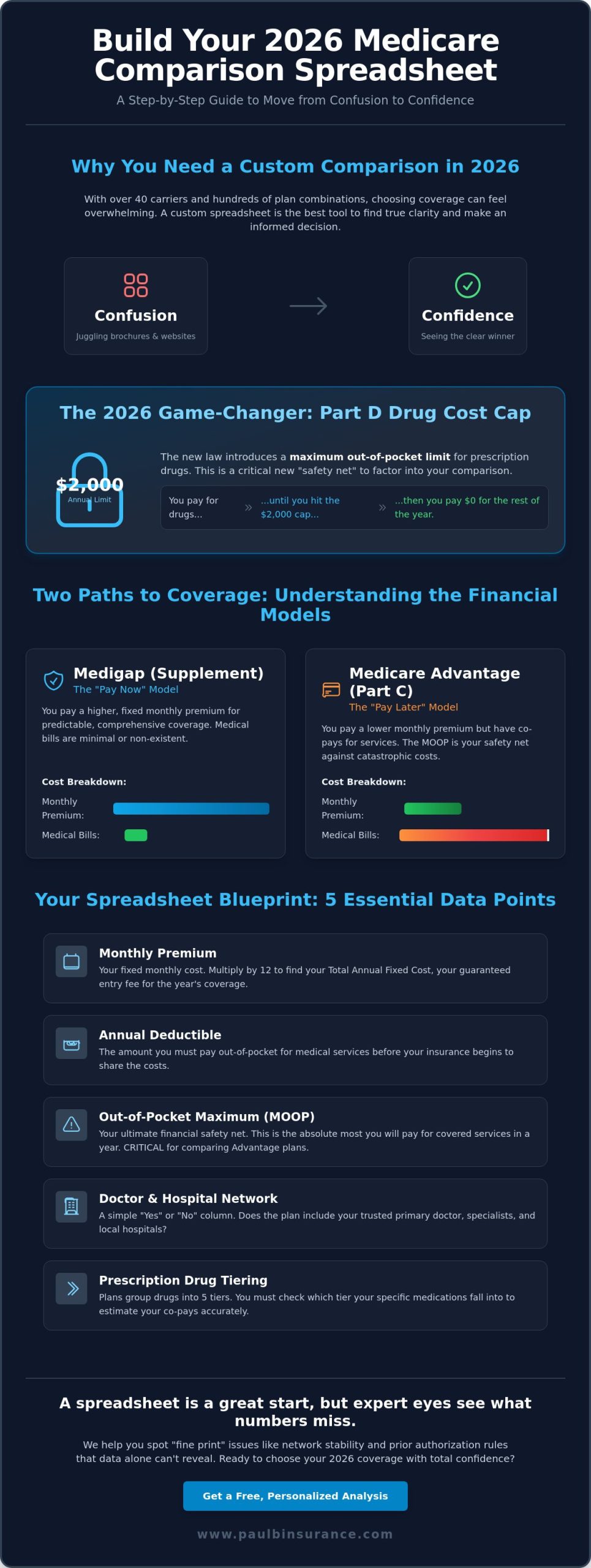

Choosing a plan in 2026 feels like staring at a wall of static. With over 40 carriers and hundreds of plan combinations available this year, your brain can quickly feel fried. We know that feeling of being overwhelmed. It’s why we believe learning how to create a medicare comparison spreadsheet is the only way to find true clarity. You need a tool that lets you see the whole picture at once, rather than clicking through dozens of tabs on a website. A custom sheet puts you back in the driver’s seat.

Many people start by understanding the basics of Medicare, but they get stuck when they see how much has changed lately. Old templates from 2024 or 2025 are now obsolete because the math simply isn’t the same. While the official Medicare.gov Plan Finder is a decent starting point, it has limitations for personal record-keeping. It doesn’t let you easily compare your history or track how a specific doctor’s visit might cost you across five different plans over several years. We use a “Confidence over Confusion” mindset at The Modern Medicare Agency. Our job is to act as your patient guide, removing the anxiety from this complex process so you can make a choice you won’t regret.

The 2026 Part D Revolution

This year marks a massive shift in how we track drug costs. The new $2,000 out-of-pocket limit for prescription drugs is now the law of the land. This means your spreadsheet must track cost-sharing differently than in previous years. Once you hit that $2,000 threshold, your costs drop to zero for the rest of the year. We’ve updated our logic to help you see exactly when you’ll reach that cap. You can read more in our Medicare Part D guide to understand how these new rules protect your retirement savings from high-cost specialty medications.

Medigap vs. Advantage: Two Different Spreadsheet Logics

You can’t compare Medigap and Medicare Advantage using the exact same columns. They are two entirely different financial models. Medigap is the “Pay Now” model. You pay a higher monthly premium, but your medical bills are almost non-existent. Medicare Advantage is the “Pay Later” model. You enjoy lower monthly premiums, but you pay co-pays as you go. To find the best fit, how to create a medicare comparison spreadsheet requires setting up two distinct sections. We’ll help you track the “Maximum Out-of-Pocket” for Advantage plans while focusing on premium stability for Medigap. This ensures you’re comparing apples to apples and not getting lost in the jargon.

The Essential Columns: What Data Points to Collect

When you start learning how to create a medicare comparison spreadsheet, the goal is to move from confusion to confidence. We want to help you build a tool that makes the right choice obvious for your 2026 health needs. To do this, you need to track specific data points for every plan you consider. Start by creating a header row with these five categories.

- Monthly Premium: This is your fixed cost. You pay this amount every month to keep the plan active, even if you never visit a doctor.

- Annual Deductible: For the 2026 coverage year, this is the amount you must pay out of your own pocket before your insurance starts sharing the costs.

- Out-of-Pocket Maximum (MOOP): Think of this as your financial safety net. It is the absolute most you will pay for covered medical services in a calendar year.

- Doctor and Hospital Network: This is a simple yes or no column. Does the plan include your trusted primary doctor and local specialists?

- Prescription Drug Tiering: Different plans group medications into 5 distinct tiers. You need to know if your specific meds fall into a low-cost or high-cost category.

You can find these specific numbers on the official Medicare website during the enrollment period. Having this data in one place removes the stress of flipping through dozens of paper brochures. We find that seeing the numbers side-by-side immediately lowers the anxiety of the decision process.

Financial Metrics You Can’t Ignore

We recommend adding a column for Total Annual Fixed Cost. You calculate this by multiplying your monthly premium by 12. This number represents your entry fee for the year. However, the most important column for those looking at Medicare Advantage is the MOOP. Since these plans often have lower premiums, the MOOP tells you the worst-case scenario for your savings if a health crisis occurs. We also suggest an Estimated Total Cost column. This combines your fixed premiums with expected copays for regular visits, giving you a realistic budget for 2026.

Qualitative Columns for Better Decisions

Numbers don’t tell the whole story. We suggest adding a Network Flexibility rating from 1 to 10. A plan that requires referrals for every specialist might get a 3, while a plan that lets you see any provider might get a 9. You should also track extra benefits like fitness memberships or transportation. Many of our clients find that standard plans lack enough coverage for their teeth, so we often suggest looking at dental insurance options to fill those gaps. If the spreadsheet feels like a lot to handle, you can always schedule a call with us to walk through these columns together. We believe that learning how to create a medicare comparison spreadsheet is the first step toward a worry-free retirement.

Step-by-Step: Building Your Medicare Comparison Sheet

We want to move you from a state of confusion to total confidence. Learning how to create a medicare comparison spreadsheet is the most effective way to see through the marketing noise. First, choose your tool. We suggest Google Sheets if you want to collaborate with a spouse or a trusted advisor. If you prefer keeping your health data on your own computer, Microsoft Excel is the better choice for privacy. Both platforms allow us to organize messy data into a clear, logical path.

Start by setting up your header row with the categories we listed earlier. Your very first entry should be your current coverage. We call this your “Baseline” plan. Seeing your current costs side-by-side with 2026 options helps you realize if a change is actually necessary. We often find that seniors feel pressured to switch when their current plan is actually performing well. Once your baseline is set, pick 3 to 5 top-rated plans to evaluate. You can find these by looking at quality of care initiatives and star ratings to ensure the companies have a history of treating members fairly.

The most vital number you will calculate is the “Max Possible Spend.” To find this, multiply your monthly premium by 12 and add the plan’s Maximum Out-of-Pocket (MOOP) limit. This number represents your total financial risk for the year. It gives you peace of mind to know exactly what the worst-case scenario looks like for your bank account. Knowing your risk is the first step toward true security.

How to Find Accurate 2026 Data

The Summary of Benefits is the gold standard for data because it acts as the legal contract of what is covered. You can download these PDFs directly from insurance company websites or the official Medicare portal. We urge you to stay away from third-party lead generation sites. These sites often use outdated 2025 figures or generic averages that don’t apply to your specific zip code. If you are looking at a Medicare Advantage Guide, always verify the specific network for your county before entering it into your sheet.

Using Formulas to Automate Your Math

We don’t want you to spend hours with a calculator. Use a simple SUM formula to annualize your costs. For example, if your premium is in cell B2, use =(B2*12) to see the yearly total. You can also use “IF” statements to protect yourself. A formula like =IF(D2="No", "WARNING", "OK") can instantly flag any plan that doesn’t include your primary doctor. Finally, use conditional formatting to color-code your results. We recommend setting “Green” for low-risk plans and “Red” for any plan where the total spend exceeds your comfort level. This visual map makes the right choice obvious and removes the anxiety from your decision.

Analyzing the Results: Medigap vs. Medicare Advantage

Now that you’ve filled in the numbers, your spreadsheet will start telling a story. It’s a journey from confusion to confidence. When you look at the columns, you’ll see two very different paths for your 2026 healthcare coverage. One path prioritizes predictable costs, while the other focuses on low monthly overhead. Seeing these side by side is the best way to remove the anxiety from your decision.

The Medigap Advantage in Your Sheet

Medigap rows often show a higher monthly cost. This is your “Fixed Cost.” You pay the premium, and in return, your medical bills stay predictable. We like to call this budget stability. If you check our Medigap overview, you’ll see how these plans eliminate the fear of a surprise $5,000 hospital bill. The biggest win here is the “Freedom Factor.” You don’t need to check if a doctor is in a network. If they accept Medicare, you’re covered. This is why many people who travel or have specific specialists prefer this route. Your spreadsheet will show higher premiums but almost zero co-pays for medical services.

The Medicare Advantage Value Proposition

Medicare Advantage plans often start with a $0 premium. This makes your spreadsheet look very attractive at first. These plans use “Variable Costs,” meaning you pay as you go through co-pays. For 2026, many plans include extra perks like dental, vision, and hearing. You can find more details in our Medicare Advantage Guide. Just remember to factor in the cost of staying within a specific network of doctors. If you’re healthy and rarely visit the doctor, the “Total Annual Cost” column for Advantage might look much lower than Medigap.

The 2026 Part D rules are a game changer for your analysis. The new $2,000 out-of-pocket cap on prescription drugs applies to both paths. This levels the playing field significantly. Whether you choose Medigap or Advantage, your pharmacy costs won’t spiral out of control. This cap means you no longer have to worry about the “donut hole” that used to cause so much stress.

To find your break-even point, look at your “Total Annual Cost” column. If you have three or more specialist visits a month, the “lower” premium of an Advantage plan might actually cost you more than a Medigap premium by October. This is why learning how to create a medicare comparison spreadsheet is so vital for your peace of mind. It reveals the hidden costs that a simple brochure might hide. We want you to feel empowered by these numbers, not overwhelmed by them.

Beyond the Spreadsheet: Why Expert Eyes Matter

You’ve put in the hard work to learn how to create a medicare comparison spreadsheet. Organizing your data is a massive win, and it puts you ahead of most people entering the system this year. However, a spreadsheet is a static tool, while the insurance market is constantly shifting. A cell in Excel can’t read the fine print of a provider contract or warn you about restrictive “prior authorization” rules that can delay your care.

We see “Network Stability” issues every single year. A doctor might be in a plan’s network on January 1, 2026, but they can choose to leave that plan mid-year. Your spreadsheet won’t alert you to which carriers have a history of losing major hospital systems. We track these trends across more than 40 carriers. We help you choose a plan that’s likely to remain stable so you don’t have to start this process all over again in six months.

At The Modern Medicare Agency, we use professional enrollment software to verify your DIY math. Our systems pull real-time data directly from carrier databases. This allows us to double check your formulas and ensure the numbers you’ve gathered match the actual costs you’ll see on your medical bills. We act as your unbiased advocate, making sure the plan you picked on paper actually performs in real life.

Common Spreadsheet Mistakes to Avoid

- Missing the Part B Premium: Many people forget to add the standard Part B premium to their monthly cost. For 2026, the estimated premium is $185.00. You must pay this even if your Advantage plan has a $0 premium.

- Miscalculating Tier 3 Drugs: Tier 1 and 2 drugs usually have flat copays. Tier 3 “preferred brand” drugs often require you to pay a percentage of the cost, which can fluctuate.

- Network Nuances: An HMO requires referrals and strictly stays in-network. A PPO offers more freedom but costs significantly more if you see an out-of-network provider.

From Confusion to Confidence

You’ve already done the heavy lifting by organizing your options. Now, let’s make sure that data leads to the right decision. We want to help you move from a state of confusion to a state of total confidence. We invite you to join us for a “Spreadsheet Review” call where we can look at your findings together. We’ll simplify the jargon and ensure you haven’t missed any hidden costs. Our goal is to protect you from late penalties and expensive enrollment errors. You’ve built the foundation; let us help you finish the house. Schedule a Call With Paul today to get your personalized review.

Take Control of Your 2026 Medicare Journey

Learning how to create a medicare comparison spreadsheet is a powerful first step toward gaining clarity. You now have the tools to track 2026 deductibles and compare the network limitations of various plans side by side. This organized approach helps you see through the noise of the insurance system so you can focus on what matters most. While data is vital, even the best sheet can’t capture every nuance of the 40 plus carriers we represent across 34 states. We provide year round support to ensure your coverage fits your life perfectly without any hidden surprises. Paul Barrett and our team act as your personal advocates; we simplify the jargon and remove the stress from the process. We’re here to make sure you don’t miss a single detail or face a costly late penalty. You deserve to feel certain about your healthcare future.

Ready to move from confusion to confidence? Schedule a call with us today.

We’re ready to help you turn that data into a solid plan for a worry free 2026.

Frequently Asked Questions

Is there a free Medicare comparison spreadsheet template for 2026?

Yes, we provide a free 2026 Medicare comparison spreadsheet template on our website to help you organize your options. While the official Medicare.gov Plan Finder allows you to export drug lists, our custom template includes specific columns for the latest 2026 legislative changes. This tool helps you move from confusion to confidence by laying out premiums and deductibles in one clear, simple view.

What is the most important column to have in my Medicare spreadsheet?

The Maximum Out-of-Pocket, or MOOP, column is the most critical entry in your spreadsheet. For 2026, the CMS has set specific limits on these amounts for Medicare Advantage plans to protect you from high medical bills. While the monthly premium is easy to see, the MOOP tells you the absolute most you’ll pay for covered services in a single calendar year if a major health event occurs.

How do I compare Medicare Part D plans in my spreadsheet with the new $2,000 cap?

You should create a column for Estimated Annual Drug Costs and cap it at $2,000 for your 2026 planning. Since the Inflation Reduction Act now limits your out-of-pocket prescription spending to this amount, you don’t need to worry about the old donut hole. We suggest adding a row to note if the plan offers the Medicare Prescription Payment Plan, which lets you spread these costs over 12 months.

Can I use a spreadsheet to compare Medigap and Medicare Advantage side-by-side?

Yes, you can use a spreadsheet to compare Medigap and Medicare Advantage side-by-side by focusing on total annual costs. Learning how to create a medicare comparison spreadsheet involves listing the higher monthly premiums of Medigap against the lower premiums of Advantage plans. You’ll see that Medigap offers more predictable costs, while Advantage plans often include extra benefits like dental and vision that require separate rows for a fair comparison.

How often should I update my Medicare comparison spreadsheet?

We recommend updating your spreadsheet every October during the Annual Enrollment Period. Plans change their drug lists and provider networks every year, and the 2026 landscape is different than it was in 2025. By reviewing your data between October 15 and December 7, you ensure your coverage still fits your health needs and budget. This simple annual habit prevents you from staying in a plan that has become too expensive.

Should I include my spouse’s Medicare info on the same spreadsheet?

We suggest using separate tabs within the same file for you and your spouse. Since Medicare is individual coverage, your medications and doctor preferences will likely differ. Keeping the data on separate sheets prevents confusion while allowing you to see the total household healthcare budget in one place. This organized approach helps both of you feel more secure and less overwhelmed by the decision making process.

What are the most common data entry errors in Medicare planning?

The most common error is forgetting to include the standard Part B premium, which is a required monthly cost for most beneficiaries. Another mistake is entering retail drug prices when your plan requires preferred pharmacy pricing to get the lowest rate. These small data errors can make a plan look cheaper than it actually is. We help you double check these numbers so you don’t face an unexpected bill later in the year.

Can a Medicare broker help me fill out my comparison worksheet?

Absolutely, an independent broker is your best resource when you’re learning how to create a medicare comparison spreadsheet. We do the heavy lifting by pulling accurate data from multiple insurance carriers to fill in the gaps for you. Our goal is to serve as your patient guide, ensuring every number is verified and every benefit is explained. This partnership moves you from a state of stress to total peace of mind without any pressure.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com