On January 12, 2026, a client named Elena sat in our office feeling overwhelmed because she thought her status as a permanent resident meant she would be denied health coverage. She’s not alone; many seniors feel that same knot in their stomach when they look at the complex insurance rules for the coming year. We know you’ve worked hard to build a life here, and the last thing you need is a denied application or a surprise bill for high premiums.

We believe medicare enrollment for green card holders should be simple and stress-free. Whether you’ve been here for six years or are just approaching your fifth anniversary, we’re here to help you move from confusion to confidence. We’ll explain exactly how to qualify under the latest residency rules and what your total costs will look like in 2026. We’re going to walk through the 5-year residency requirement, the specific enrollment timeline, and how to avoid the common mistakes that lead to late enrollment penalties.

Key Takeaways

- We clarify how Lawful Permanent Residents still qualify for coverage in 2026, ensuring you stay protected under the latest residency rules.

- Understand the two specific paths to medicare enrollment for green card holders, whether you have a U.S. work history or meet the five-year residency requirement.

- Learn the simple step-by-step process for gathering your documents and contacting the Social Security Administration at the right time to avoid delays.

- We break down the 2026 premium estimates and “buy-in” options so you can plan your healthcare budget with total peace of mind.

- Discover how our expert guidance helps you steer clear of costly enrollment mistakes and moves you from a state of confusion to total confidence.

Understanding Medicare Eligibility for Green Card Holders in 2026

We know that moving through the maze of healthcare can feel like a heavy burden. If you’re a Lawful Permanent Resident (LPR), the rules might seem complex, but we’re here to clear the path for you. As of 2026, the process for medicare enrollment for green card holders remains a stable and reliable way to secure your health as you age. Our goal is to move you from a place of confusion to a state of total confidence.

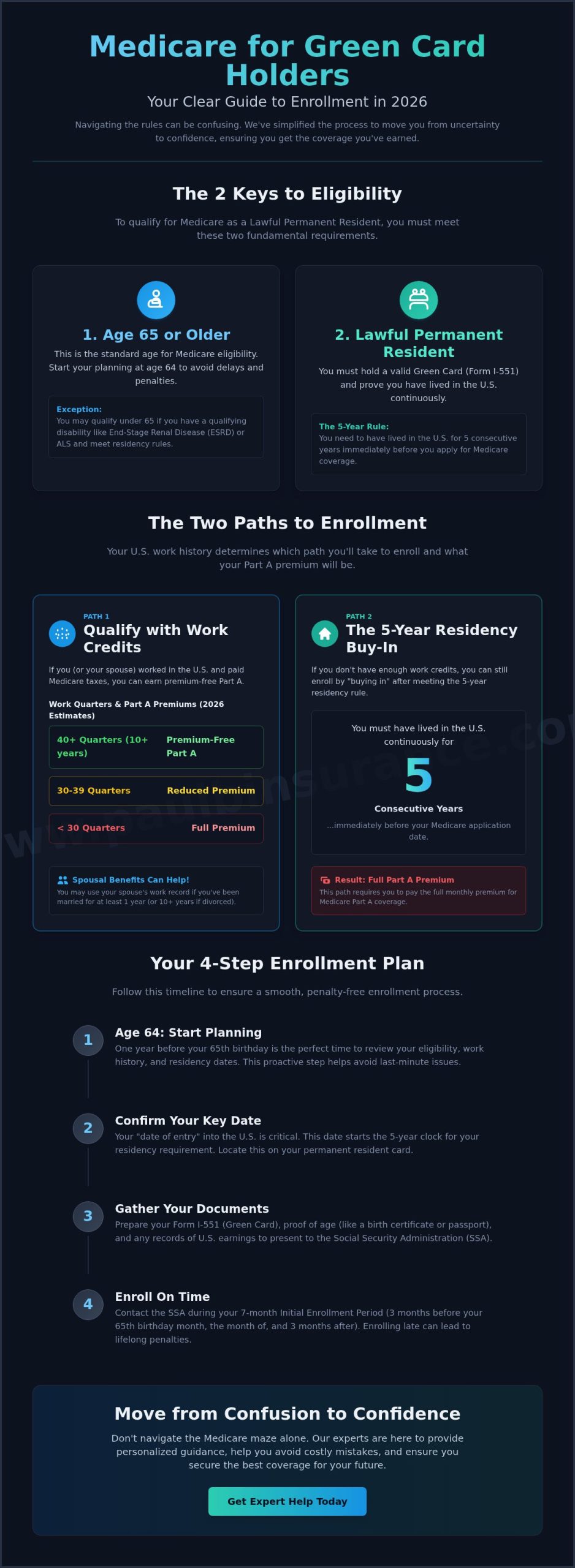

Think of your eligibility as a simple “Rule of Two.” To qualify for the program, you generally need to meet two specific markers. First, you must be at least 65 years old. Second, you must meet the residency requirements. We often see seniors worry that they aren’t eligible because they aren’t yet U.S. citizens, but that’s a common misconception. Your status as a permanent resident is enough to get you started, provided you’ve followed the timeline correctly.

Who is considered “Lawfully Present” today?

To qualify, you must hold a valid Green Card, which is officially known as Form I-551. A policy shift that took effect on January 1, 2025, clarified how the government views “lawful presence” for insurance purposes. This update narrowed the field to focus primarily on LPRs and residents from the Compact of Free Association (COFA) nations. While some temporary visa categories now face stricter limits, your status as a Green Card holder protects your right to apply. We focus on your “continuous residency” during this stage. It isn’t just about having the card in your wallet. You must show that you’ve lived in the U.S. for five years straight before your coverage can begin.

The age 65 milestone

For most of our clients, 65 is the magic number. This is the age when the door to the Medicare program overview opens for you. You don’t have to wait for citizenship to access these benefits. If you’ve reached 65 and met the five-year residency rule, you’re ready to move forward. We always suggest you start your planning at age 64. This gives us 12 months to organize your documents and protect you from costly late enrollment penalties. If you’re under 65, you might still qualify if you’ve lived here for five years and have a qualifying disability, such as End-Stage Renal Disease (ESRD) or ALS.

Your date of entry into the United States is the most important piece of information you own. It determines exactly when your five-year clock started ticking. We use this specific date to ensure your medicare enrollment for green card holders happens at the exact right moment. Knowing this date helps us steer you clear of mistakes and ensures you get the protection you deserve without any unnecessary delays.

The Two Paths to Medicare: Work History vs. The 5-Year Rule

We know that figuring out Medicare enrollment for green card holders feels like trying to solve a puzzle with missing pieces. It’s common to feel a bit overwhelmed by the rules, but we’re here to help you find the clear path forward. In 2026, the system still looks at two main factors to decide if you qualify: how long you’ve worked in the U.S. and how long you’ve lived here as a legal resident. We’ll simplify these options so you can move from confusion to confidence.

Path 1: Qualifying through U.S. work credits

Most people qualify for Medicare through their work history. To get premium-free Part A, you generally need 40 “quarters” of coverage, which equals about 10 years of work. For the year 2026, you earn one credit for every $1,900 in covered earnings. You can earn a maximum of four credits per year. If you don’t have the full 40 quarters, you aren’t disqualified, but you’ll likely have to pay a monthly premium for Part A.

- 30 to 39 quarters: You’ll pay a reduced monthly premium for Part A.

- Fewer than 30 quarters: You’ll pay the full standard premium for Part A.

- Spousal History: We often find that clients can qualify based on a spouse’s work record. If you’ve been married for at least one year and your spouse is 62 or older, you might be able to use their credits. This even applies to divorced spouses if the marriage lasted 10 years or more.

Path 2: The 5-year residency buy-in

If you didn’t work in the U.S. long enough to earn credits, you can still enroll through the residency “buy-in” method. This path requires you to be a lawful permanent resident who has lived in the U.S. continuously for the five years immediately before you apply. You can check the Social Security Administration Medicare information pages for the most current documentation requirements for your application.

Continuous residence doesn’t mean you can never leave the country. However, we advise being careful with long trips. If you’re outside the U.S. for more than six months at a time, the government might decide your residency wasn’t “continuous,” which could reset your five-year clock. You must also be physically present in the U.S. when you actually file your paperwork. This rule ensures that medicare enrollment for green card holders is reserved for those who have truly made the U.S. their permanent home.

We want to make sure you steer clear of costly enrollment mistakes. If you’re wondering how your specific residency dates affect your choices, you can explore our Medicare Advantage guide to see how these plans provide extra support once your eligibility is confirmed.

How to Enroll in Medicare as a Permanent Resident

Starting the enrollment process can feel like a heavy burden. We know the stress of trying to get every detail right. Our goal is to move you from confusion to confidence by breaking this down into four simple steps. We simplify the jargon so you know exactly how the system works for you in 2026.

- Step 1: Collect your permanent resident card, also known as the I-551. You will also need documents that prove you have lived in the United States for at least five years without leaving for long periods.

- Step 2: Contact the government. You should start this process exactly three months before you turn 65. You can find essential details through the Social Security Administration Medicare Information portal to begin your application.

- Step 3: Choose the right coverage style. You can stay with Original Medicare and add a Medigap plan to cover the gaps, or you can look into Medicare Advantage plans.

- Step 4: Secure your prescriptions. Even if you don’t take many medications now, you need to select a Medicare Part D plan to avoid permanent late enrollment penalties that could cost you for years to come.

When is your Initial Enrollment Period (IEP)?

Your IEP is a critical seven month window. It begins three months before your 65th birthday month, includes your birthday month, and continues for three months after. Timing is everything. If you wait until your birthday month or later to sign up, your coverage might not start on day one. This creates a gap in protection that we want to help you avoid. If you are still working in 2026 and have insurance through a large employer, you might qualify for a Special Enrollment Period later. This allows you to delay Medicare without any penalties while you keep your current work benefits.

Required documentation for non-citizens

The medicare enrollment for green card holders requires specific physical evidence. You must present your original Green Card. Photocopies are rarely accepted by the SSA. You also need to prove your five year residency. We recommend gathering five years of federal tax returns, lease agreements, or utility bills from 2021 through 2025. Organizing this paperwork maze is where many seniors feel most overwhelmed. We provide the guidance you need to get these documents ready before you ever pick up the phone. Our process ensures you are never rushed and never pressured while you prepare your application.

Securing medicare enrollment for green card holders is a major milestone in your life in the United States. By following these steps, you protect your health and your finances. We are here to ensure you make these choices with total clarity and peace of mind.

Understanding Your Costs and Coverage Options

We know that seeing the price tag on healthcare can feel overwhelming. Medicare enrollment for green card holders involves a few costs that differ from those of lifelong citizens, but we are here to make the numbers clear. If you have lived in the U.S. for at least five years but haven’t worked 40 quarters (10 years) yet, you will likely need to “buy in” to Medicare Part A. For 2026, the estimated full monthly premium for Part A is $532. If you have earned at least 30 work credits, that cost drops to approximately $293. We help you review your work history so you know exactly what to expect on your monthly bill.

The Part B premium is much more straightforward. In 2026, most people pay about $188.50 per month. This rate is the same for everyone, whether you are a new resident or a naturalized citizen. We focus on these details so you can plan your budget with total confidence. You shouldn’t have to guess about your future expenses.

Medigap vs. Medicare Advantage for LPRs

Choosing the right path after you enroll in Parts A and B is a big decision. Medigap plans are designed to act as a safety net. They pay for the 20% of costs that Original Medicare doesn’t cover, which protects you from massive hospital bills. These plans are often the best choice if you travel back to your home country. They don’t restrict you to a local network of doctors. You can see any provider in the U.S. that accepts Medicare.

If you prefer a more bundled approach, Medicare Advantage Plans might be the right fit. These plans often have very low monthly premiums. They combine your hospital, medical, and drug coverage into one simple card. Many of our clients appreciate the extra benefits these plans include, such as vision care or fitness memberships. We will help you compare these options side by side to see which one fits your lifestyle best.

Prescription Drug Coverage (Part D)

You need to sign up for Medicare Part D as soon as you are eligible. Even if you don’t take many medications today, waiting can lead to a permanent late enrollment penalty. This penalty is added to your premium every month for the rest of your life. We want to help you avoid that unnecessary cost from day one.

The year 2026 is an excellent time to be on Medicare because of new consumer protections. Thanks to the Inflation Reduction Act, your out-of-pocket drug costs are capped at $2,000 for the year. This means once you spend $2,000 on covered prescriptions, your plan pays 100% of the remaining costs. It is a huge relief for seniors who worry about rising pharmacy prices. We can look at your current medications together to ensure your plan covers everything you need.

Don’t let the complexity of the system keep you from the care you deserve. Get a clear, personalized Medicare cost breakdown today.

Navigating the Maze: How We Help You Secure Your Future

We understand that looking at insurance options feels like wandering through a maze without a map. Our mission is to lead you from a state of confusion to confidence. We believe every resident deserves a clear path to healthcare, regardless of where they were born. Medicare enrollment for green card holders involves unique hurdles, especially regarding the five year residency rule and Social Security work credits. We don’t just give you a brochure; we provide a dedicated partner who understands these nuances deeply.

Our team takes the time to compare over 40 different insurance carriers. This variety is vital because your residency timeline might make certain plans more beneficial than others in 2026. We follow a “Never Rushed” promise. This means we sit with you, listen to your story, and explain the rules in plain English. We won’t move forward until you feel empowered by your choices. You’re not just a number on a spreadsheet to us; you’re a neighbor we want to protect.

Avoiding costly enrollment mistakes

Many people start their journey by talking to a captive agent. These agents work for only one insurance company, so their advice is limited to what that single company offers. We take an independent, unbiased approach. This is crucial because a single mistake regarding your entry dates or residency status can lead to a permanent 10% late enrollment penalty. In 2026, with healthcare costs evolving, you can’t afford a lifetime of extra fees. We stay by your side year-round, not just during the busy fall season, to ensure your coverage remains accurate as your life changes.

Your next steps toward peace of mind

Waiting until you turn 65 to think about Medicare is a common trap. If you are a green card holder, you need to verify your five year continuous residency status well in advance. We suggest starting this conversation early to avoid any gaps in coverage. We invite you to experience a simple, no-pressure consultation where we answer your questions without the sales pitch. We’ll look at the 2026 plan landscape together and find the right fit for your budget and health needs. To get started, Schedule a Call With Paul today to simplify your Medicare journey and secure your future.

Take the Next Step Toward Your 2026 Coverage

Navigating medicare enrollment for green card holders doesn’t have to feel like a battle against a complex system. Whether you’ve just hit your five year residency milestone or you’re checking how your 40 work credits impact your Part A costs, the rules in 2026 require careful attention. We’ve helped seniors across 34 states compare plans from over 40 different insurance carriers to find the right fit. You don’t need to guess which path is right for your specific immigration status or worry about missing a deadline that could lead to permanent penalties.

Our team specializes in the updated 2026 eligibility rules for permanent residents. We take the time to listen and ensure you’re never rushed or pressured into a decision. We’ll help you look at every option with clarity so you can move forward with total certainty. You deserve a partner who fights for your best interests and simplifies the jargon into plain English. Let us help you move from confusion to confidence; Schedule a Call With Paul Barrett today.

We’re ready to help you protect your future and secure the healthcare you’ve worked so hard for.

Frequently Asked Questions

Can I get Medicare if I have only had my Green Card for 3 years?

No, you generally can’t enroll in Medicare until you’ve lived in the U.S. as a Lawful Permanent Resident for at least 5 years in a row. This 5-year residency rule is a strict requirement for medicare enrollment for green card holders who don’t have a long U.S. work history. We know this wait feels long, but we’re here to help you plan for that 5-year milestone so you’re ready the moment you’re eligible.

Do I have to pay for Medicare Part A if I didn’t work in the U.S.?

Yes, you’ll have to pay a monthly premium for Part A if you haven’t worked at least 10 years in the United States. In 2026, the full Part A premium is $518.00 per month for individuals with fewer than 30 work credits. If you’ve earned between 30 and 39 credits, that cost drops to $285.00. We’ll help you check your Social Security statement to see exactly where you stand so there are no surprises.

What is the 5-year residency rule for Medicare?

The 5-year residency rule requires you to live in the U.S. continuously as a Green Card holder for 60 months before you can apply for Medicare. You must be physically present in the country during this time; leaving for long periods can sometimes reset your clock. We guide you through these timing details to ensure you don’t face unnecessary delays. It’s all about moving you from confusion to confidence.

Can my spouse get Medicare based on my work history if they are a Green Card holder?

Yes, a Green Card holder can often qualify for premium-free Medicare Part A based on their spouse’s work record. Your spouse needs to be at least 62 years old and have earned 40 work credits, which equals about 10 years of work. You must also be at least 65 and have met the 5-year residency requirement yourself. This is a common way we help families save significantly on their monthly healthcare costs.

Will getting Medicare affect my path to U.S. citizenship?

No, enrolling in Medicare won’t hurt your chances of becoming a U.S. citizen. The U.S. Citizenship and Immigration Services (USCIS) doesn’t consider Medicare benefits a “public charge” in their evaluations. You can use these health benefits to stay well without any fear for your legal status. We want you to focus on your health while we handle the complex details of the insurance system.

What happens to my Medicare if I move back to my home country for a year?

If you move back to your home country for a year, your Medicare coverage won’t pay for any medical care you receive while abroad. You’ll still need to pay your Part B premiums every month to keep the policy active. If you stop paying and let the coverage lapse, you’ll likely face a 10 percent late enrollment penalty for every year you were gone. We help you weigh these costs before you make a big move.

Are Green Card holders eligible for Medicare Advantage plans?

Yes, Green Card holders can join Medicare Advantage plans once they’re officially enrolled in both Medicare Part A and Part B. These plans are run by private companies and often include extra benefits like dental, vision, and hearing coverage. In 2026, more than 54 percent of all Medicare beneficiaries choose these plans for their added value. We’ll help you compare the local options in your area to find the best fit.

How much does Medicare cost for a Green Card holder in 2026?

In 2026, the standard monthly premium for Medicare Part B is $185.00. If you don’t have 40 quarters of U.S. work history, you may also pay up to $518.00 for Part A. These costs can feel overwhelming, but we’re here to simplify the jargon and show you the clear path forward. Understanding medicare enrollment for green card holders is much easier when you have a patient guide by your side.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com