Last Tuesday, a 68-year-old grandmother named Martha realized her existing policy wouldn’t even cover half of the average funeral costs projected for 2026. Like many of us, she felt a heavy weight in her chest, worrying that her children would have to dip into their own savings to say goodbye. We understand that finding the best life insurance for seniors over 65 feels like trying to solve a puzzle where the pieces don’t fit. You’ve likely spent hours wondering if your health history makes you uninsurable or if a monthly premium will eat into your fixed retirement budget. It’s frustrating to feel like you’re being priced out of the protection your family deserves.

We’re here to clear the fog and show you how to secure a reliable, jargon-free policy that guarantees a payout for final expenses. You’ll learn how to find coverage that fits your lifestyle today without the stress of medical exams or complicated paperwork. We’ll walk you through the simple steps to move from confusion to confidence, comparing options that prioritize your peace of mind over corporate profits.

Key Takeaways

- We show you how to identify the best life insurance for seniors over 65 by comparing policies that prioritize your unique health profile and budget in 2026.

- Understand the critical differences between term and whole life coverage so you can avoid the common trap of rising premiums as you move through your 70s.

- Learn how to navigate health challenges with “no-exam” options that offer guaranteed protection, even if you’ve been worried about pre-existing conditions.

- Follow our simple step-by-step guide to calculating your exact needs for final expenses and legacy goals without overstretching your monthly budget.

- Discover why an independent broker is your strongest advocate in finding a carrier that truly wants your business, rather than settling for a limited, single-brand agent.

What Is the Best Life Insurance for Seniors Over 65 in 2026?

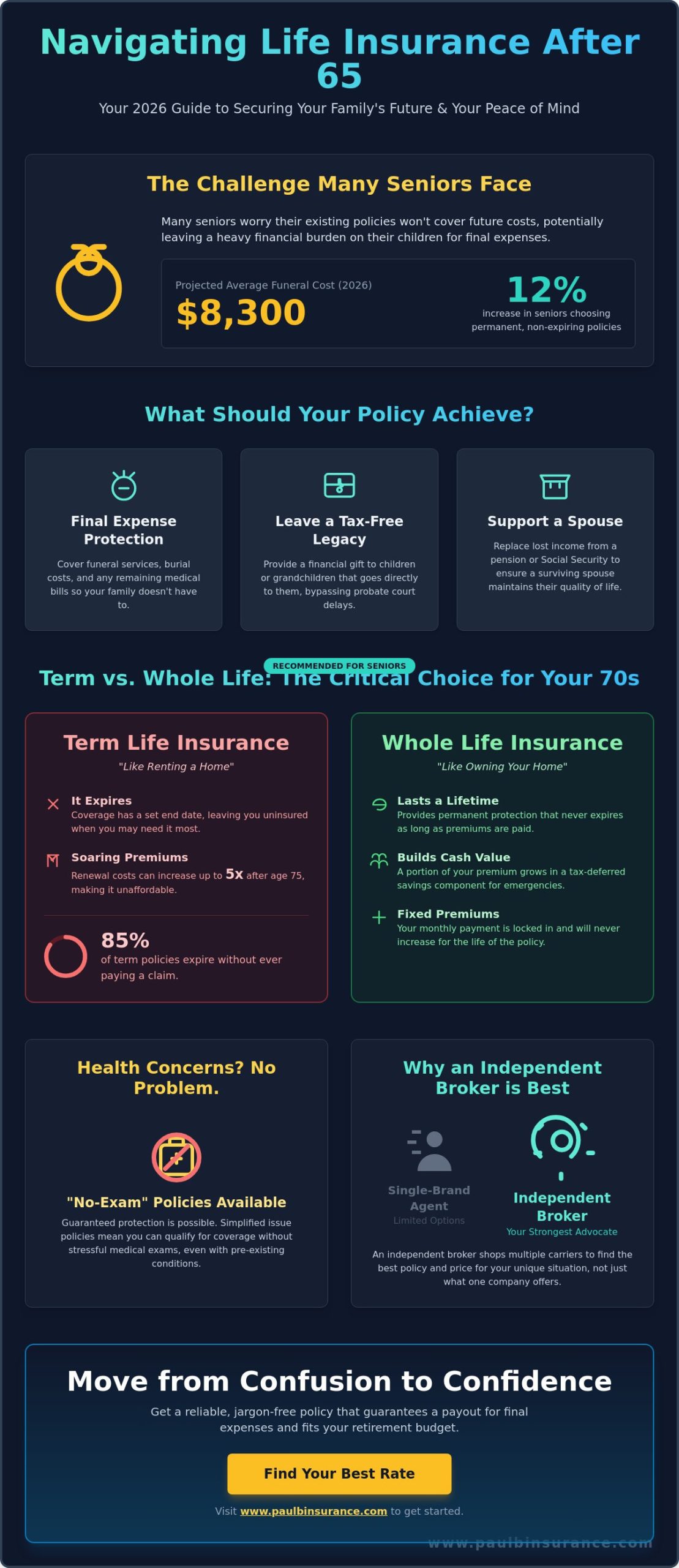

We understand that looking for insurance can feel like a confusing maze. In 2026, the best life insurance for seniors over 65 isn’t a one-size-fits-all plan. It’s a specialized tool designed to handle final expenses and protect your family’s future. For many, this means moving away from the high-value term policies you might have carried in your 40s. Instead, we now see a 12% increase in seniors choosing permanent protection that lasts a lifetime. This shift ensures that your coverage doesn’t expire just when your family needs it most.

To understand the basics of how these plans function, you might ask, What is life insurance? At its core, it’s a contract that ensures your loved ones aren’t left with a financial burden. In 2026, market shifts have made “simplified issue” policies much easier to access. You don’t always need a stressful medical exam anymore. We find that the right choice always depends on your current health and your monthly budget. We’re here to help you find that balance without any pressure or rush.

Why Your Needs Change After Age 65

Your priorities naturally shift as you enter this new chapter of life. Most seniors have paid off their 30-year mortgages or finished raising their children. Your focus moves from replacing a full salary to covering funeral costs, which averaged $8,300 in late 2025. We also use these policies for estate equalization to ensure every heir receives a fair share. We always suggest reviewing your life insurance alongside your Medigap enrollment. This ensures your total health and legacy plan is solid and works together perfectly.

The Three Main Goals of Senior Coverage

We focus on three primary objectives to give you total confidence in your choice. When we look for the best life insurance for seniors over 65, we prioritize these outcomes:

- Final expense protection: This is often called “Burial Insurance.” It’s a permanent policy that pays for your service and any remaining medical bills.

- Leaving a tax-free legacy: You can set aside a specific amount for your grandchildren. This money goes directly to them without the delays of probate.

- Supplementing a surviving spouse’s income: If a pension or Social Security check stops when a spouse passes, a life insurance payout can fill that financial gap.

We simplify the jargon so you know exactly how it works. Our goal is to move you from a state of confusion to a place of absolute confidence.

Term vs. Whole Life: Which Makes Sense for Your 70s?

Choosing the best life insurance for seniors over 65 often comes down to one fundamental question: do you need coverage for a little while, or do you need it forever? We understand that this decision feels heavy. Many of the folks we talk to are worried about leaving a financial burden on their children or spouse. We are here to clear away that fog and help you move from confusion to confidence.

Term life insurance is like renting a home. It provides a high death benefit for a lower initial cost, but it has an expiration date. In 2026, we see many seniors hit a “premium wall” once they pass age 75. At this stage, renewing a term policy can become five times more expensive than it was in your 60s. Whole life insurance, by contrast, is like owning your home. It stays with you as long as you pay the premiums. It also builds “cash value,” a small savings element that grows over time. This acts as a safety net you can access if an emergency arises. We help you look at the math to see which path protects your family without draining your retirement savings.

Term Life Insurance for Seniors

Term insurance works best when you have a specific financial “finish line.” If you have a mortgage with eight years left or a specific debt that will be paid off by 2034, a 10-year term policy is a smart, budget-friendly tool. We often suggest a “laddering” strategy. This involves owning a larger term policy for immediate debts and a smaller permanent policy for final expenses. This reduces your total costs as you age. However, you must consider the risk of outliving the policy. According to 2026 industry reports, 85% of term policies never pay a claim because the policyholder outlives the term. This can leave you uninsured at age 80 when finding new coverage is both difficult and costly.

Whole Life and Final Expense Insurance

For many of our clients, the best life insurance for seniors over 65 is a permanent whole life or final expense policy. These plans are the gold standard for seniors because they offer total predictability. Your premiums are fixed. They will never increase, even if your health changes or the economy shifts. We believe in simplicity, and nothing is simpler than knowing your coverage will be there when your family needs it most. These policies pair perfectly with Medigap plans to create a complete safety net. While your Medigap plan handles the medical bills, your life insurance ensures your final legacy is protected. If you want to see how these pieces fit together for your specific budget, you can schedule a call with Paul for a clear, no-pressure conversation.

Overcoming Health Hurdles: How to Qualify in 2026

We know the biggest worry for most folks is the fear of being turned down because of a medical history. You might think a past heart procedure or a chronic condition makes you uninsurable, but that’s rarely the case in 2026. Technology has transformed how we find the best life insurance for seniors over 65. Today, insurance carriers use sophisticated digital underwriting tools to analyze health risks in minutes. This shift means we can often secure an approval for you without the long, stressful waiting periods that used to be the industry standard.

In years past, getting a policy often meant waiting for a nurse to visit your home for a blood draw. While fully underwritten plans still offer the lowest premiums for those in peak health, “no-exam” policies have become the preferred choice for many of our clients. These modern options use real-time data from prescription databases and motor vehicle records to confirm your eligibility instantly. We take the time to explain these differences so you can move from a state of confusion to total confidence in your choice. Our goal is to ensure you’re never rushed or pressured into a decision that doesn’t fit your specific health profile.

Guaranteed Acceptance vs. Simplified Issue

Simplified Issue policies are an excellent middle ground for many seniors. You don’t have to deal with a medical exam, but you will answer a few basic health questions about your history. Because there’s a small amount of risk assessment involved, these plans are generally more affordable than “no-question” options. We typically recommend Guaranteed Acceptance as a reliable fallback for those with very serious or recent health events. It requires no health questions or exams, though it carries a higher cost to account for the carrier’s increased risk. We’ll help you compare both to see which one protects your budget and your family best.

Common Health Conditions and Insurance

Managing conditions like type 2 diabetes or heart disease shouldn’t stop you from protecting your family. We specialize in finding “high-risk” carriers that have updated their guidelines for 2026 to be more inclusive. Current data shows that approximately 88 percent of seniors with well-managed chronic illnesses now qualify for some form of coverage. We always emphasize being 100 percent honest on your application to ensure your family receives a valid claim when they need it most. A Graded Death Benefit is a two-year waiting period for guaranteed policies. This structure allows companies to provide the best life insurance for seniors over 65 regardless of their health, providing a path to peace of mind for everyone.

A Step-by-Step Guide to Choosing Your Policy

Finding the best life insurance for seniors over 65 often feels like wandering through a thick fog. We believe the process should be clear and calm. Our goal is to move you from confusion to confidence by following a simple, logical path. We simplify the jargon so you know exactly how your protection works without any of the typical insurance industry stress.

We start by looking at your actual needs rather than a generic sales pitch. We recommend a methodical approach to ensure your family is protected without overstretching your fixed income. This starts with a clear look at your finances and your health history.

- Audit your monthly budget: A policy only provides peace of mind if it’s sustainable. We help you find a premium that fits comfortably within your 2026 expenses.

- Gather your history: Make a list of your current medications and recent health dates. This transparency helps us find carriers that view your specific health profile favorably.

- Compare 10+ independent carriers: Don’t settle for the first quote you see. We look at at least 10 different providers to find the sweet spot of price and reliability.

- Choose an independent broker: A “captive agent” only works for one company. We work for you, comparing the entire market to find the best life insurance for seniors over 65.

Calculating Your Coverage Amount

Many seniors worry they need a massive policy, but a coverage amount between $10,000 and $25,000 is often the perfect fit for final expenses. In 2026, the National Funeral Directors Association reports that average funeral and burial costs have reached approximately $9,850. We suggest adding a small cushion to account for future inflation and any small remaining debts.

It’s also wise to look at what you already have. You can use our Medicare Advantage Guide to see how your current health plan handles medical costs. If your health expenses are already well-managed, you can focus your life insurance strictly on funeral costs and legacy goals.

What to Look for in a Carrier

We only point you toward companies with strong financial foundations. We check AM Best ratings to ensure a carrier has an “A” or “A+” grade. This rating acts as a promise that the company will have the funds to pay your beneficiaries when the time comes. We also look for modern “Living Benefits” riders. These allow you to access a portion of your death benefit early if you are diagnosed with a chronic or critical illness, providing a financial safety net while you are still here.

We are here to protect and empower you throughout this entire process. Schedule a call with Paul today to receive a personalized, unbiased comparison of the top-rated policies available in 2026.

Why an Independent Broker Is Your Best Advocate

Choosing a policy shouldn’t feel like a gamble. Many people start their search by calling a big-name insurance company they saw on television, but they often end up talking to a “captive agent.” These agents are employees of one specific brand. They can only offer you what that one company sells, even if it’s not the best fit for your needs or your wallet. If that company’s underwriting department doesn’t like your health history, the agent has no choice but to give you a high price or a rejection letter.

We do things differently. As independent brokers, we represent you, not the insurance companies. We shop over 40 different carriers in 2026 to find the one that views your health profile most favorably. Whether you have managed diabetes or a history of heart issues, there is usually a carrier that wants your business. This personalized shopping is the most effective way to secure the best life insurance for seniors over 65 while keeping your monthly premiums affordable.

We guide you through a simple 5-step process designed to move you from “Confusion to Confidence”:

- Discovery: We listen to your goals and determine exactly what you want to protect.

- Health Analysis: We look at your medical history to see which carriers will offer the best rates in 2026.

- Market Search: We compare 40+ top-rated companies simultaneously to find the lowest price.

- Plain English Review: We explain the pros and cons of your top three options without any confusing jargon.

- Final Enrollment: We handle the paperwork and follow up until your policy is active.

Personalized Guidance for Every State

Insurance rules are not the same everywhere. In 2026, states like New York, California, and Florida have specific regulations that can change which policies are available to you. We navigate these state-level details so you don’t have to. Our unbiased approach focuses on saving you money over the entire life of the policy. We also help you see how your coverage fits into your broader Medicare Planning to ensure your legacy and your health are both protected.

Ready for Peace of Mind?

Our promise to you is simple: no rush, no pressure, and just clear answers. We know this is a big decision, and we want you to feel completely comfortable with your choice. Our team provides year-round support that goes far beyond just signing a policy. We’re here to answer questions for you and your beneficiaries whenever they arise.

It is never too late to protect your family. Whether you are looking for a small final expense policy or a larger legacy gift, we can help you find the best life insurance for seniors over 65 available today. Schedule your “Confusion to Confidence” call with us right now and let’s get your questions answered.

Take the Next Step Toward Your Family’s Security

Securing the best life insurance for seniors over 65 in 2026 shouldn’t feel like a chore. We’ve simplified the process by comparing term and whole life options while navigating the latest health qualification standards. You now have the roadmap to move from confusion to confidence. We believe that every senior deserves a plan that fits their unique needs without the pressure of a captive agent.

Our team has spent over a decade helping seniors move from confusion to confidence. With licenses in 34 states, including New York, California, and Florida, we understand the specific regulations that affect your coverage in 2026. We provide access to over 40 top-rated insurance carriers to ensure you aren’t limited to a single company’s options. You deserve a partner who is never rushed and never pressured. Schedule a Call With Paul to Find Your Perfect Plan and start your journey toward a secure future today.

Frequently Asked Questions

Is it worth getting life insurance after age 65?

Yes, life insurance remains a vital tool for protecting your family from unexpected final expenses and debt. In 2026, the average cost of a traditional funeral has reached approximately $11,500 according to recent industry reports. By securing a policy now, you ensure your loved ones aren’t left scrambling to cover these costs during a difficult time. We help you find a plan that provides immediate peace of mind without breaking your monthly budget.

How much does a $25,000 whole life policy cost for a 70-year-old?

Your monthly premium depends on your health, gender, and the specific carrier you choose. For a 70-year-old, rates are higher than for younger applicants, but we work with dozens of carriers to find the most competitive options available in 2026. Instead of guessing at a number, we provide a personalized comparison of the top five rated companies to show you exactly what your costs will be. This ensures you never pay more than necessary for your coverage.

Can I get life insurance if I have a serious pre-existing condition?

You can absolutely qualify for coverage even with a history of heart disease, diabetes, or other chronic conditions. In 2026, over 45 percent of seniors over 65 manage multiple health issues, and insurance companies have created guaranteed issue policies specifically for this group. These plans don’t require a medical exam or health questions. We specialize in navigating these options so you get the protection you need regardless of your medical history.

What is the best type of life insurance for someone over 65?

The best life insurance for seniors over 65 is typically a whole life or final expense policy because the premiums never increase and the coverage never expires. While term insurance is cheaper, 98 percent of term policies never pay a claim because the policyholder outlives the term. We recommend whole life for most seniors because it provides a permanent solution that guarantees your family receives the full benefit when they need it most.

Do I need a medical exam to get senior life insurance in 2026?

No, most modern senior policies in 2026 don’t require a physical exam or blood work. Many carriers now use accelerated underwriting, which allows them to check your prescription history and medical records electronically in less than 15 minutes. This makes the application process simple and stress free. We focus on these no-exam options to help you get approved quickly and easily from the comfort of your own home.

What happens if I outlive my term life insurance policy?

If you outlive your term, the coverage simply ends and your beneficiaries won’t receive a payout. This is why we often suggest permanent options for seniors. However, some 2026 term policies include a conversion rider that lets you switch to a whole life plan without a new medical exam. We can review your current policy to see if you have this option or help you transition to a more stable, permanent plan.

How does life insurance work with my Medicare coverage?

Life insurance and Medicare are completely separate programs that serve different purposes. Medicare pays for your doctors and hospital visits, but it doesn’t provide any money for funeral costs or family support after you pass away. Even with the 2026 Medicare updates, there’s no death benefit included in your health coverage. We help you bridge this gap by setting up a life insurance plan that works alongside your Medicare to provide full protection.

Is the “9.95 a month” insurance plan actually a good deal?

Those heavily advertised 9.95 plans can be misleading because that price usually only buys one unit of coverage. For a 70-year-old male in 2026, one unit might only provide about $500 in actual benefits, which won’t cover most final expenses. We believe in transparency and want you to understand exactly what you’re buying. We’ll show you how those teaser rates compare to comprehensive plans so you don’t end up underinsured when it matters most.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com