Last Tuesday, a daughter named Sarah called us in a panic because her father was being moved to a facility, and she just realized her 2026 Medicare plan would not pay for his stay. It is a terrifying moment when you realize that medicare coverage for nursing home care is not the universal safety net most people assume it is. We understand the stress of watching your life savings feel vulnerable to rising healthcare costs. You deserve to feel secure about your future without being buried in fine print.

We are here to clear up the “rehab” versus “long-term care” confusion so you can breathe easier. We promise to simplify the rules and show you exactly what is paid for and what comes out of your own pocket. In this guide, we will walk through the 100-day rule, explain the vital difference between skilled and custodial care, and provide three specific steps to protect your hard-earned assets from unexpected facility bills.

Key Takeaways

- We clear up the common confusion between short-term recovery and long-term residence so you aren’t caught off guard by facility costs in 2026.

- Understand why your specific hospital status is the deciding factor in qualifying for medicare coverage for nursing home care under the “Three-Day Rule.”

- Learn how the 100-day benefit clock actually works and what steps you can take to handle the expensive daily co-pays that begin after day 20.

- See how your choice between a Medicare Advantage plan and Medigap changes your access to care and your requirements for prior authorizations.

- Move from confusion to confidence by learning exactly what happens when Medicare benefits end and how to prepare for the reality of care beyond Day 101.

The Big Question: Does Medicare Cover Nursing Home Care?

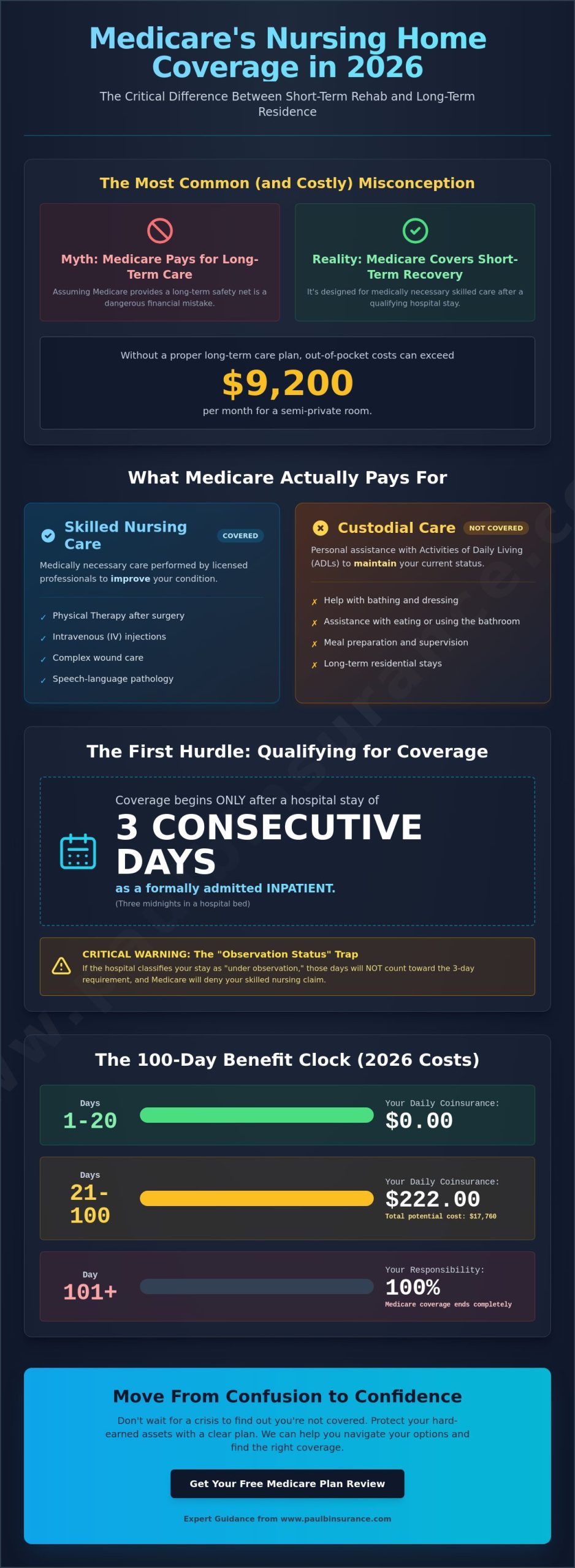

We hear this question every day from seniors who feel lost in the “crazy maze” of the insurance system. The short answer is that Medicare covers short-term recovery, not long-term residence. Many families use the term “nursing home” to describe any facility where a senior lives and receives help. This is where the confusion begins. Assuming that Medicare is a long-term care plan is a dangerous financial mistake in 2026. Without a clear strategy, you might face out-of-pocket costs exceeding $9,200 per month for a semi-private room. Understanding medicare coverage for nursing home care starts with looking at the actual services provided. To build a strong foundation, we recommend reviewing Medicare basics to see how different parts of the program interact. Our goal is to move you from confusion to confidence so you can make decisions without the stress of the unknown.

Defining “Skilled Nursing” vs. “Custodial Care”

Skilled care includes medically necessary therapy and nursing provided by licensed professionals. This might be daily physical therapy after a hip replacement or intravenous injections for a severe infection. Custodial care is different; it involves help with “Activities of Daily Living” like dressing, bathing, or using the bathroom. Medicare strictly excludes custodial-only stays because the program is designed to treat medical conditions rather than provide long-term personal assistance. We simplify this jargon so you know exactly what to expect when a loved one needs help. Many people choose to supplement their coverage with a Medigap plan to help with these gaps, but even those plans have specific limits on what they will pay for.

Why the Distinction Matters for Your 2026 Planning

In 2026, most facilities are “dual-certified,” which means they offer both types of care under one roof. The moment your coverage stops is when your care shifts from “improving” your health to simply “maintaining” your current status. This transition happens quickly. We tell our clients to look at the clinical care plan rather than the name on the building. If the medical team decides you’ve reached your maximum recovery potential, your medicare coverage for nursing home care will end. We want to help you steer clear of costly mistakes by planning for this shift before it happens. Our mission is to be your advocate, ensuring you are never rushed and never pressured into a plan that doesn’t fit your needs.

How Medicare Part A Handles Skilled Nursing Stays in 2026

We know how stressful it feels when a loved one needs more help than you can provide at home. The rules for medicare coverage for nursing home care can feel like a maze, but we are here to help you find the path. In 2026, Medicare Part A covers skilled nursing facility (SNF) care, but only under very specific conditions. It isn’t meant for long term stays. Instead, it’s designed for short term recovery after a serious health event like a stroke or hip replacement.

The Qualifying Hospital Stay Requirement

To qualify for SNF coverage, you must have a three-day inpatient hospital stay. This means three consecutive midnights in a hospital bed as an admitted patient. We see many families get caught in the “observation status” trap. If the hospital classifies you as under observation rather than admitted, those nights don’t count toward the three-day requirement. Even if you stay in a hospital room for a week, Medicare won’t pay a dime for your nursing home stay if you weren’t officially admitted. You can find the official Medicare coverage rules on the government website to see exactly how they define these stays. We simplify these details for our clients so they can advocate for themselves at the hospital before discharge happens.

The 100-Day Countdown Explained

Once you meet the hospital requirement, the Medicare clock starts ticking. The coverage is broken down into three specific phases based on how long you stay. We want you to understand these costs upfront so there are no surprises on your bill.

- Days 1 through 20: You pay $0 per day. Original Medicare covers 100% of the costs for these first three weeks.

- Days 21 through 100: You are responsible for a daily coinsurance amount. For 2026, this rate is $222.00 per day.

- Day 101 and beyond: Medicare coverage ends completely. You are responsible for all costs out of pocket.

The daily cost for those middle 80 days adds up quickly. A stay that lasts the full 100 days could result in a bill of over $17,000 just for the coinsurance. This is why we often suggest looking into Medigap plans. Most of these plans cover that $222.00 daily cost, protecting your savings from being drained during a long recovery. We believe in providing this clarity so you can focus on getting better rather than worrying about the mail.

A “benefit period” is another vital piece of the puzzle. It begins the day you enter the hospital or SNF and ends when you haven’t received any inpatient hospital or skilled care for 60 days in a row. If you go home for 60 days and then have a new health issue, your benefit period resets. This gives you a fresh 100 days of medicare coverage for nursing home care. If you feel overwhelmed by these timelines, you can always schedule a call with us to clear up the confusion and move forward with confidence.

Comparing Your Options: Advantage Plans vs. Medigap for Nursing Care

Choosing how you receive your benefits changes your entire experience with medicare coverage for nursing home care. We see many families feel overwhelmed by the costs that start piling up after the first 20 days. It is a choice between two very different paths, and we want to help you find the one that fits your life best.

Medicare Advantage and Skilled Nursing

Medicare Advantage plans often look attractive because many of them waive the strict requirement for a three day inpatient hospital stay before covering nursing care. This flexibility helps if you need rehab but did not stay in the hospital long enough to trigger standard Medicare benefits. However, there is a trade-off you should understand. These private plans use a process called “Prior Authorization.” This means the insurance company decides if your stay is still medically necessary. Even if your doctor thinks you should stay, the plan might decide your progress has plateaued and stop payments. We explain these nuances in detail in our Medicare Advantage Guide.

How Medigap Fills the Daily Coinsurance Gap

If you stay with Original Medicare and add a Medigap policy, your financial experience is much more predictable. For 2026, the daily coinsurance for days 21 through 100 is $214.00. That adds up to $17,120 if you need the full 100 days of care. Medigap Plan G is our “gold standard” for a reason; it pays 100 percent of that daily bill. You will not see a single invoice for those 80 days. Plan N also covers this cost in full. This path offers incredible peace of mind because as long as Medicare approves the care, the supplement pays its share without an insurance company official questioning the stay. You can read more about these options in our guide to Medicare Supplement Insurance.

We help you decide between these paths by looking at your health history and your comfort with risk. Here are a few things we consider together:

- Budget: Advantage plans usually have lower monthly premiums but higher costs when you actually use the facility.

- Control: Medigap allows you and your doctor to remain in control of your recovery timeline without outside interference.

- Predictability: Medigap removes the fear of a $214.00 daily bill, while Advantage plans may have varying daily copays.

Our goal is to move you from confusion to confidence. We simplify the jargon so you know exactly how medicare coverage for nursing home care works before you ever need it. We are here to protect your savings and your health.

Navigating the 100-Day Limit and Beyond

We often see families hit a wall of stress when they realize medicare coverage for nursing home care isn’t permanent. On Day 101, the financial support from Medicare Part A stops completely. In 2026, the average cost for a semi-private room in a skilled nursing facility has reached $260 per day. Without a plan, these costs can quickly deplete a lifetime of savings. We are here to help you understand exactly what happens when that 100-day clock runs out so you can protect your future.

Even if you are paying for the facility yourself after Day 100, your other benefits don’t just disappear. It’s a common misconception that all support ends. Your Medicare Part D plan remains a vital resource. It continues to cover your prescription drugs while you are in the facility, even if the room and board are no longer covered. We make sure you understand these transitions so you don’t face unexpected bills for your daily medications.

The “Improvement Standard” Myth

You might hear that you’ll be discharged because you aren’t “getting better” anymore. This is a mistake. Thanks to the Jimmo v. Sebelius ruling, Medicare must provide coverage if skilled care is needed to maintain your current condition or to slow down any decline. You don’t always have to show progress to stay eligible for those first 100 days. If the facility issues a discharge notice and you believe the care is still medically necessary, you have the right to request an expedited appeal through a Quality Improvement Organization. This process ensures an independent body reviews your case before your coverage is cut off.

Alternatives for Long-Term Care Funding

When medicare coverage for nursing home care ends, you must transition to other payment sources. Medicaid is the primary payer for long-term stays, covering 62% of all nursing home residents in 2026. However, Medicaid requires you to meet strict state-specific asset and income limits. For those who want more control, Long-Term Care (LTC) insurance or hybrid life insurance policies offer a way to pay for extended stays without exhausting your personal assets. We help you compare these options so you can choose a path that provides lasting peace of mind.

Don’t let the complexity of the 100-day limit overwhelm you. Schedule a Call With Paul today to move from confusion to confidence regarding your long-term care plan.

Moving From Confusion to Confidence in Your Care Planning

Trying to find your way through the Medicare maze on your own is a gamble with your savings. In 2026, the rules for medicare coverage for nursing home care are more specific than ever. One wrong turn can lead to a bill for thousands of dollars that you didn’t see coming. We believe you shouldn’t have to be an insurance expert just to get the care you deserve. Our team is here to act as your shield, protecting you from the stress of fine print and the anxiety of the unknown.

We don’t just help you sign a form and disappear. Our commitment is to provide year-round support because your health needs don’t stop once enrollment ends. If you get a confusing bill in July or a new facility preference in October, we’re just a phone call away. We treat our clients like family, ensuring you always have a dedicated advocate to call when the system feels overwhelming.

Unlike a captive agent who only represents one company, we are independent brokers. This means we work for you, not the insurance companies. We compare over 40 different carriers to find your specific “Best Fit.” In 2026, the differences between plans can be vast; some might offer better access to the local skilled nursing facilities you prefer, while others might have lower out-of-pocket costs. We lay all the options on the table so you can make a choice based on facts, not a sales pitch.

The 5-Step Process to Securing Your Future

- Step 1: A calm, no-pressure conversation. We start by listening. We want to hear about your concerns and your budget without any rush or sales tactics.

- Step 2: Reviewing your current doctors and facility preferences. We check which plans your preferred doctors accept and which facilities are in-network for 2026 to ensure medicare coverage for nursing home care aligns with your actual needs.

- Step 3: Comparing the math. We look at the hard numbers between Medigap and Medicare Advantage for 2026, including the new $2,000 out-of-pocket cap for prescriptions.

Ready to Simplify Your Medicare?

Don’t wait for a medical crisis to understand your coverage. By the time you need a nursing home, you should already have the peace of mind that your plan is solid. We are here to protect your health and your hard-earned savings from the rising costs of care. Let us take the weight off your shoulders and replace your questions with clear, actionable answers.

We’re ready to help you move from confusion to confidence today. Schedule a Call with Paul to get started.

Move From Confusion to Confidence in Your Care Planning

Navigating the Medicare maze doesn’t have to feel like a full-time job. We’ve explored how Part A handles your first 100 days of skilled nursing and why choosing between a Medigap plan or an Advantage plan in 2026 makes a massive difference for your wallet. While Medicare provides a vital safety net, it isn’t a permanent solution for long-term stays. Understanding the specifics of medicare coverage for nursing home care is the first step in protecting your savings and your future comfort.

We’re here to help you find clarity. Our team offers independent, unbiased guidance across 34+ states and provides access to more than 40 insurance carriers to ensure you get the right fit. You’ll never feel rushed or pressured when you talk to us. We simply want you to have the facts so you can steer clear of costly enrollment mistakes. If you’re ready to clear up the jargon and see your path forward, we’re ready to guide you.

Get a Free, Unbiased Review of Your Medicare Options

You deserve to feel secure about your health care choices as we navigate 2026 together.

Frequently Asked Questions

Does Medicare Part B cover any part of nursing home care?

Medicare Part B doesn’t pay for your room and board in a nursing home, but it does cover your medical needs while you stay there. We see many seniors get confused by this distinction. In 2026, Part B continues to pay for 80 percent of your doctor visits, physical therapy, and speech pathology services after you meet your annual deductible. You’re still responsible for the remaining 20 percent unless you have a supplement plan to bridge that gap and provide peace of mind.

What is the “Three-Midnight” rule for 2026?

The Three-Midnight rule in 2026 requires you to stay in a hospital as a formal inpatient for at least three consecutive days before Medicare pays for skilled nursing. Observation status doesn’t count toward these three days, which is a common trap that leads to unexpected bills. We help you verify your hospital status early so you can secure your benefits. This rule remains a cornerstone for qualifying for medicare coverage for nursing home care after a surgery or sudden injury.

Will Medicare pay for a private room in a nursing home?

Medicare only pays for a private room if a doctor states it’s medically necessary, such as for infection control or a severely weakened immune system. In all other cases, Medicare covers a semi-private room shared with another resident. If you prefer a private room for personal comfort, the facility will likely charge you the difference in price. Most facilities provide a written agreement outlining these extra daily costs before you move in so there aren’t any surprises.

Does a Medicare Supplement plan cover long-term custodial care?

No Medicare Supplement plan covers long-term custodial care, which includes help with daily activities like dressing, bathing, or eating. These plans are designed to pay for the medical gaps, like your Part A coinsurance for skilled nursing. According to 2026 Medicare guidelines, custodial care is considered non-medical. We want you to have the facts early so you can look into alternative options like long-term care insurance or Medicaid to protect your savings.

What happens if I need to return to the nursing home after being discharged?

You can return to a nursing home, but your coverage depends on whether you’ve started a new benefit period. A benefit period ends once you haven’t received any inpatient hospital or skilled nursing care for 60 days in a row. If you go back before those 60 days pass, you’re still in the same period and won’t get a fresh 100 days of coverage. This 60-day window is a strict federal requirement used to track your usage and reset your benefits.

Can I keep my Medicare Advantage plan if I move into a nursing home permanently?

You can keep your Medicare Advantage plan if you move into a nursing home permanently, but you must ensure the facility is in your plan’s network. Some plans offer a Special Enrollment Period if you move into a long-term care facility, allowing you to switch to a plan that better fits your new location. We recommend reviewing your plan’s 2026 Evidence of Coverage to see how they handle institutionalized residents. We’re here to help you navigate these network changes without the stress.

How much does Medicare pay for skilled nursing in 2026?

Medicare pays 100 percent of the costs for the first 20 days of your stay in a skilled nursing facility. Starting on day 21 through day 100, you’re responsible for a daily coinsurance amount. For 2026, the Centers for Medicare and Medicaid Services set this daily rate based on updated federal budget formulas. After day 100, Medicare stops paying entirely, and you’re responsible for all costs. This is a key part of understanding medicare coverage for nursing home care and planning your finances.

Does Medicare cover dementia care in a nursing home?

Medicare covers medical services for dementia, but it doesn’t pay for the long-term housing or “memory care” that many families need. If a person with dementia requires skilled nursing or therapy after a hospital stay, Medicare pays for those specific medical services for up to 100 days. However, the daily supervision and safety monitoring required for advanced memory loss are considered custodial care. We help families navigate these difficult distinctions so they aren’t overwhelmed by the high costs of memory care units.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com