If you’ve been researching Medicare Supplement plans, you’ve seen the AARP name everywhere. It’s on the mailers in your mailbox, the commercials on TV, and probably a few ads that followed you around the internet. AARP/UnitedHealthcare is the single largest Medigap brand in the country — and that kind of visibility creates a natural assumption: this must be the best option.

But is it?

After 18+ years of working exclusively in Medicare and helping thousands of clients compare Medigap options, I want to give you an honest, straight answer — not a sales pitch in either direction. The truth is more nuanced than most people expect.

AARP/UHC is a legitimate, financially sound carrier with real advantages. It’s also consistently one of the more expensive options in most markets, and there are a few things about how it’s structured that you genuinely need to understand before enrolling. This guide covers all of it.

Key Takeaways

- AARP is not an insurance company. UnitedHealthcare underwrites all AARP Medicare Supplement plans and pays AARP a royalty fee for use of its brand name.

- On Plan G specifically, AARP/UHC is frequently one of the top 3 most competitive carriers in many states — and rarely falls outside the top 5. Plan N is a different story, running significantly higher than competitors in most markets.

- Plan G from AARP/UHC averages $170–$177 per month at age 65 in 2026. Comparable A-rated carriers often run $30–$70 per month less for identical coverage.

- UHC uses a unique “enrollment discount” pricing model in most states — premiums start discounted and rise as the discount phases out, in addition to any general rate increases.

- In August 2025, AM Best downgraded UHC’s insurance subsidiaries from A+ to A — still an Excellent rating, but a meaningful change.

- UHC does not offer High-Deductible Plan G in most states — a significant gap for cost-conscious enrollees.

- For some people, AARP/UHC is a solid choice. For many others, an independent broker can find the same benefits from an equally A-rated carrier for considerably less.

Table of Contents

- First Things First — What Is AARP, and What Is UHC?

- What Plans Does AARP/UHC Offer?

- What Does It Actually Cost in 2026?

- The Enrollment Discount — The Thing Nobody Explains Upfront

- How Does UHC Price Its Plans? The Community Pricing Story

- What Are the Real Advantages of AARP/UHC?

- What Are the Real Drawbacks?

- How Does It Compare to Competitors?

- The AM Best Downgrade — What It Means for You

- So — Is It Worth the Premium?

- Frequently Asked Questions

First Things First — What Is AARP, and What Is UHC?

This is the single most important thing to understand before any comparison — and most people don’t know it.

AARP is not an insurance company.

AARP is a nonprofit advocacy organization for older Americans. What they do with Medicare Supplement insurance is license their brand — their name, their logo, their trusted reputation — to UnitedHealthcare Insurance Company in exchange for royalty fees. UnitedHealthcare then uses the AARP name to market and sell Medigap plans.

UnitedHealthcare actually underwrites your policy, processes your claims, and provides all customer service. AARP’s role is essentially brand licensing — and they’re compensated for it through fees built into the arrangement. This is disclosed in UHC’s own plan materials and confirmed in every piece of AARP/UHC marketing, though it’s easy to miss in the fine print.

This means two things for you as a consumer:

First, when you see “AARP Medicare Supplement,” you’re actually buying a UnitedHealthcare product. The AARP name is marketing. The insurance company is UHC.

Second, AARP’s endorsement of UHC is a business arrangement — not an independent consumer review. AARP receives royalty fees from UHC for the use of its intellectual property. That’s disclosed in fine print on every piece of AARP/UHC marketing material, but most people never read it.

None of this makes AARP/UHC a bad product. UnitedHealthcare is a legitimate, experienced carrier. But understanding what you’re actually buying — and what the AARP name does and doesn’t represent — is essential context.

What Plans Does AARP/UHC Offer?

AARP/UHC is one of the most plan-diverse carriers in the Medigap market. They offer nine of the ten standardized Medigap plan types across all 50 states and Washington D.C. You can review all standardized Medigap plan types at medicare.gov:

- Plans A, B, C, D, F, G, K, L, and N

What they don’t offer: High-Deductible Plan G is not available from UHC in most states. This is a meaningful gap. HD Plan G offers the same ultimate coverage as standard Plan G but with a lower monthly premium in exchange for meeting a $2,950 deductible first — making it an excellent option for healthy enrollees looking to manage costs. If HD Plan G is on your radar, you’ll need to look at other carriers.

Plan G and Plan N are the most popular choices for new enrollees in 2026. Plan G covers virtually all Medicare gaps after the annual Part B deductible ($283 in 2026). Plan N is similar but includes small copays at office and emergency room visits in exchange for a lower monthly premium.

What Does It Actually Cost in 2026?

Here’s where the story is more nuanced than most people expect — and where your specific plan choice matters enormously.

Plan G from AARP/UHC averages $170–$177 per month for a 65-year-old woman in 2026. And here’s something that surprises a lot of people: on Plan G specifically, UHC is frequently one of the most competitive carriers in the market. ValuePenguin rates them as the best overall Medigap company in part because of their competitive Plan G pricing, noting that seven of their ten plans come in below the national average. In many states, AARP/UHC ranks in the top three for Plan G pricing — and rarely falls outside the top five.

This is a meaningful distinction from the “always overpriced” reputation they sometimes carry. On Plan G, they often earn their place.

However — Plan N is a different story. NerdWallet’s analysis found that AARP/UHC’s Plan N premiums ran approximately 45% higher than the least expensive option in the same market. If Plan N is on your radar, UHC is generally not your most cost-competitive choice.

Here’s a general comparison for Plan G premiums for a 65-year-old woman in 2026 (national ranges — your actual rate depends on your state, ZIP code, and gender):

| Carrier | Plan G Monthly Range |

|---|---|

| AARP / UnitedHealthcare | $160–$200 |

| Mutual of Omaha | $110–$165 |

| Aetna | $105–$160 |

| Cigna / HealthSpring | $115–$170 |

| Blue Cross Blue Shield | $120–$180 |

One critical nuance inside UHC itself: There are actually two UHC books of business. Newer AARP Medigap policies are written through UnitedHealthcare Insurance Company of America (UHICA), which typically quotes 10–20% lower than the original UHC book. If you’re comparing UHC quotes, always ask which entity is writing the policy. The newer UHICA book is almost always the more competitive starting point.

The pricing summary: on Plan G, UHC is genuinely competitive — sometimes the best option in your state. On Plan N, they’re generally not. And on long-term trajectory, the enrollment discount dynamic (explained below) is something every prospective enrollee needs to understand before signing up.

Always get quotes specific to your ZIP code and age. National averages are directional — the state-level comparison is what actually matters.

The Enrollment Discount — The Thing Nobody Explains Upfront

This is the part of AARP/UHC’s pricing structure that surprises people most — and that many agents never explain clearly.

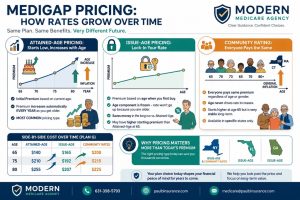

In most states, AARP/UHC uses a pricing model built around an enrollment discount. When you first sign up, your premium includes a built-in discount based on your age. That discount is significant — and the exact starting percentage and phase-out schedule has actually changed over time for newer enrollees.

For policyholders who enrolled several years ago, the discount typically started at around 36–39% and decreased by three percentage points per year beginning around age 69. For newer enrollees, UHC has updated the structure — the starting discount is now higher (reportedly around 45% for some newer books), with a slower phase-out of approximately two percentage points per year. Because the exact discount structure varies by enrollment date, state, and the specific book of business, it’s worth asking UHC directly for your personal discount schedule when you enroll.

The core concept remains the same regardless of the specific percentages: your premium includes a built-in discount that gradually phases out as you age, creating premium growth above and beyond any general rate increases UHC files for inflation and claims costs.

A real-world example from Pennsylvania: one policyholder received notice that their Plan G premium was increasing from $175 to $201 per month — a 15% jump in a single year — driven largely by the enrollment discount declining combined with a general rate increase.

This discount structure is entirely legal and fully disclosed, but it’s buried in policy documents and rarely explained clearly at the point of sale. If you enrolled in an AARP/UHC Medigap plan several years ago and haven’t reviewed your premiums recently, it’s worth taking a close look at where your rate is now relative to where it started — and what comparable A-rated carriers are offering today.

How Does UHC Price Its Plans? The Community Pricing Story

One genuinely positive aspect of AARP/UHC — and one that often gets overlooked in the criticism — is their pricing model in most states.

In 43 of 50 states, UHC uses community pricing for their Medigap plans. This means your premium is not based on your current age and does not automatically increase each year simply because you had another birthday. Everyone in the same geographic area pays the same base rate regardless of age.

This is actually a significant structural advantage over attained-age pricing — where your premium goes up every year as you get older. Under community pricing, once the enrollment discount has fully phased out (around age 81), your only ongoing increases come from general inflation and claims-based adjustments — not age.

The three states where UHC uses attained-age pricing instead are Kansas, North Dakota, and Oregon. If you live in one of those states, this advantage doesn’t apply to you.

For enrollees planning to keep their plan long-term and who enroll later in retirement (say, age 70+), community pricing can make UHC more competitive than it appears at first glance — because you’re not adding an age-based escalator on top of everything else.

What Are the Real Advantages of AARP/UHC?

Let’s be fair. There are legitimate reasons this is the most popular Medigap carrier in the country.

1. Available in All 50 States UHC offers AARP Medigap plans everywhere. Not every carrier operates in every state. If you move in retirement or want consistency regardless of where you live, UHC delivers that.

2. Low NAIC Complaint Score Despite their size, UHC’s Medigap-specific NAIC complaint index is approximately 0.68 — meaningfully below the 1.0 national average. Members rarely file formal complaints. Whatever people feel about their premiums, the actual claims experience and customer service track record is solid.

3. Renew Active Fitness Benefit UHC includes gym membership access through their Renew Active program at no additional cost. For enrollees who already pay for a gym membership, this is a genuine dollar-value offset against the higher premium. For those who don’t use a gym regularly, it’s less relevant.

4. 24/7 Nurse Line Access to a registered nurse by phone at any time. For older enrollees managing health questions, this can be genuinely useful.

5. Broad Plan Selection Nine of ten standardized plans available in most markets — more options than many competitors.

6. Community Pricing in Most States As described above, no automatic age-based premium increases in 43 states. This is a structural long-term advantage.

7. Brand Familiarity and Trust For some enrollees, there’s real comfort in a name they recognize. If having a household name on your insurance card reduces your anxiety and increases your confidence in your coverage, that has value — even if it’s hard to quantify.

What Are the Real Drawbacks?

1. Plan N Is Significantly More Expensive On Plan G, UHC is frequently competitive — often top 3 in many states. But Plan N is a different story. Independent analysis found UHC’s Plan N premiums running approximately 45% higher than the least expensive option in the same market. If Plan N is what you’re considering, UHC is generally not your most cost-effective choice.

2. The Enrollment Discount Structure As described above, the phasing-out enrollment discount creates compounding premium growth in the early years of your coverage. This is a structure that favors UHC financially and can disadvantage policyholders who don’t understand it going in.

3. No High-Deductible Plan G UHC does not offer HD Plan G in most states. For healthy, cost-conscious enrollees, this is a real gap in their product lineup.

4. No Household Discount in Most States Mutual of Omaha offers household discounts of 7–12% when a spouse or partner also enrolls. Aetna offers around 6%. UHC does not offer a comparable household discount in most states — meaning couples can end up paying more than necessary compared to carriers that reward multi-policy households.

5. The AM Best Downgrade In August 2025, AM Best downgraded UHC’s insurance subsidiaries from A+ (Superior) to A (Excellent). They remain financially sound with a stable outlook — this is not a distress signal. But it’s a meaningful change, particularly for a carrier that many people chose specifically because of their premium financial strength rating. An A (Excellent) is still a strong rating, but it’s no longer the A+ (Superior) it was.

6. The AARP Royalty Arrangement A portion of your premium flows to AARP as a royalty fee for brand licensing. You’re not paying for additional coverage — you’re partially funding a marketing relationship. Whether that bothers you is a personal judgment, but it’s worth knowing.

How Does It Compare to Competitors?

Here’s a side-by-side summary across the factors that matter most for a long-term Medigap decision:

| Factor | AARP / UHC | Mutual of Omaha | Aetna |

|---|---|---|---|

| AM Best Rating | A (Excellent) | A+ (Superior) | A (Excellent) |

| NAIC Complaint Index | ~0.68 | ~0.52 | ~0.74 |

| Plan G Monthly (age 65) | $160–$230 | $110–$165 | $105–$160 |

| HD Plan G Available | No (most states) | Yes | Yes |

| Household Discount | No (most states) | Yes (7–12%) | Yes (~6%) |

| Pricing Model | Community (43 states) | Attained-age | Attained-age |

| Enrollment Discount | Yes — phases out to age 81 | No | No |

The takeaway from this table:

- If long-term rate stability and community pricing are your priority, UHC has a structural advantage over attained-age carriers.

- If starting premium, household discount, or HD Plan G access matter to you, Mutual of Omaha and Aetna are worth a serious look.

- If financial strength rating is a priority, Mutual of Omaha’s A+ currently edges UHC’s A.

No single carrier wins on every dimension. This is exactly why working with a broker who represents all of them — and can run a personalized comparison for your specific state, age, and situation — is so valuable.

The AM Best Downgrade — What It Means for You

In August 2025, AM Best downgraded UnitedHealthcare’s Medigap-writing subsidiaries from A+ (Superior) to A (Excellent). The stated reason: significant deterioration in UHC’s operating performance, primarily driven by unexpected cost increases in their Medicare Advantage business — with the company projecting an additional $6.5 billion in medical expenses for 2025. You can verify UHC’s current rating directly at ambest.com and check their complaint history at content.naic.org/consumer.

What this means for current AARP/UHC Medigap policyholders: not much in the short term. An A (Excellent) rating means UHC still has excellent ability to meet its long-term financial obligations. The outlook is stable, meaning AM Best doesn’t anticipate further downgrades in the near term.

What it does illustrate: even the largest carrier in the Medigap market isn’t immune to rating changes. The financial strength you enrolled with can change. This is why we always recommend verifying ratings at ambest.com before enrolling — and checking periodically after.

So — Is It Worth the Premium?

Here’s my honest, experience-based answer after 18+ years in this business:

AARP/UHC is worth considering for you if:

- You want Plan G specifically — in many states they’re top 3 in pricing and rarely outside the top 5

- You live in one of the 43 states where community pricing applies and plan to keep your plan long-term

- You genuinely use a gym and the Renew Active benefit has real dollar value for you

- You’re enrolling at age 70 or older, where the enrollment discount phase-out matters less

- You want the broadest plan selection from a single carrier available in all 50 states

- Brand familiarity and name recognition genuinely matter to your peace of mind

AARP/UHC is probably not your best choice if:

- You’re considering Plan N — their pricing is significantly above market on this plan

- You want High-Deductible Plan G — UHC doesn’t offer it in most markets You and a spouse are both enrolling — the lack of household discount means

- you’re leaving savings on the table compared to carriers like Mutual of Omaha

- You enrolled several years ago in the older UHC book (not UHICA) — the enrollment discount may be driving your rate higher than alternatives

The most important thing I can tell you: Don’t choose AARP/UHC — or skip it — based on brand recognition alone. Run the actual numbers for your specific situation. That means getting quotes from at least three to four A-rated carriers in your state, understanding the pricing model each one uses, and asking about rate increase history.

The coverage is identical. The company and the cost are what actually differ.

If you’d like help running that comparison — including rate histories that aren’t publicly available — I’m happy to do it at no cost to you.

Call 631-358-5793 or visit paulbinsurance.com to schedule your free consultation.

Frequently Asked Questions

Is AARP the same as UnitedHealthcare for Medicare Supplement? No. AARP is a nonprofit advocacy organization that licenses its brand to UnitedHealthcare in exchange for royalty fees. UnitedHealthcare is the actual insurance company that underwrites, prices, and administers AARP Medicare Supplement plans. When you enroll in an AARP Medigap plan, your insurance company is UnitedHealthcare — AARP’s role is branding and marketing.

Do I have to be an AARP member to get an AARP Medicare Supplement plan? Yes. You must be an AARP member to enroll in an AARP/UHC Medigap plan. AARP membership costs approximately $20 per year. This is an additional cost that most competing carriers don’t require.

What is UHC’s enrollment discount and how does it work? AARP/UHC’s Medigap premiums in most states include a built-in discount that decreases as you age. At age 65, the discount is approximately 39%. It reduces by about three percentage points per year between ages 69 and 81. By age 81, the discount is fully gone and you pay the full undiscounted base rate. This creates premium growth above and beyond any general rate increases, particularly in your late 60s and 70s.

Does AARP/UHC offer High-Deductible Plan G? No — not in most states. High-Deductible Plan G is offered by carriers like Mutual of Omaha and Aetna but is not a standard part of UHC’s lineup in most markets. If HD Plan G is an option you want to consider, you’ll need to look at other carriers.

What is UHC’s AM Best rating after the 2025 downgrade? As of August 2025, UHC’s Medigap-writing subsidiaries hold an AM Best Financial Strength Rating of A (Excellent) — downgraded from A+ (Superior). The outlook is stable. An A (Excellent) is still a strong rating for a long-term insurance commitment, but it is one notch below where UHC was previously. Always verify current ratings directly at ambest.com before enrolling.

Can I switch from AARP/UHC to a different carrier? Yes — you can apply to switch at any time. Outside of specific guaranteed issue windows, you’ll need to pass medical underwriting, meaning the new carrier can ask health questions and may decline your application based on your health history. If you’re in good health, this is worth exploring — especially if your current premium has climbed significantly. In New York, you can switch carriers at any time without underwriting due to the state’s year-round guaranteed issue protections.

Why does AARP/UHC cost more than other carriers for the same Plan G? Several factors contribute. UHC pays royalty fees to AARP for brand licensing — a cost that flows through the premium structure. UHC is also the market leader by enrollment and doesn’t need to compete as aggressively on price. Their Renew Active fitness benefit adds a cost layer. And their enrollment discount structure means the starting premium isn’t always the apples-to-apples comparison it appears to be.

Is AARP/UHC a trustworthy company for claims? Yes. Their NAIC Medigap-specific complaint index of approximately 0.68 is well below the 1.0 national average — meaning they receive fewer complaints relative to their size than most carriers. Whatever people may feel about their premium increases, the actual claims-paying and customer service record is solid.

The Bottom Line

AARP/UHC is a real company offering real coverage backed by real financial strength. Their community pricing model in most states is genuinely favorable for long-term enrollees. Their customer service record is good. Their brand recognition brings real comfort to many seniors.

But they’re also consistently more expensive than most A-rated competitors for the same standardized benefits. Their enrollment discount structure creates compounding premium growth that many policyholders don’t fully understand until it’s already happening. They don’t offer HD Plan G in most markets. And they don’t offer household discounts.

The AARP name doesn’t make the plan better. The coverage inside is identical to what any other Medigap carrier offers for Plan G.

What matters is: which A-rated carrier offers the most stable, most affordable long-term cost in your specific state, at your specific age, given your specific situation?

That’s the question an independent broker — one who represents 40+ carriers with no allegiance to any of them — is specifically positioned to answer. And it won’t cost you a penny to find out.

Paul Barrett is the founder and Principal Agent of The Modern Medicare Agency, a Medicare-only independent brokerage based in Melville, NY. With 18+ years of Medicare-exclusive experience, licensure in 34 states, and relationships with 40+ carriers, Paul has helped 5,000+ clients navigate Medicare with clarity and confidence. He is the author of Medicare Mastery Unlocked.