-

By Paul Barrett, Principal Agent, The Modern Medicare Agency | Updated June 2026

Before You Read Another Word — A Disclosure You Deserve

Most articles comparing Medicare Supplement and Medicare Advantage are written by websites that earn money when you pick one over the other. Lead generation sites. Comparison engines. Affiliate marketers. Even some well-known names you’d recognize.

I don’t work that way.

I’m Paul Barrett. I’ve spent 18 years working exclusively in Medicare, representing 40+ carriers across 34 states. I am paid a commission whether you choose Medicare Advantage or a Medigap plan. My commission is actually higher on some Medicare Advantage plans than on the Medigap plans I most often recommend. I tell you this not to pat myself on the back — I tell you because it’s the thing that makes this article different from almost everything else you’ll find online.

I have no reason to push you in either direction. What I have is 18 years of watching both go right and both go catastrophically wrong. That’s what I’m going to give you here.

The Fundamental Difference in Two Sentences

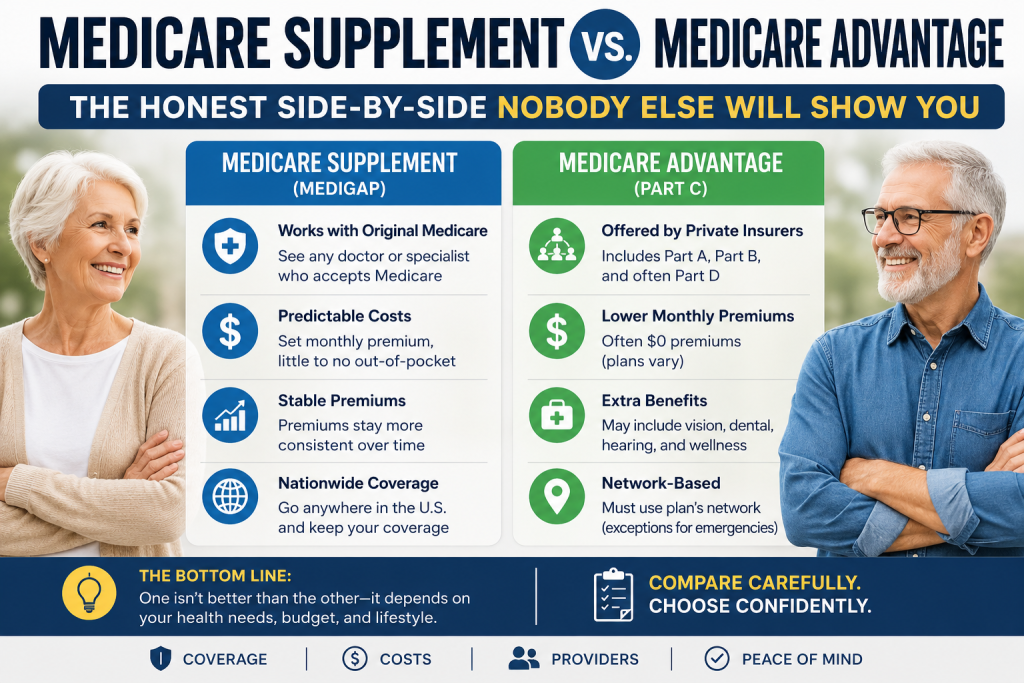

Medicare Advantage replaces Original Medicare with a private insurance plan. You get Medicare coverage through the plan — which means their network, their rules, their prior authorization requirements, and their annual benefit changes.

Medicare Supplement (Medigap) works alongside Original Medicare. Medicare remains your primary insurance; the Medigap policy covers what Medicare doesn’t. Any doctor who takes Medicare takes you — no networks, no referrals, no permission required.

Everything else in this article flows from that distinction.

The Numbers You Need to Know First

Before we compare, here are the verified 2026 Medicare baseline figures from CMS, because everything depends on these:

Cost Item

2026 Amount

Part B Monthly Premium

$202.90/month (everyone pays this regardless of which path you choose)

Part B Annual Deductible

$283

Part A Hospital Deductible

$1,736 per benefit period

Part A SNF Coinsurance (Days 21-100)

$217/day

Medicare Advantage MOOP Maximum

$9,250 in-network (average actual: $5,421)

HD Plan G Deductible

$2,950

Part D Out-of-Pocket Cap

$2,100

Source: CMS 2026 Medicare Costs; KFF Medicare Advantage in 2026

The Market Right Now: What’s Actually Happening

Before we get into which is better for you, you need to understand the landscape in 2026 — because it’s changed dramatically.

Approximately 54% of all Medicare beneficiaries are now enrolled in Medicare Advantage plans, reflecting their enormous growth over the past decade. At the same time, that growth is running into serious turbulence.

Approximately 10% of Medicare Advantage policyholders enrolled in non-employer HMO or PPO plans experienced forced disenrollment in 2026 when their current plan exited their county — a tenfold increase from historical averages, according to Johns Hopkins Bloomberg School of Public Health research published in JAMA. The forced disenrollment rate averaged just over 1% between 2018 and 2024, jumped to 6.9% in 2025, and reached 10% in 2026. About 2.6 million people lost Medicare Advantage coverage when their insurer pulled out of markets in 2026, and more than a million lost coverage for 2025.

Meanwhile, on the Medigap side: approximately 14 million Americans hold Medigap policies in 2026, a number forecast to grow as Medicare Advantage plan exits push seniors back to Original Medicare.

Why does this matter for your decision? Because the stability of your coverage type — not just the cost today — is part of what you’re choosing.

The Premium Trap: Why $0/Month Is Not Free

This is the most important thing I want you to understand, and it’s the thing Medicare Advantage marketing will never tell you clearly.

Three quarters (75%) of enrollees in individual Medicare Advantage plans with prescription drug coverage pay no premium other than the Medicare Part B premium in 2026. That $0 premium is genuine — you really don’t pay an additional monthly premium beyond the Part B premium everyone pays.

But $0/month is not the same as free.

Here’s what you’ll actually pay when you use your Medicare Advantage plan. These are typical ranges based on national averages — and this is important to understand: Medicare Advantage plan costs vary dramatically by geographic area, carrier, and plan type. A plan in rural Oklahoma looks nothing like a plan in suburban Boston. The figures below reflect common cost-sharing structures but your specific plan could be meaningfully higher or lower on any of these line items:

- Doctor copays: $5-$50 per visit depending on PCP vs. specialist (some plans charge $0 for PCP; others charge $35+)

- Hospital copays: Often $300-$400 per day for the first several days of a hospital stay (some plans front-load costs; others spread them differently)

- Outpatient surgery: 20% coinsurance in many plans, though some plans use flat copays of $200-$399

- Specialist visits: $45-$50 copay each on average, ranging from $0 to $75+ depending on plan

- Imaging (CT, MRI): $200-$300 per scan in many plans, but this varies widely

Always read the specific Summary of Benefits for any plan you’re considering — not the marketing materials, not the TV commercial. The actual Summary of Benefits document tells you exactly what you’ll pay for every covered service.

And here’s the number that matters most: the average out-of-pocket limit for Medicare Advantage enrollees is $5,421 for in-network services and $9,825 for in-network and out-of-network services combined in 2026.

That out-of-pocket maximum is a ceiling, not an expectation. But it’s a real ceiling — and if you hit it, you’ve paid $5,421 beyond your monthly Part B premium.

Compare that to Medigap Plan G: your total out-of-pocket exposure for covered Medicare services is $283 for the year — the Part B deductible. That’s it. After that, Plan G covers everything Medicare approves for the rest of the year. Zero hospital bills. Zero surgeon bills. Zero specialist bills.

The math question isn’t “which plan costs less per month?” The math question is “which plan costs less per year given how much care I actually use?” Those are very different questions.

Five Real Scenarios Where Medigap Wins

Scenario 1: You Have a Chronic Condition or Frequent Medical Needs

If you see specialists regularly, manage an ongoing condition, take multiple medications, or anticipate significant healthcare use — Medigap’s predictability is not just convenient, it’s financially superior.

A Medicare beneficiary with heart disease who has three specialist visits, a stress test, a cardiac procedure, and two hospital days in a year:

- With Plan G: $283 (Part B deductible). Everything else covered.

- With Medicare Advantage: Specialist copays + imaging + procedure coinsurance + hospital day copays. Depending on the plan, realistically $2,000-$6,000 or more.

The Medigap premium is higher every month. The total annual cost is often significantly lower the moment your health needs become substantial.

Scenario 2: Your Doctors and Hospitals Matter to You

This is the scenario that catches people most off guard. Medicare Advantage plans limit you to specific provider networks and typically don’t cover out-of-state care. Medigap, however, allows you to see any doctor in the U.S. who accepts Medicare.

If you are in an HMO — which accounts for more than 6 in 10 enrollees in individual Medicare Advantage plans — out-of-network care is generally not covered at all outside of emergencies. You are in that network, full stop.

The real-world consequence: a patient who enrolled in a Medicare Advantage HMO to save money on premiums discovered her preferred surgeon at a major academic medical center was out of network. Out-of-network surgical costs in that scenario can range from $30,000 to $60,000 — wiping out years of premium savings in a single procedure.

With Medigap, your surgeon is whoever your surgeon is. As long as they accept Medicare, you’re covered. Full stop.

Scenario 3: You Travel, Split Time in Multiple States, or Live Away from Home Seasonally

Medicare Advantage plans are geographically restricted. Medicare Advantage plans typically don’t cover out-of-state care. If you spend winters in Florida and summers in New York, or travel frequently across state lines, a network-based plan creates real access problems. Emergency care is always covered, but routine care and specialist visits require you to be within your plan’s service area.

Medigap has no service area. Any Medicare provider, any state, any time. For snowbirds, frequent travelers, or anyone who spends meaningful time in more than one location, this is a decisive advantage.

Scenario 4: You Want Certainty About What Your Healthcare Will Cost

For many retirees on fixed incomes — Social Security, pension, modest savings — the unpredictability of Medicare Advantage cost-sharing is the core problem. You cannot budget for a $0-$9,250 out-of-pocket range. You can budget for $283/year plus your known monthly premium.

Medigap delivers what no Medicare Advantage plan can: genuine, year-round cost certainty for covered medical services. Your bill from a hospital admission with Plan G is $0. Your bill from an outpatient procedure is $0. You know this in advance. That predictability has real dollar value for anyone managing retirement income carefully.

Scenario 5: You Need Specialist Access Without Gatekeeping

In most Medicare Advantage HMOs, you need a referral from your primary care physician to see a specialist. In Medigap, you call the specialist directly, show your Medicare card and Medigap card, and get your appointment. No referral. No prior authorization for most services. No waiting for approval.

For someone managing a complex condition who sees multiple specialists, the friction of managed care isn’t just an inconvenience. It’s a real barrier to timely care.

Five Real Scenarios Where Medicare Advantage Makes Sense

Let me be equally honest about when Medicare Advantage is the right answer — because it genuinely is for many people.

Scenario 1: You Are in Good Health and Use Medicare Minimally

If you are 65, in excellent health, take no regular medications, and primarily need preventive care and the occasional routine visit — Medicare Advantage’s low monthly premium can represent genuine value. Your copays for the few visits you make each year are manageable, you’ll likely never approach the out-of-pocket maximum, and you keep hundreds of dollars per month in your pocket.

The calculus changes when your health changes. But for truly healthy seniors in their initial Medicare years, the premium savings are real.

Scenario 2: Budget Is the Primary Constraint

Not everyone has $200-$350/month for a Medigap premium on top of their Part B premium. For seniors living on modest Social Security income, that monthly expense is simply not possible. A $0-premium Medicare Advantage plan is not the ideal healthcare solution — but it is a real and honorable choice for someone who cannot afford the alternative.

I tell this to every client: the best plan is the one you can maintain financially over years. A plan you can’t afford to keep does you no good.

Scenario 3: You Want Dental, Vision, and Hearing Coverage Included

Medigap covers what Medicare covers — and Medicare does not cover routine dental, vision, or hearing. Those benefits simply don’t exist in the Medigap world without purchasing separate standalone policies.

Many Medicare Advantage plans include some level of dental, vision, and hearing benefits. For someone who primarily needs regular cleanings, glasses, and a hearing exam, those bundled benefits can represent real value — particularly if they offset the need to purchase separate coverage.

The important caveat: these extra benefits vary enormously in quality, network adequacy, and dollar value. Some are genuinely useful. Some are so restricted in what they cover and where they can be used that the stated benefit doesn’t translate to meaningful real-world value. Always read the details.

Scenario 4: You Live in an Area With Robust MA Plan Options and a Stable Network

In major metropolitan areas with dense provider networks, competitive Medicare Advantage plans, and multiple carriers to choose from, the risk of network disruption is lower and the plan options are stronger. A senior in suburban Chicago with 15 Medicare Advantage plans available, multiple large health systems in network, and genuine dental and vision benefits bundled in may be genuinely better served by MA than by Medigap.

Geography matters enormously. The Medicare Advantage experience in a rural county with one available plan is completely different from the experience in a major metro area with broad plan competition.

Scenario 5: Prescription Drug Coverage Coordination Matters

Medicare Advantage plans typically include Part D drug coverage in the same plan. Medigap does not include drug coverage — you purchase a standalone Part D plan separately. For someone with complex medication needs who benefits from having one plan coordinate everything, the integrated MA-PD approach can simplify administration and sometimes optimize drug cost-sharing.

The Hidden Costs Both Sides Don’t Advertise

On the Medicare Advantage Side

Prior authorization is more pervasive than most people realize — and it’s coming to traditional Medicare too. In 2024, nearly 53 million prior authorization requests were submitted to Medicare Advantage insurers, with insurers denying 4.1 million — nearly 8% of those requests. A KFF survey found that 11% of all Medicare beneficiaries had a problem with prior authorization in the previous year, suggesting that about one in five MA enrollees experienced a prior authorization problem. An audit by the HHS Office of Inspector General found that 13% of prior authorization denials in MA were for services that met Medicare coverage rules — likely preventing or denying medically necessary care. Almost all Medicare Advantage enrollees — 99% according to KFF — must obtain prior authorization for some services.

A significant development worth knowing: Starting January 2026, CMS launched the WISeR Model (Wasteful and Inappropriate Service Reduction) — a six-year pilot program running through December 31, 2031, that introduces AI-assisted prior authorization to Original Medicare for the first time, in six states: New Jersey, Ohio, Oklahoma, Texas, Arizona, and Washington. The model covers 17 select services CMS has identified as vulnerable to fraud, waste, and abuse — including nerve stimulation, spinal steroid injections, cervical fusion, knee arthroscopy for osteoarthritis, and skin substitutes. It does not affect emergency or inpatient services.

This matters for anyone comparing the two coverage paths: prior authorization, long considered an MA-specific friction point, is now being tested inside traditional Medicare as well. The scale is currently limited — just under 628,243 prior authorization reviews for traditional Medicare beneficiaries were submitted to CMS in 2024, translating to about 2 prior authorization reviews per 100 traditional Medicare beneficiaries, compared to tens of millions in MA — but CMS has stated explicitly that WISeR data collected through 2031 will inform decisions about whether prior authorization expands to additional services and additional states. If you are in one of those six states and use any of the covered services, this is already part of your Original Medicare experience in 2026. If the pilot expands, it will change the prior authorization calculus for the traditional Medicare plus Medigap path going forward.

Your plan can change every year. Benefits that exist in 2026 are not guaranteed in 2027. Copay amounts, formulary tiers, dental allowances, gym memberships — all of it resets every January 1. What attracted you to the plan may not be there next year.

Your plan can exit your market entirely. As noted above, 10% of Medicare Advantage HMO and PPO enrollees faced forced disenrollment in 2026. When a plan exits, your doctors may leave with it — and switching to a new plan means a new network, new prior authorization rules, and potentially new drug formularies mid-treatment.

Out-of-network costs can be catastrophic in HMOs. If you’re in an HMO and you receive care outside the network — even inadvertently, even from an anesthesiologist you didn’t choose — you may be responsible for the full cost. This happens more often than the marketing materials suggest.

On the Medigap Side

The premium keeps going up — and there’s not always somewhere cheaper to go. Medigap Plan G premiums have increased 12%-26% in early 2026 filings, according to Telos Actuarial. In community-rated states like New York, where UHC is already the lowest-priced carrier, a 17.8% rate increase means everyone in the market moved up together. There may be no meaningful alternative to switch to.

Here’s something critical that’s often glossed over in Medigap marketing: the premium increase problem is frequently most acute in the first few years after enrollment. Many carriers offer enrollment discounts — sometimes called “welcome” or “introductory” discounts — that phase out over the first 3-5 years of your policy. A policyholder who started at $150/month might be paying $220/month five years later not because of one dramatic rate filing, but because a 10% general rate increase compounded with the gradual loss of that initial discount. When you’re shopping for Medigap coverage, ask your broker to show you not just the current rate, but the rate without any enrollment discounts — that’s the rate you’re trending toward as those discounts disappear. The combination of phasing enrollment discounts plus annual general rate increases can produce premium trajectories that look very different from the number you saw in the sales presentation.

You still pay the Part B deductible every year — and it increases. The $283 deductible in 2026 is not fixed. CMS adjusts it annually and it has risen consistently. The Part B premium itself has also increased significantly — rising from $185 to $202.90 in 2026 alone, a $17.90 jump that outpaced the 2.8% Social Security COLA, meaning the Part B increase ate more than a third of the average beneficiary’s Social Security raise. Healthcare costs under Medicare are consistently outpacing inflation, and that pressure affects everyone — regardless of which supplemental coverage path they choose.

No dental, vision, or hearing without separate policies. For seniors who need significant dental work, this gap is real money.

The open enrollment window closes and doesn’t fully reopen. Outside of your six-month initial enrollment window — and the limited guaranteed-issue exceptions — switching to Medigap requires answering health questions in most states. If your health has changed, you may be declined or charged more. (New York is a notable exception — more on this below.)

The Switching Trap: Why Getting Back to Medigap Later Is Harder Than People Think

This is the most consequential section of this entire article. Please read it carefully.

When you first turn 65 and enroll in Medicare Part B, you have a six-month Medigap Open Enrollment Period during which any carrier must accept you for any plan at standard rates — no health questions, no underwriting, no denials. This is the most valuable enrollment window in all of Medicare. Most people don’t fully understand what they’re giving up when they let it pass.

Here’s the trap. You enroll in a Medicare Advantage plan at 65 because the $0 premium is appealing and you’re healthy. Five years later, you’ve been diagnosed with diabetes, had a cardiac event, or received a cancer diagnosis. Now you want to switch to Medigap for the predictability and provider freedom. In most states, you can apply — but the Medigap carrier can now ask you health questions and deny your application based on those conditions. You wanted to switch. They said no. You’re stuck in managed care when you most need the freedom of Original Medicare.

This is not hypothetical. It happens constantly.

If you decide at some point to switch to Medicare Advantage, be sure to cancel your Medigap policy so you are not stuck paying the premium for something you cannot use. If you join a Medicare Advantage plan and are not satisfied, once you switch back to Original Medicare, you have a one-year period to return to your Medigap plan as long as it is offered in your state. That one-year trial period is your only protected pathway back in most states.

There are limited guaranteed-issue rights that allow you to get Medigap without underwriting outside of your initial window:

- Your Medicare Advantage plan is discontinued or leaves your service area

- You move out of your plan’s service area

- The plan’s contract with Medicare ends

But these are specific, limited exceptions — not a general right to switch whenever you want.

The New York exception: New York requires community-rated pricing and year-round guaranteed issue for Medigap. New Yorkers can apply for any Medigap plan at any time without medical underwriting. This is genuinely rare and valuable — but as we’ve documented in the rate increase data, it comes with premiums that are among the highest in the country precisely because the risk pool is open to all.

The broader point: The decision you make at 65, when you’re healthy and the $0 premium looks appealing, is a decision that will be very difficult to undo if your health changes. Underwriting risk is the hidden cost of Medicare Advantage that never appears in any comparison chart.

The 7-Question Decision Framework

Use these questions to think through which path makes sense for your actual situation — not the hypothetical version of your situation.

Question 1: How much healthcare do you currently use? If you see multiple doctors, have ongoing conditions, or take several medications — the copay structure of Medicare Advantage accumulates quickly. Run the math on your actual usage, not your optimistic projection.

Question 2: Do your current doctors accept Medicare? This is the right question — not “are they in my plan’s network.” If you start with Original Medicare and Medigap, any doctor who takes Medicare takes you. If that matters, it matters here.

Question 3: Do you travel, or live part of the year in a different location? If yes, a geographically restricted Medicare Advantage plan creates real problems. Medigap’s nationwide coverage is a genuine functional advantage.

Question 4: Can you afford the Medigap premium — and sustain it as it increases? Be honest. A plan you can’t maintain long-term doesn’t serve you. If the premium is genuinely unworkable, Medicare Advantage is a real and legitimate choice.

Question 5: How important is predictability to you? Some people are comfortable with the uncertainty of “I’ll pay whatever I use up to the out-of-pocket maximum.” Others find that uncertainty genuinely stressful and want to know their healthcare costs are fixed. Both are valid preferences. Medigap serves the second group definitively.

Question 6: What is your health trajectory? If your family history, your current conditions, or your doctor’s guidance suggests your health needs will increase — factor that into your decision. The window to get Medigap at standard rates without underwriting closes once your initial enrollment period ends.

Question 7: Are you comfortable with a managed care structure? Prior authorization requirements, network restrictions, referrals for specialists, annual plan changes — these are real features of Medicare Advantage, not bugs that some plans have and others don’t. If managing those requirements feels burdensome given your health situation, that’s meaningful data.

The MedPAC Validation You May Not Have Seen

The Medicare Payment Advisory Commission — Congress’s own independent Medicare advisory body — addressed this tension directly in its June 2026 Report to Congress. MedPAC’s June 2026 analysis found that while MA plans spend less per enrollee on medical services than traditional Medicare, the federal government actually pays more for MA enrollees than it would for the same people in traditional Medicare.

The key mechanism: according to MedPAC, plans receive an additional $2,664 per enrollee above their estimated costs of providing Medicare-covered services. That extra federal payment funds the supplemental benefits and low premiums that make MA attractive to consumers. It also funds the insurer’s profit margin and administrative costs.

The practical implication for you: the “extra benefits” in Medicare Advantage — the dental allowances, the gym memberships, the OTC cards — are not gifts from the insurer. They are funded by federal overpayments to the insurer. When those overpayment calculations change (as they did with the 2025-2026 payment adjustments that triggered the market exit wave), the benefits that attracted you can disappear.

Why There Will Always Be a Need for Both Options

Something worth saying plainly before we get to the bottom line: neither Medicare Advantage nor Medigap is going away, and the reason is structural — not political.

Medicare costs are consistently outpacing inflation. Part B premiums, Part B deductibles, and Medigap premiums are all rising faster than Social Security cost-of-living adjustments. The Part B premium increase in 2026 alone ate more than a third of the average beneficiary’s Social Security raise. Medigap Plan G premiums are rising 12-26% per year in many markets. The math of maintaining comprehensive Medigap coverage on a fixed retirement income is getting harder every year.

At the same time, Medicare Advantage plan instability — a 10% forced disenrollment rate in 2026, narrowing networks, benefit reductions — is pushing people back toward traditional Medicare and Medigap in meaningful numbers. About 440,000 people who lost Medicare Advantage coverage in 2026 did move to a Medicare supplement policy, according to Deft Research.

The honest reality is that the Medicare coverage landscape needs both options because no single solution serves everyone well:

- Someone in their first Medicare year, healthy, and budget-constrained may genuinely be better served by Medicare Advantage — today.

- Someone in their 75th year, managing multiple specialists, and living on a predictable pension may genuinely be better served by Medigap — today.

- And what serves someone today may not serve them in five years as their health changes, their finances shift, or their plan exits the market.

The most important thing you can do is make the decision deliberately, with full information, and revisit it regularly. That’s exactly what an independent broker is for.

Paul’s Bottom Line: What I Actually Tell My Clients

After 18 years and thousands of individual conversations, here’s the honest summary I give every client when they ask me directly:

For most people who can afford it, Medigap Plan G provides superior long-term financial protection and healthcare freedom — particularly as they age, their health needs increase, and the value of network-free access to any Medicare provider becomes more pronounced.

The case for Medicare Advantage is real and legitimate for healthy seniors on tight budgets, people who genuinely value the integrated supplemental benefits, and those who are well-served by the available plans in their specific geography.

The case against Medicare Advantage that I see most often in practice is not about the plan itself — it’s about the switching trap. The people who get hurt are the ones who chose MA at 65 in good health, developed health conditions that made leaving difficult, and found themselves locked into managed care at precisely the moment they needed the freedom of Original Medicare the most.

The decision you make at 65 is harder to undo than it looks from the outside. Make it with full information — not just about what each plan costs today, but about what each path looks like when your health changes.

Ready to Talk It Through?

If you’ve read this far, you’re taking this decision seriously — and you deserve a real conversation, not a sales pitch.

I’m happy to look at your specific situation: your doctors, your medications, your health history, your geography, your budget. I’ll tell you honestly what I think — even if the answer is Medicare Advantage.

Paul Barrett | The Modern Medicare Agency

(631) 358-5793 medicare@paulbinsurance.com paulbinsurance.com

(631) 358-5793 medicare@paulbinsurance.com paulbinsurance.comSources and Further Reading

- CMS: WISeR (Wasteful and Inappropriate Service Reduction) Model

- KFF: Examining the Potential Impact of Medicare’s New WISeR Model

- Congress.gov CRS: Overview of the Medicare WISeR Model

- Kiplinger: Prior Authorization Coming to Traditional Medicare

- KFF: Medicare Advantage in 2026 — Premiums, Out-of-Pocket Limits, Supplemental Benefits, and Prior Authorization

- KFF: Medicare Advantage Insurers Made Nearly 53 Million Prior Authorization Determinations in 2024

- KFF: A Snapshot of Sources of Coverage Among Medicare Beneficiaries

- Johns Hopkins Bloomberg School of Public Health: 1 in 10 Medicare Advantage Enrollees Face Forced Disenrollment in 2026

- AJMC: Unprecedented Spike in Plan Exits Threatens Medicare Advantage Stability

- AAMSI: Medigap Policyholders Forecast 2026

- CBS News/KFF Health News: Medigap Premiums Leap, and Consumers Have Few Alternatives (April 2026)

- CBPP: Growth in Medicare Advantage Raises Concerns

- MedPAC June 2026 Report to Congress — Chapter 1: Improving Payment Incentives in Medicare

- Medicare.gov: Compare Medigap Plan Benefits

- CMS 2026 Medicare Costs

- U.S. News: Medicare Advantage vs. Medigap

Paul Barrett is the founder and Principal Agent of The Modern Medicare Agency. He has worked exclusively in Medicare for 18+ years, holds licenses in 34 states, and represents 40+ carriers. He is the author of Medicare Mastery Unlocked and hosts the Insurance Wise Guys Podcast. This article is for educational purposes only. Individual circumstances vary — contact a licensed independent Medicare broker for guidance specific to your situation.

medicare@paulbinsurance.com

medicare@paulbinsurance.com

How to Check Your Medicare Enrollment Status: A Simple 2026 Guide

Imagine sitting at your kitchen table, staring at two different government websites and wondering which one actually holds the key to your healthcare…