Medicare Parts A and B, together called Original Medicare, form the foundation of federal health coverage for Americans turning 65. Part A covers hospital and inpatient care. Part B covers doctor visits and outpatient services. Most people need both to avoid serious coverage gaps and permanent financial penalties. This guide breaks down what each part covers, what it costs in 2026, and how to enroll without making costly mistakes. At Paulbinsurance, we have helped Medicare consumers navigate these decisions since 2007, and the confusion around Parts A and B is the most common starting point.

Medicare parts A and B explained: what they cover and why both matter

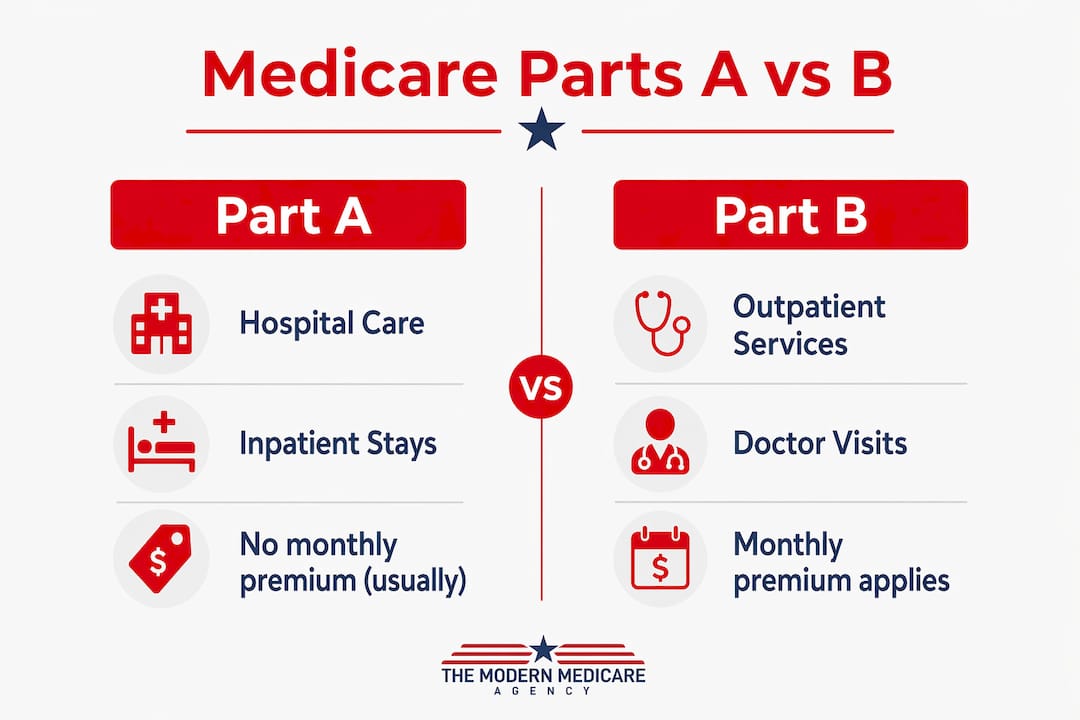

Original Medicare is made up of two distinct parts that work together. Part A handles the big inpatient events. Part B handles the ongoing outpatient care most people use every year. Think of it this way: Part A is your hospital insurance, and Part B is your medical insurance. You need both because neither one covers what the other does.

Most people approaching 65 assume Medicare is a single plan. It is not. Without Part B, a routine visit to your doctor or a lab test is not covered at all. Without Part A, a hospital stay can expose you to costs that run into the thousands. Understanding both parts before your enrollment window opens is the single most important step you can take.

What does Medicare Part A cover and how much does it cost?

Part A is hospital insurance. It covers inpatient hospital stays, care in a skilled nursing facility after a qualifying hospital stay, hospice care, and some home health services. If you are admitted to a hospital, Part A is the coverage doing the work.

The good news on cost: most people pay $0 in monthly premiums for Part A. That applies if you or your spouse worked and paid Medicare taxes for at least 40 quarters, which equals 10 years. That work history earns you premium-free Part A for life.

Cost-sharing under Part A works differently than a typical insurance plan. There is no annual deductible in the traditional sense. Instead, Part A uses benefit periods.

- Inpatient hospital deductible: $1,736 per benefit period in 2026

- Days 1–60: $0 coinsurance after the deductible

- Days 61–90: Daily coinsurance applies per benefit period

- Skilled nursing facility (days 21–100): Daily coinsurance applies

- Hospice care: Covered with minimal cost sharing for eligible patients

- Home health care: Covered when medically necessary and ordered by a doctor

A benefit period starts the day you are admitted and ends when you have been out of the hospital or skilled nursing facility for 60 consecutive days. If you are readmitted after that 60-day gap, a new benefit period begins and the $1,736 deductible applies again. That detail catches many people off guard.

Pro Tip: Part A does not cover emergency room visits unless you are formally admitted as an inpatient. If the hospital observes you but does not admit you, that is outpatient care under Part B. Always ask whether you are being admitted or placed under observation.

For a full breakdown of what Part A covers, the Part A benefits guide at Paulbinsurance walks through every category in plain language.

What services does Medicare Part B cover and what are its costs?

Part B is medical insurance. It covers outpatient care, doctor visits, preventive services, lab tests, mental health services, and durable medical equipment like wheelchairs and walkers. If you see a doctor outside of a hospital admission, Part B is almost always involved.

Part B has three cost layers you need to budget for:

- Monthly premium: The standard 2026 premium is $202.90 per month. Higher earners pay more through Income-Related Monthly Adjustment Amounts, known as IRMAA.

- Annual deductible: You pay the first $283 in covered services each year before Medicare starts sharing costs.

- Coinsurance: After the deductible, you pay 20% of the Medicare-approved amount for most covered services. Medicare pays the other 80%.

That 20% coinsurance has no annual cap under Original Medicare. A serious illness with frequent specialist visits or outpatient procedures can add up to thousands of dollars in a single year. That is not a worst-case scenario. It is a real risk that many beneficiaries face without supplemental coverage.

Preventive services are a notable exception. Annual wellness visits, flu shots, mammograms, and colonoscopies are covered at no cost to you when your provider accepts Medicare assignment.

Pro Tip: Budget for all three Part B cost layers before your coverage starts. The $202.90 premium is the visible cost. The deductible and 20% coinsurance are the ones that surprise people mid-year.

You can get a detailed look at how the Part B premium works and what factors affect your specific amount at Paulbinsurance.

What are the key differences between Medicare Part A and Part B?

The simplest way to separate them: Part A pays when you are admitted to a facility, and Part B pays when you see a provider outside of an admission. Both are necessary for complete Original Medicare coverage.

| Category | Medicare Part A | Medicare Part B |

|---|---|---|

| Type of coverage | Hospital and inpatient care | Outpatient and medical care |

| Monthly premium | $0 for most people | $202.90 standard in 2026 |

| Annual deductible | $1,736 per benefit period | $283 per year |

| Cost sharing | Coinsurance by day after deductible | 20% coinsurance after deductible |

| Enrollment | Automatic for most at age 65 | Must actively enroll |

| Out-of-pocket cap | None | None |

| Covers ER visits | Only if formally admitted | Yes, for outpatient ER visits |

| Covers doctor visits | No | Yes |

The enrollment difference is critical. Most people are automatically enrolled in Part A when they turn 65 if they are already receiving Social Security benefits. Part B requires an active decision. If you miss your window, you face a permanent penalty on top of the standard premium.

Original Medicare also has no annual out-of-pocket maximum for either part. That is a structural gap that sets it apart from most private insurance plans and makes supplemental coverage worth evaluating seriously.

How to enroll in Parts A and B and avoid late penalties

Enrollment timing is where most Medicare mistakes happen. The rules are specific, and the consequences for missing deadlines are permanent.

Your Initial Enrollment Period (IEP) is a 7-month window. It starts 3 months before the month you turn 65, includes your birthday month, and ends 3 months after. Enrolling in the first 3 months of your IEP means your coverage starts on the first day of your birthday month.

- If you are already on Social Security: You are automatically enrolled in both Part A and Part B. You will receive your Medicare card in the mail before your 65th birthday.

- If you are not on Social Security yet: You must actively sign up through the Social Security Administration, either online at SSA.gov, by phone, or in person at a local office.

- If you have employer coverage: You may qualify for a Special Enrollment Period (SEP) that lets you delay Part B without penalty while you remain covered by a current employer’s group health plan.

- If you retire and lose employer coverage: Your SEP gives you 8 months to enroll in Part B without a penalty starting from the date your employer coverage ends.

The Part B late enrollment penalty is permanent and adds up fast. For every 12-month period you were eligible but did not enroll, your monthly premium increases by 10%. That surcharge stays with you for life. On a $202.90 base premium, two years of delay adds roughly $40 per month forever.

COBRA and retiree health coverage do not count as qualifying employer coverage for SEP purposes. Enrolling in Part B while on COBRA is the right move in most cases.

The Paulbinsurance guide on avoiding late enrollment penalties covers every exception and scenario in detail, including what to do if you missed your window.

Key takeaways

Medicare Parts A and B together form Original Medicare, but Part B requires active enrollment and carries permanent penalties for late sign-up that most people do not realize until it is too late.

| Point | Details |

|---|---|

| Part A covers inpatient care | Hospital stays, skilled nursing, and hospice are covered with a $1,736 per-benefit-period deductible. |

| Part B covers outpatient care | Doctor visits, labs, and preventive services cost $202.90 per month plus 20% coinsurance in 2026. |

| No out-of-pocket maximum | Original Medicare has no annual cap, leaving beneficiaries exposed to unlimited cost-sharing. |

| Part B enrollment is not automatic | You must actively sign up during your Initial Enrollment Period or risk a permanent premium penalty. |

| Both parts are needed | Having only Part A leaves all outpatient costs uncovered; having only Part B leaves hospital costs exposed. |

What I have learned after nearly 20 years helping Medicare consumers

Most people come to me thinking Medicare is one thing. They hear “Medicare” and picture a single card that covers everything. The moment they realize it is actually a system of parts, each with its own costs and rules, the questions start coming fast.

The mistake I see most often is underestimating Part B. People focus on the premium because it shows up on their Social Security check. But the 20% coinsurance is the real exposure. If you have a joint replacement, a cancer diagnosis, or even a string of specialist visits, that 20% with no cap can cost more in a year than most people expect.

The second most common mistake is assuming COBRA or retiree coverage protects them from the Part B penalty. It does not. I have spoken with people who delayed Part B for two years on COBRA and then discovered they owe a permanent 20% surcharge on their premium for the rest of their lives. That is a painful and avoidable lesson.

My advice is always the same: learn Parts A and B first, then evaluate your supplemental options. You cannot make a good decision about a Medicare Supplement or Medicare Advantage plan if you do not understand what Original Medicare does and does not cover. Education comes first. The decisions follow naturally from there.

— Paul

How Medicare Supplement plans can fill the gaps in Original Medicare

Original Medicare leaves real financial exposure. The 20% Part B coinsurance and the per-benefit-period Part A deductible can add up to significant out-of-pocket costs, especially for people with ongoing health needs.

Medicare Supplement plans, also called Medigap, are designed to cover those gaps. Depending on the plan you choose, a Supplement can pay your Part B coinsurance, your Part A deductible, and even some foreign travel emergency costs. That turns unpredictable cost-sharing into a more manageable monthly budget. If you prefer a plan that bundles coverage differently, Medicare Advantage is an alternative worth comparing. The team at Paulbinsurance can walk you through both options based on your health needs and budget, with no pressure and no obligation.

FAQ

What is the difference between Medicare Part A and Part B?

Part A covers inpatient hospital care, skilled nursing facilities, and hospice. Part B covers outpatient services, doctor visits, preventive care, and durable medical equipment.

Do I have to pay a premium for Medicare Part A?

Most people pay $0 for Part A if they or their spouse worked and paid Medicare taxes for at least 40 quarters. Those who do not meet that threshold pay a monthly premium.

What happens if I miss my Medicare Part B enrollment window?

Missing your Initial Enrollment Period without a qualifying exception triggers a permanent penalty. Your monthly premium increases by 10% for every full 12-month period you were eligible but did not enroll.

Does Original Medicare have an out-of-pocket maximum?

No. Original Medicare has no annual out-of-pocket cap for either Part A or Part B, which means your costs can continue to grow without a ceiling.

Can I have Part A without Part B?

Yes, but it leaves a significant gap. Part A alone covers nothing for doctor visits, outpatient procedures, or lab work. Most people need both parts for complete basic coverage.