In New York, your health history cannot stop you from switching your insurance coverage, no matter what time of year it is. We know how overwhelming it feels to look at a list of over 40 different carriers and see price gaps of thousands of dollars for the exact same benefits. It’s frustrating to realize that a neighbor in Buffalo might pay hundreds less than someone in New York City for their medicare supplement plans in New York. You deserve clarity and a plan that doesn’t break the bank.

We’re here to help you cut through the noise and find a plan that protects your savings without sacrificing your choice of doctors. We understand the stress of choosing between Plan G and Plan N, especially when regional pricing makes the decision feel even more complex. This guide walks you through the 2026 landscape, explaining the specific rules that protect New York residents and showing you how to lower your monthly premiums. We’ll outline a simple, step by step path to finding a trusted local expert who can handle the paperwork for you, turning a confusing process into a journey toward certainty.

Key Takeaways

- Understand how these plans offer you the freedom to see any doctor in the country who accepts Medicare without needing a referral.

- Compare Plan G and Plan N to see if you’d rather have total cost predictability or lower premiums with small office visit copays.

- Learn why your specific zip code matters when shopping for medicare supplement plans in New York and how to avoid regional price traps.

- Discover how New York’s year-round enrollment rules allow you to switch your coverage at any time without worrying about your health history.

- Find out how we compare over 40 different carriers to help you secure the lowest possible rate for your 2026 coverage.

Understanding Medicare Supplement Plans in New York for 2026

Medicare is a wonderful foundation, but it isn’t perfect. Original Medicare usually covers about 80% of your outpatient costs, leaving you to pay the remaining 20% out of your own pocket. This is where medicare supplement plans in New York come in. We like to think of these plans as a safety net that catches the costs Medicare misses, such as deductibles and coinsurance. By choosing one of these plans, you are choosing a predictable way to eliminate surprise medical bills in 2026.

One of the biggest reasons our clients choose these plans is the freedom they provide. You aren’t restricted to a small network of local doctors or forced to get referrals for every specialist visit. In 2026, these plans remain the gold standard for healthcare freedom. You can see any provider in the United States who accepts Medicare. Whether you’re visiting family in Florida or seeing a specialist in Manhattan, your coverage follows you. It’s about giving you control over your own health journey.

These policies work seamlessly alongside your existing coverage. When you use Medicare Part A for hospital stays and Part B for doctor visits, your supplement plan automatically pays its share. For a deeper look at the standardized options available, Understanding Medigap Plans can help you see how different plan letters provide different levels of protection. We take the time to explain these differences so you can feel confident in your choice.

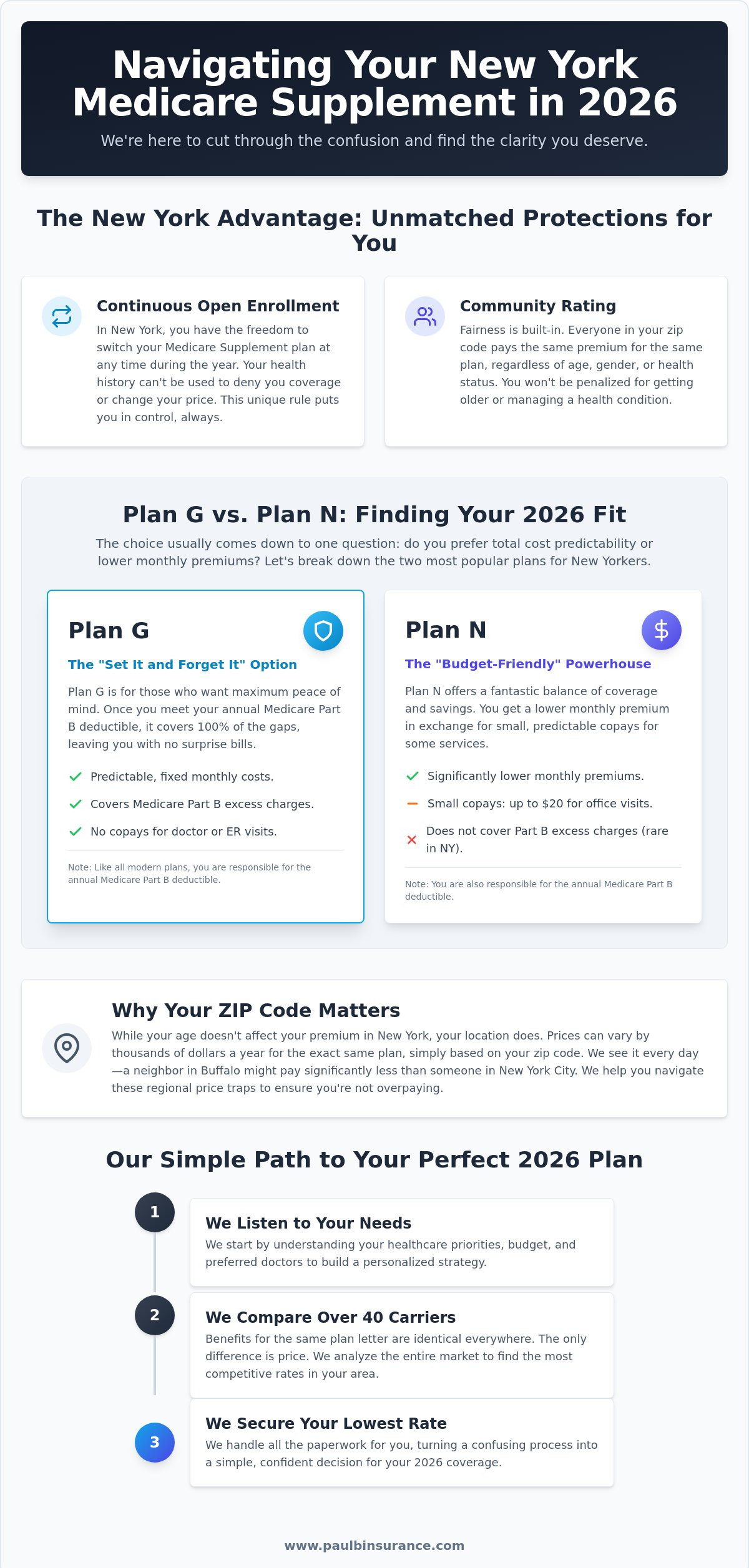

The “NY Difference”: Community Rating Explained

New York is unique because it requires “Community Rating” for all its supplement plans. In most other states, your price goes up as you get older or if your health declines. That doesn’t happen here. Everyone in your area pays the same premium regardless of their age, gender, or medical history. This makes New York one of the most consumer-friendly states in the country. It ensures that you aren’t penalized for simply getting older or managing a chronic condition. It provides a level of fairness that is hard to find elsewhere.

Why 2026 is a Critical Year for NY Medigap

The landscape is changing this year. Inflation adjustments have shifted the Part B deductible, making it even more important to have a plan that manages your out-of-pocket limits. We’ve also seen some insurance carriers exit the New York market recently. This makes it vital to work with an independent broker who can compare over 40 different options for you. Most new enrollees in 2026 are moving toward Plan G or Plan N because these two options offer the best balance of monthly cost and comprehensive protection in the current market.

Comparing the Best Medigap Plans in New York: Plan G vs. Plan N

Choosing between the two most popular medicare supplement plans in New York often comes down to one simple question: do you prefer a fixed monthly cost or a lower premium with small occasional copays? In 2026, the vast majority of our clients find their perfect fit in either Plan G or Plan N. Both plans offer incredible freedom, but they handle your out of pocket costs differently. We’re here to help you weigh the monthly savings of one against the total peace of mind offered by the other.

While we focus on these two, it’s worth a quick mention that Plan F is still around for some. If you were eligible for Medicare before January 1, 2020, you might still have access to Plan F. However, for most people entering the system today, the choice sits firmly between G and N. When researching Top-Rated Medigap Companies, you’ll notice that the benefits for Plan G or Plan N are identical across every carrier. The only real difference is the price they charge you.

Plan G: The “Set It and Forget It” Option

Plan G is currently the favorite for New Yorkers who want zero surprise costs. Once you pay your annual Part B deductible, this plan covers 100% of everything else Medicare leaves behind. It covers your hospital stays, doctor visits, and even those pesky excess charges that some providers might bill. We often recommend this to clients who want a predictable monthly budget because it removes the guesswork from healthcare spending. You can think of Plan G as a safety net that catches every medical expense Medicare leaves behind, ensuring you never face a bill you didn’t expect. It’s the ultimate plan for those who want to see any doctor, anywhere, without reaching for their wallet at the front desk.

Plan N: The “Budget-Friendly” Powerhouse

If you’re looking to keep your monthly fixed costs as low as possible, Plan N is an excellent choice. Plan N premiums in New York can be significantly lower than Plan G, often saving residents over $1,000 a year in premiums. In exchange for that lower monthly bill, you agree to pay a small copay of up to $20 for some office visits and up to $50 for emergency room visits. For healthy New Yorkers who don’t visit the doctor every week, these small copays are a minor trade off for the massive annual savings. It still provides the same great access to specialists and hospitals, just with a slightly different cost structure. If you’re feeling stuck between these two, we can help you run a personalized comparison of Medicare Supplement (Medigap) Plans to see which fits your lifestyle best.

The Cost of Medigap in New York: Why Your Zip Code Matters

It often comes as a surprise to our clients that living just a few miles away can change the price of your insurance. While New York uses a community rating system, this doesn’t mean there’s one single price for the entire state. Instead, the state is divided into several rating regions. This means that while your health status won’t affect your premium, your home address certainly will. We see price gaps where the exact same Plan G coverage can vary by $100 or even $400 per month depending on whether you’re in Manhattan or a rural county upstate. It’s a confusing system, but we’re here to help you find the logic in it.

The New York State Department of Financial Services oversees these regional boundaries and approves the rates carriers charge. They ensure that within your specific region, every person buying the same plan from the same company pays the same price. This protection is wonderful because it means you’ll never be charged more just because you have a heart condition or a history of cancer. However, it also means you must be very careful to compare all 40+ carriers available in your specific zip code. Because the benefits are standardized by law, paying more for the same lettered plan doesn’t get you better coverage; it just costs you more money.

Medigap Pricing in NYC and Long Island

If you live in the 100-104 zip codes of New York City or the 110-119 areas of Long Island, you’re in the highest-cost regions in the state. In 2026, premiums here trend significantly higher than the statewide average of $483 for Plan G. Because these areas are so competitive, some carriers offer “outlier” rates to attract new members. We often use our Melville office as a hub for local Long Island expertise to help neighbors navigate these high-cost waters. We don’t want you to overpay simply because you live in a specific neighborhood.

Upstate New York Rate Trends

Moving north to Albany, Rochester, or Buffalo usually brings lower monthly costs for medicare supplement plans in New York. In the Albany area, for example, some popular Plan G options are available for around $342.50 per month in 2026. While regional carriers like Highmark or Excellus have a strong presence in these areas, we often find that national carriers provide the most aggressive pricing. We help Upstate residents look beyond the local names to see if a national provider can offer the same robust protection for a much smaller monthly bill. Our goal is to move you from a state of price uncertainty to a place of total financial peace.

NY’s Secret Weapon: Continuous Open Enrollment

In most states, buying a Medigap plan feels like a high-stakes gamble. If you don’t pick the right one during your first six months of Medicare, you might be locked in for life. If you develop a health condition later, insurance companies in other parts of the country can deny your application or charge you much higher premiums. This is not the case for medicare supplement plans in New York. Our state has a “secret weapon” that protects you every single day of the year.

New York law requires continuous open enrollment. This means you can buy or switch your plan 365 days a year. You will never have to answer a single medical question to qualify for coverage. Whether you are perfectly healthy or managing a serious illness, the price you pay is the same as everyone else in your region. We use this unique flexibility to help our clients “shop” their rates annually. If your current carrier raises prices in 2026, we simply move you to a more affordable option with the exact same benefits. You are never trapped in a plan that no longer fits your budget.

Switching Plans Without the Stress

Moving from one plan to another is a straightforward process when you have a guide. We start by looking at your current premium and comparing it against the 40+ carriers available in your zip code. Once we find a better rate, we handle the application and ensure your new coverage starts exactly when the old one ends. You don’t have to wait for the Fall Open Enrollment period to make a change. In NY, “Open Enrollment” is every day of the year. You have the power to save money whenever a better deal appears, and we make sure the transition is seamless.

Guaranteed Issue Rights in New York

This law provides a massive amount of security for your future. We’ve seen carriers leave the New York market before, and it can be scary to think your coverage might disappear. However, your guaranteed issue rights mean you can always find a new home with another insurer without being penalized for your health. Your coverage can never be cancelled because of your medical history. This level of protection is why we encourage everyone to review our Medicare Supplement (Medigap) Plans overview to see how these laws work in your favor. You are never stuck, and you are never alone in this process.

If you feel like you are paying too much for your current coverage, we can help you find a better rate in minutes. Let us compare your 2026 options today.

How We Find Your Perfect New York Medicare Supplement

We’ve explored the unique rules, the regional price gaps, and the different levels of coverage available for 2026. Now, the final step is making sure you don’t have to face the overwhelming list of 40+ carriers alone. As independent brokers, we don’t work for the insurance companies. We work for you. Our mission is to protect your interests and your savings, acting as a shield between you and the high-pressure tactics of the insurance industry. We are your advocates, your educators, and your guides through this entire process.

When we look for medicare supplement plans in New York, we use a sophisticated system to compare every available option in your specific zip code simultaneously. We identify the lowest rates for your region while ensuring the carrier has a strong reputation for reliability. Our service is 100% free to you. The insurance companies pay us for our work, which allows us to provide unbiased, expert advice at no cost to your household. We believe everyone deserves access to clear, simple information without a hidden price tag attached.

Our relationship doesn’t end once your application is approved. We provide year-round support to help you with claims, answer questions about your benefits, or monitor rate changes. If a carrier raises their price in the future, we’ll be the first to let you know and help you switch to a more affordable option. We turn a one-time transaction into a lifelong partnership built on trust and security.

The Modern Medicare Agency Advantage

There’s a significant difference between a local NY broker and a national call center. We understand the regional nuances of medicare supplement plans in New York, from the specific zip code boundaries in Long Island to the carrier preferences in Buffalo. A national representative often misses these details, but we live and work here too. Our “Simplicity First” approach means we handle the paperwork and the follow-up calls so you don’t have to. We also ensure your Medigap policy is perfectly integrated with Medicare Part D, creating a complete coverage package that leaves no gaps in your protection.

Start Your Journey to Certainty Today

We invite you to reach out for a personalized rate comparison. There’s no reason to feel anxious or confused when a clear path to savings is just a conversation away. We’re committed to removing the stress from your healthcare decisions and replacing it with the peace of mind you deserve. Let us help you move from a state of uncertainty to one of total financial confidence. Contact us for a free New York Medigap quote and see how much you can save in 2026.

Take the Next Step Toward Healthcare Peace of Mind

Finding the right coverage shouldn’t feel like a second job. We’ve shown you how New York’s unique laws protect your ability to switch plans 365 days a year without health questions. You now know that while your zip code influences your premium, your medical history never will. This freedom is your greatest advantage in 2026. By comparing the top options side by side, you can stop overpaying and start feeling secure in your coverage.

We’re here to make the transition simple. As independent experts, we provide unbiased consultations at zero cost to you. We’ll look at over 40 different carriers to find the most competitive medicare supplement plans in New York for your specific neighborhood. Our team handles all the paperwork and ensures your transition is seamless, so you can focus on enjoying your life instead of worrying about medical bills. We are licensed experts who specialize in these local rules to keep you protected.

You deserve a plan that fits your life and a guide who truly cares. We’re ready to help you find that certainty today.

Frequently Asked Questions

Can I be denied a Medicare Supplement plan in New York due to my health?

No, you cannot be denied coverage or charged a higher rate due to your health history in New York. State law requires that all medicare supplement plans in New York be offered to every applicant regardless of their medical condition. This protection is a cornerstone of the New York market. It ensures that even those with chronic illnesses have access to the same robust coverage and pricing as everyone else in their region.

When is the best time to apply for Medigap in New York State?

The best time to apply is whenever you feel your current coverage isn’t meeting your needs because New York allows you to enroll 365 days a year. Unlike most states where you have a limited window, we can help you switch or start a plan at any time. If you find your current premium is increasing or your budget has changed in 2026, you don’t have to wait for a specific season to find a better deal.

What is the difference between Plan G and Plan N in New York?

The main difference lies in how much you pay at the doctor’s office versus what you pay each month for your premium. Plan G covers 100% of the gaps in Medicare after you meet your annual Part B deductible. Plan N usually has lower monthly premiums but requires small copays of up to $20 for office visits and $50 for emergency room visits. we help you look at your visit frequency to see which option saves you more.

Why are Medigap premiums so much higher in NYC than in Buffalo?

Prices vary because New York is divided into specific rating regions where the cost of medical care and local utilization differ. Insurance carriers set their rates based on the claims experience in those specific zip codes. While a resident in Buffalo might see lower averages, someone in NYC is in a higher cost region. Even so, we compare all 40+ carriers to ensure you’re getting the best possible rate for your specific neighborhood.

Do I need a separate Part D plan if I have a Medicare Supplement?

Yes, you will need a separate Part D plan because medicare supplement plans in New York do not include prescription drug coverage. We recommend pairing your Medigap policy with a standalone Part D plan to ensure you don’t face late enrollment penalties from Medicare. We can help you look at your current medications to find the drug plan that offers the best value alongside your supplement, keeping your total costs as low as possible.

Can I switch from Medicare Advantage back to a Medigap plan in NY?

Yes, you can switch from a Medicare Advantage plan back to a Medigap plan at any time during the year. Because of New York’s unique rules, you won’t face health questions or medical underwriting during this transition. It’s a common move for people who want more freedom to choose their doctors or who want more predictable out of pocket costs. We can guide you through the timing to ensure you don’t have a gap in your protection.

Does New York allow “Attained-Age” pricing for Medigap?

No, New York does not allow “Attained-Age” pricing, which would cause your rate to increase simply because you got a year older. Instead, all plans in the state must be “Community Rated.” This means every person in your rating region pays the same premium for the same plan, regardless of their age or gender. It provides a level of price stability that residents in many other states don’t get to enjoy as they age.

Are there any discounts available for Medigap plans in New York?

Yes, many carriers offer small discounts that can lower your monthly bill. The most common is a household discount for two people living together, even if only one person is applying for a policy. Some companies also offer minor savings if you set up automatic payments from a bank account. We always check for these available savings when comparing the 40+ different options for you to ensure you keep more of your own money.