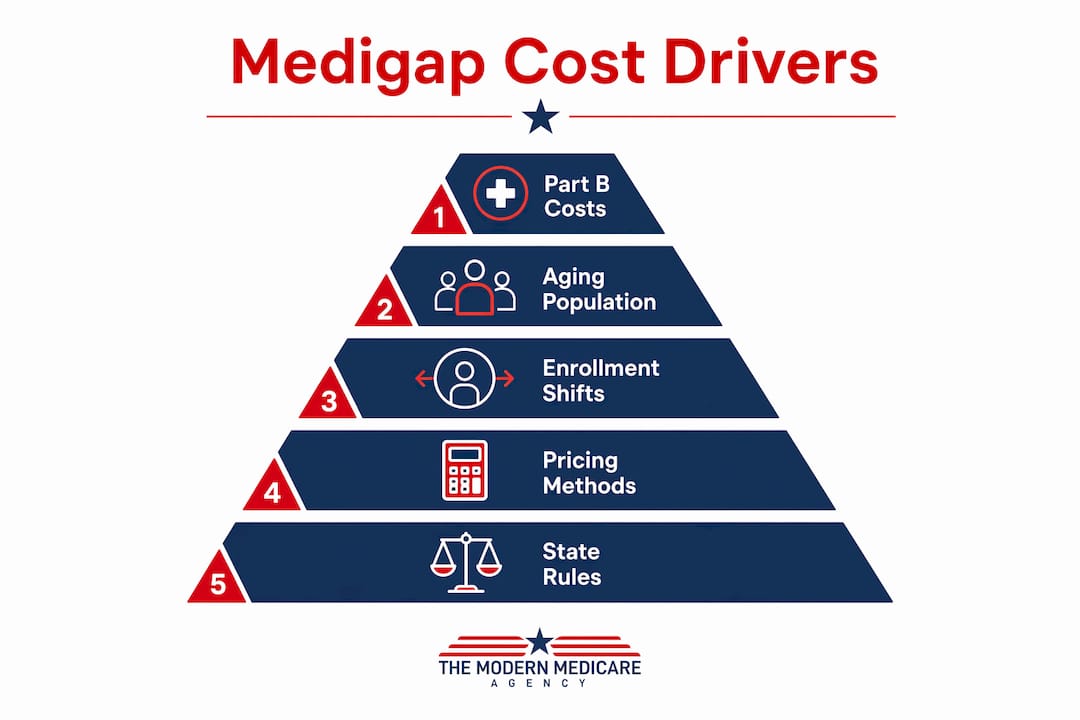

Medicare Supplement premiums rise because insurers face higher claims costs driven by increased medical service use, rising Medicare Part B premiums, an aging beneficiary population, and shifting risk pools caused by Medicare Advantage market instability. These are not random price hikes. Each increase traces back to a specific, measurable force inside the healthcare and insurance markets. Understanding why medicare supplement premiums rise gives you real power to make smarter coverage decisions, whether you are approaching Medicare eligibility or already enrolled in a Medigap plan.

Why do Medicare supplement premiums rise every year?

The most direct cause is the rising cost of Medicare Part B. The 2026 Part B premium rose 9.7% to $202.90 per month. That single increase ripples through every Medigap plan because Medigap covers the 20% coinsurance that Medicare does not pay on Part B services. When Part B costs go up, Medigap claims go up automatically.

The Part B annual deductible also rose by $26 to $283 in 2026. That adds to the total cost burden that Medigap plans absorb. The math is straightforward: more cost exposure for the insurer means higher premiums for you.

The relationship between Part B costs and Medigap claims is not one-to-one. For every $1 increase in Part B covered services, Medigap claims typically rise $0.20, but actual claims often accelerate faster because Medigap enrollees tend to use more healthcare services than average. This nonlinear effect pushes premium inflation above what the raw Medicare cost numbers suggest.

Medicare also makes annual changes to deductibles and copayments that directly affect supplemental plan costs. Rising spending on physician services, outpatient care, and drugs compounds the pressure year after year.

| Year | Part B Monthly Premium | Part B Annual Deductible |

|---|---|---|

| 2024 | $174.70 | $240 |

| 2025 | $185.00 | $257 |

| 2026 | $202.90 | $283 |

The table above shows a clear upward trend. Each year’s increase feeds directly into the claims costs that Medigap insurers must cover.

Pro Tip: Check your Part B premium changes each fall during the Medicare Annual Enrollment Period. A jump in Part B costs is a reliable early signal that your Medigap premium will also increase in the coming year.

How do demographics and enrollment shifts push costs higher?

An aging beneficiary population is a structural driver of rising Medigap costs. Older beneficiaries use more healthcare services, generating more claims and higher insurer costs. As the overall Medicare population ages, the average claims cost per enrollee rises, and insurers adjust premiums to keep up.

The Medicare Advantage market adds another layer of pressure. When Medicare Advantage plans exit a region or reduce their service areas, the beneficiaries they leave behind often move into Medigap plans. These members enter Medigap pools without medical underwriting, meaning insurers cannot screen for pre-existing conditions. The result is a risk pool that suddenly includes sicker, higher-cost members.

This is one of the most overlooked reasons for premium spikes. A healthy Medigap enrollee who has been in the same plan for years may see a sharp rate increase that has nothing to do with their own health. The increase reflects the higher average cost of the entire pool, not just their individual claims.

Key demographic and enrollment factors driving premium increases include:

- Aging enrollees: Longer plan tenure means higher average age and greater healthcare use per member.

- Medicare Advantage exits: Plan withdrawals push sicker members into Medigap without underwriting.

- Guaranteed-issue rights: Federal law requires insurers to accept certain enrollees regardless of health status, which raises pool risk.

- Utilization rates: Medigap enrollees historically use more services than Medicare Advantage members, partly because there are no network restrictions or prior authorization requirements.

- Enrollment timing: Beneficiaries who delay Medigap enrollment and later switch often bring higher claims histories into the pool.

Pro Tip: If a Medicare Advantage plan in your area is exiting, act quickly. You may have a guaranteed-issue window to enroll in a Medigap plan without underwriting. Missing that window could mean health questions and possible denial later.

How do insurer pricing methods and state rules affect your rate?

State regulations, pricing methods, and guaranteed-issue rules significantly influence how premiums rise and vary from one zip code to the next. The pricing method an insurer uses is one of the biggest factors in how fast your premium grows over time.

There are three main pricing structures:

Attained-age pricing ties your premium to your current age. Your rate increases every year as you get older, on top of any general rate increases the insurer applies. This method produces the steepest long-term cost growth.

Issue-age pricing sets your premium based on your age when you first enrolled. Your rate does not increase simply because you age, though general rate increases still apply. This method is more predictable over time.

Community-rated pricing charges every enrollee in a plan the same premium regardless of age. Younger enrollees pay more upfront, but older enrollees avoid the age-driven increases that come with attained-age plans.

| Pricing Method | Premium Tied To | Long-Term Cost Growth |

|---|---|---|

| Attained-age | Current age | Highest |

| Issue-age | Age at enrollment | Moderate |

| Community-rated | Same for all ages | Most predictable |

State rules add another layer. Some states have birthday rules that allow enrollees to switch plans annually without underwriting, which can help beneficiaries find lower rates. However, these rules also create adverse selection risk for insurers, because healthier members switch away while sicker members stay. Insurers respond by raising rates across the remaining pool.

Guaranteed-issue rights, required under federal law, force insurers to accept certain enrollees without health screening. This protects beneficiaries but increases insurer risk. The cost of that risk gets spread across all policyholders through higher premium rates.

Some insurers reported Plan G premium increases ranging from 12% to over 26% in early 2026. That range reflects differences in state regulations, insurer risk pools, and pricing methods. Two people in different states with identical health profiles can face very different rate increases for the same plan letter.

What can you do to manage rising Medigap costs?

Annual review of your Medicare Supplement coverage is the single most effective action you can take. Agents recommend comparing plans yearly because switching rules and health underwriting can limit your options if you wait too long. A plan that was competitive two years ago may no longer be the best value in your market.

Here are the steps Paulbinsurance recommends for managing premium increases:

- Review your current premium every fall. Compare it against current market rates for the same plan letter in your area. Rates vary significantly by insurer even for identical coverage.

- Check your switching rights. Outside your initial enrollment period, switching Medigap plans typically requires answering health questions. Know your rights before your options narrow.

- Understand your state’s birthday or anniversary rules. Some states allow annual plan switches without underwriting. This is a valuable tool if your current insurer raises rates sharply.

- Evaluate Medicare Advantage as an alternative. Medicare Advantage plans often carry lower monthly premiums, but they come with networks, prior authorization requirements, and out-of-pocket cost structures that differ significantly from Medigap. Weigh the trade-offs carefully based on your health needs and financial situation.

- Work with an independent agent. An independent agent has access to multiple insurers and can show you real rate comparisons. Captive agents represent only one company and cannot show you the full market.

- Factor in total cost, not just premium. A lower Medigap premium may come with a higher plan deductible. Calculate your expected total annual cost, including premiums, deductibles, and any out-of-pocket exposure.

Medigap premiums are rising faster than general inflation due to healthcare labor costs, higher utilization, and regulatory impacts on insurer risk pools. Automatic renewal without review is a costly habit. The market changes every year, and your coverage decision should reflect current conditions, not the ones that existed when you first enrolled.

Key Takeaways

Medicare supplement premiums rise because of compounding forces: higher Part B costs, aging enrollees, Medicare Advantage market instability, and insurer pricing methods that amplify each of these pressures over time.

| Point | Details |

|---|---|

| Part B drives Medigap costs | The 2026 Part B premium rose 9.7% to $202.90, directly increasing Medigap claims costs. |

| Risk pool shifts matter | Medicare Advantage exits push sicker members into Medigap pools, raising rates for all enrollees. |

| Pricing method shapes growth | Attained-age plans produce the steepest long-term increases; community-rated plans are most predictable. |

| Annual review is non-negotiable | Rates vary by insurer and state; comparing plans yearly is the most effective cost management tool. |

| Act during guaranteed-issue windows | Missing a guaranteed-issue window can mean health underwriting and possible denial of coverage later. |

What I’ve learned after nearly two decades helping Medicare consumers

Most people focus on the headline number when they get a premium increase notice. They see a $30 or $40 monthly jump and immediately assume their insurer is being unreasonable. What they miss is the chain of events behind that number: a Part B increase in the fall, a Medicare Advantage plan that exited their county, and an insurer absorbing a wave of new high-cost enrollees without any ability to underwrite them.

The Medicare Advantage instability factor is the one that surprises people most. I have seen beneficiaries in perfectly good health receive significant rate increases simply because their Medigap risk pool changed around them. That is not a flaw in the system. It is how insurance math works. But it means you cannot evaluate your Medigap plan in isolation. You have to understand what is happening in the broader Medicare market in your area.

The other mistake I see constantly is waiting. Beneficiaries receive a rate increase, decide to shop around, and then discover they are outside their guaranteed-issue window and face health questions they cannot pass. The time to review your coverage is before the increase hits, not after. Every fall, before the Medicare Annual Enrollment Period closes, is the right moment to sit down with an independent agent and look at the full picture.

Working with someone who represents multiple insurers, not just one, is the difference between seeing the market and seeing a single company’s product line. At Paulbinsurance, that independent perspective is the foundation of everything we do.

— Paul

Paulbinsurance can help you make sense of your Medicare options

Rising premiums do not have to catch you off guard. Paulbinsurance specializes in helping Medicare consumers understand exactly what is driving their costs and what their real options are in the current market.

Whether you are comparing Medicare supplement costs for the first time or looking at whether a Medicare Advantage plan makes more sense given today’s premium environment, the team at Paulbinsurance brings independent, education-first guidance to every conversation. Paul Barrett has been helping Medicare consumers since 2007, and the team works across Medicare supplements, Medicare Advantage, Part D, and a full range of senior insurance products. Reach out to get a clear picture of your options before your next renewal.

FAQ

Why did my Medigap premium go up if my health did not change?

Medigap premiums reflect the claims costs of your entire risk pool, not just your individual health. If sicker members joined your pool or overall utilization increased, your rate rises even if you personally had no claims.

What is the difference between attained-age and community-rated pricing?

Attained-age pricing increases your premium every year as you age, producing the steepest long-term cost growth. Community-rated pricing charges every enrollee the same amount regardless of age, making costs more predictable over time.

Can I switch Medigap plans to get a lower premium?

Switching is possible but may require answering health questions outside of your initial enrollment or a guaranteed-issue window. Some states have birthday or anniversary rules that allow annual switches without underwriting.

How does Medicare Advantage affect Medigap premiums?

When Medicare Advantage plans exit a market, the beneficiaries they leave behind often move into Medigap without medical underwriting. This introduces higher-cost members into Medigap risk pools, which pushes premiums up for all enrollees.

How often should I review my Medicare Supplement plan?

Review your plan every year, ideally each fall before the Annual Enrollment Period closes. Rates and market conditions change annually, and comparing current options is the most reliable way to avoid overpaying.