Did you know that about 8% of people on Medicare are currently paying much more than the standard $202.90 monthly premium because of a tax return they filed two years ago? It feels confusing and even a bit unfair to be charged extra today based on what you earned back in 2024. We know that watching your Social Security COLA get swallowed up by the new $283 deductible and rising premiums can cause a lot of anxiety.

We believe you deserve total clarity and peace of mind regarding your healthcare budget. If you want to know how to minimize medicare part b premiums in 2026, we are here to help. We designed this guide to replace your stress with a clear, expert-backed plan to protect your retirement savings and lower your monthly costs.

We will walk you through the new 2026 IRMAA brackets, explain how to use Form SSA-44 to appeal surcharges if your circumstances have changed, and show you how to avoid lifelong late-enrollment penalties. You’ll finish this article feeling confident that you aren’t overpaying for your coverage and that your budget is secure.

Key Takeaways

- Learn why Medicare costs are shifting in 2026 and how to protect your retirement budget from rising premiums and deductibles.

- Discover effective ways how to minimize medicare part b premiums through smart income timing and charitable giving strategies.

- Understand the two-year lookback rule so you can anticipate how your 2024 income affects your current monthly bills.

- Find out if you qualify for a premium reduction through the life-changing event appeal process using Form SSA-44.

- See how an independent guide can help you navigate dozens of plan options to ensure you never pay more than necessary.

The 2026 Medicare Part B Landscape: Why Are My Premiums Rising?

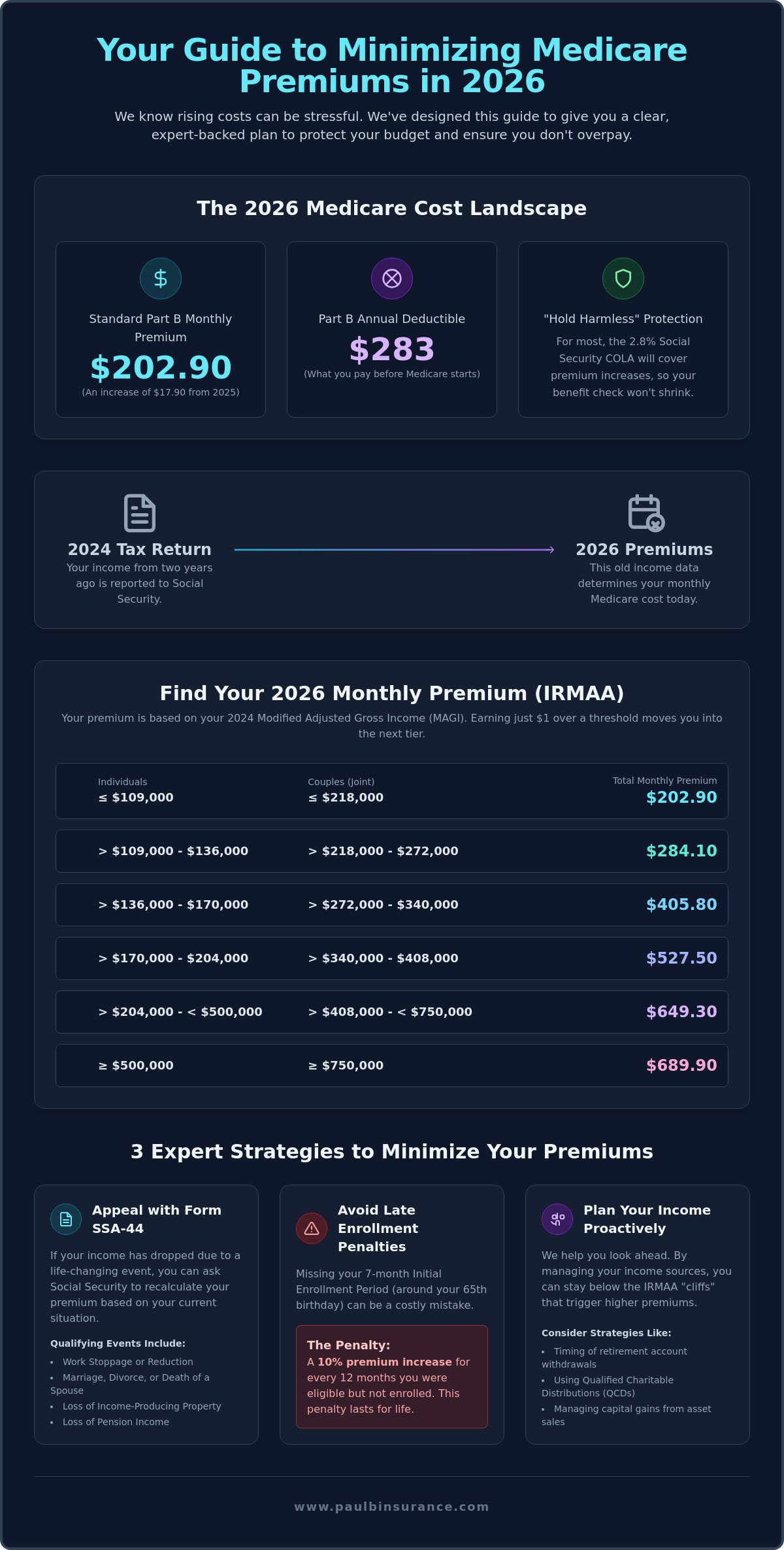

We know that opening your mail to find a higher bill is never a pleasant surprise. For 2026, the standard monthly premium for Medicare Part B is $202.90. This is an increase of $17.90 from the 2025 rate. This monthly cost covers essential services like your doctor visits, outpatient care, and medical supplies. You might wonder why this number keeps climbing every year. It’s largely due to rising healthcare inflation and the ongoing effort to ensure the Medicare trust fund remains solvent for future generations.

We want to help you understand these changes so you can learn how to minimize medicare part b premiums and protect your retirement budget. One piece of good news is the “Hold Harmless” provision. This rule is designed to protect your Social Security check. If the increase in your Part B premium is larger than your Social Security cost-of-living adjustment (COLA), the government limits the premium hike. For 2026, the expected 2.8% COLA should cover the premium increase for most recipients, meaning your take-home benefit won’t actually shrink.

Standard Premiums vs. IRMAA Surcharges

About 95% of people on Medicare pay the standard base rate we mentioned above. However, if your income is higher, you may be subject to the Income-Related Monthly Adjustment Amount, or IRMAA. This is an extra charge added to your base premium. These costs are typically deducted automatically from your Social Security benefits. If you don’t receive Social Security yet, you’ll get a bill for these amounts. Understanding these tiers is the first step in discovering how to minimize medicare part b premiums through proactive planning.

The High Cost of Waiting: Late Enrollment Penalties

One of the most expensive mistakes we see is missing the signup deadline. Your Initial Enrollment Period is the seven-month window that begins three months before you turn 65, includes your birth month, and ends three months after your 65th birthday. If you miss this window and don’t have “creditable coverage” from a current employer, you’ll face a lifetime penalty. This penalty adds an extra 10% to your premium for every 12-month period you were eligible but didn’t sign up. These penalties stay with you for life, making it much harder to keep your costs low.

While we are focusing on premiums here, your total costs also include your annual deductible, which is $283 in 2026. Managing these expenses is a journey, and we are here to guide you. Whether you are looking at a Medigap plan to cover your out-of-pocket costs or exploring a Medicare Advantage plan, we can help you find the right fit for your budget.

Mastering the IRMAA Surcharge: How Your 2024 Income Affects Your 2026 Costs

We understand how frustrating it is to look at your 2026 Medicare bill and see a surcharge based on money you earned two years ago. This is known as the two-year lookback rule. It means the Social Security Administration reviews your 2024 tax return to decide what you pay for Medicare Part B today. This delay often catches people off guard, especially if they have recently retired and their current income is much lower than it was back in 2024.

One of the most stressful parts of this system is the “cliff” effect. In many tax situations, earning a little more money only means you pay a higher rate on that extra dollar. Medicare doesn’t work that way. If you go just one dollar over an income threshold, you are pushed into a higher bracket for your entire premium. This small oversight can cost you thousands of dollars over the year. This is why we recommend reviewing your income brackets every single year with an expert who knows how to minimize medicare part b premiums.

The 2026 IRMAA Income Brackets

Your tax filing status determines which threshold applies to you. For 2026, the surcharges begin once your 2024 income exceeds $109,000 for individuals or $218,000 for married couples filing jointly. We have listed the 2026 tiers below to help you see where you stand.

| Individual Income (2024) | Joint Income (2024) | Part B Surcharge (Monthly) |

|---|---|---|

| $109,000 or less | $218,000 or less | $0 (Standard Premium) |

| $109,001 – $137,000 | $218,001 – $274,000 | +$81.20 |

| $137,001 – $171,000 | $274,001 – $342,000 | +$202.90 |

| $171,001 – $205,000 | $342,001 – $410,000 | +$324.60 |

Why Your MAGI Is Different Than Your AGI

Medicare uses a specific number called Modified Adjusted Gross Income (MAGI) to set your rates. Medicare defines your Modified Adjusted Gross Income as your adjusted gross income plus any tax-exempt interest you earned during the year. Many seniors are surprised by the “tax-exempt interest trap.” Interest from municipal bonds, which is usually tax-free for the IRS, is “added back” when calculating your Medicare costs. If you are worried about these surcharges, we can help you look at your overall coverage. You might find that a Medicare Part D plan with lower costs can help balance out your retirement budget.

5 Practical Strategies to Lower Your Monthly Medicare Costs

Many people feel trapped in the middle-income gap. You might make too much to qualify for state assistance, yet a high monthly premium still hurts your budget. We believe there is always a way to protect your savings. Learning how to minimize medicare part b premiums often comes down to how you manage your income sources before they ever reach your tax return.

One powerful tool for anyone wondering how to minimize medicare part b premiums is the Qualified Charitable Distribution (QCD). If you are over age 70.5, you can send money directly from your IRA to a qualified charity. This money never shows up in your Adjusted Gross Income. Because it stays off your return, it won’t trigger an IRMAA surcharge. Similarly, you must watch your Required Minimum Distributions (RMDs). If you don’t need the full amount to live on, an RMD can easily push you over an income cliff. Planning these withdrawals with an expert ensures you don’t accidentally raise your own healthcare costs.

If you are still working past age 65, your Health Savings Account (HSA) can be a secret weapon. As long as you haven’t signed up for any part of Medicare yet, you can keep contributing to your HSA. These contributions lower your taxable income today. This proactive step is one of the best ways to ensure your future MAGI stays below the surcharge levels.

Income Shifting and Tax-Efficient Withdrawals

We often see clients fall into the Roth Conversion Trap. Converting a traditional IRA to a Roth IRA is a great long-term move, but doing it all at once can be a mistake. A large conversion in 2024 will spike your income and result in much higher 2026 premiums. It is better to spread these conversions over several years to stay under the IRMAA thresholds. Remember that Understanding Medicare Part D is also vital here. IRMAA surcharges don’t just apply to Part B; they also add an extra cost to your prescription drug plan.

Medicare Savings Programs (MSP) for 2026

If your income or assets are more limited, you might qualify for a Medicare Savings Program. These state-run programs, such as the Qualified Medicare Beneficiary (QMB) or the Specified Low-Income Medicare Beneficiary (SLMB) program, are lifelines. In many cases, the state will pay your entire Part B premium for you. This is different from Extra Help, which specifically lowers drug costs. If you are struggling with the $202.90 monthly standard premium, checking your eligibility for these programs is a crucial step. We can help you understand the asset limits in your state so you can find the relief you need.

The Life-Changing Event Appeal: Your Path to Lower Premiums

We know that sinking feeling you get when you see an IRMAA surcharge on your statement. It feels like a penalty for your past success. However, you don’t have to just accept it. If your life has changed since 2024, the Social Security Administration has a process to help you. Learning how to minimize medicare part b premiums through an appeal is one of the most effective ways to protect your retirement budget. We believe you shouldn’t pay a surcharge based on a salary you are no longer earning.

The system uses a two-year lookback, which means your 2026 premiums are based on your 2024 tax return. If you retired in 2025 or early 2026, that 2024 income is no longer a fair reflection of your financial reality. We are here to tell you that you can ask for a “new initial determination.” This process allows the government to look at your current income instead of your old tax return. It is a journey from a state of frustration to one of financial certainty.

What Qualifies as a Life-Changing Event?

The Social Security Administration recognizes eight specific “Life-Changing Events” (LCE) that allow you to appeal your premium. These events include:

- Work Stoppage: You have fully retired.

- Work Reduction: You are working significantly fewer hours.

- Marriage, Divorce, or Annulment: Your filing status has changed.

- Death of a Spouse: This often changes your household income and filing status.

- Loss of Pension Income: A plan was terminated or reorganized.

- Loss of Income-Producing Property: This must be due to a disaster or event beyond your control.

- Employer Settlement: You received a payment due to an employer’s closure or bankruptcy.

To document a work stoppage for the SSA, you need to provide a signed statement from your former employer on company letterhead. This letter should clearly state your final date of employment and confirm that you are no longer receiving a salary. This simple piece of paper is often the most vital evidence you have.

How to File Form SSA-44 Successfully

The key to your appeal is Form SSA-44. This is the official document used to report your life-changing event and provide an estimate of your new, lower income. When you fill out this form, you will need to provide your estimated Modified Adjusted Gross Income (MAGI) for 2026. Gathering your evidence early is essential. Along with your employer letter, you might need a death certificate or divorce decree depending on your situation.

Once you have completed the form, you can mail it or take it to your local Social Security office. We recommend keeping a copy for your records and tracking the delivery. Appeals can take several weeks to process, but don’t lose heart. If your appeal is approved, the SSA will adjust your premium and refund any overpayments made during the year. If you are looking for more ways to save, understanding how a Medigap plan can lower your out-of-pocket costs is another great step in learning how to minimize medicare part b premiums.

If you are feeling overwhelmed by these forms, we are here to help you navigate the process; contact us today for a guide who puts your needs first.

Finding Peace of Mind: How We Help You Manage Medicare Costs

We know that the rising costs of 2026 can feel like a heavy weight on your shoulders. Between the $202.90 standard premium and the $283 deductible, it’s easy to feel like your retirement budget is under attack. We are here to change that. Our mission is to take the confusion out of the system and replace it with a clear, calm path forward. We believe that everyone deserves to feel secure in their healthcare choices.

As an independent broker, we don’t work for the insurance companies. We work for you. We compare options from over 40 different carriers to find the one that actually fits your life and your wallet. This independence is exactly how to minimize medicare part b premiums and other out-of-pocket expenses. We don’t have quotas to fill or specific plans we are forced to sell. We only have a commitment to protect your financial security and provide the unbiased guidance you need.

Our support doesn’t end when you sign up for a plan. We provide year-round assistance to ensure your coverage continues to work for you as your health or income changes. Whether you need help with a life-changing event appeal or you just have a question about a bill, we are your dedicated advocate. We want to make your experience with Medicare simple, clear, and entirely stress-free for 2026 and beyond.

Beyond the Premium: Choosing the Right Overall Plan

Sometimes, the best way how to minimize medicare part b premiums is to look at your coverage as a whole. Some Medicare Advantage Plans offer what is called a “Part B buy-back” or “give-back” benefit. This feature can actually reduce the amount taken out of your Social Security check each month. However, a Medigap plan might be the better choice if you prefer a predictable budget with fewer surprises. We help you weigh the total cost of ownership, including premiums and out-of-pocket maximums, so you can choose with confidence.

Your Next Steps to Savings

We are ready to help you build your 2026 strategy today. To get the most out of our time together, we suggest gathering a few documents for your consultation:

- Your 2024 tax return to check for any potential IRMAA triggers.

- A list of your current medications and dosages.

- Your current Medicare or insurance ID cards.

- Any notices you have received from Social Security or Medicare regarding 2026 rates.

You can book a free, no-obligation review of your strategy at any time. We will sit down with you, listen to your concerns, and map out a plan that prioritizes your peace of mind. Our goal is to ensure you never pay more than you have to for the care you deserve. Let us help you turn this complex journey into a certain path toward a protected retirement.

Take Control of Your 2026 Medicare Journey

Managing your healthcare costs doesn’t have to be a source of stress. We’ve explored how a life-changing event appeal can reverse unfair surcharges and how strategic income timing can keep you out of higher tax brackets. Learning how to minimize medicare part b premiums is a proactive step that gives you more control over your retirement budget. You don’t have to navigate these complex rules alone or settle for limited options that don’t fit your life.

We are dedicated to being your advocate and guide. As independent brokers representing over 40 carriers, we prioritize your needs over company quotas. We are licensed in 34+ states and provide year-round support to ensure you always have a partner in your corner. Our mission is to move you from a state of uncertainty to one of total confidence.

Let us help you find the best Medicare plan for your budget—schedule your free 2026 consultation today. We are ready to help you protect what you’ve worked so hard to build. You deserve a healthcare plan that offers both security and peace of mind.

Frequently Asked Questions

Is the Medicare Part B premium based on gross income or net income?

Medicare premiums are based on your Modified Adjusted Gross Income (MAGI). This number is your adjusted gross income from your tax return plus any tax-exempt interest you earned. It’s not based on your net “take-home” pay or your income after personal expenses. Understanding this distinction is a key part of learning how to minimize medicare part b premiums because it helps you see which income sources trigger higher costs.

What happens if I miss the IRMAA appeal deadline?

You usually have 60 days to file an appeal after receiving your IRMAA notice. If you miss this window, you might lose your chance to lower your 2026 costs unless you have a very good reason for the delay, such as a serious illness. We recommend acting quickly as soon as your notice arrives. If you miss the window this year, you can still plan ahead for next year’s income review to prevent future surcharges.

Can I lower my Part B premium if I am still working at age 66?

You can lower your overall costs if your employer coverage is considered “creditable” by Medicare standards. If you stay on a large employer’s plan, you may not need to enroll in Part B yet, which saves you the monthly cost entirely. If you are already enrolled, the best way how to minimize medicare part b premiums is to manage your taxable withdrawals and salary to stay below the $109,000 individual or $218,000 joint income thresholds.

How much is the Medicare Part B late enrollment penalty in 2026?

The late enrollment penalty is an extra 10% of the standard premium for every 12-month period you waited to sign up. Since the 2026 standard premium is $202.90, a one-year delay adds $20.29 to your bill every single month. This penalty stays with you for as long as you have Medicare coverage. It’s a permanent increase that can significantly eat into your retirement savings over time.

Does a one-time capital gain from a home sale affect my Medicare premium?

A large capital gain can definitely impact your premium if it exceeds certain limits. While the first $250,000 of gain for individuals or $500,000 for couples is excluded from taxes, any profit above those amounts counts toward your MAGI. This one-time spike in your 2024 income could result in a much higher premium for the 2026 calendar year. We can help you look at your 2024 return to see if this applies to you.

What is the “Hold Harmless” provision and does it apply to me?

The Hold Harmless provision ensures your Social Security check doesn’t go down because of a Part B price hike. If the $17.90 increase in 2026 is more than your cost-of-living adjustment, your premium will be lowered to protect your check. This rule applies to most beneficiaries who have their premiums deducted from their benefits. However, it does not protect those who are subject to IRMAA surcharges.

How often does Social Security recalculate my IRMAA surcharge?

Social Security recalculates your premium every single year. They use a rolling two-year lookback to determine your rate. This means they will review your 2024 taxes for your 2026 premium and your 2025 taxes for your 2027 premium. This annual review is why we suggest looking at your income brackets every year with a professional who can help you stay in the lowest possible tier.

Can I get help paying my Part B premium if I only have a small Social Security check?

You can get significant help through state-run Medicare Savings Programs if you meet certain requirements. If your income and assets are below specific limits, programs like QMB or SLMB will pay your entire $202.90 monthly premium for you. This allows you to keep your full Social Security benefit for your daily living expenses. We can help you understand the asset limits in your state so you can find the relief you need.