What if the “best” Medicare coverage isn’t the one with the most benefits, but the one that actually fits your lifestyle here in White Plains? It’s completely normal to feel a bit of anxiety when comparing Medigap Plan N vs Plan G. You want to protect your savings from unexpected medical bills, yet you don’t want to feel like you’re overpaying every month for “just in case” scenarios. It’s a balancing act that can feel overwhelming without a clear guide by your side.

I promise to help you replace that confusion with absolute confidence. In 2026, the choice often comes down to how you feel about small, predictable copays versus a higher fixed premium. We’ll look at the specific differences, including how New York’s unique year-round enrollment rules work in your favor. By the end of this article, you’ll understand exactly how the $283 Part B deductible and potential excess charges impact your wallet. We’re going to map out your out-of-pocket exposure step-by-step, ensuring you find the security and the doctor access you deserve.

Key Takeaways

- Discover how Medigap plans bridge the 20% gap in Original Medicare and why the coverage for each plan letter is identical regardless of which insurance company you choose.

- See why Plan G is the “gold standard” for predictability in 2026, leaving you with nothing to pay for covered services once you meet your annual Part B deductible.

- Compare the costs of Medigap Plan N vs Plan G to see if trading small copays for lower monthly premiums fits your personal budget and health needs.

- Learn the truth about “excess charges” and how New York’s specific laws protect you from being denied coverage or charged more based on your health history.

- Use a simple self-test to identify your “coverage personality,” helping you move from uncertainty to a clear, confident decision about your healthcare future.

Understanding Medigap Basics in 2026

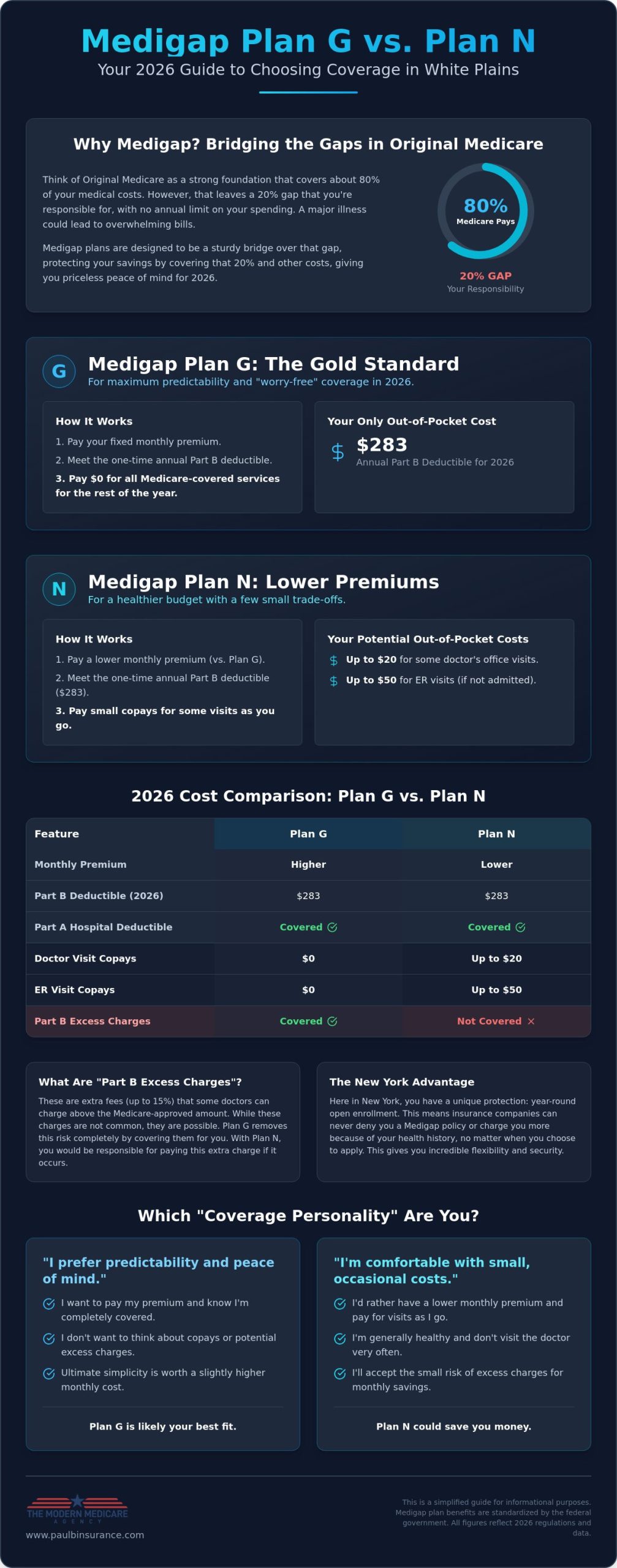

Think of Medigap as a sturdy bridge. Original Medicare is a solid foundation, but it leaves behind significant gaps that can swallow up your retirement savings. Specifically, it usually pays about 80% of your doctor bills. You’re left holding the bill for the remaining 20%. That might not sound like much for a routine checkup, but for a major surgery or a chronic illness, it’s a financial cliff. Understanding Medigap Basics means realizing these plans exist solely to fill those holes and give you back your peace of mind.

Why Original Medicare Isn’t Enough

Without a supplement, your financial risk is essentially unlimited. You’re responsible for the $283 Part B deductible in 2026, and then there’s no “stop-loss” or out-of-pocket maximum on the remaining costs. If you end up with a $10,000 hospital bill, you’d owe $2,000 out of your own pocket. If the bill is $100,000, you’re looking at $20,000. That’s a lot of stress to carry during a health crisis. A Medigap plan steps in and pays those costs for you. It provides a level of financial security that allows you to see any doctor who accepts Medicare without worrying about a surprise bill in the mail.

The Standardization Rule: Same Letters, Different Prices

One of the most reassuring things about Medicare is that the government standardizes the plans. This means a Plan G with one company offers the exact same medical benefits as a Plan G with another company. They’re identical. You aren’t paying for better coverage when you pay a higher premium; you’re often just paying for a brand name or a large marketing budget. Because these benefits are locked in by law, the smart move is to shop for the lowest price. As an independent broker, I compare over 40 carriers to do that shopping for you, ensuring you don’t pay a penny more than necessary for your chosen letter.

In 2026, the conversation for most people in White Plains centers on Medigap Plan N vs Plan G. These two plans have become the clear favorites since Plan F was phased out for new enrollees. They offer the most comprehensive protection available today. We prioritize these two options because they provide the best balance of value and reliable protection. When we sit down to look at your options, we’ll spend most of our time comparing Medigap Plan N vs Plan G to see which one fits your lifestyle and budget best. Choosing between them is the most important decision you’ll make for your healthcare future, and we’re here to make that choice simple and clear.

Medigap Plan G: The Gold Standard for Predictable Costs

If you’re looking for the most “worry-free” experience Medicare has to offer, Plan G is likely where your search ends. It’s designed for people who value predictability above all else. When you’re comparing Medigap Plan N vs Plan G, the primary appeal of Plan G is its simplicity. You pay your monthly premium, and in return, you get a level of coverage that is nearly total. There are no copays at the doctor. There are no surprise bills from the hospital. It’s the closest thing to “first-dollar” coverage available to new enrollees today.

What Plan G Covers in Full

The list of what you don’t have to pay for is impressive. Plan G covers your Part A hospital deductible, which is $1,736 per benefit period in 2026. It also covers your Part B coinsurance and care in a skilled nursing facility. One of the biggest advantages is that it covers “Part B Excess Charges.” These are extra fees some doctors charge above the Medicare-approved amount. While these charges are rare, Plan G removes the risk entirely. You also get foreign travel emergency coverage, which is a wonderful safety net if you plan on visiting family or vacationing outside the country.

The Only Out-of-Pocket Cost: The Part B Deductible

To get to that $0 out-of-pocket state, you only have to clear one small hurdle each year. That’s the Medicare Part B deductible. For 2026, the Centers for Medicare & Medicaid Services has set this amount at $283. You pay this once per year for your outpatient services, like doctor visits or lab tests. Once you’ve paid that first $283, Plan G takes over. For the rest of the calendar year, you won’t pay another dime for Medicare-covered services. It’s a clean, simple system that removes the guesswork from your healthcare budget.

This level of certainty is why so many of our neighbors choose this path. It provides the freedom to see any doctor in the country who accepts Medicare without needing a referral or staying within a network. If you’d like to see how this fits your specific situation, you can explore our Medicare Supplement options to get a clearer picture. While the monthly premiums are generally higher than other plans, the peace of mind you gain is often worth the trade-off. In the ongoing debate of Medigap Plan N vs Plan G, Plan G remains the champion for those who want their medical billing to be as boring and predictable as possible.

Medigap Plan N: Lower Premiums with a Few Small Trade-offs

If Plan G is the “all-inclusive resort” of Medicare, Plan N is the savvy traveler’s choice. It offers the exact same core medical protection but asks you to chip in a tiny bit when you actually use the services. This “middle ground” approach is perfect for many neighbors in White Plains who want to keep their monthly overhead low without sacrificing the quality of their care. When weighing Medigap Plan N vs Plan G, you’ll find that Plan N still gives you the absolute freedom to see any doctor in the country who accepts Medicare. You aren’t restricted by networks; you’re just choosing a different way to pay for your care.

The Three Small Costs of Plan N

There are three specific instances where Plan N requires a bit of cost-sharing. First, you might have a copay of up to $20 for some office visits. It’s important to know this only applies to “chargeable” visits, like seeing a specialist for a new problem, rather than routine preventive care. Second, there is a $50 copay for emergency room visits, though this is waived if you are admitted to the hospital. Finally, Plan N doesn’t cover “Part B Excess Charges.” While that sounds scary, it’s rarely an issue because 96% of doctors nationwide accept Medicare assignment, meaning they agree to Medicare’s set prices. In New York, the risk is even lower due to state-specific protections.

Why Plan N Premiums Are More Stable

Many people find that Plan N premiums stay more consistent over time compared to Plan G. This is largely because the small copays act as a “stabilizer.” When people have a small stake in the cost of their office visits, they tend to use the system more mindfully. This leads to a better “claims experience” for the insurance company, which often results in smaller annual rate increases for you. It’s a smart way to manage your long-term budget while keeping your major medical risks fully covered.

For healthy individuals who only visit the doctor a few times a year, the math often favors Plan N. You save money every single month on your premium, and those savings usually far outweigh the occasional $20 copay. You can learn more about Medigap plan structures to see how these small differences add up over a full year. Deciding between Medigap Plan N vs Plan G doesn’t have to be stressful. It’s simply a matter of deciding whether you’d rather pay a bit more upfront for “zero-copay” peace of mind or keep that extra cash in your pocket each month in exchange for a few small copays at the doctor’s office.

Plan G vs. Plan N: A Side-by-Side Comparison of Costs

Putting these two plans next to each other shows how similar they really are for major health events. In 2026, both plans fully cover your $1,736 Part A hospital deductible. Both plans also require you to pay the first $283 for your outpatient care through the Part B deductible. The real fork in the road for the Medigap Plan N vs Plan G decision is whether you want to pay a higher premium to have $0 copays, or a lower premium with small costs per visit. Both give you the freedom to skip the referrals and see any specialist you choose.

The Math: When Plan N Saves You Money

Choosing a plan often comes down to a simple calculation of your yearly costs. If Plan N saves you $30 a month compared to Plan G, you’ve saved $360 before you even see a doctor. Since the office visit copay is a maximum of $20, you’d have to see a specialist 18 times in a single year to “break even” with the cost of Plan G. For many people in White Plains, that’s a lot of doctor visits. While Plan G is the emotional favorite for its simplicity, Plan N is frequently the winner for those who look strictly at the numbers.

A Note on Part B Excess Charges

The biggest technical difference is how “excess charges” are handled. Plan G covers them, while Plan N does not. These charges occur if a doctor bills more than the Medicare-approved amount. However, the risk is incredibly low. Most doctors nationwide accept Medicare assignment. In New York, we have specific state laws that limit or prohibit these charges entirely, making it a very minor risk for our local clients. You can compare 2026 Medigap rates to see the exact premium difference in your area.

Deciding which one is right for you depends on your comfort level with small bills. Some people find that paying a $20 copay is a small price for the monthly savings. Others find that those small bills are a nuisance they’d rather avoid. We help you look at your past year of medical visits to see which plan would have actually cost you less. It’s about moving from a guess to a data-driven decision that protects your retirement savings.

Making Your Decision: Which Plan Fits Your Lifestyle?

By now, you’ve seen that the choice between Medigap Plan N vs Plan G isn’t about finding a “winner.” It’s about finding the plan that lets you live your life in White Plains without a second thought about your medical bills. Both plans offer incredible security. The decision really comes down to your personal “coverage personality” and how you like to manage your monthly budget. There is no wrong choice here, only the one that makes you feel most protected.

The “Coverage Personality” Test

To help you decide, ask yourself these three simple questions. Your answers will likely point you toward your ideal fit for 2026.

- Do you want to “pay it and forget it”? If you prefer to pay one monthly premium and never deal with a copay or a surprise bill, Plan G is your best match. It offers the ultimate peace of mind.

- Are you healthy and want to keep more money in your pocket? If you don’t mind paying a $20 copay a few times a year in exchange for lower monthly premiums, Plan N is likely the right choice for you.

- Is a $0 premium your top priority? If you are comfortable with doctor networks and referrals in exchange for the lowest possible monthly cost, you might want to consider Medicare Advantage instead of a supplement.

Completing Your 2026 Coverage

Choosing your supplement is a huge step, but it’s only one piece of the puzzle. To have a truly “worry-free” retirement, you need to think about the full picture. First, neither plan covers your prescriptions. You will still need a Part D prescription drug plan to avoid late-enrollment penalties and keep your medication costs predictable. Second, Medigap doesn’t pay for your teeth or your eyes. Adding a supplemental dental plan ensures you aren’t paying out of pocket for cleanings, fillings, or new glasses.

This is where the value of an independent expert becomes clear. We aren’t here to push one carrier or one specific plan letter. Our mission is to protect you by comparing over 40 different carriers to find the exact combination that fits your needs and your budget. You don’t have to do this alone. If you’re still feeling a bit stuck on the Medigap Plan N vs Plan G debate, reach out to us for a personalized comparison. Why working with a Medicare Broker makes this easy is because we take the stress off your shoulders and do the heavy lifting for you. We can show you exactly how each plan would have performed for you over the last year, moving you from uncertainty to absolute certainty.

Secure Your Peace of Mind for 2026

You’ve taken a significant step today toward a more secure future. Choosing between Medigap Plan N vs Plan G is really about deciding how you want to interact with the healthcare system. Whether you prefer the total predictability of Plan G or the savvy monthly savings of Plan N, you’re now equipped to decide with absolute confidence. You understand the math, the protections available in White Plains, and how to complete your coverage with the right drug and dental plans.

Our mission is to make this journey from confusion to certainty as smooth as possible. As independent agents licensed in 34 states and representing over 40 carriers, we have the tools to find your best fit without any high-pressure tactics. We’ll guide you through our methodical process to ensure every gap is filled and your retirement savings are protected. Let us help you find your perfect plan; get a free, unbiased comparison today!

We look forward to being your advocate and ensuring you have the security you deserve in 2026. You’re ready to make a choice that fits your lifestyle perfectly.

Frequently Asked Questions

Can I switch from Plan N to Plan G later if my health changes?

You can definitely switch at any time. New York is unique because of its year-round guaranteed issue rule. This means you don’t have to worry about medical exams or health questions if you decide to change plans later. If your health needs change and you want to move from Plan N to Plan G, the state protects your right to do so whenever you choose.

Do Plan G and Plan N cover prescription drugs?

No, these plans only cover medical costs. To get help with your prescriptions, you’ll need to add a separate Part D plan. We usually set this up for our clients in White Plains at the same time as their supplement. This prevents late enrollment penalties and ensures your medication costs stay predictable throughout 2026.

Is there a “High Deductible” version of Plan G or Plan N?

Only Plan G has a high-deductible version. This option has much lower premiums, but you pay all your medical costs out of pocket until you reach the 2026 limit set by Medicare. Most people we work with prefer the standard versions. They find that the peace of mind of having lower out-of-pocket costs is worth the higher monthly premium.

Will my doctor accept both Plan G and Plan N?

Yes, any doctor who accepts Original Medicare will accept your supplement. When you’re comparing Medigap Plan N vs Plan G, you should know that the insurance carrier doesn’t decide which doctors you can see. There are no networks or gatekeepers. If a provider is in the Medicare system, they’ll take your plan, no matter which company’s name is on your card.

Does Medigap Plan G or N cover dental and vision care?

No, Medigap plans focus on medical gaps like hospital stays and doctor visits. They don’t cover routine cleanings, fillings, or eye exams. To protect your teeth and eyes, we recommend adding a standalone dental and vision plan. This completes your coverage and prevents large, unexpected bills for routine wellness care.

What happens to my Plan G or N if I move to another state?

Your plan is portable and moves with you to any state in the country. Since the benefits are standardized by the government, your coverage stays exactly the same. Your premium might be adjusted based on the cost of living in your new zip code. Keep in mind that you might lose New York’s year-round right to switch plans if your new state has different regulations.

How much will the Part B deductible be in 2026?

The Part B deductible for 2026 is $283. You’ll pay this once per year for outpatient services like doctor visits or lab work. Whether you choose Medigap Plan N vs Plan G, this is the first cost you’ll meet before your supplement starts paying its share. It’s a predictable, annual figure that helps you plan your healthcare budget.

Are Medigap premiums expected to rise in 2026?

Premiums do tend to rise slightly each year as the cost of healthcare goes up. However, Plan N often sees more stable rates than Plan G. The small copays in Plan N help keep the overall claims lower for the insurance company. We monitor these rates for our clients and can help you shop around if your premium ever feels like it’s becoming too high.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com