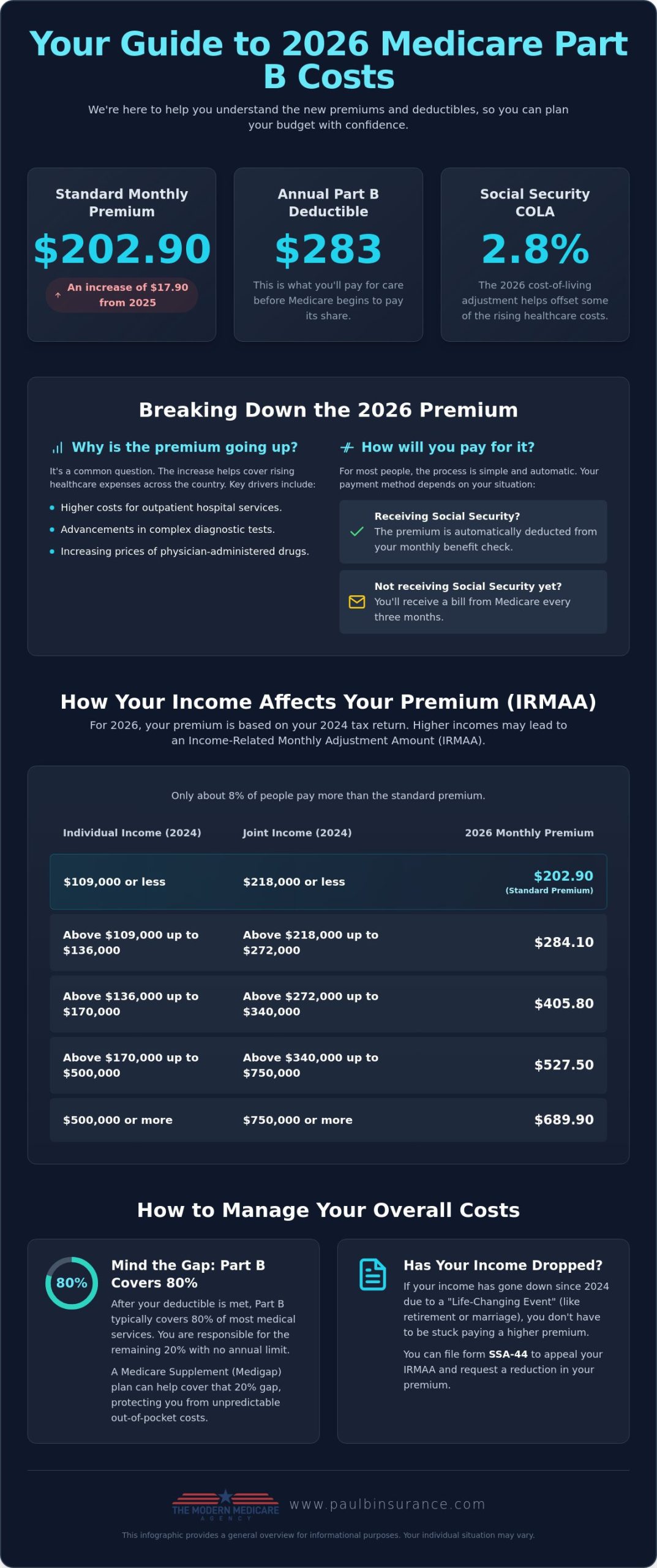

What if your Social Security raise was already spoken for before it even hit your bank account? In 2026, the standard Medicare Part B premium has jumped to $202.90, which is a nearly 10 percent increase from last year. It’s completely normal to feel a bit of sticker shock when you see those numbers, especially when you’re trying to manage a fixed budget during these inflationary times. You deserve to know exactly what is the medicare part b premium in 2026 for your specific situation so you can plan your year with confidence. We understand that seeing your hard-earned benefits shift can feel unsettling, but we’re here to walk you through it as your calm and patient guide.

We’ll clear up the confusion by breaking down the new $283 annual deductible and explaining how the 2.8 percent Social Security cost-of-living adjustment helps offset these higher costs. You’ll also discover if your income level triggers any extra surcharges and how to ensure you aren’t overpaying for your coverage. Our goal is to move you from a state of uncertainty to a place of total financial clarity, giving you the peace of mind you deserve. This guide provides a simple, step-by-step path to understanding your 2026 costs without the stress of complex jargon.

Key Takeaways

- See why the standard monthly cost has risen to $202.90 and how this $17.90 increase affects your monthly budget.

- Learn exactly what is the medicare part b premium in 2026 for your specific income bracket to avoid unexpected surcharges.

- Get clarity on the new $283 annual deductible and what you’ll need to pay before Medicare starts covering its share.

- Calculate whether the 2.8 percent Social Security cost-of-living adjustment is enough to offset your higher healthcare premiums.

- Discover how to protect your savings by comparing supplemental plans across 40 different insurance carriers to find the best value.

The 2026 Medicare Part B Premium: Your Standard Monthly Cost

If you are planning your finances for the year, the most important number to know is $202.90. That is the standard monthly cost for Part B. You might be wondering what is the medicare part b premium in 2026 compared to previous years. It’s a jump of $17.90 from the 2025 rate of $185.00. While a nearly 10 percent increase can feel heavy, knowing the exact figure now allows you to adjust your budget before the new year begins. This rate is set by the federal government, not by private insurance companies, so it remains the same regardless of which state you live in or which doctor you see.

Most people don’t have to worry about writing a check for this amount every month. If you’re already receiving Social Security benefits, the government simply deducts the premium from your monthly check before it reaches your bank account. This automatic process helps ensure you never lose your coverage due to a missed payment. It’s a reliable system, though it does mean your take-home Social Security amount will reflect this new 2026 cost. If you aren’t yet collecting Social Security, you’ll receive a bill called a Medicare Premium Bill every three months.

Why is the Part B Premium Increasing in 2026?

It’s natural to feel frustrated when costs go up. The 2026 increase is largely driven by the rising prices of outpatient hospital services and complex diagnostic tests. Additionally, the cost of physician-administered drugs continues to climb, which puts more pressure on the system. By law, the standard premiums are designed to cover exactly 25 percent of the total estimated costs of the Part B program. As the healthcare system spends more on technology and treatments, the premium must adjust to keep the program stable for everyone who relies on it.

Who Pays the Standard Premium?

The majority of people enrolled in the Medicare program will pay the standard $202.90. This rate applies to individuals with a modified adjusted gross income of $109,000 or less, or married couples filing jointly with $218,000 or less. If you’re enrolling for the first time in 2026, this is the base rate where your journey begins. While this covers your outpatient care, many people choose to pair it with Medicare Supplement (Medigap) plans to help manage the remaining 20 percent of costs that Part B doesn’t cover. Understanding these boundaries helps you see exactly where your money is going and where you might need extra protection.

How Your Income Affects Your 2026 Part B Premium (IRMAA)

While we’ve already covered the standard monthly rate, some people find their bill is higher than the base amount. This extra cost is known as the Income-Related Monthly Adjustment Amount, or IRMAA. If you’re asking what is the medicare part b premium in 2026 for higher earners, the answer depends entirely on your income from two years ago. Social Security looks at your 2024 tax return to decide your 2026 costs. This two-year delay often surprises people, especially those who have recently retired and are now living on a lower budget than they were in 2024.

It’s helpful to remember that most people don’t have to worry about these surcharges. Only about 8 percent of beneficiaries pay more than the standard premium. For the vast majority of retirees, the cost remains at the base level we discussed earlier. However, if you’ve had a successful career or significant investment income, understanding these brackets is the best way to remove the anxiety of a surprise bill. We want you to feel empowered by this information rather than overwhelmed by it.

The 2026 IRMAA Income Brackets

For 2026, the surcharge begins if your 2024 modified adjusted gross income was higher than $109,000 as an individual or $218,000 for a married couple filing jointly. As your income moves into higher tiers, the premium increases in steps. These adjusted premiums range from $284.10 all the way up to $689.90 per month for those in the highest income bracket. Since these costs can also apply to your Medicare Part D plans, the total impact on your monthly budget can be quite significant if you aren’t prepared for it.

What to Do if Your Income Has Changed

If your income has dropped significantly since 2024, you don’t necessarily have to pay the higher rate. The government recognizes that life happens. You can file an appeal using the SSA-44 form if you’ve experienced what they call a “Life-Changing Event.” This process allows you to request a reduction in your premium based on your current, lower income. Common qualifying events include:

- Retiring or reducing your work hours.

- The death of a spouse.

- Marriage, divorce, or annulment.

- Loss of income-producing property or a pension.

Navigating these forms can feel like a heavy burden when you’re already managing a major life transition. You don’t have to do it alone. An independent broker can help you understand the appeal process and ensure you aren’t overpaying for your coverage. If you feel stuck, we can help you review your specific situation to find the most cost-effective path forward for your 2026 budget.

The 2026 Part B Deductible and Out-of-Pocket Costs

While most people focus on what is the medicare part b premium in 2026, the annual deductible is another key number that affects your wallet. For 2026, the Part B deductible is $283. This is an increase of $26 from the 2025 rate. Think of this deductible as your entry fee for the year. You must pay this full amount for your doctor visits or outpatient services before Medicare begins to pay its portion of the bill. Once you’ve met this $283 requirement, Medicare typically steps in to cover 80 percent of your approved medical costs.

The remaining 20 percent is your responsibility, and this is where many people feel the most financial pressure. Unlike many private employer plans you may have had in the past, Original Medicare does not have an “out-of-pocket maximum.” This means there’s no limit to how much you might have to pay in a year if you face a serious illness or a long series of treatments. These gaps in coverage are the primary reason so many retirees choose to enroll in Medicare Supplement Insurance to protect their savings from unpredictable medical debt.

Understanding the 20% Coinsurance

To see how this works in real life, imagine you need a series of diagnostic tests that cost $1,000. If you haven’t been to the doctor yet in 2026, you would first pay your $283 deductible. After that, Medicare covers 80 percent of the remaining $717. You would then be responsible for the other 20 percent, which is about $143. Without a secondary plan, these 20 percent charges can add up quickly. Even if you know exactly what is the medicare part b premium in 2026, failing to account for these potential coinsurance costs can lead to a stressful financial surprise during a health crisis.

How Medigap and Advantage Plans Handle These Costs

You have options to help manage these “leftover” costs. Medigap plans are designed specifically to fill the holes in Original Medicare. Most modern Medigap plans will cover that 20 percent coinsurance for you, though you’ll still pay the $283 deductible out of pocket. On the other hand, Medicare Advantage Plans work differently. They often have their own set co-pays for doctor visits and usually include a maximum limit on what you’ll pay each year.

It’s also important to remember that these Part B costs don’t include your prescriptions. Your medications are handled separately through Medicare Part D. By looking at all these pieces together, you can move from a state of uncertainty to a clear, structured plan for your 2026 healthcare journey.

Will Rising Premiums “Eat Up” Your Social Security COLA?

The 2.8 percent cost-of-living adjustment (COLA) for 2026 was designed to be a breath of fresh air. For the average retiree, this adds about $56 to their monthly Social Security check. However, for many, that extra money feels like it is being spent before they even see it. When you ask what is the medicare part b premium in 2026 going to do to your budget, the $17.90 increase is the main factor. It is a reality that can feel discouraging. We understand that frustration. You work hard to manage your finances, only to have a significant portion of your raise diverted to healthcare costs before it hits your bank account.

You may have heard of the “hold harmless” provision. This rule is a safety net. It is meant to ensure that your Social Security check does not actually decrease from one year to the next due to Medicare premium hikes. Because the COLA is 2.8 percent this year, most people’s checks will grow by more than the $17.90 premium increase. This means the “hold harmless” protection won’t apply to the majority of beneficiaries in 2026. You will likely pay the full $202.90, even if it feels like the government is taking back a large slice of your annual raise. Knowing what is the medicare part b premium in 2026 ahead of time helps you prepare for this shift in your take-home pay.

Calculating Your Net Social Security Increase

Let’s look at the actual math to remove the mystery. If your monthly benefit is $2,000, a 2.8 percent COLA adds exactly $56 to your check. Once you subtract the $17.90 increase for Part B, your actual “net” raise is $38.10. It is still an increase, but it is not as large as the initial headlines might suggest. Understanding this specific number is the best way to avoid stress when your first check of the year arrives in January. For a broader look at how the rules are shifting this year, you can explore our guide on Medicare Changes for 2026.

Managing Your Budget on a Fixed Income

When your fixed income feels tight, it is a perfect time to look at your total household spending. We recommend taking a “total cost” view of your healthcare. Sometimes, you can find significant savings by reviewing other expenses, such as your Dental Insurance, or by checking if there is a more competitive supplemental plan available in your area. We often find that people are paying for benefits they no longer need. An independent review can uncover these hidden savings and help you keep more of your Social Security raise in your own pocket. If you want to make sure your 2026 plan is the most cost-effective option for you, we invite you to reach out for a personal consultation today.

How to Lower Your Overall Medicare Costs in 2026

While the government sets the base price for your outpatient care, you still have the power to decide how much you pay for your total healthcare package. You can’t change the fact that the government has raised the base rate, but you can certainly change your supplemental coverage. Since you now know what is the medicare part b premium in 2026, the next logical step is to look at the other side of your budget. By comparing over 40 different carriers, we often find that clients can switch to a more competitive Medicare Supplement (Medigap) plan that offers the same protection for a lower monthly price.

Another option to consider is moving toward a Medicare Advantage plan. Many of these plans offer $0 monthly premiums. Even though you still pay your Part B premium to the government, having no extra premium for your private coverage can help offset the $17.90 increase we’ve seen this year. It is all about finding the right balance for your specific health needs and your wallet. We want to help you move from a place of feeling squeezed by inflation to a state of total financial clarity.

The Advantage of an Independent Broker

When you start looking for a better deal, you might run into “captive” agents. These are representatives who work for just one insurance company. Because they are restricted, they can only offer you the plans their company sells, even if a better or cheaper option exists elsewhere. An independent broker works for you, not the insurance companies. We have the freedom to shop the entire market to find the best value for your 2026 budget. Having a single, dedicated point of contact for all your Medicare questions removes the stress of dealing with giant call centers. We offer a no-pressure consultation where the only goal is to protect your interests and your savings.

Next Steps for Your 2026 Medicare Planning

To ensure you are prepared for the coming year, there are a few simple actions you can take right now. First, check your latest Social Security statement to see if you have received any notices regarding IRMAA surcharges. Next, take a moment to review your current plan’s Evidence of Coverage. This document will tell you exactly how your specific plan is changing for 2026. If you find that your co-pays or premiums are rising, it is a clear sign that you should explore other options. You deserve to feel certain that you aren’t overpaying for your care. Schedule a simple, stress-free review with Paul Barrett today to secure your path to a worry-free 2026.

Secure Your Financial Peace for 2026

Knowing that the standard premium is $202.90 and the annual deductible has reached $283 is the first step toward taking control of your retirement. While the 2.8 percent Social Security COLA helps, we’ve seen how the $17.90 monthly increase can still impact your household budget. You don’t have to navigate these changes alone or settle for a plan that no longer fits your needs. Now that you have the answer to what is the medicare part b premium in 2026, it’s time to ensure your supplemental coverage is working as hard as it should.

As an independent agency licensed in over 34 states, including New York, Florida, and California, we offer unbiased guidance from more than 40 insurance carriers. You can have direct access to Paul Barrett for personalized Medicare planning that puts your needs first. We are here to remove the anxiety from this process and guide you toward a state of certainty. Get a Free, Simple Medicare Review for 2026 and let us help you protect your hard-earned savings. You’ve done the hard work of educating yourself today, and we’re ready to help you take the final step toward a secure and confident 2026.

Frequently Asked Questions

How much is the Medicare Part B premium for 2026?

The standard monthly premium for Medicare Part B in 2026 is $202.90. This amount is a $17.90 increase from the 2025 rate of $185.00. If you are already receiving Social Security benefits, this cost is typically deducted automatically from your monthly check. Most people will pay this base rate unless their income triggers a higher surcharge.

Is the Medicare Part B deductible going up in 2026?

Yes, the annual Part B deductible is increasing to $283 in 2026. This is a $26 rise from the $257 deductible in 2025. You must pay this full amount for your medical services before Medicare begins to cover its 80 percent share. Understanding what is the medicare part b premium in 2026 and this deductible helps you plan your healthcare budget more accurately.

What is the IRMAA threshold for 2026?

For 2026, the income threshold for the Income-Related Monthly Adjustment Amount (IRMAA) starts at $109,000 for individuals and $218,000 for married couples filing jointly. Social Security uses your 2024 tax returns to determine if you owe these extra surcharges. If your income was above these limits, your monthly premium could range from $284.10 to as high as $689.90.

Can I get help paying my Medicare Part B premium?

There are several state-run programs designed to help those with limited income and resources. Medicare Savings Programs can help pay for your Part B premiums and sometimes even your deductibles and coinsurance. If you are struggling with these rising costs, it’s a good idea to check with your local Medicaid office to see if you qualify for this vital financial support.

How is the Part B premium deducted if I don’t get Social Security?

If you aren’t yet collecting Social Security, you will receive a bill every three months called a Medicare Premium Bill. You can pay this directly through your bank or sign up for Medicare Easy Pay. This service automatically deducts your monthly premium from your bank account, ensuring you never miss a payment and your coverage remains active throughout the year.

What happens if I don’t sign up for Part B when I’m first eligible?

Delaying your enrollment can lead to a permanent late enrollment penalty. For every 12-month period you were eligible but didn’t sign up, your premium increases by 10 percent. This penalty stays with you for as long as you have Part B coverage. Knowing what is the medicare part b premium in 2026 is important, but timing your enrollment correctly is just as crucial for your long term savings.

Does Medicare Advantage include the Part B premium?

No, you must continue to pay your Part B premium to the government even if you join a Medicare Advantage plan. While some Advantage plans may have a $0 monthly premium for their specific benefits, they require you to stay enrolled in Part B. A few plans offer a “Part B Buy-Back” that pays a portion of the premium for you, but these are specific to certain areas and plans.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com