Did you know that New York is one of the only states where your savings account won’t stop you from getting help with your monthly Medicare premiums? It’s 2026, and many of our neighbors feel squeezed by rising drug costs and Part B bills that seem to climb every year. You might feel stuck in a maze of paperwork, wondering if there is a better way to manage your healthcare budget. We understand that stress. We’re here to show you exactly how to lower medicare costs with the right plan in New York by using state-specific programs and smarter enrollment strategies.

You’ll discover how we help seniors secure predictable out-of-pocket maximums and find out if you qualify for a program that pays your Part B premium for you. We’ll walk you through the latest 2026 strategies that protect your retirement savings while ensuring you have the high-quality care you deserve. From leveraging EPIC benefits to understanding New York’s unique Medigap flexibility, we’ve got the clear, simple answers you need to move from confusion to confidence.

Key Takeaways

- Learn why New York’s lack of a resource test means your home or car won’t stop you from getting state help with your Part B premiums.

- Discover how to lower medicare costs with the right plan in New York by taking advantage of our state’s unique continuous open enrollment rules.

- See how a simple audit of your 2026 Part D medications can prevent unexpected hits to your wallet at the pharmacy counter.

- Understand the clear difference between independent brokers and captive agents when it comes to finding the lowest prices across 40 different carriers.

- Find out how to secure predictable out-of-pocket costs so you can stop worrying about surprise medical bills and focus on enjoying your retirement.

Understanding Medicare Costs in New York for 2026

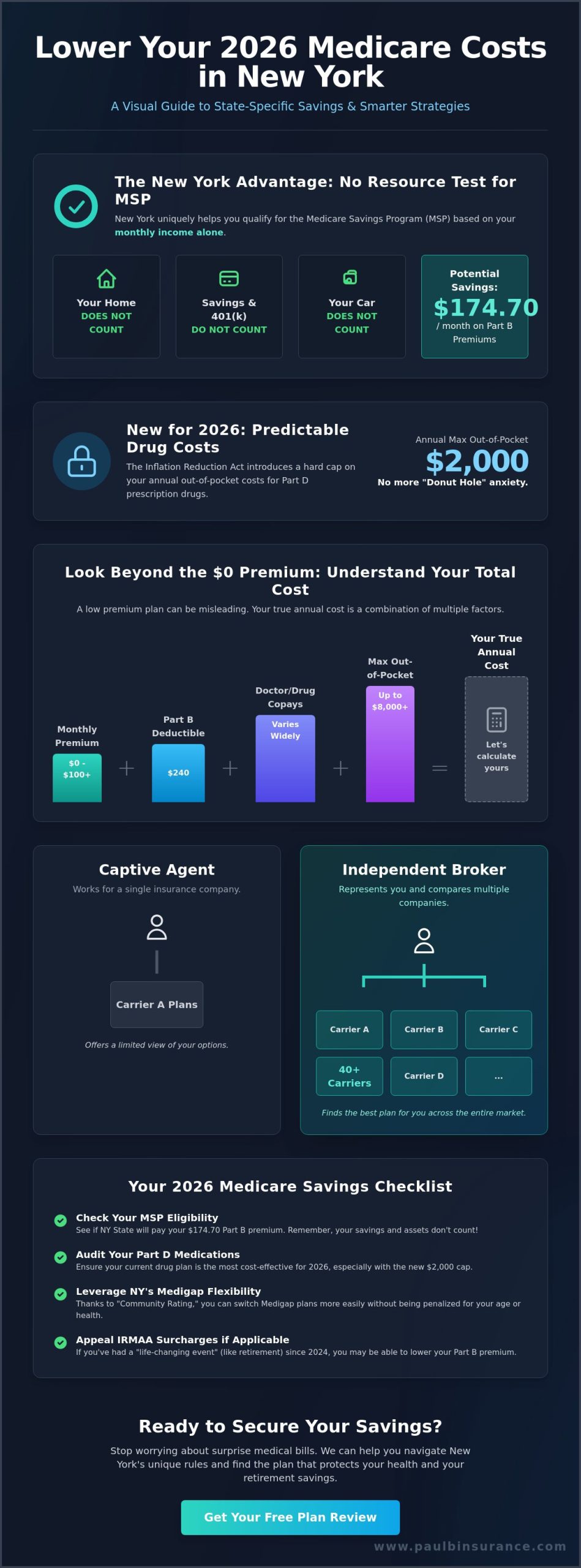

Living in New York brings a certain sense of pride, but it also comes with a higher price tag for nearly everything. Medicare is no different. We often meet seniors who feel overwhelmed because they focus only on the monthly premium they see on their billing statement. This is a common trap. To truly master how to lower medicare costs with the right plan in New York, we must look at the “Total Cost of Ownership.” This approach means we account for premiums, the $240 Part B deductible, copays, and the maximum out-of-pocket limits that protect your savings if you face a serious illness.

We believe in looking at the big picture. A plan with a $0 premium might look attractive on paper, but if the copays for your specific specialists are high, you could end up paying more by December than you would with a higher-premium plan. By analyzing your specific healthcare habits, we can move you from a state of financial stress to a place of total clarity. Understanding Medicare Costs is the first step toward reclaiming control over your retirement budget.

The 2026 Part B Premium and IRMAA

Your Part B premium for 2026 is not actually based on what you earn today. Instead, Social Security looks at your tax return from two years ago, which in this case is 2024. For most of our neighbors, the standard monthly premium is $174.70. However, if your 2024 income exceeded certain thresholds, you may be hit with an Income Related Monthly Adjustment Amount, or IRMAA. These surcharges can catch you off guard, especially if you recently retired and your income has dropped significantly since 2024. We help our clients identify these “life-changing events” so they can appeal these surcharges and keep more money in their pockets.

New York Cost Trends for Supplemental Coverage

New York is one of only four states that requires “community rating” for Medigap plans. This means insurance companies cannot charge you more just because you are older or have a health condition. While this makes monthly premiums in New York higher than in some other states, it provides a level of protection and flexibility you won’t find elsewhere. You can switch plans more easily here without being “locked in” due to your health history.

On the pharmacy side, 2026 marks a major milestone for your wallet. Thanks to the Inflation Reduction Act, your total out-of-pocket spending for Medicare Part D prescription drugs is now capped at exactly $2,000 for the entire year. This change eliminates the old “donut hole” anxiety and makes your medication costs much more predictable. When we compare Medicare Advantage plans against Medigap, we factor in these new caps to ensure your choice remains cost-effective for the long haul.

New York Medicare Savings Programs: Help Without a Resource Test

One of the biggest financial reliefs available to New Yorkers is the Medicare Savings Program (MSP). This is a state-run lifeline that can significantly reduce your monthly expenses by having the state pay your Part B premium. For many, this puts $174.70 back into their Social Security check every single month. We see so much unnecessary stress because people assume they won’t qualify for help. They think they have too much in savings or that their home will count against them. In most states, that might be true, but New York is different.

We call this the “New York Advantage.” Unlike many other parts of the country, New York does not use a resource test for its Medicare Savings Programs. This means your savings accounts, your 401(k), your home, and your car do not disqualify you from receiving help. We focus on your monthly income alone. Finding how to lower medicare costs with the right plan in New York often starts with this single, powerful program that many middle-income residents overlook. If you’re unsure where to start, we can help you review your eligibility during a quiet, no-pressure conversation.

Qualifying for the MSP in 2026

As we move through 2026, the income limits for these programs have adjusted to keep pace with the cost of living. There are two primary levels we look at for our clients. The first is the Qualified Medicare Beneficiary (QMB) program, which provides the most comprehensive help by covering premiums, deductibles, and coinsurance. The second is the Qualifying Individual (QI) program, which specifically pays for your Part B premium. Even if you feel your income is a bit too high, it’s worth checking the 2026 limits through your Local Department of Social Services (LDSS). Many New Yorkers find they qualify for the QI level even with a comfortable retirement income.

The Extra Help Program for Prescriptions

The benefits of the MSP don’t stop at your Part B premium. When you are enrolled in an MSP in New York, you are automatically enrolled in the federal “Extra Help” program. This is a game-changer for your Medicare Part D costs. Extra Help lowers your drug plan premiums and reduces your pharmacy copays to just a few dollars for most prescriptions. New York eliminated the asset test for MSPs to simplify eligibility. This connection between state and federal aid ensures that your total healthcare costs remain predictable and manageable throughout the year. We simplify this jargon so you can see exactly how these programs work together to protect your retirement savings.

Medicare Advantage vs. Medigap: Choosing the Cost-Effective Path

Choosing between Medicare Advantage and Medigap is often the most stressful part of the process for our clients. We see the confusion every day. Do you take the plan with the $0 monthly premium, or do you pay more upfront for total peace of mind? To understand how to lower medicare costs with the right plan in New York, you have to look past the monthly bill and focus on your potential medical usage. We believe in finding a balance that protects your health and your bank account.

New York seniors have a secret weapon that most of the country doesn’t. Our state requires continuous open enrollment. This means you can switch from one plan to another at any time of the year without answering a single health question. We use this “NY Rule” to help our clients adjust their coverage as their health needs change. You aren’t “locked in” to a plan just because you developed a health condition. This flexibility is a massive cost-saving strategy because it allows us to move you to a more protective plan exactly when you need it most.

Is a $0 Premium Plan Actually Cheaper?

A $0 premium Medicare Advantage plan sounds like a dream, but it’s really a “pay-as-you-go” system. For a healthy New Yorker who only sees a doctor for annual checkups, these plans can be incredibly cost-effective. However, specialist copays in New York City often range from $40 to $50 per visit in 2026. If you require frequent diagnostic tests or physical therapy, those small costs add up quickly. You also have to consider the Maximum Out-of-Pocket (MOOP) limit. In 2026, if your copays hit that ceiling, the plan pays 100% of your covered costs, but you must have the savings ready to reach that limit first. For a deeper dive into how these networks function, our Medicare Advantage Guide offers a clear breakdown.

The Medigap Advantage in New York

If you live with a chronic condition, a Medigap Plan G or Plan N often provides a better long-term return on your investment. While the monthly premium is higher than an Advantage plan, the out-of-pocket costs at the doctor’s office are virtually eliminated. We often find that the “Total Cost of Ownership” for Medigap is lower for those who see multiple specialists each month. You also avoid the “Prior Authorization” hurdles that can sometimes delay your care in an Advantage plan. Because New York law protects your right to switch plans, we can help you start with a lower-cost option and move to a Medigap plan later if your health situation changes, giving you total confidence in your financial future.

5 Steps to Lowering Your Medicare Expenses With the Right Plan

Reducing your monthly healthcare bill shouldn’t feel like a part-time job. We’ve simplified the process into five logical steps to help you move from confusion to confidence. If you’re wondering how to lower medicare costs with the right plan in New York, these actions are your roadmap to real savings in 2026. We are here to protect your retirement and ensure you never feel rushed or pressured into a decision.

- Step 1: Audit your medications. Check your current prescriptions against the latest Part D formulary changes. Plans often move drugs between “tiers,” which can change your copay from $10 to $50 overnight.

- Step 2: Check state assistance. Re-evaluate your eligibility for the New York Medicare Savings Program or EPIC annually. Since New York has no asset test for MSPs, your savings won’t disqualify you.

- Step 3: Verify your doctors. Medical groups in the Hudson Valley and Long Island frequently shift networks. Ensure your preferred specialists are still “in-network” for 2026 to avoid out-of-network penalties.

- Step 4: Review “extra” benefits. Look for plans that include dental, vision, or hearing coverage to prevent paying full price for these essential services.

- Step 5: Use an independent broker. A captive agent only shows you one company. We look at 40+ carriers to find the lowest price for your specific zip code.

We want you to feel empowered by these choices. If you want a clear, unbiased look at your 2026 options, you can schedule a call with us to start your personalized savings plan.

The Annual Plan Audit

Every year from October 15 through December 7, the Annual Enrollment Period gives you the chance to reset your costs. We recommend a full “check-up” of your coverage during this window. Use the 2026 Medicare Plan Finder tool to input your specific drugs and pharmacy. This tool is the most accurate way to see your total projected spending for the coming year. Several major New York provider groups have updated their plan affiliations for 2026, so a doctor who was covered last year might not be covered now. We simplify this jargon so you know exactly which plans your doctors accept.

Bundling and Ancillary Savings

Many New Yorkers focus so much on the medical side that they forget about the high cost of teeth and eyes. Adding a standalone dental or vision plan can actually lower your total annual spending by preventing high out-of-pocket bills for crowns or new lenses. In 2026, many Medicare Advantage plans also offer “Flex Cards.” These cards provide a set dollar amount for over-the-counter items like aspirin or vitamins, which keeps more money in your wallet. You should verify your “Notice of Change” letter every September to spot price hikes before they happen.

How an Independent Broker Simplifies Your Savings in New York

We know the “crazy maze” of the Medicare system is exhausting. You’ve learned about the 2026 Part D caps and the lack of a resource test for New York assistance programs. But how do you actually apply this to your life? This is where the choice of an agent makes all the difference. A “captive agent” works for a single insurance company. Their job is to sell you that specific brand, whether it’s truly the best fit for your budget or not. We take the opposite path as an independent broker.

We access 40+ carriers to find the lowest price for your specific zip code. This unbiased approach is a key part of how to lower medicare costs with the right plan in New York. We aren’t here to push a product; we are here to be your advocate from start to finish. Our relationship doesn’t end when you sign your enrollment form. We provide year-round support to help you resolve medical bills or claims issues that might pop up during the year. We are never rushed, never pressured, and always here to help.

Unbiased Guidance at No Cost to You

Many people ask how our services are free. It’s simple. We are compensated by the insurance companies, but those payments are standardized. This means our only goal is to find the plan that serves you best. As a local Melville-based agency, we live and work in the same New York medical landscape you do. We know which local hospital systems are currently in-network and which pharmacy chains offer the best rates for 2026. For a deeper look at what to look for in an advisor, you can read our Medicare Broker guide to build trust in your choice.

Ready for Peace of Mind?

We believe you deserve to feel empowered, not overwhelmed. During your first 15-minute consultation, we listen to your needs, review your current costs, and identify where you might be overpaying. Our simple 5-step process is designed to move you “From Confusion to Confidence” with total clarity. We handle the paperwork and the follow-ups so you don’t have to deal with the stress. If you’re ready to secure a more predictable financial future, you can Schedule a Call With Paul today. We are ready to help you discover how to lower medicare costs with the right plan in New York while protecting your peace of mind.

Take Control of Your 2026 Healthcare Budget

You deserve to enjoy your retirement without the constant worry of rising medical bills. We’ve explored how New York’s unique lack of a resource test for state assistance and the new $2,000 cap on prescription drugs can provide immediate relief to your wallet. Knowing how to lower medicare costs with the right plan in New York is about more than just picking a name you recognize; it’s about matching your unique health needs to the specific benefits available in our state. We believe that with the right guidance, you can stop overpaying for coverage you don’t use.

We are here to help you move from confusion to confidence. Our team of NY-based experts understands our local hospital networks and has access to over 40 insurance carriers to find your perfect fit. You’ll never feel rushed or pressured when you speak with us. We take the time to ensure you understand every detail so you can make a choice that protects your savings for years to come. Ready for a clearer path forward? Get Your Free 2026 Medicare Cost Audit Today. We’ll help you find the peace of mind you’ve been looking for.

Frequently Asked Questions

What is the income limit for the Medicare Savings Program in NY for 2026?

The income limits for 2026 have increased to reflect the current cost of living. For the Qualifying Individual (QI) program, which pays your full Part B premium, the monthly limit is approximately $2,420 for individuals and $3,280 for couples. Because New York does not have a resource test, your savings, 401(k), or home won’t disqualify you from this help. We can help you verify your exact eligibility based on your current 2026 Social Security statement.

Can I switch from Medicare Advantage to Medigap in New York at any time?

Yes, New York is one of the only states that offers continuous open enrollment for Medigap plans all year long. You can switch from a Medicare Advantage plan to a Medigap plan at any time without answering health questions or undergoing a medical exam. This “guaranteed issue” right is a powerful tool for seniors whose health needs change unexpectedly. It ensures you are never stuck in a plan that no longer fits your medical situation.

Does New York have a resource or asset test for Medicare assistance?

New York does not have a resource or asset test for its Medicare Savings Programs. This means the state only looks at your monthly income to determine if you qualify for help with your premiums and costs. Your house, car, and retirement accounts are completely exempt from the calculation. This unique policy makes it much easier for middle-income New Yorkers to access financial help compared to seniors living in almost any other state.

How much can I save on Part D drugs with the 2026 Inflation Reduction Act changes?

You can save thousands of dollars thanks to the $2,000 annual out-of-pocket cap on prescription drugs that is fully in effect for 2026. Before this change, seniors often faced unlimited costs if they had expensive specialty medications. Now, once you hit that $2,000 limit at the pharmacy counter, your plan pays 100% of your covered drug costs for the rest of the year. This cap is a major factor in how to lower medicare costs with the right plan in New York.

What is the “Extra Help” program and how do I apply in NY?

The Extra Help program is a federal benefit that significantly lowers your prescription drug premiums and pharmacy copays. In New York, if you qualify for a Medicare Savings Program, you are automatically enrolled in Extra Help without a separate application. If you don’t qualify for an MSP but still have limited income, you can apply directly through the Social Security Administration. We simplify this process by checking your eligibility for both programs during our initial consultation.

Are there $0 premium Medicare plans available in Long Island and NYC?

Yes, there are many $0 premium Medicare Advantage plans available throughout Long Island and the five boroughs of NYC in 2026. These plans are very common in high-population areas where insurance companies compete heavily for your enrollment. While the premium is $0, we always help you look at the specialist copays and doctor networks to ensure the plan is actually your most cost-effective choice. Sometimes a plan with a small premium offers better long-term savings on your specific medications.

What happens if I miss the Medicare enrollment deadline in New York?

If you miss your enrollment deadline, you may face lifetime late enrollment penalties that increase your monthly premiums for Part B and Part D. You might also have to wait until the General Enrollment Period to sign up, which could leave you without any health coverage for several months. However, if you recently moved or lost employer-sponsored insurance, you may qualify for a Special Enrollment Period. We help you identify these windows to avoid costly mistakes and late fees.

How does an independent broker help me lower costs compared to calling an insurance company directly?

An independent broker works for you, while an insurance company agent only represents one corporation. We compare over 40 different carriers to find the lowest price and best doctor network for your specific zip code. Calling a company directly limits your options to only their specific products. Using our unbiased guidance ensures you see the entire 2026 market, helping you discover how to lower medicare costs with the right plan in New York without any added fees or pressure.