What if you could test-drive a new health plan for a full year without any risk of losing your original coverage? For many seniors in 2026, the fear of making an irreversible mistake keeps them stuck in plans that might not be the best fit. We know how overwhelming it feels to stare at a $202.90 Part B premium and wonder if you’re getting the most value for your money. You shouldn’t have to worry about being denied for a pre-existing condition just because you wanted to try something new. Having the medicare advantage trial right period explained simply is your key to moving from confusion to confidence.

We agree that the insurance system often feels like a maze designed to trap you, but this “Medicare mulligan” gives you a guaranteed 12-month safety net. We promise to show you exactly how to test a Medicare Advantage plan with the peace of mind that you can return to Original Medicare and your Medigap policy whenever you choose. We’ll walk you through the critical deadlines and the simple steps to protect your health and your wallet during this transition.

Key Takeaways

- Learn how to use the 12-month “Medicare Mulligan” to test-drive an Advantage plan without the stress of being locked into a plan that doesn’t fit your needs.

- See the medicare advantage trial right period explained for the two specific scenarios where you can safely return to your original coverage.

- Discover how “Guaranteed Issue Rights” protect you from medical questions or higher premiums if you decide to switch back to a Medigap policy.

- Understand the critical 2026 deadlines and why we always recommend waiting for a new approval before canceling your current coverage.

- Find out how an independent expert can help you compare options across dozens of carriers to ensure you never lose your preferred doctors or benefits.

Understanding the Medicare Advantage Trial Right Period

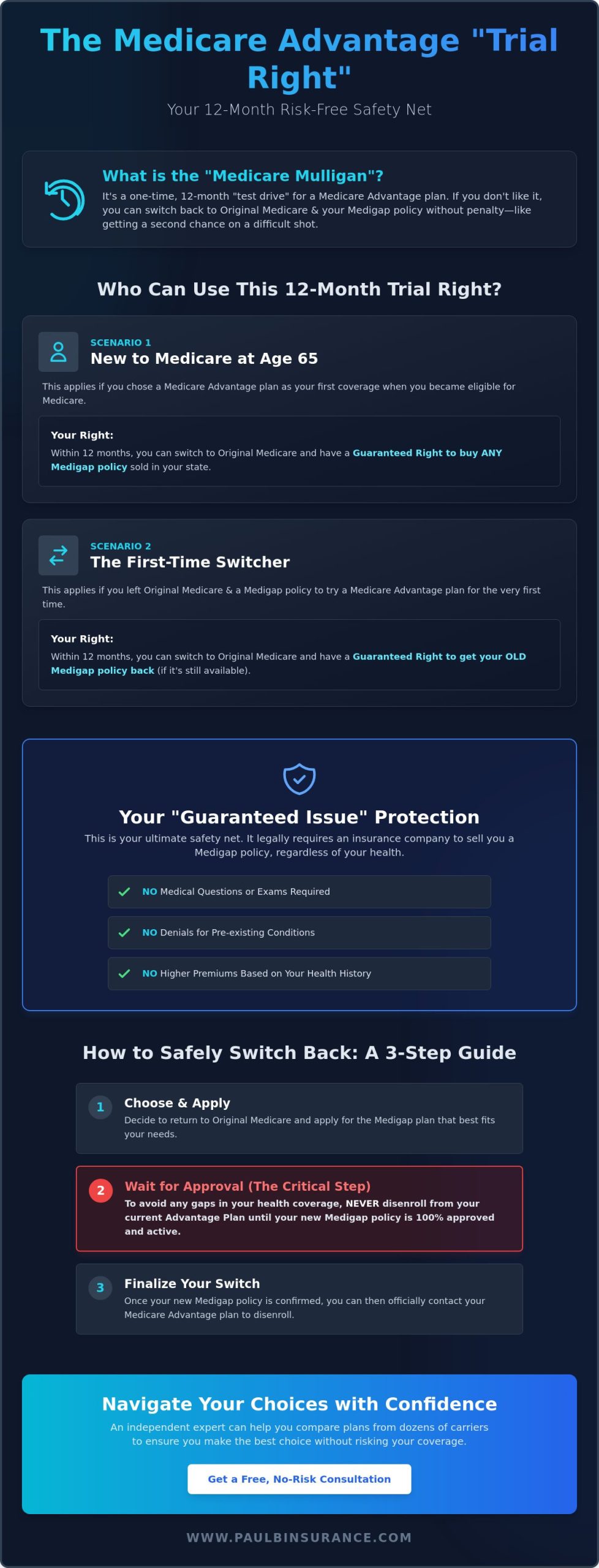

We believe no one should feel trapped in a health plan that doesn’t meet their needs. That is why the federal government created a special protection called the trial right. Think of it as a 12-month test-drive for your healthcare. Having the medicare advantage trial right period explained simply is the first step toward making a confident choice in 2026. While the standard Annual Enrollment Period happens every autumn for everyone, this trial right is personal to you. It starts the moment your new plan begins and gives you a full year to see if the network of doctors and the costs actually work for your life.

We often call this the “Medicare Mulligan.” In golf, a mulligan is a second chance to hit a shot without a penalty. This protection works the same way. The core benefit is simple. If you decide the plan isn’t for you, you have a guaranteed path back to Original Medicare. You won’t just be returning to the basic program; you will also have the right to buy a Medigap policy to cover those gaps like the $1,736 Part A deductible. This protection is vital. It removes the medical exam hurdle that usually blocks people from switching back later in life.

What exactly is a “Trial Right”?

A trial right is essentially a “Guaranteed Issue” right. In the insurance world, this means a company cannot look at your medical history or ask about your health conditions. They must sell you a policy at the best available rate. This is the ultimate safety net for seniors who worry that a chronic condition might leave them uninsurable if they leave their Medigap plan. We are here to help you track these specific 12-month deadlines. We want to ensure you never lose this protection because of a calendar mistake.

Why Medicare provides this safety net

Medicare created this rule to ensure you have real choices. As you can read about the history of Medicare Advantage on Wikipedia, these private plans were designed to offer more options. However, the government realized that seniors might be hesitant to try something new if the decision was permanent. By offering this safety net, they encourage competition among carriers. This gives you the emotional relief of knowing your choice isn’t forever. If your plan’s drug formulary changes or your favorite specialist leaves the network during that first year, you have the power to walk away. You can return to the stability of Original Medicare without any penalty or stress.

The Two Specific Situations Where Trial Rights Apply

We want you to feel completely secure in your choices, but it’s important to know that this protection isn’t a blanket rule for everyone at all times. The law is very specific about who can use this safety net. Essentially, the 12-month clock starts ticking the very first day your new coverage begins. Because this is often a once-per-lifetime “mulligan,” we want to make sure you have the medicare advantage trial right period explained so you don’t accidentally waste your opportunity. There are two primary groups of people who qualify for these protections in 2026.

Scenario 1: New to Medicare at Age 65

If you just turned 65 and chose a Medicare Advantage plan right out of the gate, you are in a great position. Medicare gives you a full year to decide if that private plan actually fits your lifestyle. If you find that the network is too restrictive or the co-pays are adding up faster than you expected, you can switch back to Original Medicare. In this scenario, you have a “Guaranteed Issue” right to buy any Medigap policy available in your state. Whether you want the comprehensive coverage of Plan G or the lower premiums of Plan N, the insurance company cannot turn you down. You can learn more about these initial steps in our guide to Medicare Eligibility: A Clear and Simple Guide for 2026.

Scenario 2: The First-Time Switcher

This second situation applies to those who have been on Original Medicare for a while. Perhaps you had a Medigap policy for years but decided to try a Medicare Advantage plan for the very first time in 2026. If you find yourself missing the freedom to see any doctor who accepts Medicare, you can use your trial right to return to your previous coverage. The rule here is a bit more specific. You have the right to get your old Medigap policy back from the same company if they still sell it. If that specific plan is no longer offered, you can choose from several other standard plans.

As this Medicare Advantage Trial Period Explained resource notes, the timing is everything. You must apply for your new Medigap policy no later than 63 days after your Advantage plan coverage ends. We suggest starting this process much earlier. If you’re unsure which scenario fits your situation, you can review our full guide to see where you stand. Understanding these nuances is the best way to move from confusion to confidence. For a deeper dive into how these supplement plans work, take a look at What Is Medicare Supplement Insurance? A Simple Guide to Medigap.

Guaranteed Issue Rights: Your Ticket Back to Medigap

We want you to have the medicare advantage trial right period explained in a way that highlights your strongest protection. The “Guaranteed Issue” right is essentially your legal golden ticket. It ensures that if you decide to leave your Advantage plan within that first 12-month window, insurance companies cannot treat you differently because of your health. In the maze of the insurance system, this is one of the few times the power is entirely in your hands. We simplify the jargon so you know exactly how it works, ensuring you don’t feel pressured by carriers or confused by fine print.

In 2026, we focus on the three “No’s” of Guaranteed Issue to give you peace of mind. First, there are no health questions. You don’t have to disclose a recent diagnosis, a chronic condition, or a planned surgery. Second, there are no waiting periods. Your new coverage starts the moment your old plan ends. Third, there are no higher premiums. You won’t be charged a penny more just because you’ve had health struggles in the past. Our team works with over 40 different carriers to help you navigate these options. We do the heavy lifting to find the right replacement so you can steer clear of costly enrollment mistakes and late penalties.

What “Guaranteed Issue” means for your premiums

This protection is your shield against “medical underwriting.” Normally, if you try to buy a Medigap policy after your initial enrollment window, companies scrutinize your entire medical history. They might deny you coverage or charge a fortune for a pre-existing condition. Guaranteed Issue rules force them to give you the same “standard” rate as a perfectly healthy person your age. It prevents the “lock-in” effect where seniors stay in a plan that doesn’t fit their needs just because they’re afraid they can’t pass a physical. We believe you should always have the freedom to choose the best care for your body.

Which Medigap plans can you actually get?

The specific plans available to you often depend on your “Trial Right” scenario. In 2026, most of our clients choose between Plan G and Plan N. Plan G remains a top choice because it covers almost everything once you pay the $283 Part B deductible. Plan N is a fantastic alternative for those who want lower monthly premiums and don’t mind small co-pays at the doctor. If you were eligible for Medicare before January 1, 2020, you might still have the right to get Plan F. You can explore the specific benefits of each on our Medigap page. Understanding the Medicare Advantage trial period is the best way to keep these doors open and protect your financial future.

Trial Rights vs. Open Enrollment: Clearing the Confusion

We often see seniors wait until January to make a change, thinking they must follow the standard calendar. This is a common mistake that can lead to unnecessary stress and missed opportunities. While the Medicare Advantage Open Enrollment Period (OEP) is a fixed window from January 1 to March 31, it’s very different from your trial rights. Having the medicare advantage trial right period explained clearly means understanding that you don’t have to wait for an “official” season to protect your health. Your trial right is a personal, rolling 12-month window that starts the day your new coverage begins.

The biggest danger we want to help you avoid is the “OEP Trap.” During the standard Open Enrollment window, anyone in an Advantage plan can switch to a different one or return to Original Medicare. However, doing this during OEP does not usually give you a “Guaranteed Issue” right for Medigap. If you leave your plan in February using OEP rules but you don’t qualify for a trial right, you might find yourself on Original Medicare without any supplemental coverage. In 2026, this means you would be responsible for the full $283 Part B deductible and 20% of all medical costs out of your own pocket. We believe you deserve better than that kind of financial risk.

Key differences in timing and rules

This table helps you see at a glance why the trial right is your superior safety net. We want you to move from confusion to confidence by knowing which window you are actually using.

| Feature | MA Open Enrollment (OEP) | Trial Right Period |

|---|---|---|

| Dates | January 1 – March 31 | Personal 12-month window |

| Medigap Access | No Guaranteed Issue | Full Guaranteed Issue Rights |

| Eligibility | Anyone currently in an MA plan | Specific first-time scenarios |

Why the Trial Right is more powerful

The trial right is more powerful because it allows you to “undo” a switch even in the middle of summer. You aren’t tethered to the spring calendar. Furthermore, when you use this right, you also get a special window to enroll in a standalone Part D prescription drug plan. This ensures your medications stay covered without any late enrollment penalties. If you’re currently exploring these options, we suggest reviewing our Medicare Advantage Plans: A Simple Guide for 2026 to see how these plans compare.

We are here to help you navigate these dates so you never feel rushed or pressured. If you are unhappy with your current plan, don’t wait for the next enrollment season to see if you qualify for a switch. You can schedule a call with us today to review your specific start date and protect your right to return to Original Medicare.

How to Safely Switch Back to Original Medicare in 2026

We want to make sure your transition is seamless and stress-free. The single most important piece of advice we can give you is our Golden Rule: Never cancel your current Medicare Advantage plan until you have a written approval for your new Medigap policy. If you cancel your coverage too early, you could find yourself in a dangerous gap without any protection. Having the medicare advantage trial right period explained is only the first step. Executing the switch safely is how we truly protect your health and your savings in 2026.

Our process follows three simple steps to move you from confusion to confidence. First, we review your current Medigap options to see which carriers offer the best rates for Plan G or Plan N in your area. Second, we submit your “Guaranteed Issue” application. We include specific proof of your trial right so the insurance company knows they cannot ask health questions or deny your coverage. Third, we coordinate your prescription drug plan. With the 2026 Part D out-of-pocket cap set at $2,100, it’s vital to ensure your new drug plan is active the moment your old plan ends. We manage these moving parts so you don’t have to.

The step-by-step disenrollment process

Timing is everything when you’re returning to Original Medicare. We help you coordinate with Medicare and Social Security to ensure all paperwork is filed correctly. The goal is to have your “Effective Dates” line up perfectly. If your Advantage plan ends at midnight on the last day of the month, your Medigap and Medicare Part D coverage must begin at 12:01 AM the very next day. Even a 24-hour gap could leave you responsible for the $1,736 Part A hospital deductible out of your own pocket. We double-check every date to prevent these costly enrollment mistakes.

How an independent broker protects your “Mulligan”

You might feel tempted to call your current insurance company directly to cancel, but this is often a mistake. Their representatives are often captive agents whose job is to keep you enrolled in their specific products. They might not explain your trial rights fully or could lead you toward a plan that benefits the company more than it benefits you. We act as your personal advocate and educator. We are never rushed and never pressured. Our “Schedule a Call With Paul” process is designed to take you from a state of overwhelm to total clarity in just 15 minutes. We stay by your side until your new Medigap card is in your hand, ensuring your 2026 “Medicare Mulligan” is handled with the care you deserve.

Secure Your Health Future with Confidence

You now have the medicare advantage trial right period explained and understand how this 12-month safety net protects your choices in 2026. You know that you can test a new plan without the fear of being locked out of Medigap or facing higher premiums due to your health history. Whether you are new to Medicare at age 65 or trying an Advantage plan for the first time, your right to return to Original Medicare is a powerful tool for your financial and physical well-being. This “Medicare Mulligan” ensures that your first year of coverage is a time of exploration, not a source of anxiety.

We don’t want you to feel overwhelmed by the deadlines or the complex paperwork. As an independent broker with access to over 40 carriers, we use a methodical 5-step process to move you from confusion to confidence. We provide year-round support across 34 states to ensure your coverage always fits your life perfectly. Don’t navigate the Medicare maze alone; schedule a call with Paul today to protect your trial rights! We are here to serve as your dedicated advocate, ensuring you are never rushed and never pressured. You deserve the peace of mind that comes with a clear, simple roadmap for your healthcare.

Frequently Asked Questions

What happens if I miss the 12-month trial right deadline?

If you miss the 12-month deadline, you lose your “Guaranteed Issue” protection. This means that after the 365th day, any Medigap company can ask you health questions and potentially deny you coverage or charge higher premiums based on your medical history. We want to help you avoid this risk by tracking your specific dates so you don’t lose the safety of the medicare advantage trial right period explained in this guide.

Can I use the trial right if I switch from one Medicare Advantage plan to another?

No, you cannot use the trial right if you are simply moving from one Advantage plan to another. This protection is specifically reserved for your very first time enrolling in a Medicare Advantage plan. If you have already been in an Advantage plan for more than a year, the “mulligan” window has closed, and you won’t have a guaranteed path back to Medigap without medical underwriting.

Do I need to undergo a physical exam to get my Medigap plan back?

You do not need a physical exam or any medical underwriting when you exercise your trial right. The law requires insurance companies to accept your application regardless of your health status. This is the core benefit of the medicare advantage trial right period explained above. It ensures that seniors with chronic conditions aren’t trapped in a plan that doesn’t meet their needs.

What happens to my prescription drug coverage if I use my trial right?

Your prescription drug coverage will transition to a standalone Part D plan when you switch back to Original Medicare. Because most Advantage plans include drug coverage, leaving the plan triggers a Special Enrollment Period. This allows you to pick a new drug plan that fits your 2026 medications, ensuring you stay under the $2,100 out-of-pocket cap for the year.

Can an insurance company charge me more for Medigap when using a trial right?

No, an insurance company cannot charge you a higher premium because of your health when you use a trial right. They must offer you the same “standard” rate they give to a healthy person of your same age. We work with 40 plus carriers to ensure you get the best possible price without any “sick person” penalties or hidden fees.

Is the Medicare Advantage trial period the same as the Free Look period?

The trial right is not the same as a “Free Look” period. A Free Look period is a short 30-day window typically used for Medigap policies to let you change your mind. The Medicare Advantage trial right is much more robust, giving you a full 12 months to test your coverage before you lose the right to return to your previous setup.

What if the Medigap company I used to have is no longer in business?

If your previous Medigap carrier is no longer in business, you still have protected rights. You won’t be left without options. In this situation, you are allowed to buy a standard Medigap policy from a different insurance company. We help you compare the top-rated carriers in 2026 to find a stable replacement that offers the same level of security.

Can I use a trial right if I moved to a different state during the 12 months?

You can still use your trial right if you move to a different state during your first 12 months in an Advantage plan. Moving actually gives you a separate Special Enrollment Period to change your coverage. We provide support across 34 states, so we can help you coordinate your move and ensure your “Guaranteed Issue” rights follow you to your new home.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com