What if the most stressful part of your 30-year teaching career isn’t the final exams or the grading, but the three-month window before you hand in your keys? We know you’ve spent decades caring for our community’s children, and now that your 2026 retirement date is approaching, you deserve a transition that feels like a reward, not a second job. It’s completely normal to feel overwhelmed by the crazy maze of moving from EMHP or NYSHIP to a federal system that seems to speak a different language.

Our goal is to make medicare planning for retiring teachers in Suffolk County NY as simple as a lesson plan you’ve taught a thousand times. We’re here to help you protect your hard-earned pension from unexpected IRMAA surcharges and ensure your spouse stays covered without a single day of worry. This guide provides a clear timeline for your transition, explains how Part B reimbursement works for local educators, and helps you confirm your favorite Suffolk County doctors are still in your network so you can move from confusion to confidence.

Key Takeaways

- Understand how Medicare becomes your primary insurer in 2026 and why this shift is the foundation of your retirement security as a Suffolk County educator.

- We simplify medicare planning for retiring teachers in Suffolk County NY by highlighting the critical three-month enrollment window you must meet to avoid costly lifelong penalties.

- Learn the essential steps to coordinate the Empire Plan as your secondary coverage so you can avoid “Double Coverage” mistakes that could disrupt your benefits.

- Discover how to verify that your trusted Long Island specialists at Stony Brook or Northwell Health will still see you once you transition to Medicare.

- Follow our simple 5-step roadmap to move from confusion to confidence, ensuring you have a clear and stress-free plan for your 2026 retirement.

Understanding the Shift: Why Medicare Planning Matters for Suffolk Teachers

You have spent decades shaping the future of our community in school districts like Patchogue-Medford, Half Hollow Hills, and Three Village. Your dedication to your students is unmatched, but as you approach your 2026 retirement date, the focus must shift toward your own future. Transitioning from a district-provided health plan to federal coverage is a major milestone. We know this change often feels like moving from a safe harbor into a vast, choppy ocean. Proper medicare planning for retiring teachers in Suffolk County NY ensures you don’t lose the security you worked so hard to build.

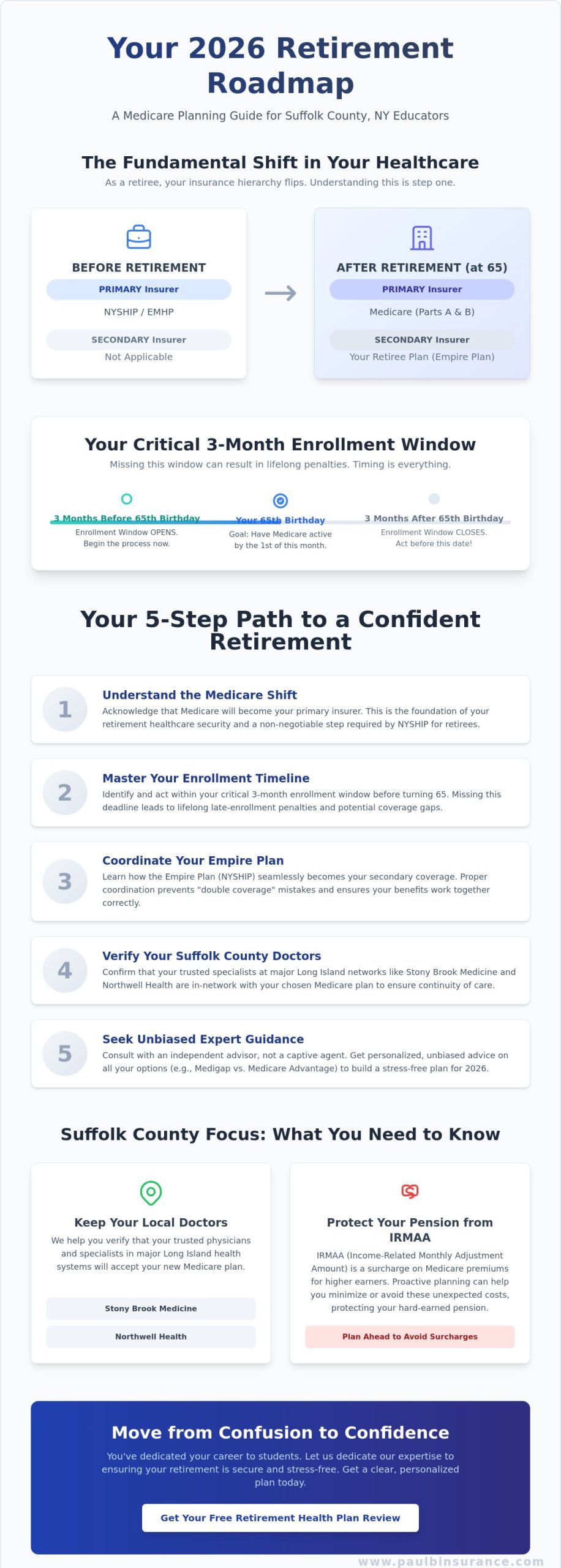

Once you retire and reach age 65, Medicare (United States) becomes your primary insurer. This means the federal government pays your medical claims first, and your retiree coverage typically pays second. A common myth among Long Island educators is that this transition happens automatically. In reality, you must take active steps to enroll in Medicare Part A and Part B to avoid lifelong late-enrollment penalties. The “automatic” safety net doesn’t exist for most teachers, especially those who aren’t yet drawing Social Security benefits.

The emotional weight of this shift is significant. For thirty years, your HR department managed the paperwork and chose your options. Now, you are the CEO of your own health management. This shift from district-led care to personal responsibility causes stress for 85 percent of the retirees we meet. We are here to act as your guide, moving you from a state of confusion to a place of total confidence. We simplify the jargon so you know exactly how your coverage works in 2026.

NYSHIP vs. EMHP: Identifying Your Starting Point

Most Suffolk County teachers start their journey with either the Empire Plan (NYSHIP) or the Employee Medical Health Plan (EMHP) of Suffolk County. Your specific district contract determines how these plans interact with Medicare. In 2026, these rules remain strict. If you miss your enrollment window, your district plan might refuse to pay claims that Medicare should have covered. We review your specific union contract to ensure your timing is perfect and your benefits remain seamless.

The Role of an Independent Advisor in 2026

We believe in education over sales. Unlike a “captive agent” who only represents one insurance company, our independent brokerage looks at the entire market for you. This distinction is vital because it gives you more options and unbiased advice. We help you choose between a Medigap plan or a Medicare Advantage plan based on your specific doctors and budget. Our goal is to help you navigate the federal and state rules without any pressure. We provide the clarity you need to make an informed decision for your retirement years.

The Essentials: Medicare Parts A & B for New York Retirees

Medicare can feel like a complex puzzle when you’re first looking at it. We are here to help you piece it together so you can focus on enjoying your hard-earned retirement. For most 2026 retirees, your journey begins with Original Medicare, which consists of Part A and Part B. Think of Part A as your hospital insurance. It covers inpatient stays, skilled nursing facility care, and some home health services. Part B is your medical insurance. It handles your doctor visits, outpatient care, medical supplies, and preventive services. Together, they form the foundation of your healthcare coverage.

If you’re turning 65 in 2026, timing is everything. The three months leading up to your 65th birthday are the most critical. This is when you should finalize your medicare planning for retiring teachers in Suffolk County NY to ensure there are no gaps in your coverage. Waiting until the last minute often leads to unnecessary stress and potential delays in receiving your benefits. We want to help you avoid that pressure entirely.

For members of the New York State Health Insurance Program (NYSHIP), the rules are very specific. You’re required to enroll in both Medicare Part A and Part B as soon as you become eligible for Medicare primary coverage. This typically happens when you turn 65 and retire. Understanding how NYSHIP and Medicare coordination works is vital because your Empire Plan or HMO coverage will change once Medicare becomes your primary payer. If you don’t enroll in Part B, you could find yourself facing massive out-of-pocket costs because your NYSHIP plan will not pay for services that Medicare would have covered.

The Initial Enrollment Period (IEP) for 2026 retirees is a seven-month window that begins three months before your 65th birthday month, includes your birth month, and extends for three months after your birthday month.

Avoiding the Part B Late Enrollment Penalty

Missing your enrollment window isn’t just a paperwork headache; it’s expensive. If you don’t sign up for Part B when you’re first eligible, you may have to pay a 10% penalty for every 12-month period that you could have had Part B but didn’t. This penalty stays with you for the rest of your life. However, if you’re still teaching past age 65 and have coverage through your current employer, you may qualify for a Special Enrollment Period (SEP). This allows you to sign up later without a penalty. We always recommend starting your paperwork 90 days in advance. This gives the Social Security Administration plenty of time to process your application and ensures your “Medicare red, white, and blue card” arrives before your first day of retirement.

The Truth About Part B Reimbursement

There is good news for many educators in our local area. A significant number of school districts in Suffolk County reimburse their retirees for the standard Medicare Part B premium. This effectively keeps more money in your pocket every month. To get this benefit, you usually need to submit proof of your Medicare enrollment to your former district’s HR or benefits office. The process varies slightly between districts like Sachem, Middle Country, or Bay Shore, so it’s a good idea to check your specific contract details. If you’re feeling a bit overwhelmed by the forms, you can connect with our team to help simplify the transition from your district plan to Medicare. We’ll make sure you have the right documents ready for your HR department so your reimbursement starts on time.

Coordinating the Empire Plan and NYSHIP with Medicare

For many of our neighbors in the Long Island school districts, the Empire Plan has been a reliable shield for decades. As you approach age 65, the most significant shift in your medicare planning for retiring teachers in Suffolk County NY involves understanding that Medicare now takes the lead. The Empire Plan does not disappear. Instead, it moves into a secondary position. It acts as a safety net that catches many of the costs Medicare leaves behind. We help you visualize this as a partnership where Medicare pays first, and your NYSHIP coverage fills the gaps.

We often see teachers tempted by aggressive mailers or TV commercials for private Medicare Advantage plans. You must be extremely careful here. Enrolling in a non-NYSHIP Medicare Advantage plan can trigger an automatic disenrollment from your Empire Plan coverage. This is a “Double Coverage” trap that can jeopardize your hard earned retiree benefits. We want to keep your union-negotiated perks intact. You aren’t losing your union benefits by joining Medicare; you are simply evolving how they are delivered. We make sure you stay on the right path so your transition is seamless and your coverage remains robust.

The “Medicare Primary” Transition

Once you turn 65, Medicare becomes your primary insurance payer. This means Medicare pays its share of your medical bills first, and then the Empire Plan “wraps around” those remaining costs. In many cases, teachers find their out of pocket expenses actually decrease after this transition. Your deductibles and co-pays often look different because the Empire Plan is designed to supplement Medicare’s gaps. If you want to see how this compares to other private supplement choices, you can read our guide to Medicare Supplement (Medigap) options.

Protecting Your Prescription Drug Coverage

In 2026, the landscape for prescriptions has changed significantly due to the $2,000 annual out-of-pocket cap on Part D costs. Your Empire Plan Medicare Rx (Part D) program is specifically built to integrate with these new federal limits. We prioritize verifying your specific medications against the 2026 formulary updates. This ensures your local Suffolk County pharmacy remains in-network and your maintenance medications are covered at the lowest possible tier. To learn more about how these drug plans function, visit our page understanding Medicare Part D drug plans.

- Keep Your Benefits: Retiring from a Suffolk County school district does not mean giving up your union-negotiated health security.

- Avoid Mistakes: Signing up for a private “all-in-one” plan outside of NYSHIP can lead to a permanent loss of your Empire Plan secondary coverage.

- Peace of Mind: We coordinate the paperwork so your transition to Medicare Primary is handled with zero interruptions in care.

Our goal is to move you from confusion to confidence. We handle the technical details of medicare planning for retiring teachers in Suffolk County NY so you can focus on enjoying your retirement. We simplify the jargon and provide a clear, step-by-step roadmap for your specific district’s requirements.

Suffolk County Specifics: Local Doctors and IRMAA

Medicare planning for retiring teachers in Suffolk County NY requires a local perspective. You’ve spent years building relationships with specialists at Stony Brook Medicine or Northwell Health. We understand how vital it’s to keep those connections. Moving to a plan that doesn’t include Catholic Health or your favorite local specialist can feel like a step backward. We make sure your network stays intact. Local care means you don’t have to drive into the city for quality treatment. We look at every doctor on your list to ensure they still see you once you hang up the chalk.

IRMAA is an extra charge for higher-income earners based on tax returns from two years prior. This surcharge often catches Long Island educators off guard. Your pension and social security might put you over the limit. We guide you through the math so there are no surprises on your first Medicare bill. Our goal is to move you from confusion to confidence by explaining exactly how these costs impact your monthly budget.

IRMAA for Teachers: Will Your Pension Trigger Extra Costs?

In 2026, the government uses your 2024 tax returns to decide if you pay more for Medicare. For individuals earning over $106,000 or couples over $212,000, these surcharges add up quickly. We sit down with you to review those 2024 numbers. If your income dropped because you retired, we don’t just accept the higher price. We help you file an appeal using Form SSA-44. Retirement is a “Life-Changing Event” in the eyes of Social Security. This simple step can save you hundreds of dollars each month.

Dental and Vision: The “Missing” Pieces

Many teachers are surprised to find that Original Medicare doesn’t cover their teeth or eyes. Even some robust retiree plans leave these out. We see the stress when a routine cleaning turns into a big bill. You deserve to keep your smile healthy without draining your savings. We suggest exploring dental insurance plans for retirees to fill these specific gaps. Having a separate policy for dental and vision provides the peace of mind that your basic health needs are fully met.

Ready to clear the fog and protect your retirement income? Schedule a Call With Paul to get your personalized Medicare roadmap today.

Your 5-Step Retirement Roadmap: Moving from Confusion to Confidence

Transitioning from a career in the classroom to a peaceful retirement shouldn’t feel like a final exam you didn’t study for. We understand that the transition is often filled with more questions than answers. Our goal is to replace that uncertainty with a clear, logical path forward. Here is your 2026 roadmap for medicare planning for retiring teachers in Suffolk County NY.

- Step 1: Contact Social Security 3 to 4 months before your 65th birthday. Even if you plan to keep working or delay your pension, you need to initiate the Medicare enrollment process early. This window allows enough time to process your application and ensures your red, white, and blue card arrives before your current coverage ends.

- Step 2: Confirm your district’s specific requirements for Part B reimbursement. Districts across Long Island, from Patchogue-Medford to Huntington, have different protocols. Some require you to submit proof of your Part B premium annually to receive your reimbursement. Don’t leave this money on the table; check with your benefits administrator by March 2026.

- Step 3: Review your current Empire Plan or EMHP summary of benefits. These plans change every year. We’ll help you look at the 2026 “coordination of benefits” section to see exactly how your district coverage pays after Medicare takes the lead.

- Step 4: Audit your prescription drugs and preferred doctors for 2026. The $2,000 out-of-pocket cap for prescriptions is now fully active this year. We need to verify that your specific medications are still on the preferred formulary and that your local Suffolk specialists still participate in your chosen network.

- Step 5: Meet with an independent broker to verify your coordination of benefits. We look at the “big picture” to ensure there are no gaps between your district plan and Medicare.

The “Schedule a Call With Paul” Advantage

We provide a completely no-pressure environment for educators. You’ve spent your life being evaluated; you don’t need a high-pressure sales pitch now. We take the time to compare 40+ carriers. This ensures that if you choose a Medigap plan or a secondary option, it’s the most cost-effective choice for your specific needs. Our support continues long after you sign up. We stay by your side year-round to handle billing questions or network changes.

Take the First Step Toward a Stress-Free Retirement

Professional medicare planning for retiring teachers in Suffolk County NY brings a level of peace that you simply can’t get from a generic brochure. We remove the anxiety of the “crazy maze” and replace it with a simple, written plan. You deserve to enter this new chapter with total confidence. Start by downloading our 2026 Medicare Checklist to keep your documents organized. When you’re ready for a patient, expert guide to lead the way, Schedule a Call With Paul.

Take Control of Your Retirement Journey Today

You’ve dedicated your career to the students of Long Island, and now it’s time to focus on your own well-earned transition. Navigating the 2026 Medicare landscape doesn’t have to feel like a second job. We’ve explored how to seamlessly coordinate your NYSHIP or Empire Plan benefits with Medicare Part A and B. We also simplified the local nuances of Suffolk County healthcare networks and how to manage IRMAA impacts on your pension. Comprehensive medicare planning for retiring teachers in Suffolk County NY is about more than just picking a plan; it’s about protecting your peace of mind. We’ve spent over 15 years helping Long Island seniors find clarity in this complex system. With access to 40 plus insurance carriers, we ensure you won’t face costly enrollment penalties or confusing gaps in coverage. We provide no-cost, no-obligation consultations to clear up the jargon and build your personal roadmap. You don’t have to figure this out alone. We’re ready to help you move from a state of uncertainty to total confidence.

Schedule a Call With Paul to simplify your teacher retirement Medicare plan

We look forward to helping you secure the retirement you deserve. You’ve earned it, and we’re here to protect it.

Frequently Asked Questions

Do I have to sign up for Medicare if I am still teaching in Suffolk County at age 65?

No, you don’t need to enroll in Medicare Part B if you’re still actively teaching and covered by your school district’s group health plan. Since Suffolk County districts employ more than 20 people, your employer insurance remains your primary coverage. You can safely delay Part B without any late enrollment penalties until you decide to retire. We usually suggest signing up for Part A at 65 since it costs nothing for most teachers, but we’ll check your specific situation first.

How does the Empire Plan work with Medicare Part B?

The Empire Plan becomes your secondary insurance provider once you retire and your Medicare benefits begin. Medicare pays your medical bills first, and the Empire Plan picks up the remaining costs according to your specific plan rules. This transition is a vital step in medicare planning for retiring teachers in Suffolk County NY. You must have both Part A and Part B active to ensure your NYSHIP benefits continue to protect you without any gaps in coverage.

What is the IRMAA surcharge, and does it apply to NYS teachers?

IRMAA is an extra charge added to your Medicare premiums if your income exceeds certain levels set by the government. For the 2026 plan year, Social Security looks at your 2024 tax returns to determine if you owe this surcharge. Many retired teachers in New York hit these thresholds because of their pensions and retirement account withdrawals. We help you file the Social Security Form SSA-44 if your income dropped after retirement so you can potentially lower these costs.

Can I keep my Long Island doctors if I switch to a Medicare-primary plan?

Yes, you can keep your current doctors as long as they participate in the Medicare program. Most major medical groups in Suffolk County, including those at Stony Brook Medicine and Northwell Health, accept Medicare patients. If you stay with the Empire Plan as your secondary coverage, you’ll still have access to their wide network of providers. We’ll personally verify your favorite doctors during our meeting to give you total peace of mind before you make the switch.

What happens to my spouse’s health coverage when I transition to Medicare?

Your spouse can typically stay on your school district’s health plan even after you move over to Medicare. If your spouse is under 65, they’ll remain on the active teacher plan or the retiree version of the Empire Plan. Once they reach age 65, they’ll follow the same path you took by enrolling in Medicare Part A and Part B. We’ll create a clear timeline for both of you so that nobody loses their coverage during this important transition period.

Why do I keep getting mail about Medicare Advantage plans if I already have NYSHIP?

You’re getting that mail because private insurance companies buy lists of people turning 65 to market their own products. These plans are heavily advertised on television and in your mailbox, but they often don’t work well with your existing NYSHIP benefits. For most Suffolk County teachers, joining a private Advantage plan could cause you to lose your district’s secondary coverage permanently. We help you filter through the noise so you can focus on the benefits you’ve actually earned.

How do I get reimbursed for my Part B premiums by my school district?

You get reimbursed by submitting proof of your Medicare Part B payments to your school district’s business office. Most districts in Suffolk County require a copy of your annual Social Security benefit statement or a monthly billing notice. Since the standard Part B premium is a set amount in 2026, your district will typically refund this cost to you on a quarterly or annual basis. We recommend keeping a simple folder for these documents to make the reimbursement process quick and easy.

Is it better to have a Medicare Supplement or stay with the Empire Plan?

Staying with the Empire Plan is usually the best financial move because your school district likely pays a large portion of the premium. Comprehensive medicare planning for retiring teachers in Suffolk County NY involves comparing these costs against private options. While a private Supplement plan offers great coverage, the Empire Plan was specifically built to coordinate with Medicare for New York educators. We’ll sit down and run the actual numbers for you to confirm which path keeps more money in your pocket.