Staring at a list of Medicare options can feel like trying to solve a puzzle in another language. Plan F, Plan G, Plan N… it’s an alphabet soup of choices that can make selecting the right medicare supplement plans feel overwhelming. The fear of making a costly mistake is very real, especially when you’re trying to secure your financial health against unexpected medical bills that Original Medicare simply won’t cover. This confusion can leave you feeling stuck, worried that one wrong move could lead to years of financial stress.

This guide is here to change that. We believe that understanding your healthcare options shouldn’t be a source of anxiety. Our promise is to provide trusted, straightforward guidance that demystifies Medigap once and for all. We’ll walk you through how these plans work, what each one covers, and how to confidently compare the most popular options. By the end, you will move from confusion to confidence, equipped with the clarity needed to choose the perfect plan for your needs and achieve lasting peace of mind.

Key Takeaways

- Understand how Medigap works with Original Medicare to cover out-of-pocket costs like deductibles and coinsurance.

- Learn the fundamental differences between Medigap and Medicare Advantage to decide which path is right for your healthcare needs.

- Discover the most popular medicare supplement plans, like Plan G and Plan N, to see how they can provide predictable healthcare costs.

- Pinpoint your personal Medigap Open Enrollment Period-the one-time window to enroll with guaranteed acceptance, regardless of your health.

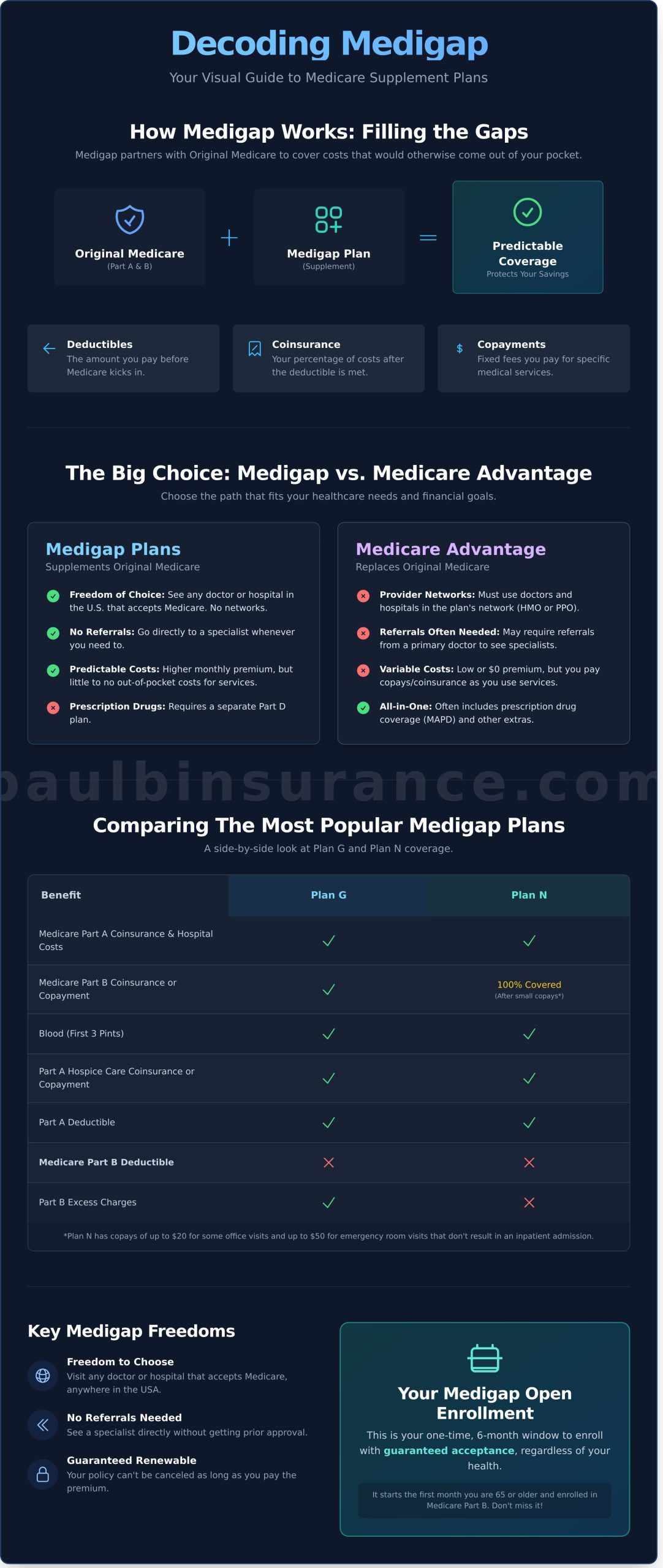

What is a Medicare Supplement (Medigap) Plan?

Navigating your healthcare options can feel overwhelming, but understanding Medicare Supplement plans doesn’t have to be. The simplest way to think of a Medigap plan is as gap insurance for your health. It isn’t a replacement for your Original Medicare (Part A and Part B); instead, it works with it to provide you with greater financial predictability and peace of mind.

Original Medicare is a fantastic foundation, but it was never designed to cover 100% of your medical costs. It leaves behind “gaps” that you are responsible for paying out-of-pocket. These gaps include costs like:

- Deductibles: The amount you must pay before Medicare starts paying.

- Coinsurance: A percentage of the cost for a service after your deductible is met.

- Copayments: A fixed amount you pay for a covered service.

These plans are sold by private insurance companies but are standardized by the federal government. This standardization, which is well-documented by neutral sources like Wikipedia’s guide to Medigap (Medicare Supplement Insurance), is a key feature that simplifies your choice. It means that a Plan G from one company must offer the exact same core benefits as a Plan G from another. The only differences are the monthly premium and the company’s customer service reputation.

How Medigap Protects Your Savings

Imagine a hospital stay without a Medigap plan. You would be responsible for the substantial Medicare Part A deductible, and if your stay is lengthy, you’d also face daily coinsurance costs. These unexpected bills can quickly add up. With one of the comprehensive medicare supplement plans, like Plan G, those costs are covered. You simply pay your predictable monthly premium, protecting your savings from surprise medical expenses.

Key Features of All Medigap Plans

Beyond filling cost gaps, Medigap policies offer powerful freedoms and protections that many people value. Key features include:

- Freedom to Choose: You can see any doctor or visit any hospital in the U.S. that accepts Original Medicare.

- No Referrals Needed: You don’t need a referral from a primary care physician to see a specialist.

- Guaranteed Renewable: Your policy cannot be canceled as long as you pay your premiums on time.

- Important Note: Medigap plans sold today do not include prescription drug coverage. You will need a separate Medicare Part D plan for your prescriptions.

Medigap vs. Medicare Advantage: The Most Important Choice

When you first become eligible for Medicare, you face a fundamental choice that will shape your healthcare for years to come. This is the big fork in the road: should you enhance Original Medicare with one of the many medicare supplement plans, or replace it entirely with a Medicare Advantage plan? Understanding this difference is the first step toward making a confident decision. One path offers unparalleled freedom and predictable costs, while the other provides an all-in-one, low-premium alternative.

Comparing Costs and Coverage

The financial structure of these two options is fundamentally different. With a Medigap plan, you pay a higher, fixed monthly premium to a private insurer. In exchange, the plan pays for your Medicare deductibles and coinsurance, leaving you with very few, if any, out-of-pocket costs when you receive care. Your budget is predictable and stable.

Medicare Advantage plans often attract people with their low or $0 monthly premiums. However, you pay for services as you need them through copays and coinsurance. These plans have a Maximum Out-of-Pocket (MOOP) limit that caps your annual spending, but this safety net can still be several thousand dollars.

Doctor Choice and Networks

Your freedom to choose providers is another crucial distinction. Because Medigap supplements Original Medicare, you can see any doctor or visit any hospital in the U.S. that accepts Medicare. There are no networks to worry about, and you never need a referral to see a specialist. For more details on how these plans are structured, official state resources like the Consumer’s Guide to Medicare Supplement Insurance can provide valuable context.

Medicare Advantage plans, on the other hand, are network-based (typically HMOs or PPOs). To keep costs down, you must use doctors, specialists, and hospitals within the plan’s approved network. Many HMO plans also require you to get a referral from your primary care physician before seeing a specialist.

Medigap Plans

- Premiums: Higher monthly premium

- Doctor Choice: Freedom to see any doctor accepting Medicare, nationwide

- Out-of-Pocket: Little to no costs for covered services

Medicare Advantage

- Premiums: Low or $0 monthly premium

- Doctor Choice: Must use doctors in a local provider network (HMO/PPO)

- Out-of-Pocket: Pay copays and coinsurance as you go

Which Path is Right for You?

Ultimately, the best choice depends on your priorities. If you value predictable healthcare spending and the complete freedom to choose your providers without network hassles, a Medigap plan is an excellent choice. If you prefer a lower monthly premium and are comfortable navigating a provider network for your care, then a Medicare Advantage plan might be a better fit.

Feeling stuck? This is the most important decision you’ll make, and you don’t have to make it alone. Our expert guidance can simplify this choice.

The Standardized Medigap Plans (A-N): Explained Simply

Navigating the different medicare supplement plans can feel like trying to solve a puzzle. The good news? It’s much simpler than it looks. In most states, there are 10 standardized plans, labeled with letters A through N. “Standardized” means that the benefits for each plan letter are the same, no matter which insurance company offers it. A Plan G from one company has the exact same core benefits as a Plan G from another.

While there are 10 options, most new Medicare enrollees find that their best choice is either Plan G or Plan N. Let’s break down the most popular options to help you find your perfect fit.

Plan G vs. Plan N vs. Plan F: A Quick Comparison

- Part B Deductible:

- Plan G: You pay this ($240 in 2024).

- Plan N: You pay this ($240 in 2024).

- Plan F: Covered (Only for those eligible for Medicare before Jan 1, 2020).

- Part B Coinsurance/Copayments:

- Plan G: 100% covered.

- Plan N: Covered, but you pay small copays (up to $20 for doctor visits, up to $50 for ER).

- Plan F: 100% covered.

- Part B Excess Charges:

- Plan G: 100% covered.

- Plan N: Not covered.

- Plan F: 100% covered.

Plan G: The Most Comprehensive Choice

Plan G is the most popular choice for new Medicare beneficiaries, and for good reason. It offers the most comprehensive coverage available. Once you pay the annual Medicare Part B deductible ($240 in 2024), Plan G covers nearly all of the remaining gaps in Original Medicare. This means no copays for doctor visits and no surprise bills. It is the ideal choice for anyone who wants maximum coverage, predictable costs, and ultimate peace of mind.

Plan N: A Lower Premium Option

If you’re looking for excellent coverage with a lower monthly premium, Plan N is a fantastic option. In exchange for that lower premium, you agree to some minor cost-sharing. This includes small, predictable copayments: up to $20 for some office visits and up to $50 for an emergency room visit (if you aren’t admitted). Plan N does not cover Part B “excess charges,” which are rare situations where a doctor charges more than the Medicare-approved amount. It’s a great fit for healthier individuals comfortable with small, occasional out-of-pocket costs.

Other Medigap Plans

While G and N are the front-runners, a few other medicare supplement plans exist. The High-Deductible Plan G offers very low premiums but requires you to meet a large annual deductible before it pays anything. Other plans, like K, L, and M, involve different cost-sharing structures but are far less common. While it can be helpful to know these exist, getting expert guidance can help you determine if they are right for your specific situation. For truly unbiased, free counseling, you can also connect with a volunteer at your local State Health Insurance Assistance Program (SHIP).

Ultimately, our goal is to help you move from confusion to confidence. Finding the right plan doesn’t have to be complicated. Contact us today for personalized, straightforward guidance.

How to Enroll: Your Medigap Open Enrollment Period

Navigating the timing of your enrollment is one of the most critical steps in securing the right coverage. If there’s one piece of advice to take away, it’s this: your one-time Medigap Open Enrollment Period is the single best time to buy a Medigap plan. This is your golden ticket to getting any plan you want, without any health-related hurdles.

This crucial window begins on the first day of the month you are both 65 or older and enrolled in Medicare Part B. It lasts for six full months. During this protected period, you have what are called “guaranteed issue rights.” This simply means that insurance companies that sell medicare supplement plans in your state must sell you any plan they offer. They cannot use your health history to deny you coverage or charge you a higher premium. This is your one chance to get the best price regardless of pre-existing conditions.

What Happens if You Miss Your Open Enrollment?

If you miss this six-month window, you can still apply for a Medigap plan at any time. However, you will likely have to go through medical underwriting. An insurance company can review your entire health history, ask detailed medical questions, and based on that information, they have the right to deny your application or charge you a much higher rate. While certain situations, like losing employer coverage, may grant you another Special Enrollment Period, your initial Open Enrollment is your most powerful opportunity.

The Simple 4-Step Enrollment Process

We believe in turning confusion into confidence. Enrolling in the right plan doesn’t have to be complicated. Here is a straightforward, four-step process to guide you:

- Step 1: Confirm Your Enrollment. First, ensure you are officially enrolled in both Medicare Part A and Part B. You cannot purchase a Medigap plan without them.

- Step 2: Choose Your Plan. Decide which plan letter (like the popular Plan G or Plan N) offers the level of coverage that gives you peace of mind.

- Step 3: Compare Insurers. Because medicare supplement plans are standardized, a Plan G from one company has the exact same medical benefits as a Plan G from another. The only difference is the price. Comparing quotes is essential.

- Step 4: Apply with Unbiased Guidance. Working with an independent broker ensures you see all your options without any bias toward one company. We help you find the best rate and handle the application for you.

The comparison shopping in Step 3 is where many people feel overwhelmed. Let us provide the clarity and support you deserve. We’ll do the heavy lifting to find the most competitive rates for the plan you choose, at no cost to you. Get your free quote today.

Making Your Medigap Decision with Confidence

Navigating the world of Medicare can feel overwhelming, but understanding the fundamentals is the first step toward peace of mind. As you’ve learned, the right medicare supplement plans work with Original Medicare to cover costs like deductibles and copayments. Recognizing the crucial differences between Medigap and Medicare Advantage, and knowing the importance of your Open Enrollment Period, empowers you to make a choice that protects both your health and finances for years to come.

You don’t have to sort through this complex maze alone. For personalized advice tailored to your specific needs, let us help you compare your options. As an independent broker representing over 40 carriers, we provide the unbiased, expert guidance that has helped over 5,000 clients find their ideal coverage with confidence. Our goal is to help you avoid costly enrollment mistakes and secure a plan that truly works for you.

Get a Free, Unbiased Medigap Plan Comparison

Take the next step toward clarity and security in your healthcare journey. You’ve got this.

Frequently Asked Questions About Medicare Supplement Plans

Do Medicare Supplement plans cover prescription drugs?

This is a common and important question. Medicare Supplement plans do not include coverage for prescription drugs. Their purpose is to help pay for your out-of-pocket costs from Original Medicare Part A and Part B, such as deductibles and coinsurance. To get coverage for your medications, you will need to enroll in a separate, standalone Medicare Part D Prescription Drug Plan. We can help you find a Part D plan that fits your specific medication needs and simplifies your coverage.

Can I be denied a Medigap plan because of my health?

The timing of your application is crucial. When you first become eligible for Medicare, you have a six-month Medigap Open Enrollment Period. During this protected window, insurance companies cannot deny you coverage or charge you more because of pre-existing health conditions. However, if you apply outside of this period, they can use medical underwriting to review your health history and may deny your application. This is why planning ahead is so important to secure your coverage with confidence.

Are Plan G and Plan F the same thing?

While very similar, Plan G and Plan F are not the same. The only difference is that Plan F covers the annual Medicare Part B deductible, while Plan G does not. For many people, the lower monthly premium for Plan G makes it a better value, even after paying the deductible out-of-pocket. It’s also important to know that Plan F is only available to individuals who were eligible for Medicare before January 1, 2020. For new beneficiaries, Plan G is the most comprehensive option available.

Can I switch my Medicare Supplement plan at any time?

Unlike Medicare Advantage, there is no annual open enrollment period to switch your Medigap plan. You can apply to change your policy at any time, but in most states, you will likely have to go through medical underwriting. This means the insurance company can review your health history and may deny your application for a new plan. That’s why choosing the right plan from the start is so important. We can provide the expert guidance to help you make a confident choice.

Does my Medigap plan work if I travel to another state?

Yes, and this is one of the greatest benefits of having a Medigap policy. Your coverage travels with you anywhere in the United States. As long as the doctor or hospital accepts Original Medicare, your Medigap plan will work seamlessly, with no network restrictions to worry about. This freedom is a major reason why so many people choose medicare supplement plans for their healthcare needs, giving them peace of mind whether they are at home or on the road.

Why do different companies charge different prices for the same Medigap plan?

This is where expert guidance becomes invaluable. While all medicare supplement plans of the same letter (like Plan G) are standardized by the government to offer identical benefits, the insurance companies that sell them are not. Each company sets its own monthly premium based on its own business costs and pricing methods. This means you could pay significantly more for the exact same coverage. Our job is to compare these prices for you, ensuring you get the best value without the confusion.