Medicare Advantage network problems are defined as gaps in care access that occur when your plan’s provider list shrinks, becomes inaccurate, or fails to meet federal adequacy standards. These issues affect real decisions: whether your oncologist stays covered, whether your surgery gets approved, and whether you pay in-network or out-of-pocket rates. The good news is that you can solve most Medicare Advantage network problems through specific, documented steps. Federal rules from the Centers for Medicare and Medicaid Services (CMS), the No Surprises Act, and formal appeals processes give you more power than most beneficiaries realize.

How to solve Medicare Advantage network problems before they cost you

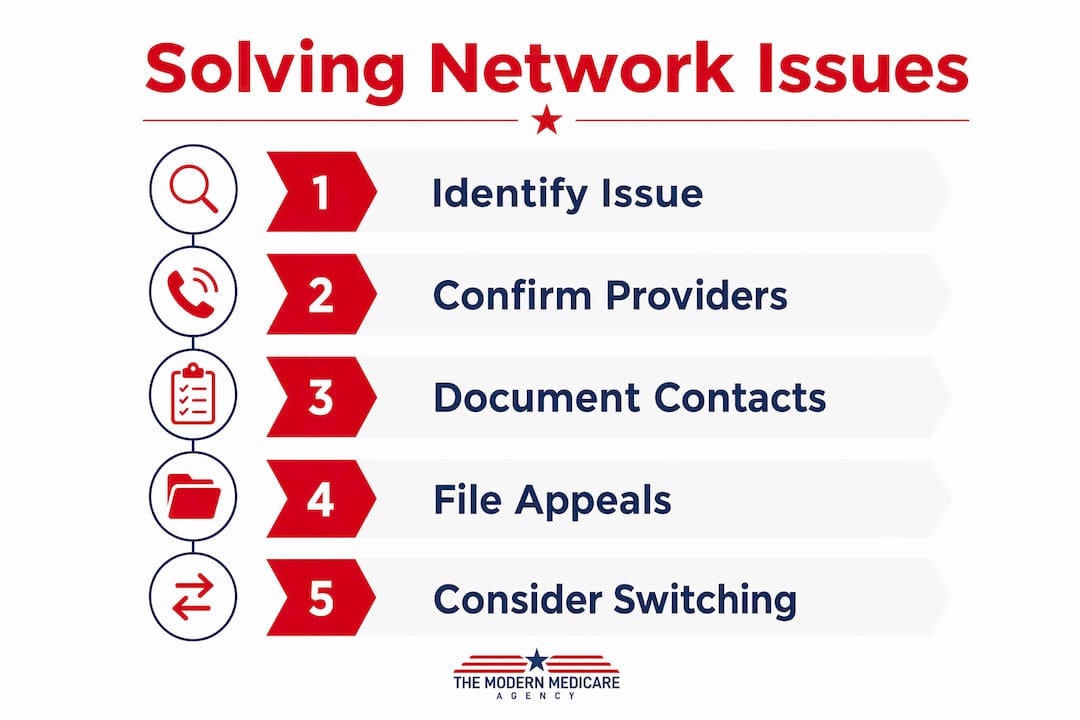

The first step is understanding what you are actually dealing with. Medicare Advantage plans operate on closed or limited networks, meaning your plan only covers care from contracted providers. When a doctor or hospital leaves that network, your costs can spike overnight. Medicare Advantage plans may change their networks mid-year, and you generally cannot switch plans immediately in response. That reality makes early action critical.

Three types of problems account for most beneficiary complaints: a provider leaving the network mid-year, an inaccurate plan directory listing doctors who no longer participate, and prior authorization denials for care your doctor ordered. Each has a specific solution path. Knowing which problem you face determines which tool you use.

How do you confirm your provider is still in-network?

Plan directories are the first place most beneficiaries check, but they are often wrong. Ghost networks, meaning inaccurate plan directories that list providers who no longer participate, are a systemic issue across Medicare Advantage. Relying on an online directory alone puts you at risk of unexpected bills.

Follow these steps to confirm your provider’s status accurately:

- Call your provider’s office directly. Ask the billing department whether they currently accept your specific plan. Get the name of the person you spoke with and write down the date.

- Call your plan’s member services line. Ask them to confirm the provider’s in-network status verbally, then request written confirmation by mail or secure message.

- Check the plan’s online directory as a secondary reference only. Do not treat it as definitive.

- Review any notices your plan has sent. Plan notices of network changes must arrive at least 30 days in advance, but notices sometimes arrive late or not at all.

- Document everything in writing. Note dates, names, and what was confirmed. This record becomes your evidence if you need to appeal.

Pro Tip: Keep a dedicated notebook or digital log for all provider confirmations. If you later need to file an appeal or a CMS complaint, a dated log of your calls and written responses is far stronger than your memory alone.

What rights do you have when your provider leaves mid-year?

The No Surprises Act gives you a specific protection when a provider leaves your network during active treatment. Under this rule, you may continue seeing that provider at in-network cost-sharing rates for up to 90 days, but only if you request it in writing.

This protection applies in these situations:

- You are undergoing an active course of chemotherapy or radiation.

- You are pregnant and past your first trimester.

- You are recovering from a recent surgery and still require follow-up care from the same surgeon.

- You have a serious or complex condition requiring ongoing specialist management.

Routine visits, annual checkups, and new referrals do not qualify. The protection covers continuity of an existing treatment relationship, not general access to a preferred doctor. Submit your written request to your insurer as soon as you learn of the provider’s departure. Waiting too long can forfeit the right entirely. This transitional care clause protects you both financially and medically during a vulnerable period of treatment.

How do you appeal a denied service or prior authorization?

Prior authorization denials are one of the most common Medicare Advantage issues beneficiaries report, and they are also the most reversible. Less than 20% of Medicare Advantage claim denials are ever appealed, despite a 95% overturn rate on appeal. That gap means most beneficiaries accept denials that would have been reversed if challenged.

Not all denials are the plan’s fault. Administrative errors, such as incomplete documentation or incorrect billing codes submitted by the provider’s office, cause a significant share of denials. Always ask your doctor’s office to review the denial letter before assuming the plan is acting in bad faith.

Follow this process to appeal effectively:

- Request the denial in writing. You are entitled to a written explanation of why the service was denied.

- Identify the reason for denial. Determine whether it is a medical necessity dispute, a network issue, or a paperwork error.

- Gather supporting documentation. Collect your doctor’s notes, test results, treatment plans, and any prior approval records.

- File a Level 1 appeal with your plan. Submit within 60 days of the denial notice. Include all supporting documents.

- Escalate if needed. If your plan upholds the denial, you can request an independent review by a Qualified Independent Contractor (QIC).

Key documents to include in every appeal:

- The original denial letter

- A letter of medical necessity from your treating physician

- Relevant clinical guidelines supporting the treatment

- Your dated log of calls and communications with the plan

For a complete walkthrough, the Medicare Advantage appeal guide at Paulbinsurance covers each level of the process in plain language.

How do you file a network adequacy complaint with CMS?

Network adequacy is the federal standard requiring Medicare Advantage plans to maintain a sufficient number of in-network providers for each specialty in your area. When a plan fails that standard, you have the right to file a formal complaint with CMS. Filing complaints can result in approval for out-of-network care at in-network rates if CMS finds the network inadequate.

Common violations that justify a complaint include:

- No in-network specialist available within a reasonable distance for your condition

- A plan directory listing providers who have not accepted patients in months

- Repeated referral denials due to lack of contracted specialists

- Documented refusal by in-network providers to accept new patients

To build a strong complaint, gather this evidence first:

- A list of in-network specialists you contacted and their responses

- Dates and names from calls to your plan’s member services

- Any written denials or referral refusals

- Documentation showing the nearest in-network provider is unreasonably far away

File your complaint by calling 1-800-MEDICARE or using the online complaint portal at Medicare.gov. You can also contact your State Health Insurance Assistance Program (SHIP) for free local help preparing your submission.

Pro Tip: Federal scrutiny of Medicare Advantage networks is intensifying. Collective complaints from multiple beneficiaries in the same area carry more regulatory weight and are more likely to trigger a formal plan audit.

When should you consider switching plans?

Switching plans is not always possible mid-year. Most routine network changes do not qualify for a Special Enrollment Period (SEP), meaning you are generally locked in until the next enrollment window. Understanding the timeline prevents costly mistakes.

Your main enrollment windows are:

- Annual Enrollment Period (AEP): october 15 through december 7 each year. This is your primary opportunity to switch Medicare Advantage plans.

- Medicare Advantage Open Enrollment Period: january 1 through march 31. You can switch to a different Advantage plan or return to Original Medicare once during this window.

- Special Enrollment Periods: Available in limited circumstances, such as moving out of your plan’s service area or qualifying for Medicaid. A provider leaving your network alone rarely qualifies.

Before switching, research the new plan’s provider directory carefully. Call the offices of your most important doctors and confirm they accept the new plan before you enroll. Also consider what switching means for any Medigap coverage you might want later. Returning to Original Medicare after years on a Medicare Advantage plan can make it harder to qualify for a Medicare Supplement policy at standard rates, depending on your state’s rules.

Pro Tip: Start your AEP research in september, not october. Give yourself six weeks to compare networks, call provider offices, and review drug formularies before the window opens.

For guidance on selecting the right plan based on your specific providers and health needs, Paulbinsurance has a practical checklist built for this exact decision.

Key Takeaways

Solving Medicare Advantage network problems requires documentation, knowledge of your federal rights, and timely action through appeals, complaints, and enrollment planning.

| Point | Details |

|---|---|

| Verify provider status directly | Call the provider’s billing office and your plan to confirm in-network status. Never rely on directories alone. |

| Use No Surprises Act protections | Request transitional care in writing within 90 days if your provider leaves during active treatment. |

| Appeal every denial | Less than 20% of denials are appealed, yet 95% are overturned. File with full documentation every time. |

| File CMS complaints for network gaps | Documented evidence of inadequate networks can result in out-of-network care approved at in-network rates. |

| Plan switches during AEP, not mid-year | Most network changes do not trigger a Special Enrollment Period. Research and switch during october 15 to december 7. |

What I’ve learned after nearly 20 years helping Medicare beneficiaries

The single biggest mistake I see is beneficiaries accepting the first “no” they get. A denial letter feels final. It is not. The appeals process exists precisely because the system produces errors, and the data backs that up. A 95% overturn rate is not a fluke. It reflects how often initial denials are wrong, incomplete, or based on missing paperwork.

The second mistake is waiting. When your doctor leaves your plan’s network, the clock starts immediately. The 90-day transitional care window under the No Surprises Act does not pause while you figure out what to do. I have seen beneficiaries lose that protection simply because they did not know they had to request it in writing within a specific timeframe.

What actually works is treating your Medicare coverage like a job. Keep records. Confirm things in writing. Call back if you do not get a response. The beneficiaries who get the best outcomes are not the ones with the most complicated situations. They are the ones who document everything and push back when something is wrong. Federal oversight of Medicare Advantage is tightening, and that is good news. But the rules only protect you if you use them.

— Paul

How Paulbinsurance helps you get the coverage that actually works

Network problems are often a sign that a Medicare Advantage plan is no longer the right fit. Paulbinsurance has been helping Medicare beneficiaries cut through plan confusion since 2007, and the team of independent agents knows how to match your specific doctors, health needs, and budget to the right coverage.

Whether you are weighing a plan switch during the Annual Enrollment Period or exploring whether a Medicare Supplement plan gives you more predictable access to care, Paulbinsurance offers no-pressure, education-first guidance. You can also compare your options directly with the Advantage vs. Supplement comparison guide to see which structure fits your situation. Reach out to Paulbinsurance for a personalized review at no cost.

FAQ

What is a Medicare Advantage network problem?

A Medicare Advantage network problem occurs when your plan’s provider list changes, becomes inaccurate, or lacks sufficient specialists, limiting your access to covered care. Common examples include a doctor leaving the network mid-year or a prior authorization denial for a medically necessary service.

Can I switch Medicare Advantage plans if my doctor leaves the network?

Most mid-year network changes do not qualify for a Special Enrollment Period, so you are typically locked in until the Annual Enrollment Period from october 15 through december 7. Call 1-800-MEDICARE or your SHIP counselor to confirm whether your specific situation qualifies for an exception.

How often are Medicare Advantage denials overturned on appeal?

Approximately 95% of Medicare Advantage denials are overturned when beneficiaries appeal, yet fewer than 20% of denials are ever challenged. Filing a documented appeal is the single most effective step you can take after a denial.

What is a ghost network in Medicare Advantage?

A ghost network is a plan directory that lists providers who no longer accept the plan, misleading beneficiaries into thinking they have more coverage options than they actually do. Always call the provider’s office directly to confirm participation before scheduling care.

How do I file a network adequacy complaint with CMS?

Call 1-800-MEDICARE or submit a complaint through Medicare.gov with documented evidence that your plan lacks sufficient in-network providers. CMS can approve out-of-network care at in-network rates if it finds the plan’s network inadequate.