Last Tuesday, a Massapequa resident named Robert sat at his kitchen table staring at a stack of 2026 mailers, wondering if he could still afford to see his regular specialist at St. Joseph Hospital. It’s a common scene in Nassau County where the sheer volume of “zero dollar” plan offers can feel more like a sales pitch than actual help. We understand that the fear of hidden Part D costs or falling into a coverage gap can keep you up at night. Understanding Medicare costs in Massapequa NY shouldn’t be this stressful, and you shouldn’t have to guess if your favorite local doctors are still in your network.

We’re here to simplify the jargon and provide you with the exact dollar amounts you need to know for the 2026 season. Our goal is to move you from a state of confusion to total financial confidence by breaking down the new $2,000 out-of-pocket prescription cap and the latest local premium shifts. This guide provides a clear look at the 2026 Nassau County landscape so you can protect your health and your savings without the pressure of a typical insurance agent.

Key Takeaways

- We explain the unique 2026 landscape in Nassau County so you can navigate the latest coverage changes with total peace of mind.

- Understanding Medicare costs in Massapequa NY becomes simple as we break down the 2026 premiums, deductibles, and IRMAA rules for your household.

- Learn how to use our financial checklist to verify that your preferred specialists at Northwell Health or Catholic Health remain in-network for the coming year.

- We compare the predictable budgeting of Medigap against Medicare Advantage options to help you choose the path that best protects your retirement savings.

- Discover the advantage of using an independent broker to compare 40+ carriers and find a “best fit” plan tailored specifically to your Massapequa lifestyle.

The 2026 Medicare Landscape in Massapequa: What’s Changed?

Living in Massapequa means enjoying the best of the South Shore, from the quiet streets of Massapequa Park to the waterfront views in Biltmore Shores. However, for many of our neighbors reaching age 65 or looking at their annual options, the local insurance market feels like a confusing maze. We know that the stress of choosing the right plan can be overwhelming. You want to protect your health and your savings, but the sheer volume of mail and phone calls you receive makes it hard to find clarity. The Modern Medicare Agency’s goal is to replace that anxiety with peace of mind by simplifying the complex world of 2026 coverage.

The 2026 environment in Nassau County is more competitive than ever. Because our area has a high density of healthcare providers and a large population of seniors, private insurers fight for your business. This competition gives Massapequa residents more options than almost any other part of New York State. While the foundation of Medicare (United States) provides the same basic Parts A and B across the country, the local Advantage and Supplement plans available in our 11758 zip code are unique. The Modern Medicare Agency helps you look past the flashy advertisements to see what these plans actually offer your specific lifestyle.

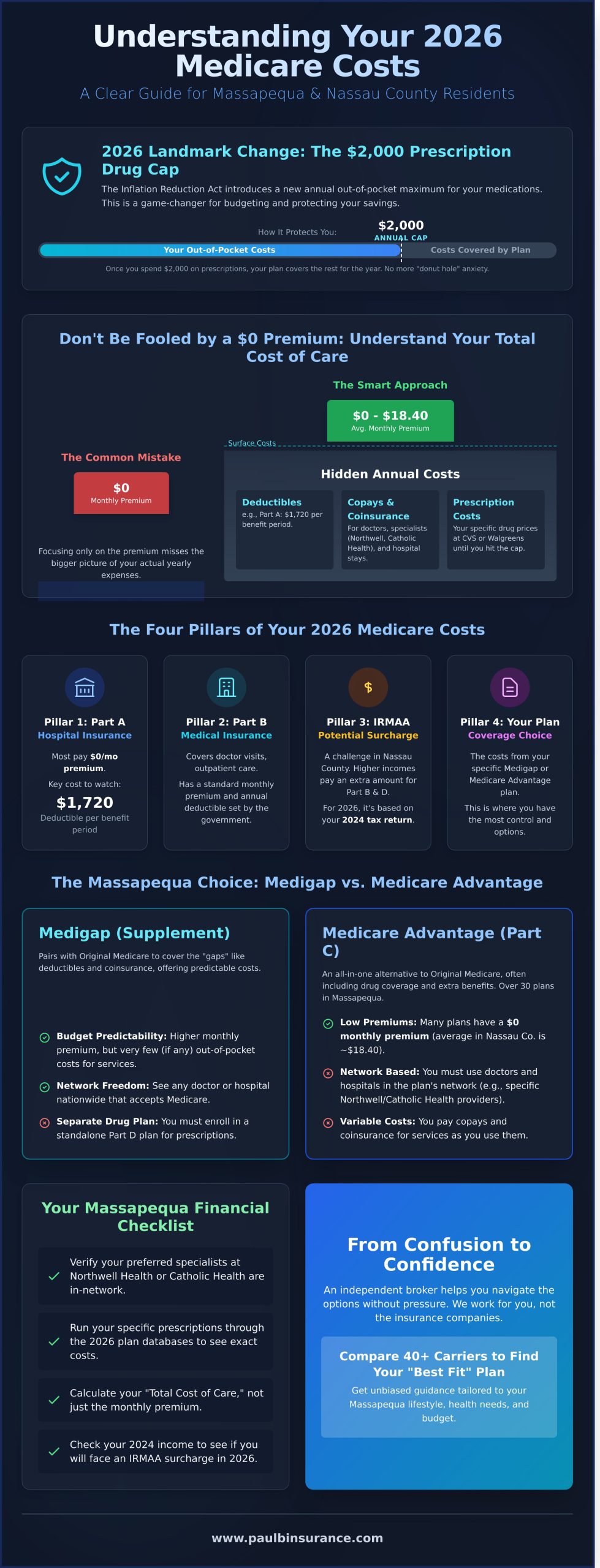

Understanding Medicare costs in Massapequa NY requires a shift in how you view your healthcare budget. Many people make the mistake of looking only at the monthly premium. The Modern Medicare Agency teaches our neighbors to focus on the “Total Cost of Care” instead. This includes your premiums, but it also accounts for deductibles, copays at local Northwell or Catholic Health facilities, and the price of your specific prescriptions at the neighborhood CVS or Walgreens. A plan with a $0 premium might actually cost you more over a full year if your specialist copays are high.

Massapequa Medicare by the Numbers

For the 2026 plan year, Massapequa residents can choose from over 30 different Medicare Advantage plans. This variety is a double edged sword. While $0 premium plans have become the standard in Nassau County, they aren’t “free” healthcare. These plans often use a network of specific doctors and require copayments for every visit. The average monthly premium for a Medicare Advantage plan in Nassau County for 2026 sits at approximately $18.40, though many residents successfully find high quality coverage for no monthly cost at all.

Why 2026 is a Landmark Year for Costs

This year marks a massive shift because of the full implementation of the Inflation Reduction Act. The most significant change for Massapequa seniors is the new $2,000 annual out of pocket limit on prescription drugs. If you have high medication costs, this cap is a literal lifesaver. It prevents the “donut hole” from draining your retirement savings. The Modern Medicare Agency specializes in helping you transition from confusion to confidence during this historic shift. The Modern Medicare Agency takes the time to run your specific medications through the 2026 databases so you know exactly what your pharmacy bill will look like on January 1st. Understanding Medicare costs in Massapequa NY shouldn’t be a guessing game. The Modern Medicare Agency provides the clear, unbiased guidance you need to feel secure in your choices.

Breaking Down the Four Pillars of Medicare Costs

We know how heavy the mail feels when you approach age 65. It’s a mountain of glossy brochures and confusing letters that make you feel like you’re back in a high-pressure classroom. Understanding Medicare costs in Massapequa NY doesn’t have to be a source of stress. We believe in keeping things simple. By breaking your expenses down into four clear pillars, we can help you plan a budget that protects your hard-earned savings. In 2026, these costs are more predictable than ever, but you still need a clear map to avoid the pitfalls of the Long Island healthcare market.

Many of our neighbors in Massapequa face a unique challenge: the Income Related Monthly Adjustment Amount, or IRMAA. Because many local households have higher retirement incomes or recently sold property, they often trigger these surcharges. If your modified adjusted gross income from two years ago exceeds specific thresholds, the government adds an extra fee to your Part B and Part D premiums. We help you look back at your 2024 tax returns to see if these 2026 surcharges will impact your monthly check. It’s all about removing the “gotcha” moments from your retirement.

Part A & B: The Government Foundation

Part A is your hospital insurance. For most of us, the monthly premium is $0, but the deductible is the number to watch. In 2026, the Part A deductible has risen to $1,720 per benefit period. This isn’t an annual cost; you could potentially pay it more than once a year if you have multiple hospital stays. Part B covers your doctor visits and outpatient care. The standard monthly premium for 2026 is $194.50, which is typically deducted directly from your Social Security benefits. You can view a full list of current Medicare costs to see how these base rates apply to your situation.

The biggest risk we see in Massapequa is relying on “Original Medicare” alone. There’s a 20% gap that the government doesn’t cover. If you have a major procedure at a facility like St. Joseph Hospital or Northwell Health, you’re responsible for 20% of the total bill with no limit. On Long Island, where medical costs are among the highest in the country, that 20% can easily reach tens of thousands of dollars. This is why we focus so heavily on the Maximum Out-of-Pocket (MOOP) limit. Your MOOP is the most important number in your plan because it acts as a financial ceiling, ensuring a health crisis doesn’t become a financial one.

Part D: The 2026 Prescription Revolution

This year marks a massive shift in how you pay for medications. The 2026 Medicare landscape is much friendlier to your wallet thanks to the official end of the “Donut Hole.” You no longer have to worry about that confusing gap in coverage where costs suddenly spiked. Instead, everyone now benefits from a $2,000 annual out-of-pocket cap on prescription drugs. Once you spend $2,000 on covered medications at your local CVS or Walgreens, your plan pays 100% of your drug costs for the rest of the year. This change provides incredible peace of mind for seniors managing chronic conditions.

Choosing the right Medicare Part D plan is still a personal process. We don’t believe in one-size-fits-all solutions. We look at the specific medications you take and check which plans offer the best “formularies” or lists of covered drugs. We also check which plans have the best relationships with the pharmacies right here in Massapequa. If you want to make sure you aren’t overpaying for your prescriptions this year, you can schedule a quick review with us to look at your 2026 options. We’ll help you move from confusion to confidence by showing you exactly where every dollar is going.

- Part A Deductible: $1,720 per benefit period in 2026.

- Part B Premium: $194.50 monthly for most beneficiaries.

- Part D Cap: A new $2,000 maximum limit on your annual drug costs.

- The 20% Gap: The financial risk of not having a supplemental or Advantage plan.

Medigap vs. Medicare Advantage: The Massapequa Choice

Choosing between Medigap and Medicare Advantage is the most significant decision you’ll face this year. We see many of our Nassau County neighbors feeling stuck between these two very different paths. Understanding Medicare costs in Massapequa NY requires looking past the monthly premium and seeing the full picture of your potential out-of-pocket expenses. Our goal is to move you from confusion to confidence by laying out the facts clearly. We rely on the official 2026 Medicare costs to build your personalized budget, ensuring there are no surprises when you visit your doctor.

The right choice depends entirely on your health needs and your financial comfort zone. Some of our clients prefer a fixed monthly cost, while others like the “all-in-one” convenience of modern plans. We take the time to look at your specific list of doctors at Northwell Health or Catholic Health to ensure they are in-network before you sign a single document. This personal touch prevents the stress of finding out your favorite specialist isn’t covered after it’s too late.

The Case for Medicare Supplement (Medigap)

Predictability is the main reason our Long Island clients choose a Medigap plan. In 2026, Plan G remains the gold standard because it covers nearly all your gaps in Original Medicare. If you have a procedure at St. Joseph Hospital, you won’t deal with a stack of unexpected co-pays. You pay your monthly premium, and the plan handles the rest. This freedom of movement is vital if you travel. You can use your coverage at any facility in the United States that accepts Medicare. There are no networks to worry about and no referrals required to see a specialist.

The Medicare Advantage (Part C) Reality

Medicare Advantage plans are popular in Massapequa because of their low or $0 monthly premiums. However, it’s a trade-off. You pay less upfront but agree to pay co-pays when you actually use services. We recommend reviewing our Medicare Advantage guide to understand how these local networks function. In 2026, these plans have added impressive “extras” that Original Medicare doesn’t offer. This includes comprehensive dental care, vision exams, and even transportation to clinics near the Sunrise Mall area. Many plans also include memberships to local fitness centers to keep you active and healthy.

Understanding Medicare costs in Massapequa NY means calculating your “total cost of ownership” for the year. We help you compare the annual maximum out-of-pocket limits on Advantage plans against the steady premiums of Medigap. We don’t believe in one-size-fits-all solutions. Instead, we provide the unbiased guidance you need to protect your savings. Our five-step process ensures you stay in control of your healthcare journey without the typical insurance jargon. We want you to feel empowered, not overwhelmed, as you make this important transition.

- Medigap: Best for those who want no network restrictions and zero co-pays at the doctor’s office.

- Medicare Advantage: Best for those who want extra benefits like dental and are comfortable using a specific network of Nassau County providers.

- Doctor Check: We verify your specific physicians to ensure your 2026 coverage matches your current lifestyle.

We are here to act as your advocate. Whether you are leaning toward the stability of Plan G or the added value of an Advantage plan, we make sure the math works for your retirement budget. You deserve a plan that offers peace of mind and keeps your favorite doctors within reach.

Your Massapequa Medicare Financial Checklist

Organizing your healthcare finances shouldn’t feel like a second job. We want to replace that heavy feeling of uncertainty with a clear, actionable plan. Understanding Medicare costs in Massapequa NY starts with a simple checklist that protects your savings and your peace of mind. By following these four steps, you can enter 2026 with total confidence in your coverage.

- Step 1: Audit your prescriptions for 2026 formulary changes. The $2,000 annual out-of-pocket cap on Part D drugs is now fully in effect for 2026. This is a massive win for seniors, but plans often change which specific drugs they cover to compensate. We check your current medications against the new 11758 area formularies to ensure you aren’t hit with a “tier jump” that raises your costs.

- Step 2: Verify your specialists at Northwell Health or Catholic Health systems. Many of our neighbors rely on Northwell Health facilities or Catholic Health providers like St. Joseph Hospital in Bethpage. Doctors frequently move in and out of insurance networks. We verify that your specific specialists on Merrick Road or Sunrise Highway are still participating in your chosen plan for the 2026 calendar year.

- Step 3: Calculate your total annual cost (Premiums + MOOP). Don’t just look at the monthly premium. The Maximum Out-of-Pocket (MOOP) limit is your ultimate safety net. In 2026, some Medicare Advantage plans have shifted these limits. We help you add up the worst-case scenario costs so you know exactly what your bank account needs to handle.

- Step 4: Assess your need for dental insurance or vision coverage. Original Medicare still leaves a gap when it comes to your teeth and eyes. Whether you need a simple cleaning or a more complex procedure, we look at standalone plans or integrated Medicare Advantage benefits to keep your smile healthy without breaking the bank.

Local Provider Networks in 11758

Massapequa sits in a unique spot where provider networks can be tricky. We’ve seen residents face “Network Gaps” where their primary care doctor on Merrick Road is in-network, but the specialist they need at a nearby hospital is not. If you choose an HMO, you generally have zero coverage for out-of-network providers. A PPO offers more freedom, but you’ll pay a higher percentage of the bill. We analyze these local 11758 networks to ensure your healthcare team stays intact. Understanding Medicare costs in Massapequa NY requires this level of local detail to avoid five-figure medical bills.

Avoiding Costly Enrollment Penalties

Missing your enrollment window is a mistake that costs you every single month for the rest of your life. The Part B late enrollment penalty adds a permanent 10% charge to your premium for every 12-month period you were eligible but didn’t sign up. Part D carries a similar 1% monthly penalty. We’re here to be your advocate and ensure you meet every deadline during your Initial Enrollment Period. If you need to make a change or missed your window, the 2026 General Enrollment Period runs from January 1 to March 31. We’ll guide you through the paperwork so you can stop worrying about the clock.

We’re ready to help you move from confusion to confidence. Schedule a Call With Paul to review your 2026 checklist today.

From Confusion to Confidence: How We Help You Save

We know the feeling of staring at a kitchen table covered in colorful Medicare brochures and feeling more lost than when you started. The 2026 landscape has brought new changes to drug pricing and plan structures that can make anyone feel overwhelmed. Understanding Medicare costs in Massapequa NY is not just about looking at a monthly premium; it is about knowing how your specific doctors and prescriptions fit into the puzzle. We are here to clear the air and move you from a state of uncertainty to total confidence.

Many seniors don’t realize there is a massive difference between a captive agent and an independent broker. A captive agent is an employee of a single insurance company. They are trained to sell you that company’s specific products, even if a competitor offers a better rate or wider network in Nassau County. We operate differently. As an independent brokerage, we don’t work for the insurance companies; we work for you. We have no loyalty to any specific brand, which means our only goal is finding the plan that protects your wallet and your health.

Our team compares over 43 different carriers available in the 11758 zip code for 2026. This is vital because plan benefits change every single year. For instance, a plan that was the “best fit” for your neighbor in 2025 might have increased its specialist copays by 15 percent this year. We use real-time data to analyze every option, ensuring you don’t overpay for coverage you don’t need. We provide this guidance at no cost to you, removing the pressure and allowing you to make a choice based on facts rather than a sales pitch.

Our relationship doesn’t end once you sign a piece of paper. We provide year-round support to handle the “what ifs” that pop up in July or October. If you receive a confusing bill from a clinic on Sunrise Highway or your medication tier changes unexpectedly, we are the first call you make. We believe that true peace of mind comes from having a local advocate who knows your name and your history, not a voice in a distant call center.

The Modern Medicare Agency Advantage

Our 5-step process simplifies your 2026 transition by focusing on discovery, research, comparison, enrollment, and annual review. We look at your specific health needs every year because your prescriptions, like Eliquis or Jardiance, might move to a more expensive tier. Having a local advocate in your corner means you have someone to fight for you if a claim is denied or if you need to find a new specialist in Massapequa who accepts your plan.

Start Your 2026 Planning Today

Waiting until the December 7 deadline often leads to rushed decisions and higher costs. In 2025, approximately 14 percent of local seniors paid higher out-of-pocket costs because they missed the optimal window for plan switches. We invite you to schedule a no-pressure, simple conversation with our team to review your options early. You don’t have to navigate the Medicare maze alone; let us lead the way. Schedule a Call With Paul today to secure your future.

Take Control of Your 2026 Coverage Today

Navigating the 2026 Medicare landscape doesn’t have to feel like a second job. We’ve explored how the four pillars of coverage impact your wallet and why choosing between Medigap and Medicare Advantage is a vital decision for your Nassau County budget. Understanding Medicare costs in Massapequa NY is really about finding that perfect balance between monthly premiums and out of pocket protection. You don’t need to guess which plan fits your lifestyle or worry about missing a deadline. With over a decade of local Long Island expertise, we’ve helped thousands of neighbors move from confusion to confidence. We provide access to 40+ insurance carriers and hold licenses in 34+ states to ensure you get unbiased guidance every single time. We’re here to protect you from late penalties and expensive enrollment mistakes that can haunt your finances for years. You deserve a partner who’s never rushed and never pressured. Let’s make sure your 2026 coverage is simple, clear, and secure. We’re ready to help you find the peace of mind you deserve.

Schedule a Call With Paul to simplify your 2026 Medicare costs today

Frequently Asked Questions

What is the average cost of a Medicare Advantage plan in Massapequa for 2026?

The average monthly premium for a Medicare Advantage plan in Nassau County for 2026 is approximately $18.40, though many residents choose plans with a $0 premium. Understanding Medicare costs in Massapequa NY involves more than just the monthly bill, as we also look at the maximum out-of-pocket limit. This year, the average limit for in-network services is $5,900. We help you compare these totals so you can choose a plan that fits your budget perfectly.

Do I need to pay a premium for Medicare Part A if I live in Nassau County?

You won’t pay a premium for Medicare Part A if you or your spouse worked at least 10 years and paid Medicare taxes during that time. This applies to about 99% of the seniors we assist in Massapequa. If you don’t meet these work requirements, the 2026 monthly premium is either $285 or $522 depending on your specific history. We’ll help you verify your status with Social Security so you can plan with total certainty.

Which Medicare plans are accepted by St. Joseph Hospital in Bethpage/Massapequa?

St. Joseph Hospital currently accepts most major 2026 Medicare Advantage plans, including those from many leading providers, such as Aetna. Because hospital contracts can change on January 1st, we always recommend checking the most recent provider directory before your first appointment of the year. We take the stress out of this process by verifying your specific doctors and specialists. This ensures you keep the medical team you already trust without any billing surprises.

How does the $2,000 drug cap in 2026 affect my Part D plan choice?

The new $2,000 out-of-pocket cap for 2026 means you’ll never pay more than that amount for covered prescriptions in a single calendar year. This federal change has completely eliminated the old “donut hole” coverage gap that caused so much confusion for years. When we help you select a Part D plan, we focus on which formulary covers your specific medications at the lowest cost before you hit that limit. It brings a new level of financial security to your retirement.

Can I switch from Medicare Advantage to Medigap in New York without a health screening?

You can switch from Medicare Advantage to a Medigap plan at any time in New York without answering a single health question. Our state follows a “continuous open enrollment” policy, which is a huge win for seniors who want to change their coverage. It doesn’t matter if you have pre-existing conditions or chronic health issues. We guide you through this transition to ensure you have a seamless move from one plan to the other without any coverage gaps.

What are the IRMAA income thresholds for 2026?

For 2026, the IRMAA surcharges begin if your 2024 tax return shows a modified adjusted gross income over $109,000 for individuals or $218,000 for couples. These thresholds determine if you’ll pay an extra amount on top of your standard Part B and Part D premiums. We’ll help you review these brackets so you aren’t caught off guard by higher costs. If your income has dropped since 2024 due to a life-changing event, we can even help you appeal the decision.

Are dental and vision covered by Original Medicare in Massapequa?

Original Medicare doesn’t cover routine dental cleanings, fillings, or vision exams for glasses in 2026. Understanding Medicare costs in Massapequa NY means looking at supplemental options, like Advantage plans that often include these benefits for $0 extra. Many local plans now offer a $2,000 annual allowance for dental work and $300 for eyewear. We’ll show you how to access these “extra” benefits so you don’t have to pay out-of-pocket for your basic wellness needs.

How do I find a local Medicare broker near Massapequa Park?

You can find a dedicated local expert by scheduling a consultation with us right here in the Massapequa area. We act as your personal guides through the maze of 35 different plans available in Nassau County this year. Our goal is to move you from a state of confusion to total confidence. We’re independent brokers, which means we work for you rather than the insurance companies. We’ll sit down, listen to your needs, and find your perfect match.