Medicare Part D is voluntary prescription drug coverage available through Medicare-approved private plans that helps lower your out-of-pocket costs for medications. If you are turning 65, retiring, or new to Medicare, understanding this benefit is one of the most important financial decisions you will make. The program covers a broad range of brand-name and generic drugs, and 2026 brought significant changes to cost limits that directly affect how much you pay at the pharmacy. Getting this right from the start saves you money and protects you from permanent penalties.

What is Medicare Part D and how does it work?

Medicare Part D is voluntary outpatient prescription drug coverage you choose through Medicare-approved private plans to help lower your prescription drug costs. It is not automatic. You must actively enroll. The program is delivered through private insurance companies that contract with the federal government, covering more than 56 million beneficiaries nationwide. That scale means plan options, costs, and drug lists vary significantly depending on where you live.

Part D comes in two forms. A standalone Prescription Drug Plan, called a PDP, pairs with Original Medicare (Parts A and B). A Medicare Advantage Prescription Drug plan, called an MA-PD, bundles drug coverage inside a Medicare Advantage plan. Both types cover outpatient drugs, but your access to specific medications and pharmacies will differ by plan.

Every Part D plan uses a formulary. A formulary is simply a list of covered drugs, organized into tiers. Lower tiers typically mean lower costs. Higher tiers, often brand-name or specialty drugs, cost more. Checking your drug’s tier before you enroll is not optional. It is the single most important step in choosing a plan.

Key facts about Part D eligibility and enrollment:

- You must be enrolled in Medicare Part A or Part B to join a Part D plan.

- Enrollment is voluntary, but skipping it without other drug coverage triggers penalties.

- Plans are offered by private insurers approved by the Centers for Medicare and Medicaid Services (CMS).

- Coverage applies to outpatient drugs only. Drugs given in a hospital are covered under Part A.

Pro Tip: If you have a Medicare Advantage plan, check whether it already includes drug coverage before enrolling in a separate PDP. Enrolling in both can cause you to lose your Medicare Advantage plan.

What does Medicare Part D cost in 2026?

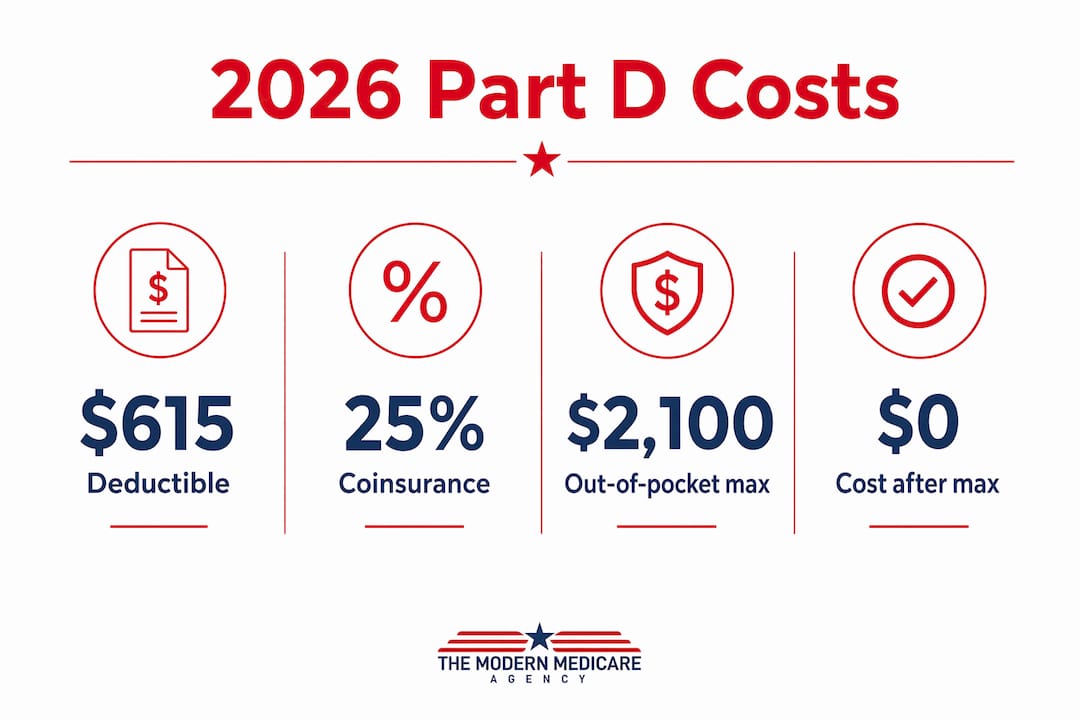

The 2026 standard Part D benefit has a clear cost structure, and it includes one major improvement for people with high drug costs. CMS set the 2026 annual deductible at $615, which is the maximum a plan can charge before coverage kicks in. After the deductible, you pay 25% coinsurance on covered drugs until your total out-of-pocket spending reaches $2,100.

Once you hit $2,100 out-of-pocket, you pay nothing for covered drugs for the rest of the year. The 2026 redesign eliminates cost sharing in the catastrophic coverage phase entirely. This is a direct result of the Inflation Reduction Act and is a major benefit for anyone managing expensive medications like cancer drugs or specialty biologics.

| Cost component | 2026 standard amount |

|---|---|

| Annual deductible | Up to $615 |

| Coinsurance after deductible | 25% of drug costs |

| Out-of-pocket cap | $2,100 |

| Cost sharing after cap | $0 |

Not every plan charges the full $615 deductible. Some plans waive it for lower-tier drugs. Premiums also vary by plan and by state. Pennsylvania residents, for example, will find a range of plan premiums depending on the insurer and county. The standard benchmark is useful for comparison, but pricing your own medications in the Medicare Plan Finder gives you the real number that matters.

Pro Tip: Do not choose a plan based on the lowest monthly premium alone. A plan with a $0 premium but a high deductible and poor drug tier placement can cost you far more over the year than a plan with a modest premium that covers your drugs at a low tier.

When can you enroll in Medicare Part D?

Enrollment timing matters more with Part D than with almost any other Medicare decision. Miss the right window, and you could pay a penalty every month for the rest of your life.

-

Initial Enrollment Period (IEP). This is the seven-month window around your 65th birthday: three months before, the month of, and three months after. Enrolling during this window gives you the earliest start date and avoids any late penalty.

-

Annual Open Enrollment Period. Open enrollment runs from october 15 to december 7 each year. Changes made during this period take effect january 1 of the following year. This is your annual chance to switch plans, drop coverage, or add a PDP.

-

Special Enrollment Periods (SEPs). Certain life events, such as losing employer drug coverage or moving out of a plan’s service area, trigger a SEP. These allow you to enroll or switch outside the standard windows.

-

Late enrollment penalty. The penalty is 1% added to your monthly premium for each month you went without Part D or creditable drug coverage. It is permanent. A 12-month gap means a 12% higher premium for life.

-

Creditable coverage documentation. If you delayed Part D because you had drug coverage through an employer or union plan, you must keep proof of that coverage. Maintaining creditable coverage documentation is the only way to avoid the penalty when you eventually enroll in Part D.

The most common mistake new enrollees make is assuming they do not need Part D because they take no medications right now. Enrolling early and paying a small premium costs far less than the penalty you accumulate by waiting.

How do you choose the best Medicare Part D plan?

The best Part D plan covers your actual medications at the lowest total cost, not just the plan with the lowest monthly premium. That distinction matters because two plans can cover the same drug at completely different cost-sharing tiers. One plan might place your blood pressure medication on Tier 1 at $5 per month. Another might place it on Tier 3 at $45 per month.

How to compare plans effectively

Start with your current medication list. Write down every drug, the dose, and how often you take it. Then use the Medicare Plan Finder at Medicare.gov to enter your drugs and your zip code. The tool shows you the estimated annual cost for each plan based on your specific medications, not just the premium.

Watch for these differences when comparing plans:

- Formulary placement. The same drug can sit on different tiers across plans, changing your cost significantly.

- Pharmacy network. Some plans offer lower costs at preferred pharmacies. Using an out-of-network pharmacy can double your copay.

- Utilization management. Plans can require prior authorization or step therapy before covering certain drugs. Two plans covering the same drug can differ in how quickly and easily you can access it.

- Deductible structure. Some plans waive the deductible for Tier 1 and Tier 2 drugs. If all your medications are generic, this can save you hundreds of dollars.

Comparing plan types side by side

| Feature | Standalone PDP | Medicare Advantage with drug coverage (MA-PD) |

|---|---|---|

| Works with Original Medicare | Yes | No |

| Includes medical coverage | No | Yes |

| Formulary flexibility | Varies by plan | Varies by plan |

| Network restrictions | Pharmacy network only | Medical and pharmacy networks |

| Best for | Those keeping Original Medicare | Those wanting bundled coverage |

Re-evaluate your plan every year during open enrollment. Formularies change annually. A drug covered at Tier 2 this year may move to Tier 4 next year. Your health needs may also change, making a different plan a better fit.

Key Takeaways

Medicare Part D is voluntary prescription drug coverage through private plans, and choosing the right plan based on your specific medications is the single most important step to controlling your drug costs.

| Point | Details |

|---|---|

| Part D is voluntary | You must actively enroll; it does not start automatically when you turn 65. |

| 2026 out-of-pocket cap | After $2,100 in drug costs, you pay $0 for the rest of the year. |

| Late penalty is permanent | Missing enrollment without creditable coverage adds 1% per month to your premium for life. |

| Match plan to your drugs | Use the Medicare Plan Finder to compare plans based on your actual medication list. |

| Review your plan annually | Formularies change every year, so re-evaluate during open enrollment each october. |

What I tell every new Medicare enrollee about Part D

Most people come to me focused on the wrong number. They want the plan with the lowest premium. I understand the instinct. A $0 premium sounds like a win. But after nearly two decades of helping people through Medicare decisions at Paulbinsurance, I can tell you that the premium is almost never the number that hurts people.

The number that hurts people is the one they see at the pharmacy counter in february when their maintenance medication suddenly costs $180 instead of $15. That happens when a plan changes its formulary and nobody told them to check. It happens when they picked a plan without verifying their specific drugs were covered at a reasonable tier.

Here is what I have learned actually works. Sit down with your medication list before open enrollment ends. Price every drug in at least three plans using the Medicare Plan Finder. Look at the total estimated annual cost, not just the monthly premium. If you take specialty medications, call the plan directly and ask about prior authorization requirements before you enroll.

One more thing most articles skip: think about the drugs you might need in the next year, not just what you take today. If your doctor has mentioned a possible new prescription, factor that in. Switching plans mid-year is rarely an option. You are locked in until the next open enrollment in most cases.

The $2,100 out-of-pocket cap in 2026 is genuinely good news for people with high drug costs. It changes the math for anyone on expensive specialty drugs. If that describes you, understanding the 2026 Part D changes in detail before you choose a plan is worth your time.

— Paul

Get personalized help choosing the right Part D plan

Sorting through dozens of Part D plans on your own is time-consuming, and the stakes are real. A wrong choice can cost you hundreds of dollars over the year.

At Paulbinsurance, our independent agents specialize in Medicare and work with new enrollees every day. We compare plans based on your actual medications, your preferred pharmacies, and your budget. Whether you are turning 65, retiring, or new to Medicare eligibility, we walk you through every option without pressure. For a complete breakdown of your Part D plan choices and a side-by-side comparison built around your needs, visit Paulbinsurance’s Part D guide or contact us directly through the website.

FAQ

What is Medicare Part D in simple terms?

Medicare Part D is optional prescription drug coverage offered through private insurance companies approved by Medicare. It helps pay for outpatient medications, including both brand-name and generic drugs.

Does Medicare Part D cover all drugs?

Part D plans must cover a wide range of drugs, but each plan has its own formulary. Plans differ in which drugs they cover and at what cost tier, so checking your specific medications before enrolling is critical.

What happens if I skip Part D when I turn 65?

If you go without Part D or creditable drug coverage, you face a late enrollment penalty of 1% of the national base premium for every month you delayed. This penalty is permanent and raises your monthly premium for as long as you have Part D.

Can I switch my Medicare Part D plan?

You can switch Part D plans during the annual open enrollment period from october 15 to december 7 each year, with changes effective january 1. Certain life events also trigger a Special Enrollment Period that allows a mid-year change.

How does Medicaid affect Medicare Part D?

People who qualify for both Medicare and Medicaid, called dual eligibles, receive Extra Help, a federal program that reduces Part D premiums, deductibles, and copays significantly. Dual-eligible enrollees are automatically enrolled in a benchmark Part D plan if they do not choose one themselves.

Recommended

- How to Check If a Drug Is Covered by Medicare Part D in 2026

- Medicare Part D Explained: Your Simple Guide to Prescription Drug Plans – The Modern Medicare Agency

- Finding the Best Medicare Part D Plans of 2026: A Simple Guide – The Modern Medicare Agency

- Medicare Part D Plans 2026: Navigating the $2,000 Out-of-Pocket Cap and Major Changes – The Modern Medicare Agency