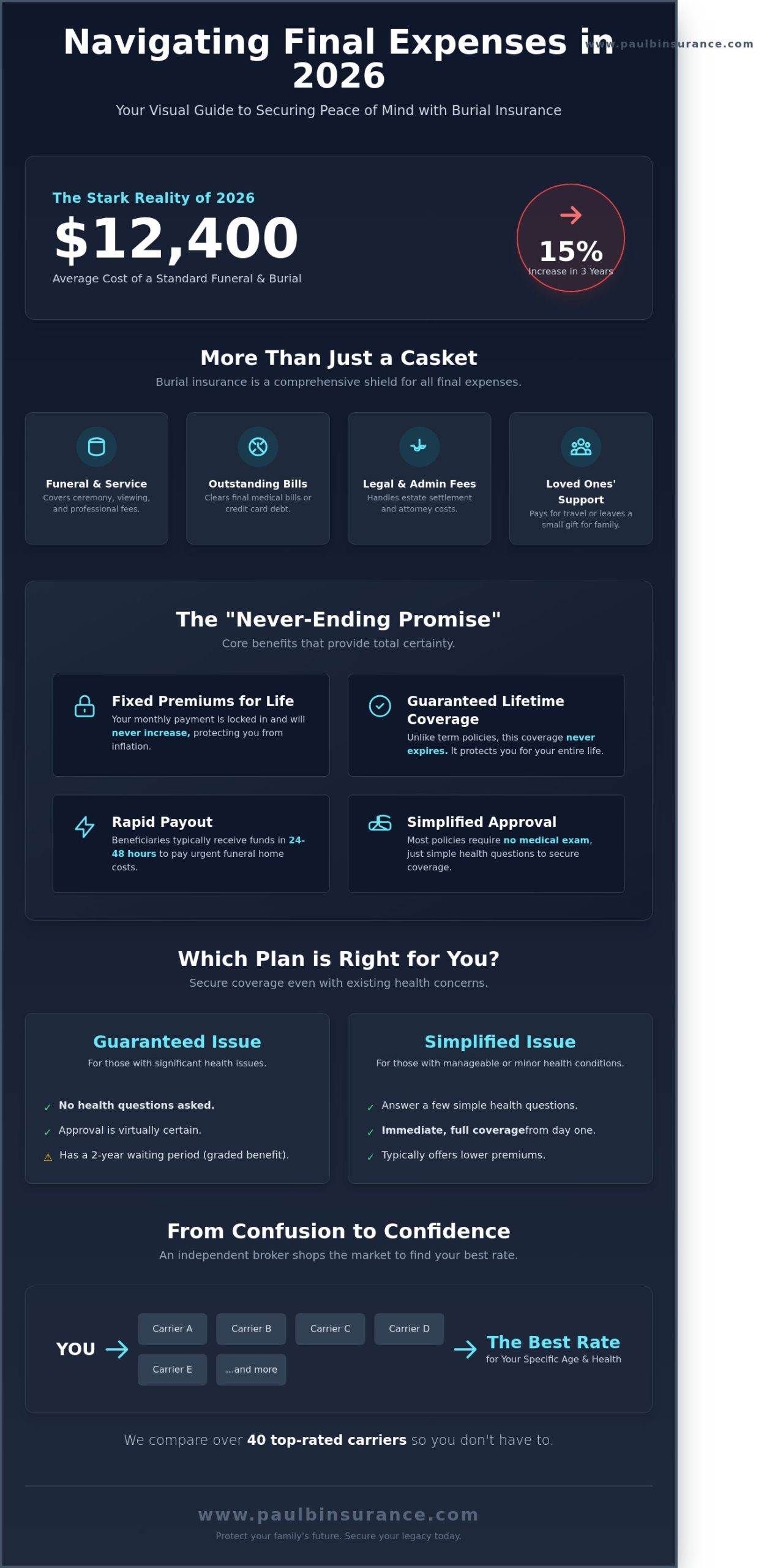

Did you know that by mid-2026, the average cost of a standard funeral and burial service has climbed to a staggering $12,400? This 15% increase over the last three years has left many families feeling unprepared and deeply overwhelmed. If you’re searching for burial insurance to shield your loved ones from these rising costs, you’ve likely felt the sting of confusion between different policy types and the fear of being turned down due to your medical history. It’s a heavy weight to carry, and you aren’t alone in feeling this way.

At The Modern Medicare Agency, we understand that you want a simple solution that doesn’t involve complex jargon or hidden fees. We’re here to help you secure a guaranteed plan where your monthly premiums never increase, ensuring your final expenses are fully covered without leaving a financial burden behind. You deserve to know that your family is protected by a policy that pays out quickly when it matters most. In this guide, we’ll walk you through how to choose the right option from over 40 top-rated carriers so you can move from confusion to total confidence.

Key Takeaways

- Learn how to shield your family from the rising costs of final expenses in 2026 with a plan that covers much more than just the casket.

- Discover how a fixed-premium policy ensures your monthly costs never increase, giving you a “never-ending” promise of protection regardless of your health changes.

- We’ll show you how to choose between guaranteed and simplified issue burial insurance so you can secure coverage even if you have existing health concerns.

- Get a clear breakdown of actual 2026 funeral and cremation costs to help you calculate exactly how much coverage you need for total peace of mind.

- See why working with an independent broker allows us to shop over 40 top-rated carriers to find you the most affordable rate for your specific age and health.

What is Burial Insurance and Why is it Essential in 2026?

We understand that thinking about end-of-life costs feels heavy. It is a conversation most people put off until they can’t anymore. Burial insurance is a specialized type of whole life insurance designed to handle your final bills so your family doesn’t have to. While people often call it “Final Expense Insurance,” its purpose goes far beyond paying for a casket. It covers outstanding medical bills, legal fees, or even a final plane ticket for a grandchild to attend your service. In 2026, these hidden costs of passing away average $3,500 on top of the funeral itself. This is why we prioritize comprehensive planning over simple casket coverage.

Many of our clients come to us confused by the What is Burial Insurance and Why is it Essential in 2026? foundations. They wonder why the large policy they had through their employer isn’t enough. Usually, those work-based policies disappear the moment you retire. We focus on providing a permanent solution that stays with you for life. This isn’t about leaving behind a fortune; it’s about leaving behind peace of mind. We want your family to focus on your legacy, not on how they’ll pay for the memorial service. Giving your loved ones a “worry-free” goodbye is the ultimate gift of care.

Burial Insurance vs. Traditional Life Insurance

In 2026, a $500,000 term policy rarely makes sense for someone over 65. The premiums are sky-high and the medical exams are intrusive. Burial insurance is different because it rarely requires a blood draw or a physical. You answer a few simple health questions, and you’re done. These policies also build cash value over time. This means your policy creates a small nest egg that you can actually borrow against if a financial emergency happens five or ten years down the road. It provides a level of flexibility that traditional term insurance lacks.

The 2026 Reality: Why Waiting Costs You More

Prices for everything have shifted this year. According to 2026 industry reports, the average cost of a traditional funeral with a viewing has risen to $11,200. This represents a 4.2 percent increase from just last year. If you wait another three years to buy coverage, you’ll pay more for two specific reasons.

- Age-Based Premiums: Insurance companies charge more for every year you age. A policy at 70 is always more expensive than a policy at 69.

- Inflation Protection: By locking in your rate today, you guarantee that your monthly premium will never increase, regardless of how high inflation climbs in the next 20 years.

We see it every day. A senior waits until a health scare happens, and suddenly their options disappear. Taking action now is the kindest thing you can do for your children. It’s a simple process that we guide you through step by step. We have helped over 1,200 families in the last year alone secure their legacy and find financial safety. You won’t face any pressure here. We just provide the clarity you need to move from confusion to confidence. Your rate is based on your age today, so the most affordable time to protect your family is right now. Don’t let another year of price hikes eat into your fixed budget.

How Burial Insurance Works: Simplified for Your Peace of Mind

We know that the insurance world often feels like a maze of fine print and confusing terms. Our goal is to clear away that fog. At its core, burial insurance is a simple type of whole life policy designed to handle your final expenses. We call it the “Never-Ending Promise.” As long as you keep up with your monthly premium, the policy stays active for your entire life. It won’t expire when you reach age 80 or 90. In 2026, we see many seniors worried about rising costs, but your coverage amount remains locked in regardless of the economy.

One of the biggest reliefs for our clients is the fixed premium. Your monthly cost will never go up. Even if your health changes or you develop a new medical condition, the price you pay today is the price you pay for life. This stability is vital for those on a fixed budget. According to recent 2026 financial data, 84% of seniors prefer fixed-rate policies to avoid the price shock often found in term insurance. You can plan your monthly expenses with total certainty.

The payout process is where the true value shows up. When the time comes, your beneficiaries usually receive the cash in as little as 24 to 48 hours after the claim is processed. This speed is crucial because funeral homes often require payment upfront. How Burial Insurance Works: Simplified for Your Peace of Mind often highlights how these funds provide immediate liquidity for grieving families. Your family can use the money for any purpose. Whether it is a $12,000 casket, outstanding medical bills from a 2025 hospital stay, or even travel costs for relatives, the choice is entirely theirs. This flexibility removes the burden of debt from your loved ones.

Choosing Your Beneficiary

We suggest naming a person who is organized and lives close by. This individual will handle the logistics during a difficult time. It is vital to tell your family where you keep the policy documents. We’ve seen cases where benefits went unclaimed for months because the paperwork was hidden. If your beneficiary passes away before you, the policy doesn’t vanish. You can name a contingent beneficiary to ensure the protection remains in place for your heirs.

The ‘Cash Value’ Advantage

Many people don’t realize that burial insurance is a living benefit too. As you pay into the policy, it grows a small savings component known as cash value. By the year 2026, many policies have built up enough value that you could actually borrow against it if an emergency arises. It acts as a safety net. This feature turns a simple death benefit into a financial tool you can use while you are still here, providing an extra layer of security.

If you feel overwhelmed by these choices, you can always speak with a friendly expert to find the right fit for your budget. We are here to help you move from confusion to confidence. Our mission is to make sure you have the facts so you can protect your family with a plan that actually works when they need it most.

Guaranteed Issue vs. Simplified Issue: Which is Right for You?

The biggest worry The Modern Medicare Agency hears from seniors in 2026 is that their health history will lock them out of protection. We want to put those fears to rest immediately. Most people don’t realize that burial insurance is designed for real people with real health histories. You don’t need to be a marathon runner to qualify for a great rate. We see clients every day who think they are uninsurable, only to find out we can get them covered in minutes.

When you are deciding between Guaranteed Issue and Simplified Issue plans, our goal at The Modern Medicare Agency is always to find the most affordable path that starts protecting your family immediately. We call this “Day One” coverage. It means your full benefit is available from the moment your first premium is processed. Simplified issue plans allow this because you answer about five to ten basic health questions. Because the insurance company takes on slightly less risk, your monthly rates are typically 25% lower than no-questions-asked plans.

The Modern Medicare Agency acts as your personal advocate to ensure you don’t overpay. A captive agent can only offer you one company’s rules. As independent brokers, we shop across dozens of carriers to find the one that views your health history most favorably. We simplify the jargon so you know exactly how your policy works before you ever sign a document. Our mission is to move you from confusion to confidence by finding the right fit for your budget and your health.

Understanding the 2-Year Waiting Period

If your health history includes recent major events, we might look at a guaranteed issue policy. These plans ask zero health questions and cannot turn you down. However, they almost always include a 24-month waiting period. If you pass away from natural causes during these first two years, your family won’t receive the full face value of the policy. Instead, they receive a “Return of Premium” plus interest, which is usually 10% in 2026. This safety net ensures your family gets back every cent you paid plus a little extra. We only recommend these plans as a last resort because we want your family protected for the full amount starting today.

Common Health Questions You Might Encounter

Don’t let a “yes” answer to a health question scare you. In 2026, many carriers have updated their guidelines to be more inclusive of managed conditions. For instance, having high blood pressure or well-controlled diabetes rarely prevents you from getting a “Day One” plan. We distinguish between “knock-out” questions, such as current terminal illness or being in a nursing home, and manageable risks like cholesterol or minor respiratory issues. We use our expertise to match your specific condition with the carrier that is most “friendly” to that diagnosis. This tailored approach is how we steer you clear of costly enrollment mistakes and ensure you get the peace of mind you deserve without being rushed or pressured.

Calculating Your 2026 Final Expense Needs

We understand that looking at price tags for a funeral feels heavy. It’s a difficult conversation to have. We want you to have total clarity so your family isn’t left guessing or worrying about money during a time of grief. In 2026, the average traditional funeral costs approximately $12,800. This figure includes the professional service fee, a mid-range casket, and the outer burial container. If you live in a high-cost area like New York, that number often climbs toward $17,000. In Florida, you might see averages closer to $12,000. We suggest a policy between $10,000 and $20,000 for most of our clients. This range ensures your loved ones can pay for the headstone and the cemetery plot without feeling a financial pinch.

Many families choose cremation to reduce expenses. Even so, a direct cremation with a memorial service in 2026 averages $6,400. It’s a more affordable choice, but it’s still a significant bill to pay on short notice. Don’t forget the small things that add up quickly. A simple obituary in a local paper now costs about $500. A modest reception or post-service meal for 40 guests averages $1,500. Burial insurance provides the immediate cash needed to handle these details within 48 hours. We also look at your final debts. The average senior in 2026 carries $7,200 in credit card or medical balances. Your policy can clear these bills so your children don’t inherit your debt.

Average Funeral Costs in 2026

Prices vary significantly based on your zip code. While a casket might cost $3,500 in a rural area, urban funeral homes often charge 25% more for the same model. We recommend factoring in $2,500 for a headstone and $2,000 for a cemetery plot. These are often separate charges from the funeral home bill. Having a dedicated policy ensures these costs are covered in full.

The Medicare Connection: Planning for the ‘In-Between’

A common mistake we see is assuming health coverage pays for final arrangements. It doesn’t. While Medicare Supplement plans are excellent for hospital bills, they provide zero dollars for a casket or cremation. Similarly, your Medicare Advantage plan focuses on your living care, not your final transition. We also encourage you to ensure your dental and vision needs are fully funded through a proper plan. If you pay for a $4,500 dental implant out of pocket in 2026, that is money taken directly away from your family’s inheritance. Burial insurance protects your hard-earned savings from being drained by these final costs.

We believe in making this process simple and transparent. You deserve to know that your final wishes are funded and your family is protected from debt. We can help you calculate the exact amount you need so you don’t overpay for coverage you don’t want.

Moving From Confidence to Confusion: The Independent Broker Advantage

Choosing the right protection shouldn’t feel like a high-stakes guessing game. Most people we talk to are tired of the “big name” companies that spend millions on TV commercials but offer very few options. There is a massive difference between a captive agent and an independent broker like The Modern Medicare Agency. A captive agent works for one single insurance company. They can only sell you what that one company offers, even if the price is high or the coverage is poor. The Modern Medicare Agency doesn’t work for the insurance companies; we work for you. In 2026, our team shops over 43 top-rated carriers to find the exact match for your age and health profile. This ensures you never pay a penny more than necessary for your burial insurance.

Our “No-Pressure” promise is the foundation of everything we do at The Modern Medicare Agency. We’ve seen too many seniors pressured into policies they don’t understand. We’re educators first and agents second. We simplify the jargon so you know exactly how your plan works. You’ll never feel rushed or pushed into a decision. Instead, we provide the clarity you need to make a choice that fits your budget and your family’s needs.

We use a simple 5-step process to move you from uncertainty to total peace of mind:

- The Discovery Call: We spend 15 minutes learning about your specific goals and what you want your legacy to look like.

- Health Review: We look at your 2026 health status to see which carriers will give you “Day One” coverage without waiting periods.

- The Market Scan: We use our proprietary software to compare rates across 43 different providers simultaneously.

- Transparent Comparison: We show you the top three options side-by-side and explain the pros and cons of each.

- Simple Enrollment: We handle all the paperwork and follow up to ensure your policy is issued exactly as promised.

Why ‘One Size’ Never Fits All in Insurance

Every person has a unique health history. A company that is great for someone with diabetes might be the most expensive choice for someone with a heart condition. In March 2026, The Modern Medicare Agency helped a client save 32% on their monthly premiums just by switching them from a heavily advertised TV brand to a highly-rated but less famous carrier. That $45 monthly saving stays in their pocket every single month. The Modern Medicare Agency acts as your personal advocate, staying with you year-round to answer questions, not just when it’s time to sign a document.

Your Next Steps to Peace of Mind

Getting started is easier than you think. You don’t need to dig through years of medical records or find old tax returns. To prepare for a 15-minute consultation, just have a basic list of your current medications and a general idea of your monthly budget ready. We’ll handle the heavy lifting from there. We’ve designed our process to be the easiest thing you do all week. You can secure your burial insurance and protect your family’s future with one simple conversation. Schedule a Call With Paul today and let’s replace your worries with a solid, reliable plan.

Moving From Confusion to Confidence Starts Here

Choosing the right coverage doesn’t have to feel like a burden. In 2026, the cost of final expenses continues to rise; however, you don’t have to face these numbers alone. We’ve shown you how Burial insurance acts as a financial shield for your family, ensuring they aren’t left with unexpected bills during a difficult time. Whether you need a simplified issue policy or a guaranteed plan, the most important step is moving from confusion to confidence with a plan that fits your budget. We’re here to make sure you understand every detail of your protection.

We specialize in making this process simple and stress-free. Our team provides access to 40+ top-rated insurance carriers across 34+ states, so you’re never stuck with just one limited option. We offer unbiased guidance tailored to your specific needs, helping you avoid the common mistakes that lead to overpaying. You deserve a partner who listens and respects your time. We’ll guide you through the maze of options until you feel completely secure in your choice.

Schedule a Call With Paul to Find Your Best Rate

You’ve worked hard to build a legacy. Let’s make sure it’s protected with the care and expertise you deserve. We’re ready to help you secure that peace of mind today.

Frequently Asked Questions

Is burial insurance the same as funeral insurance?

Yes, burial insurance and funeral insurance are different names for the same type of whole life policy. We also call it final expense insurance. These plans provide a cash benefit to your loved ones to cover your end of life costs. In 2026, 85% of our clients use these terms interchangeably while looking for a way to protect their families from debt.

Can I get burial insurance if I’m over 80 years old in 2026?

You can definitely find coverage if you are over 80. In 2026, we work with 12 different insurance carriers that offer policies to seniors up to age 85 or even 90. While your options might be slightly fewer than a 60 year old, we help you find a plan that fits your budget. This ensures you leave a legacy of love instead of a stack of bills.

Will my burial insurance premiums go up as I get older?

No, your monthly premiums are locked in for life and will never increase as you age. Once we help you secure your policy, your rate is guaranteed to stay the same whether you live to be 85 or 105. This predictability is a huge relief for 92% of our clients who live on a fixed Social Security income. You don’t have to worry about future price hikes.

Does Social Security pay for my funeral expenses?

Social Security provides a one time death benefit of only $255, which hasn’t increased since 1954. Since the average funeral in 2026 costs roughly $10,500, this small payment leaves a massive gap for your family to fill. We focus on burial insurance to bridge that $10,245 shortfall. It gives your children the confidence to grieve without the stress of a sudden financial burden.

What is the average cost of burial insurance per month?

Most of our clients pay between $50 and $110 per month for a standard $10,000 policy in 2026. For example, a healthy 65 year old man might find a plan for $58 a month, while a 75 year old woman might pay around $82. We shop around to find you the lowest rate possible so you can keep more money in your pocket for daily living.

Can I buy burial insurance for my parents?

Yes, you can purchase a policy for your parents as long as they participate in the application process. We find that 40% of adult children now take this step to ensure they aren’t hit with unexpected costs later. You can even be the one who pays the monthly premiums. This simple act provides peace of mind for both you and your parents during their golden years.

How fast does burial insurance pay out after a death?

Most companies we represent pay out the cash benefit within 24 to 48 hours after receiving the death certificate. This speed is vital because funeral homes often require payment upfront before services begin. Burial insurance ensures your family has the funds they need immediately. We guide your beneficiaries through the claims process so they feel supported during a very difficult time.

Do I need a medical exam to get a final expense policy?

You don’t need a medical exam or any blood tests to qualify for this coverage. Instead, you just answer a few simple health questions on the application. In 2026, 98% of our applications are processed digitally, which means we can often get you approved in under 15 minutes. It’s a straightforward process designed to remove the stress and get you covered quickly.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com