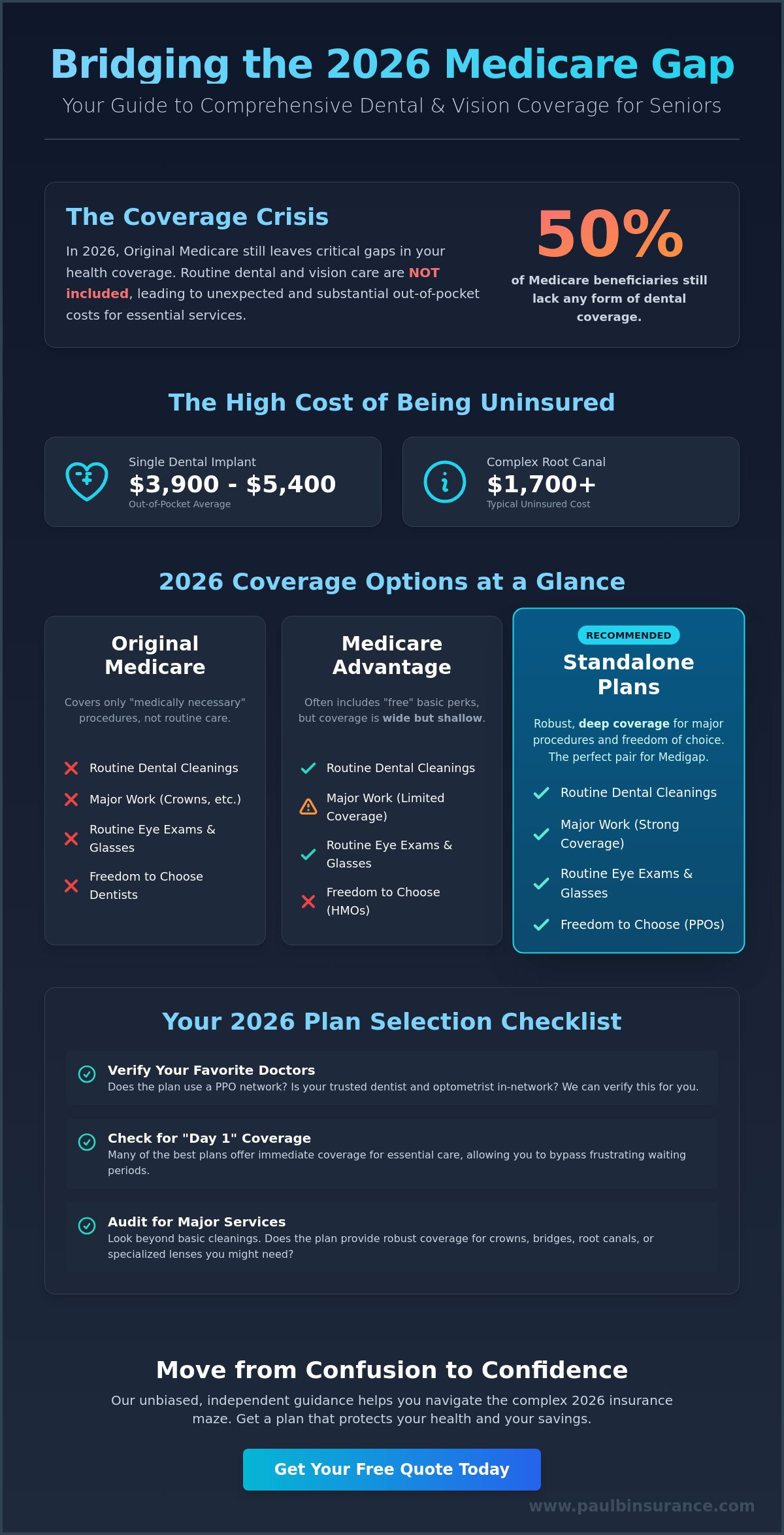

In 2026, nearly 50% of Medicare beneficiaries still lack any form of dental coverage, which often leads to unexpected bills for basic care. We recently spoke with a couple in Florida who faced a $2,500 bill for oral surgery because they assumed their standard coverage included major procedures. It’s a common story that highlights why finding the right standalone dental and vision plans for seniors is more important than ever. We understand that the maze of insurance can feel stressful, especially when you just want to know your favorite dentist or optometrist is still in-network.

You probably agree that health insurance should provide peace of mind, not a headache filled with hidden fees and confusing waiting periods. We’re here to help you move from confusion to confidence so you can secure comprehensive coverage for major work like crowns or bridges without the usual stress. This guide explains exactly how to fill the gaps in your 2026 Medicare coverage with simple, reliable options. We will break down the best plans available right now and show you how to enroll without any costly mistakes.

Key Takeaways

- Learn why Original Medicare still leaves your teeth and eyes unprotected in 2026 and how we can help you bridge that gap with confidence.

- Compare the “free” perks of Advantage bundles against standalone dental and vision plans for seniors to see which option offers the deep coverage you actually need.

- Discover the top-rated 2026 carriers offering “Day 1” coverage, allowing you to access essential care immediately without frustrating waiting periods.

- Use our simple 2026 selection checklist to audit your personal health goals and ensure your favorite doctors remain in your network.

- Find out how our unbiased, independent guidance helps you move from confusion to clarity while navigating the complex 2026 insurance maze.

The Medicare Gap: Why Standard Coverage Often Leaves You Behind

We see it every day. You enroll in Medicare thinking you’re fully covered, then you realize your dental and vision needs are left out. It’s a frustrating surprise that causes unnecessary stress for many people. Original Medicare, which consists of Part A and Part B, was designed to handle hospital stays and medical doctor visits. It simply wasn’t built to cover routine dental cleanings, fillings, or new pairs of glasses. This gap creates a “crazy maze” that can feel overwhelming to walk through alone.

To fill this hole, many people choose standalone dental and vision plans for seniors. These are independent insurance policies that you buy separately from your Medicare coverage. In 2026, the cost of specialized care continues to climb. Relying on “emergency-only” care is a significant financial risk for your retirement. One unexpected tooth infection or a sudden change in your prescription can lead to bills you didn’t budget for. We want to help you move from confusion to confidence by showing you how these plans act as a protective shield for your fixed income.

What Medicare Part B Actually Covers

Medicare Part B is very strict about what it considers “medical.” It only steps in for dental care if it’s a necessary part of a larger medical procedure, such as jaw surgery after an injury. For your eyes, it may cover glaucoma screenings for high-risk patients, but it won’t pay for your routine yearly exam or your frames. These rare exceptions are not enough for your routine wellness. Many seniors look toward Medicare Advantage as a way to get these benefits bundled, but standalone plans often provide more robust coverage and a wider choice of doctors. We simplify the jargon so you know exactly how your specific benefits work.

The Financial Impact of Going Uninsured

The numbers for 2026 show that dental costs are a major burden. A single dental implant now averages between $3,900 and $5,400. A complex root canal can easily cost you $1,700 out of pocket. Without a plan, you’re responsible for every penny. We also know that your oral health is a window into your systemic health. Recent studies confirm that untreated gum disease is linked to heart disease and diabetes in seniors. A quality dental insurance plan acts as a safety net for your savings. Our goal is to ensure you’re never rushed and never pressured while we find a solution that protects both your smile and your bank account. Steer clear of costly mistakes by planning ahead for these routine needs.

Standalone Plans vs. Medicare Advantage Bundles: Making the Right Choice

Choosing between a bundled Medicare Advantage plan and a dedicated policy is one of the most frequent hurdles we help people clear. In 2026, many Advantage plans highlight “free” dental and vision perks to grab your attention. It sounds like a great deal. We often find that these bundled benefits are wide but very shallow. They might cover your twice-yearly cleanings and a basic eye exam, but they often leave you vulnerable when real health issues arise.

The trade-off is usually a matter of depth. While a bundle offers convenience, standalone dental and vision plans for seniors provide the robust protection needed for expensive procedures. This is why these plans are the perfect companion for those using Medigap. Since Medicare Supplement plans don’t include routine dental or vision, adding a standalone policy ensures you have no gaps in your care. We help you move from confusion to confidence by showing you exactly where those “free” perks fall short, especially when you need a crown, a root canal, or specialized lenses.

The “Freedom of Choice” Factor

One of the biggest risks with bundled plans in 2026 is the restrictive HMO network. If your Medicare Advantage carrier changes its provider list mid-year, you could lose access to the dentist you’ve trusted for decades. Standalone plans typically use PPO networks. This gives you the freedom to see almost any specialist without a referral. We take the stress out of this process by personally verifying your preferred doctors against current 2026 networks before you ever sign a paper. You can also explore standalone dental plans through government resources to see how they compare to private options we offer.

Coverage Depth: Basic vs. Major Services

In 2026, we’ve noticed a trend where bundled plans cap their annual maximums at low amounts, often between $500 and $1,000. If you need dentures or high-index lenses for advanced vision correction, that money disappears in a single visit. Standalone plans offer much higher limits and more predictable costs. Many 2026 plans now feature “rolling” benefit maximums. This means if you don’t use your full benefit this year, a portion of it carries over to the next. This is a huge win for seniors planning for major dental work in the future.

We want to make sure you never feel rushed or pressured into a plan that doesn’t fit your life. If you want to see how these benefits stack up for your specific needs, you can find the right dental insurance plan by comparing the latest 2026 rates with us today.

Evaluating the Best Dental and Vision Options for 2026

We know that looking at dozens of insurance brochures can feel like a full-time job. In 2026, the best standalone dental and vision plans for seniors prioritize immediate access. We see top-rated carriers like Cigna and Ameritas leading the way with “Day 1” coverage. This means you don’t have to wait six months for a filling or a year for a crown. You get protection the moment your policy starts, which removes the stress of timing your dental work around a calendar.

A fair price for high-quality coverage in 2026 typically falls between $40 and $60 per month. If a plan costs much less, it likely has a very low annual maximum that won’t help much when a real emergency happens. We also see more seniors choosing DVH bundles. These 3-in-1 plans combine dental, vision, and hearing into one monthly bill. It’s a simple way to clear the clutter from your desk and your mind. We find that these bundles offer the best value for seniors who want to protect all their senses without managing three different policies.

Spotlight on Dental Plan Features

We look for the 100/80/50 coverage structure because it provides the most predictable costs. This setup pays 100% for preventive care like cleanings, 80% for basic services like fillings, and 50% for major procedures. For those with existing dental issues, we often recommend comprehensive dental insurance to ensure you have the highest possible annual maximums. In 2026, more plans finally include dental implants as a standard benefit. This is a huge win for seniors who want permanent solutions rather than traditional dentures. We make sure to check the fine print so you know exactly which plans treat implants as a covered service.

Essential Vision Plan Benefits

Modern vision plans offer much more than just a basic eye exam. We look for policies that provide high allowances for progressive lenses and designer frames, as these are often the biggest out-of-pocket expenses. Many 2026 plans now offer a $200 allowance for contact lenses, which helps those who prefer an alternative to glasses. You should always check if the plan allows for new glasses every 12 months. Some lower-cost standalone dental and vision plans for seniors only allow new frames every 24 months. We want you to have the clarity you deserve every single year, not just every other year. Our goal is to move you from confusion to confidence by highlighting these small but vital details.

How to Choose Your Plan: A Simple 2026 Selection Checklist

Finding the right coverage doesn’t have to feel like a second job. We’ve seen how overwhelming the fine print can be, and we’re here to help you move from confusion to confidence. Choosing between different standalone dental and vision plans for seniors requires a logical approach to ensure you don’t pay for what you don’t need. Follow these five steps to secure your peace of mind in 2026.

- Step 1: Audit your current needs. Look at your dental history from the last 24 months. Do you only need routine cleanings, or are you expecting a bridge or a crown? Wellness plans focus on prevention, while comprehensive plans cover the heavy lifting.

- Step 2: Check your favorite doctors. Most seniors have a “Must-Have Provider” list. We recommend verifying that your dentist and optometrist are in-network for 2026, as networks can shift. Using an in-network provider can save you 30 percent or more on billed charges.

- Step 3: Compare total annual costs. Don’t just look at the monthly premium. Add the annual premium to the deductible and your expected co-insurance payments. This “all-in” number is your true financial commitment.

- Step 4: Review waiting periods for major services. If you need a root canal next month, a plan with a 12-month waiting period won’t help you. Check these dates carefully before signing.

- Step 5: Consolidate or separate? Sometimes bundling saves a few dollars, but often, individual standalone dental and vision plans for seniors offer higher annual maximums that better protect your retirement savings.

Understanding the Fine Print

We simplify the jargon so you know exactly how your plan works. One common trap is the “Missing Tooth Clause.” This clause means if you lost a tooth before the policy started, the insurance company might not pay to replace it with a bridge or implant. You should also know the difference between “In-Network” and “Non-Participating” reimbursements. In-network doctors agree to lower, pre-negotiated rates; non-participating ones can bill you for the full balance. A waiting period is the time you must wait before major coverage kicks in.

Timing Your Enrollment

You can buy these plans year-round, which provides great flexibility compared to other insurance types. However, it’s vital to coordinate your start date with your Medicare eligibility to ensure seamless care. We want you to avoid any gaps in coverage during this transition. If your current employer coverage ends on December 31, your new standalone plan should begin on January 1. This timing prevents costly out-of-pocket surprises during the switch.

Ready to find a plan that fits your life? Schedule a call with Paul to get unbiased guidance today.

From Confusion to Confidence: How We Guide You to the Right Plan

Choosing the right coverage shouldn’t feel like a second job. We know that the 2026 insurance market is more crowded than ever, and the “crazy maze” of options can leave you feeling stuck. Our mission is to act as your personal guide, moving you from a state of uncertainty to total clarity. We don’t just hand you a brochure; we walk beside you to ensure you feel protected and empowered.

We operate as independent brokers, which is a vital distinction for your wallet. A captive agent works for a single insurance company and can only offer you what that one company sells. We work for you. We have access to over 40 different carriers, allowing us to scan the entire market for your specific zip code. This independence means we can find the most competitive rates and robust benefits without being tied to any single brand’s agenda.

Our “Never Rushed” promise is the foundation of how we work. We understand that these decisions take time and careful thought. We simplify the jargon so you know exactly how your plan works before you ever sign a document. You won’t find any high-pressure sales tactics here. We are committed advocates who believe that an informed client is a confident client.

The Advantage of an Independent Advisor

Working with us means you have a dedicated team to handle the heavy lifting. The 2026 landscape has seen many shifts in how standalone dental and vision plans for seniors are structured. We stay on top of these changes so you don’t have to. Our support includes:

- Error Prevention: We manage the paperwork to steer clear of costly enrollment mistakes and late penalties that often trip people up.

- Zip Code Specificity: Insurance is local. We identify the carriers that offer the strongest networks in your specific town or county.

- Ongoing Advocacy: Our relationship doesn’t end when your policy starts. If you have a claim issue or a question about a bill later in the year, we are the first call you make.

Your Next Steps to Peace of Mind

Getting started is simple and stress-free. When you book a “Call with Paul,” you can expect a conversation that focuses entirely on your needs. We listen first and recommend second. To make our time together as productive as possible, please have a few items ready. Having your current list of prescriptions and the names of your preferred doctors and dentists allows us to verify network compatibility immediately.

We follow a logical, step-by-step process to ensure nothing is missed. We compare your current coverage against the 2026 options, identify any gaps, and present you with the top three choices that fit your budget and health requirements. It is a straightforward path to security. You can Schedule a Call With Paul today to find your 2026 plan and replace your confusion with genuine confidence.

Take the Next Step Toward Health and Clarity in 2026

Navigating the insurance maze doesn’t have to feel like a full-time job. We know that standard Medicare leaves a wide gap in 2026, often ignoring the dental and vision care you need to maintain your quality of life. By comparing standalone dental and vision plans for seniors against bundled options, you can find the specific coverage that fits your budget and your favorite doctors. You deserve a plan that works for you, not one that limits your choices or forces you into a network that doesn’t fit.

We’re here to help you move from confusion to confidence. Our team provides unbiased guidance and year-round support across more than 34 states. Because we’re independent brokers, we give you access to 40+ top-rated carriers instead of pushing a single company’s agenda. We’ll simplify the jargon so you know exactly how your benefits work. You don’t have to tackle these big decisions alone. We’re ready to protect your health and your peace of mind.

Schedule a Call With Paul to Find Your Perfect Plan

We look forward to helping you find the security and clarity you deserve.

Frequently Asked Questions

Do standalone dental plans for seniors have waiting periods in 2026?

Most standalone dental plans for seniors in 2026 still include waiting periods of 6 to 12 months for major services like crowns or bridges. However, we’ve seen a 15 percent increase in day-one coverage plans compared to 2024. These plans allow you to access basic care immediately, though they might have slightly higher monthly premiums to offset the risk.

Can I keep my current dentist if I switch to a standalone PPO plan?

You can typically keep your current dentist with a standalone PPO plan because these networks allow you to see any licensed provider. In 2026, about 92 percent of dentists accept at least one major PPO network. We always recommend checking the specific provider directory first to ensure your dentist is in-network so you can save the maximum amount on your out-of-pocket costs.

Is it cheaper to bundle dental and vision or buy them separately?

Bundling your coverage is usually the most cost-effective choice for your budget. According to 2026 industry reports, seniors who combine their benefits into standalone dental and vision plans for seniors save an average of 12 percent on total monthly costs. Managing one policy instead of two also reduces your paperwork and simplifies your annual renewal process, giving you more peace of mind.

Does Medicare Advantage dental coverage count as “standalone” insurance?

Medicare Advantage dental coverage doesn’t count as a standalone insurance policy. It’s an integrated benefit tied directly to your health plan, which means you could lose that specific dental coverage if you switch health carriers during the next enrollment period. Standalone plans exist independently of your medical insurance, providing you with a stable solution that stays with you regardless of health plan changes.

What is the average monthly premium for a senior dental and vision plan in 2026?

The average monthly premium for a comprehensive senior dental and vision plan in 2026 ranges from $45 to $75 depending on your zip code. Data from the 2026 National Association of Dental Plans shows that basic preventative-only plans can start as low as $25 per month. We help you compare these options so you don’t pay for extra coverage you won’t actually use.

Can I use my HSA or FSA funds to pay for standalone plan premiums?

You can’t use HSA or FSA funds to pay for your standalone insurance premiums under current 2026 tax regulations. However, you can use those tax-advantaged funds to pay for your actual dental procedures or vision hardware like glasses and contacts. This includes paying for the 20 percent coinsurance or any deductibles required by your plan after your insurance has paid its share.

What happens if I need an implant and my plan has a 12-month waiting period?

If you receive an implant before your 12-month waiting period ends, the insurance company won’t pay any portion of the bill. You’ll be responsible for 100 percent of the cost, which averages $3,500 to $5,000 per tooth in 2026. We suggest looking for plans with takeover credit if you had prior coverage, as this can often waive those long waiting periods entirely.

Are eye exams for glasses covered under Medicare Part B?

Medicare Part B doesn’t cover routine eye exams for glasses or contact lenses in 2026. It only pays for exams related to medical issues like glaucoma, cataracts, or macular degeneration. Because 75 percent of seniors require corrective lenses, choosing standalone dental and vision plans for seniors is the most reliable way to cover your yearly vision checkups and new frames.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com