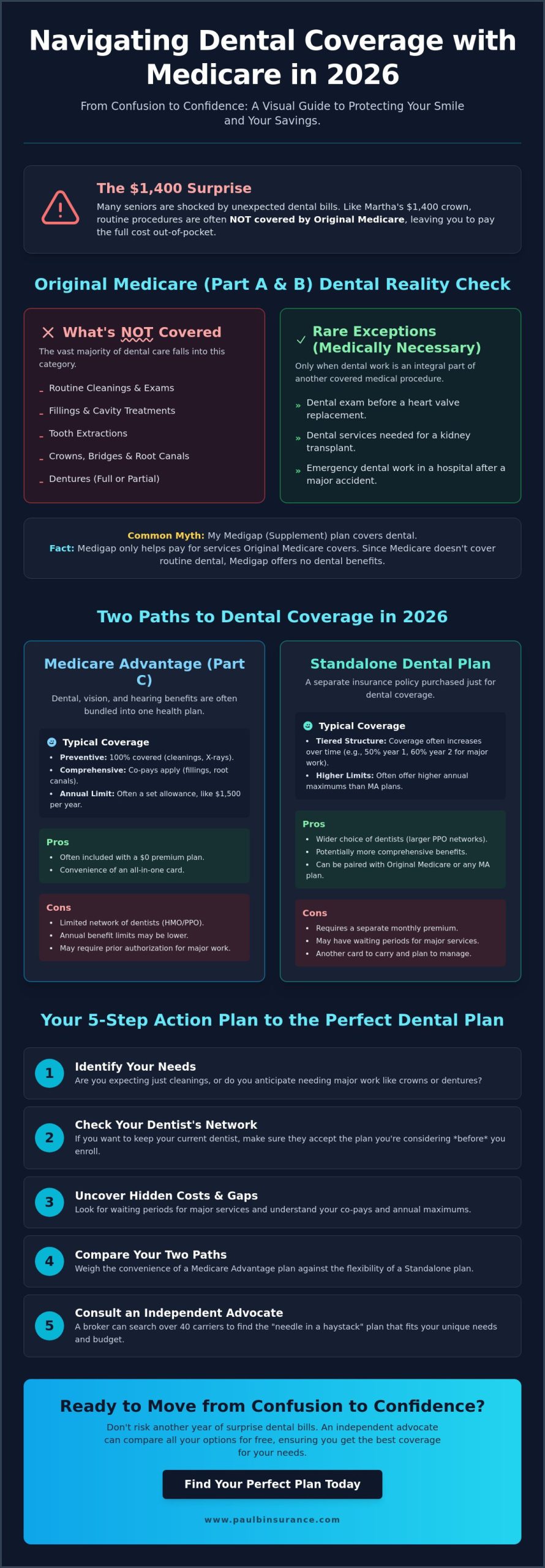

Last Tuesday, Martha sat at her kitchen table staring at a $1,400 bill for a single crown, shocked to find her basic coverage didn’t pay a cent. It’s a stressful reality for many as we enter 2026, where the gap between what you need and what Original Medicare provides feels wider than ever. We understand the frustration of trying to decode complex benefit booklets while fearing you’ll pick a plan your trusted dentist won’t even accept. You deserve a healthcare partner who simplifies the jargon and protects your peace of mind.

We promise to move you from confusion to confidence by showing you exactly how to find the right dental insurance plans for medicare recipients that offer predictable costs and reliable coverage. You don’t have to settle for surprise expenses or limited networks. This guide outlines the simple steps to compare 2026 Medicare Advantage dental benefits against standalone options so you can secure your smile without any expensive surprises. We’ll show you how to keep your preferred provider and make the enrollment process completely painless.

Key Takeaways

- Understand the 2026 reality of what Medicare excludes so you can protect your smile and your savings from unexpected out-of-pocket costs.

- Compare the pros and cons of bundled Medicare Advantage benefits versus standalone dental insurance plans for medicare recipients to find your perfect balance of flexibility and cost.

- Follow our simple 5-step process to identify your specific dental needs and ensure your trusted dentist remains in your 2026 network.

- Discover how an independent advocate can search over 40 different carriers to find the “needle in the haystack” plan that fits your unique budget.

- Learn how to move from confusion to confidence by identifying the hidden waiting periods and coverage gaps that often trip up seniors.

Does Medicare Cover Dental? The 2026 Reality Check

Trying to understand your benefits often feels like wandering through a maze. We know how overwhelming it is to realize that your red, white, and blue card might not cover your next cleaning. As we look at the landscape in 2026, many seniors still find themselves surprised by what is missing. To get started, it helps to understand What is Medicare? and what its limits are. Even now, Original Medicare (Part A and Part B) does not pay for routine dental care. This includes things like cleanings, fillings, or dentures. We see many people struggle because they assume these basics are covered; however, the reality is that the program remains focused on medical needs rather than oral health.

The gap between “routine” and “medical” is where the confusion starts. Routine dental covers the maintenance you need to keep your smile bright. Medically necessary dental is much narrower. It only applies when a dental issue is directly tied to a covered medical procedure. This distinction is vital because untreated oral issues can lead to serious complications. Research published in 2025 suggests that roughly 40 percent of seniors with chronic gum disease also face a higher risk of heart disease. We want to help you avoid these risks by finding the right dental insurance plans for medicare recipients so you can focus on enjoying your retirement.

The Rare Exceptions: When Medicare Part A/B Might Pay

There are very few times when the government steps in to help with dental costs. For example, if you need a heart valve replacement or a kidney transplant, Medicare might cover a dental exam to ensure there is no infection that could ruin the surgery. They also pay for emergency dental work if it requires a hospital stay after a serious accident. In 2026, the rule for medical necessity means the dental service must be an integral part of a covered medical procedure to qualify for payment.

Why Medigap Isn’t the Solution for Your Teeth

We often hear from clients who believe their Medicare Supplement (Medigap) plan will take care of their dentist bills. It’s a common misconception that popular options like Plan G or Plan N include dental benefits. These plans are designed to fill “gaps” in your medical billing, such as deductibles or coinsurance for things Medicare already covers. Since Medicare doesn’t cover routine dental, Medigap has nothing to supplement there. Relying on Medigap for your teeth often leads to costly surprises at the check-out desk. You need a separate, dedicated strategy to ensure your oral health is protected without breaking your budget. This is why exploring specific dental insurance plans for medicare recipients is the smartest path forward for your peace of mind.

How Medicare Advantage (Part C) Fills the Dental Gap

Original Medicare provides essential health coverage, but it leaves a hole where dental care should be. According to the official U.S. government source, Part A and Part B do not cover most routine dental services like cleanings or dentures. This is where private insurers step in. In 2026, many private companies use dental benefits as a major value-add to attract you to their Part C plans. These dental insurance plans for medicare recipients are built directly into the Medicare Advantage framework, making it easier to manage your health in one place.

We see many 2026 plans moving toward a simple allowance model. Instead of complex percentage charts, your plan might give you a set amount, such as a $1,500 annual limit, to spend on your teeth as you see fit. We help you look past the flashy marketing to see if that $1,500 actually covers your specific needs. It’s about moving from confusion to confidence so you aren’t surprised by a bill at the dentist’s office. If you are feeling stuck, you can view our dental guide to see how these allowances compare across different carriers.

Preventive vs. Comprehensive Coverage

Most 2026 plans split coverage into two buckets. Preventive care is usually covered at 100%. This includes your twice-yearly cleanings, routine X-rays, and basic exams. You shouldn’t pay a dime for these visits. Comprehensive coverage is for the bigger stuff. If you need a filling, a root canal, or dentures, you will likely have a co-pay. A common feature for 2026 is the prior authorization requirement for major work. This means your dentist must get the plan’s approval before starting a crown or bridge. We can help you check these rules before you sit in the chair.

The Pros and Cons of Advantage-Based Dental

- Pro: Most of these benefits come with a $0 additional monthly premium. You get the dental coverage as part of your standard Medicare Advantage plan.

- Con: You must stay within a specific network. If your favorite dentist isn’t in the plan’s HMO or PPO, you might pay the full price out of pocket.

Checking your network for 2026 is vital because provider lists change every year. We recommend calling your dentist’s office directly to ask if they still accept your specific 2026 plan. We want to make sure your dental insurance plans for medicare recipients actually work for you when you need them most. Our goal is to keep things simple so you can focus on your health, not the paperwork.

Standalone Dental Plans vs. Medicare Advantage: A 2026 Comparison

Choosing between a bundled benefit and a separate policy is often where the most stress happens. We see many seniors feel overwhelmed by these two paths. A Standalone Dental Plan is a dedicated policy you buy separately. In contrast, Medicare Advantage (Part C) rolls dental coverage into your health plan. According to an in-depth analysis by the Kaiser Family Foundation, traditional Medicare still lacks comprehensive dental coverage. This gap makes choosing the right path vital for your health and your budget in 2026.

One common worry we hear involves the waiting period for major work. While some standalone plans require six to twelve months of membership before covering crowns or implants, many 2026 providers now waive these if you had prior coverage. We help you find those specific options so you don’t have to delay necessary care. If you only need two cleanings a year, the dental included in an Advantage plan is a great value. However, if you anticipate needing a bridge or several root canals, the $1,000 to $1,500 annual limit on many Advantage plans will disappear quickly. Standalone dental insurance plans for medicare recipients often offer much higher limits, sometimes reaching $3,000 or even $5,000 annually.

When a Standalone Plan Makes More Sense

If you have a Medigap plan, you already enjoy the freedom to see any doctor who accepts Medicare. Pairing it with a standalone dental policy keeps that freedom intact. You can usually keep your private dentist because these plans often utilize large, nationwide PPO networks. This is the best route if you need high-limit coverage for complex procedures like implants. We find that clients who prioritize choice and have extensive dental needs feel more secure with a dedicated policy that isn’t tied to their health insurance network.

The “Bundled” Advantage: Convenience and Cost

Many of our clients prefer the simplicity of having one card for their health, drugs, and teeth. It removes the clutter from your wallet and simplifies your monthly billing. In 2026, the average monthly premium for a standalone dental plan ranges from $35 to $55, whereas many Advantage plans include basic dental for a $0 additional premium. You must weigh that cost saving against the plan’s medical out-of-pocket maximums. We guide you through this comparison to ensure you aren’t saving pennies on dental only to pay thousands more in medical costs. Our goal is to move you from confusion to confidence by showing you the math behind each option.

5 Steps to Choosing Your Perfect Dental Plan

Choosing between different dental insurance plans for medicare recipients often feels like wandering through a maze. We want to remove that stress and replace it with clarity. We’ve simplified the selection process into five logical steps to help you move from confusion to confidence for your 2026 coverage.

- Step 1: Audit your 2026 dental health. Are you looking for simple maintenance like cleanings and X-rays, or do you anticipate needing a $1,200 crown or a bridge? Knowing your expected level of care prevents you from overpaying for coverage you won’t use.

- Step 2: Verify your dentist’s network status. Networks shift every year. Call your provider and ask which specific 2026 insurance networks they participate in. A plan is only a “deal” if it includes the doctor you trust.

- Step 3: Choose your plan structure. You can get dental through a bundled Medicare Advantage plan or a standalone private policy. Standalone plans often provide higher coverage limits for major work.

- Step 4: Compare the Annual Maximum Benefit. This is the most money the plan will pay out in 2026. Compare at least three carriers; for example, one might offer a $1,500 limit while another offers $3,000 for a similar premium.

- Step 5: Hunt for the “Missing Tooth Clause.” Read the fine print carefully. Some plans won’t cover the replacement of a tooth that was lost before your policy started. We help you spot these traps so you aren’t surprised by a denied claim.

Evaluating the Network: PPO vs. HMO

We generally recommend PPO plans for our clients because they offer the flexibility seniors value. In a PPO, you can see any dentist you like, though you save more by staying in-network. HMO plans are often cheaper but restrict you to a very specific list of providers. In 2026, the risk of “balance billing” is real. If you see an out-of-network provider, they can bill you for the entire difference between their rate and what the insurance pays. Always use the most current 2026 provider directory to verify your dentist’s status before your appointment.

Understanding the Cost Sharing

Most dental insurance plans for medicare recipients follow the 100-80-50 rule. This means the plan pays 100% for preventive care, 80% for basic procedures like fillings, and 50% for major work like dentures. Don’t let a $50 deductible scare you away. It’s often the least important number in the policy. Focus instead on the waiting periods for major work, which can last 6 to 12 months. If your dentist prescribes antibiotics for an oral infection, remember that your Medicare Part D plan is what handles the cost of those medications at the pharmacy.

We are here to protect you from costly enrollment mistakes and ensure you have a plan that actually works when you’re in the dentist’s chair. Review your 2026 dental options with us today and get the peace of mind you deserve.

From Confusion to Confidence: Why an Independent Broker is Key

Choosing the right dental insurance plans for medicare recipients in 2026 can feel like trying to solve a puzzle with missing pieces. You might encounter a “captive agent” during your search. These agents work for one specific insurance company. Their goal is to sell you that company’s product, whether it’s the best fit for your life or not. We do things differently. As independent brokers, we don’t work for the insurance companies. We work for you.

We use our access to over 40 different carriers to find the needle in the haystack. Because we aren’t tied to a single brand, we can compare every available option to find the one that includes your specific dentist and covers the procedures you actually need. Our commitment doesn’t end when you sign up. We provide year-round support to answer your questions long after the enrollment period closes. Our “never rushed, never pressured” philosophy remains our core promise for 2026. We want you to feel empowered, not pushed.

We Simplify the Jargon

Insurance companies love 50-page benefit summaries filled with technical language. We take those documents and translate them into a simple “Yes” or “No” answer for your specific dentist. Our unbiased guidance helps you steer clear of enrollment mistakes and late penalties that can cost you hundreds of dollars. We use a proven 5-step process to move you from confusion to confidence:

- Listen: We learn about your specific dental history and 2026 health goals.

- Verify: We check if your current dentist is in-network for the plans we’re considering.

- Compare: We look at 40+ carriers to find the best value for your budget.

- Educate: We explain the differences in plain English so you understand your coverage.

- Enroll: We handle the paperwork and follow up to ensure everything is active.

Ready to Protect Your Smile?

You deserve to go into 2026 knowing your dental health is in good hands. We invite you to a personalized consultation where we can look at your options together. It’s important to remember that our services are at no cost to you. We’re here to be your advocate and your guide through the complex insurance system. If you’re ready to find the right dental insurance plans for medicare recipients, we’re ready to help. Schedule a Call With Paul to find your 2026 dental match and protect your smile for years to come.

Moving From Confusion to Dental Coverage Confidence in 2026

Navigating the 2026 Medicare landscape doesn’t have to feel like a maze. We’ve explored how Original Medicare still leaves gaps in your oral health care and why choosing between Medicare Advantage and standalone options requires a careful look at your specific needs. Finding the right dental insurance plans for medicare recipients is about more than just picking a name off a list. It’s about ensuring your favorite dentist is in-network and your monthly budget stays protected.

You don’t have to make these decisions alone. We provide unbiased guidance by comparing options from over 40 top-rated insurance carriers. Our team serves clients across 34 states with a personal touch that larger call centers simply can’t match. We’re here to simplify the jargon and help you avoid costly enrollment mistakes. We’ll take the time to listen to your concerns because your peace of mind is our priority.

Ready to see your options? Schedule a Call With Paul for a Free Dental Plan Comparison today. We’ll help you find the clarity you deserve so you can smile with confidence all year long.

Frequently Asked Questions

Does Medicare Plan G cover dental work in 2026?

No, Medicare Supplement Plan G doesn’t cover routine dental work like cleanings, fillings, or extractions in 2026. Because Plan G is designed to follow the rules of Original Medicare, it only pays for dental care if it’s an integral part of a covered medical procedure, such as jaw reconstruction after an accident. We help our clients find separate dental policies to ensure they have the protection they need for their everyday oral health.

Can I add dental insurance to Medicare at any time of the year?

You can purchase a standalone dental insurance policy at any time during the year without waiting for a specific enrollment window. While Medicare Advantage plans usually restrict changes to the Annual Enrollment Period starting October 15, private dental plans offer more flexibility. This means we can help you get covered today so you don’t have to worry about the cost of an unexpected toothache tomorrow.

What is the best dental insurance for seniors on Medicare who need implants?

The best dental insurance plans for medicare recipients needing implants are those that offer high annual maximums of $3,000 or more in 2026. Since a single implant often costs between $3,500 and $5,000, you want a plan that categorizes implants as a major service with at least 50% coverage. We look for specific plans that have eliminated the standard 12 month waiting period for these major procedures.

Do Medicare Advantage plans cover dentures?

Yes, approximately 97% of Medicare Advantage plans in 2026 offer some level of dental coverage which often includes dentures. Most plans classify dentures as a major restorative service, typically covering about 50% of the cost after you meet your deductible. We’ll review the summary of benefits with you to see if there are specific limits on how often you can replace your dentures, which is usually once every five years.

Are there waiting periods for dental insurance if I am already on Medicare?

Many traditional plans still have waiting periods of 6 to 12 months for major work, but 2026 has seen a rise in “no-wait” options for seniors. If you’ve had continuous dental coverage for the last 12 months, we can often find a plan that waives these waiting periods entirely. This allows you to schedule your crowns or root canals immediately after your new policy begins, providing you with instant peace of mind.

How much does dental insurance for Medicare recipients typically cost in 2026?

In 2026, monthly premiums for standalone dental insurance generally range from $25 for basic preventive plans to $65 for premium comprehensive coverage. Many of our clients find that the mid-range plans, costing about $45 per month, provide the best balance of affordable premiums and low copayments. We’ll help you compare these monthly costs against the potential price of paying for cleanings and fillings entirely out of your own pocket.

Can I keep my current dentist if I switch to a Medicare Advantage plan with dental?

It depends on whether your dentist participates in the specific PPO or HMO network of the plan you choose. While many dentists accept 2026 PPO plans, some smaller practices don’t participate in Medicare Advantage networks at all. We’ll personally check the provider directory for you or call your dentist’s office directly to confirm they are in-network so you can keep the doctor you already trust.

What happens if I need an emergency tooth extraction?

If you need an emergency extraction, most dental insurance plans for medicare recipients will cover between 50% and 80% of the cost. Original Medicare typically won’t pay for this unless the extraction is required for a covered medical surgery, like a heart transplant or radiation treatment. Having a private plan ensures that a sudden dental emergency doesn’t force you to choose between your health and your savings account.