Last Tuesday, a client named Sarah called us, her voice trembling as she looked at her new Social Security statement. She was terrified that the updated medicare part b premium 2026 would swallow her entire cost-of-living adjustment before she could even pay for her weekly groceries. We know that feeling of opening a government notice and feeling like the goalposts just moved again. It’s exhausting to worry that inflation is moving faster than your benefits, especially when the rules seem to change every January.

We’re here to protect your peace of mind by breaking down exactly what you’ll pay this year without the typical industry jargon. We promise to provide the clear dollar amounts for the 2026 premiums and the specific income brackets that trigger those frustrating IRMAA surcharges based on your 2024 tax returns. You’ll gain a complete understanding of your deductibles and monthly costs so you can plan your year with absolute confidence. This guide walks you through every financial change coming your way, ensuring you stay ahead of the curve and keep your retirement budget on track.

Key Takeaways

- Get the official breakdown of the medicare part b premium 2026 and the new annual deductible so you can budget for the year with total peace of mind.

- Understand how your 2024 tax returns impact your current costs through IRMAA surcharges and learn what steps you can take if your income has since changed.

- We clarify the relationship between this year’s Social Security COLA and your Medicare bill, ensuring you know exactly how your net check is protected by the “Hold Harmless” rule.

- Discover how to use Medicare Advantage “give-back” benefits or Medigap plans to effectively lower or cover your Part B out-of-pocket expenses.

- Learn why having an unbiased partner makes navigating the 2026 landscape simple, moving you from a place of confusion to absolute confidence.

Official 2026 Medicare Part B Premium and Deductible

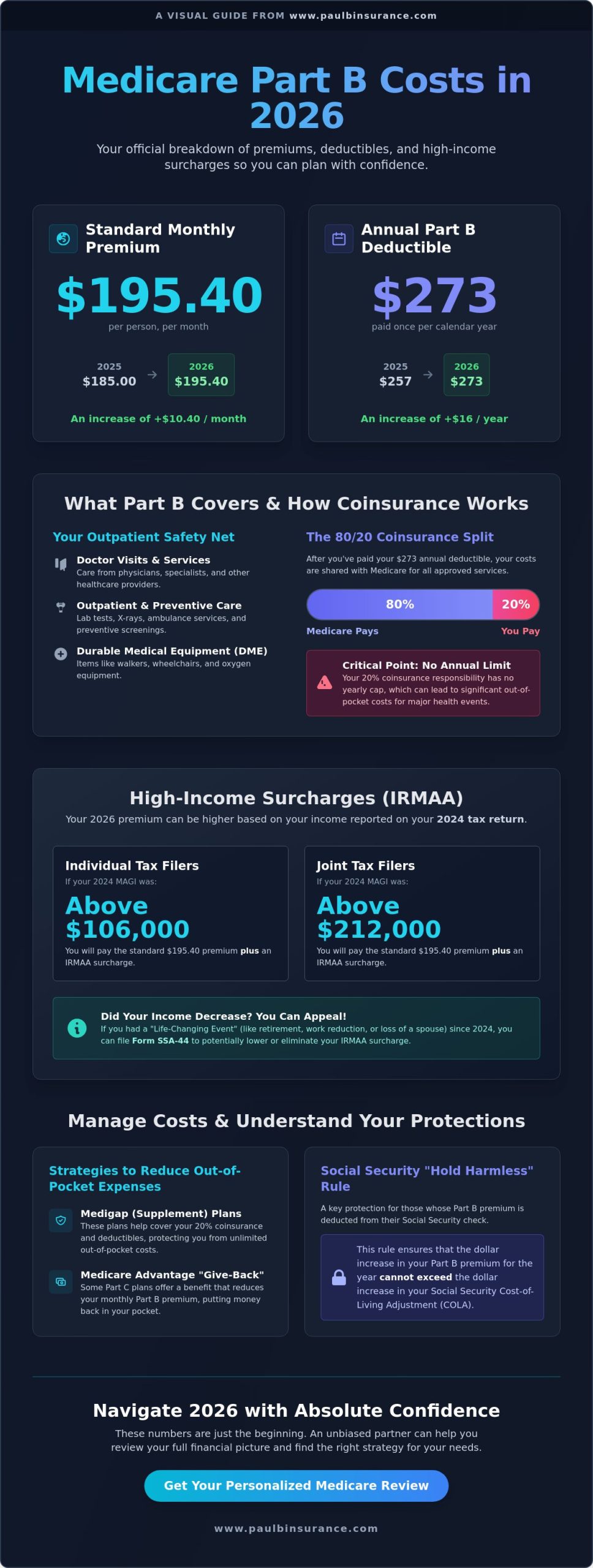

We know that seeing a change in your monthly costs can feel a bit unsettling. It’s our goal to make sure you have the facts so you can plan your budget with confidence. For 2026, the standard medicare part b premium 2026 is $195.40 per month. This represents a $10.40 increase from the $185.00 monthly rate beneficiaries paid in 2025. While any increase can feel like a burden, we are here to help you move from confusion to confidence by explaining exactly why these numbers change.

Along with the monthly premium, the annual Part B deductible has moved to $273 for the 2026 calendar year. This is a $16 increase over the 2025 deductible of $257. The federal government adjusts these costs every year based on the actual spending within the healthcare system. When the cost of technology, doctor services, and outpatient care goes up, the premiums and deductibles are adjusted to ensure the program stays stable. We recommend looking at this Overview of the Medicare Program to see how these financial pieces support the broader system of care for millions of Americans.

What Does Your Part B Premium Cover?

Think of Part B as your outpatient safety net. It covers essential services like doctor visits, lab tests, and durable medical equipment. Once you pay your $273 deductible, Medicare follows an 80/20 coinsurance split. This means Medicare pays 80 percent of the approved cost, and you are responsible for the remaining 20 percent. Because that 20 percent has no cap, many of our clients choose to look into Medigap plans to help cover those out of pocket costs. We also want to remind you that Part B is mandatory for most people. If you don’t sign up when you’re first eligible, you could face lifelong late-enrollment penalties. We want to help you steer clear of costly enrollment mistakes so your future is protected.

Who Pays the Standard 2026 Premium?

Most beneficiaries, roughly 92 percent of the people we serve, will pay the standard medicare part b premium 2026 of $195.40. If you are already collecting Social Security benefits, this payment is handled through an automatic deduction from your monthly check. It’s a simple process that ensures you never miss a payment. If you haven’t started collecting Social Security yet, you’ll receive a bill from Medicare every three months. We can guide you through setting up Medicare Easy Pay so your premiums are handled automatically from your bank account. Our mission is to simplify the jargon so you know exactly how it works, leaving you with one less thing to worry about.

Understanding IRMAA: High-Income Adjustments for 2026

We know that opening a letter from Social Security can sometimes feel like a cause for concern, especially when it mentions extra costs you weren’t expecting. If your income is above a specific limit, you might notice a surcharge on your monthly bill. This is known as the Income-Related Monthly Adjustment Amount, or IRMAA. It’s not a penalty for doing well; it’s simply a way the government adjusts the medicare part b premium 2026 based on your ability to contribute to the program. We’re here to help you understand exactly how these numbers are reached so you can plan your retirement budget with total confidence.

The 2026 IRMAA Brackets Explained

To determine your costs for this year, the Social Security Administration uses a two-year look-back rule to verify your earnings from your 2024 tax returns. There are five distinct tiers of income adjustments that can increase what you pay each month. If your modified adjusted gross income from two years ago exceeds $106,000 as an individual or $212,000 for those filing jointly, you’ll likely see an added charge on your statement. You can view a detailed breakdown of the IRMAA High-Income Adjustments for 2026 to see which tier applies to your specific financial situation.

We often meet with people whose lives look very different now than they did in 2024. If you’ve experienced what the government calls a “Life-Changing Event,” such as retirement, a work reduction, or the loss of a spouse, you don’t have to just accept the higher bill. You can file an appeal using Form SSA-44. This process allows us to help you prove that your current income is lower than it was two years ago, which could potentially lower or even eliminate the surcharge. We want to make sure you aren’t paying more than your fair share because of outdated tax data.

Managing IRMAA Costs with Part D

It’s a common surprise for many of our clients to learn that IRMAA doesn’t just apply to Part B. It also impacts your prescription drug coverage. This surcharge is a separate bill that comes directly from Medicare, rather than being included in the premium you pay to your private insurance company. It’s helpful to review Medicare Part D to see how these adjustments might change your total monthly healthcare spending. We want to remove the mystery from these bills so you can stay in control of your finances.

One proactive way to manage these costs is to look at where your retirement income originates. Income from tax-advantaged sources, like a Roth IRA or certain life insurance policies, typically doesn’t count toward the IRMAA calculation. By shifting where you draw your funds, you might be able to stay below the next income threshold in future years. If you feel stuck in the maze of these rules, you can always reach out to us for a simple explanation of your options. We’re here to turn your confusion into clarity, ensuring your medicare part b premium 2026 fits comfortably into your life.

The Social Security Connection: How COLA Impacts Your Premium

We know how stressful it feels to see your hard earned Social Security raise disappear before you even touch it. Every year, the Social Security Administration announces a Cost of Living Adjustment (COLA) to help you keep up with inflation. However, because your Part B premium is usually deducted directly from your monthly check, these two numbers are closely tied. For 2026, the balance between your raise and your medicare part b premium 2026 determines exactly how much extra money you will actually see in your bank account.

In some years, the dollar amount of the Medicare increase can swallow up the entire COLA raise. This leaves some seniors with a “net zero” increase in their take-home pay. We work with you to analyze these shifts so you can plan your household budget with certainty. Our goal is to remove the anxiety from this process and give you a clear view of your finances for the coming year. We simplify the jargon so you know exactly how it works.

The 2026 Hold Harmless Clause

We want to make sure you feel secure knowing there is a legal safety net called the Hold Harmless clause. This rule requires that your Social Security check cannot decrease from one year to the next due to Part B premium hikes. If the 2026 premium increase is larger than your COLA raise, the government limits your premium to ensure your check stays the same. This protection applies to approximately 70 percent of Medicare beneficiaries. You are excluded from this protection if you fall into these categories:

- You are a new enrollee starting Medicare in 2026.

- You pay an Income Related Monthly Adjustment Amount (IRMAA) because of higher income.

- You are not yet drawing Social Security benefits.

We help our clients calculate their actual monthly check by looking at their specific COLA notice, which usually arrives in December 2025. This ensures you have confidence in your numbers before the new year begins.

Budgeting for Out-of-Pocket Changes

When we look at your medicare part b premium 2026, we also have to consider the Part B deductible. This amount resets every January 1. This is the amount you pay for outpatient services and doctor visits before Medicare begins to pay its share. If you have your first medical appointment on January 5, 2026, you will likely be responsible for this full amount out of pocket. We often suggest looking at a Medigap plan to help cover these gaps and provide peace of mind. Staying ahead of these numbers ensures you are never rushed or pressured when a medical need arises. We are here to provide year round support to catch these changes early and keep your plan on track.

Strategies to Manage Your Medicare Costs in 2026

We know that seeing the medicare part b premium 2026 increase can feel like a heavy weight on your monthly budget. It’s perfectly normal to feel a bit overwhelmed when these numbers shift. Our goal is to move you from confusion to confidence by looking at a few smart ways to balance your healthcare spending this year. We simplify the jargon so you know exactly how it works.

Medicare Advantage vs. Medigap in 2026

Choosing between these two paths is often the biggest decision you’ll make. Medicare Advantage plans often feel like a “pay-as-you-go” system. In 2026, many of these plans offer “give-back” benefits. This means the plan actually pays a portion of your Part B premium for you. This puts money back in your Social Security check every month. You can learn more about these specific 2026 options in our Medicare Advantage Guide.

Medigap plans work differently. They follow a “fixed-monthly” style. You pay a higher premium up front; however, the plan steps in to cover your Part B deductible and the 20% coinsurance that Original Medicare leaves behind. If you prefer predictability and don’t want to worry about a large bill after a doctor’s visit, Medigap offers more stability when Part B costs rise.

Finding Extra Help and Savings

If your income is limited, you might qualify for a Medicare Savings Program (MSP). These state-run programs can pay your entire medicare part b premium 2026 for you. We also look closely at the LIS, or Extra Help program. In 2026, the out-of-pocket drug cost cap of $2,000 is a major factor in your total budget. This cap makes your Part D plan a much more predictable expense than it was in previous years. We help you look at the total picture, not just one piece of the puzzle.

We believe an annual review is essential. Plans change their prices and benefit lists every single year. Working with an independent broker gives you an advantage that a captive agent simply cannot provide. We compare over 40 different carriers to find the one that fits your specific needs and budget. We’re here to protect you from costly enrollment mistakes and late penalties. We take the time to listen, ensuring you’re never rushed or pressured. We are your dedicated advocate in this complex system.

Ready to find the right balance for your 2026 budget? Schedule a Call With Paul today for a simple, unbiased review of your options.

Why Partnering with The Modern Medicare Agency Makes 2026 Simpler

The maze of Medicare in 2026 doesn’t have to be a source of stress or anxiety. We founded The Modern Medicare Agency with a single, clear mission: moving you from “Confusion to Confidence.” When you look at your medicare part b premium 2026 statement, you might feel overwhelmed by the rising costs or the technical language. We are here to change that experience for you. Our team brings unbiased, multi-state expertise to clients across 34 states, ensuring you have access to the best options regardless of where you live.

We aren’t captive agents who only show you one company. We’re independent advisors. This distinction is vital because it means we work for you, not the insurance carriers. We simplify the jargon so you know exactly how your plan works. We handle the tedious paperwork and the technical details that often lead to costly enrollment mistakes or late penalties. Our approach is simple; we are never rushed and never pressured. We take the time you need to feel secure in your choices because your health is too important to be treated like a sales quota.

Our Simple 5-Step Process

We’ve refined a path that takes the weight off your shoulders. Our services come at no cost to you. The insurance companies compensate us directly, which allows us to focus entirely on your specific needs without any hidden fees. Understanding your medicare part b premium 2026 is much easier when you follow our proven method:

- Initial Consultation: We listen to your health history and financial goals.

- Needs Analysis: We check if your doctors and prescriptions are covered.

- Plan Comparison: We explain the differences between options in plain English.

- Seamless Enrollment: We manage the application process from start to finish.

- Year-Round Advocacy: We don’t disappear after you sign up; we are here for every question throughout the year.

We stay by your side long after the initial paperwork is filed. If you receive a confusing bill or a notice from Social Security, we are the first call you make. We believe in building relationships that last for years, not just for an enrollment season.

Ready to Secure Your 2026 Coverage?

You don’t have to face these changes alone. We invite you to schedule a personal strategy session with Paul Barrett to discuss your specific situation. Whether you need a custom quote for Medigap or want to explore how a Medicare Advantage plan might fit your budget, we provide the clarity you deserve. We will help you steer clear of the pitfalls that catch many seniors off guard. Let us be your expert guide so you can face 2026 with total peace of mind and a plan that truly protects you.

Move From Confusion to Confidence in 2026

Navigating your healthcare shouldn’t feel like a walk through a maze. We’ve covered the essential details about the medicare part b premium 2026, including the updated deductible and how the latest Social Security COLA impacts your monthly budget. It’s vital to stay informed about IRMAA brackets to avoid unexpected costs. Our goal is to remove the anxiety from this process and replace it with a clear, step by step plan tailored to your needs.

As your dedicated advocates, we provide unbiased guidance from 40 insurance carriers. We’re licensed in over 34 states and bring 15 years of Medicare expertise to every conversation. We’ll help you steer clear of costly enrollment mistakes and find the path that fits your lifestyle. You don’t have to do this alone; we’re here to ensure you’re never rushed or pressured.

Schedule a Call With Paul to Review Your 2026 Costs

Your peace of mind is our priority, and we look forward to helping you navigate 2026 with total certainty.

Frequently Asked Questions About Medicare Part B in 2026

What is the standard Medicare Part B premium for 2026?

The standard monthly medicare part b premium 2026 is projected to be $196.70 according to the latest Medicare Trustees Report. Most people have this amount automatically deducted from their Social Security benefits each month. We know that seeing these costs rise can be stressful, but we’re here to help you plan your budget. We’ll make sure you understand exactly how this fits into your overall retirement strategy so you can feel confident.

Will the Medicare Part B deductible increase in 2026?

Yes, the annual Part B deductible is projected to increase to $267 for the 2026 calendar year. This is a rise of roughly $10 from the previous year’s costs. You’re responsible for paying this amount for doctor visits and outpatient care before Medicare starts covering its 80 percent share. We can show you how certain supplemental plans can help cover these out-of-pocket expenses so you don’t face unexpected medical bills throughout the year.

How does Social Security COLA affect my Medicare Part B premium in 2026?

The Social Security Cost of Living Adjustment helps your income keep up with inflation, but it’s closely tied to your premium. If the premium increase is larger than your COLA raise, the hold harmless provision typically protects you. This rule ensures your net Social Security check doesn’t shrink from one year to the next. We track these changes carefully to ensure you always have a clear, simple picture of your monthly retirement income.

What income is used to determine 2026 IRMAA surcharges?

The Social Security Administration looks at your 2024 tax returns to decide if you’ll pay an extra surcharge in 2026. They specifically use your Modified Adjusted Gross Income from two years ago to set your rate. If your 2024 income was over $106,000 as an individual or $212,000 for a couple, you’ll likely see an IRMAA adjustment. We simplify these complex brackets so you can prepare for any potential surcharges well in advance.

Can I appeal my 2026 IRMAA if my income has recently decreased?

You can certainly appeal your IRMAA if you’ve had a life-changing event that reduced your income since 2024. Events like retirement, work stoppage, or the loss of a spouse are valid reasons to request a cost reduction. You’ll need to submit Form SSA-44 along with documentation of the change to Social Security. We guide our clients through this appeal process step by step to help them keep their monthly costs as low as possible.

Does Medicare Advantage cover the Part B premium?

You must continue paying your Part B premium even if you join a Medicare Advantage plan. However, some plans offer a Part B Buy-Back or “Give Back” benefit that pays a portion of the premium for you. This can put anywhere from $10 to over $100 back into your Social Security check every month. We can search your specific zip code to see if these money-saving options are available in your community to help your budget.

What happens if I don’t sign up for Part B when I first become eligible?

If you miss your initial window, you’ll face a permanent late enrollment penalty that gets added to your medicare part b premium 2026. This penalty is 10 percent for every full 12-month period you were eligible but didn’t have creditable coverage. Since this extra cost stays with you for life, it’s vital to enroll at the right time. We help you navigate these deadlines so you can steer clear of these expensive, lifelong mistakes.

Is the Part B premium the same for everyone in 2026?

No, the amount you pay depends on your income and your enrollment history. While about 95 percent of people pay the standard $196.70 rate, higher earners pay more due to income-related adjustments. Others might pay more because of late enrollment penalties accumulated over several years. We provide an unbiased review of your situation to help you understand exactly what your personal costs will be for the upcoming year without any guesswork.