What if the most expensive part of your loved one’s journey isn’t the doctor visits, but the daily help they need just to get through the day? Many families assume medicare coverage for dementia and alzheimer’s care is all-inclusive, only to face a care gap that puts their life savings at risk. We know how overwhelming it feels to balance being a caregiver with being an insurance expert. It’s a heavy burden to carry alone, especially when you’re worried about making a mistake during enrollment that could cost you for years to come.

We’re here to help you move from confusion to confidence. This guide explains exactly how medicare coverage for dementia and alzheimer’s care works in 2026, from the $283 Part B deductible to the important new $2,100 out-of-pocket cap on prescription drugs. We simplify the jargon so you know which plans protect your family’s finances and which ones might leave you exposed. You’ll learn the vital difference between medical and custodial care, see a clear list of covered services, and find out how to choose between Medicare Advantage and Medigap with total peace of mind.

Key Takeaways

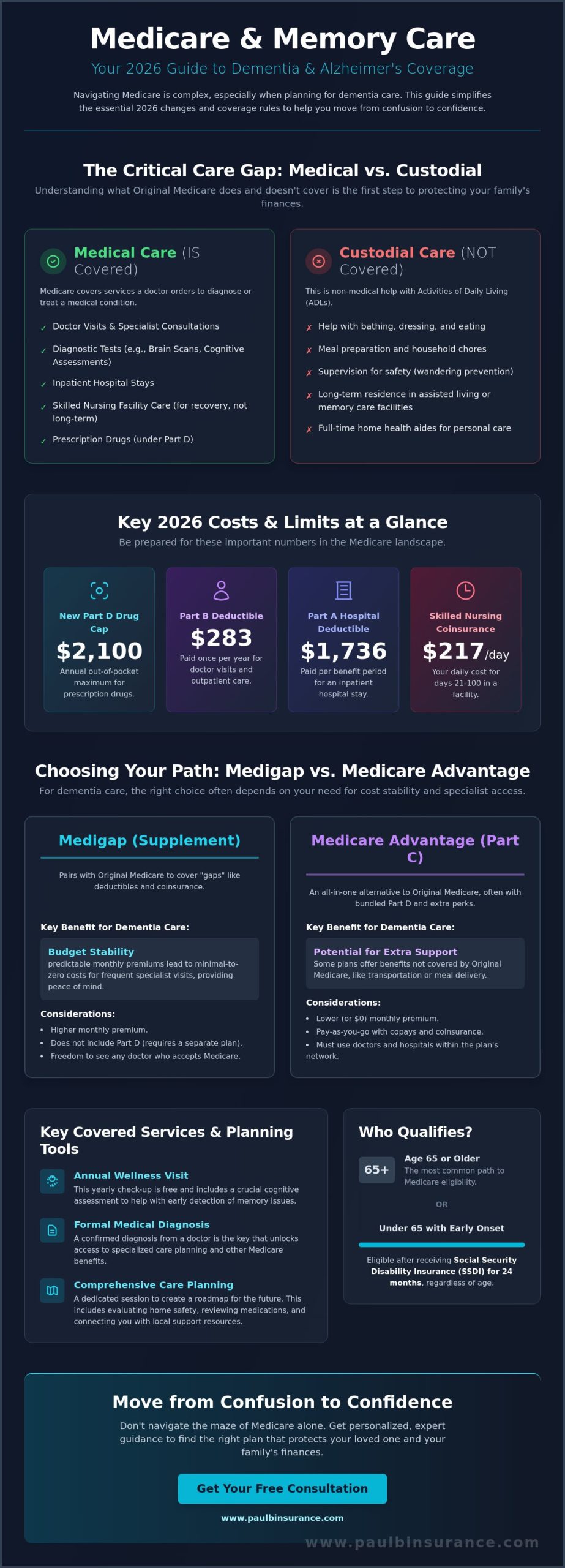

- Learn the critical difference between medical care and custodial care so you aren’t surprised by what Original Medicare won’t pay for.

- Discover how medicare coverage for dementia and alzheimer’s care changed in 2026, including the new $2,100 limit on your yearly pharmacy costs.

- Compare Medigap and Medicare Advantage to find out which option provides the most stable monthly budget for frequent specialist visits.

- Find out how to use covered care planning benefits to help your family understand treatment options and local support resources.

- Follow our 5-step guide to move from confusion to confidence and avoid costly enrollment mistakes that could impact your loved one’s care.

Understanding Medicare Coverage for Dementia & Alzheimer’s in 2026

Receiving a diagnosis of dementia or Alzheimer’s is a life-changing moment for any family. It brings up a lot of questions about the future, and one of the biggest concerns is how to pay for the help your loved one needs. It’s helpful to know that Medicare treats these conditions as medical illnesses. This means that the doctors, tests, and hospital stays required for treatment fall under the standard rules of Understanding Medicare. We’ve spent years helping families move from a state of total overwhelm to a place of clarity. We use our “Confusion to Confidence” framework to make sure you aren’t guessing about your benefits. As independent brokers, we’re here to protect your interests, not the insurance companies’ bottom line.

The 2026 Medicare Landscape for Memory Loss

The insurance world changes every year, and 2026 is no different. For this year, the standard Medicare Part B deductible is $283. This is the amount you’ll pay for doctor visits and diagnostic tests before Medicare starts to pick up its share of the cost. We always encourage our clients to take full advantage of the Annual Wellness Visit. It’s a benefit that costs you nothing out-of-pocket and includes a cognitive assessment. This is a vital tool for early detection. By looking at these 2026 regulations early, we can help you prepare for the road ahead without the stress of unexpected bills.

Who Qualifies for Dementia-Related Medicare Coverage?

A common misconception is that you must be 65 to access these benefits. While most people join Medicare at 65, those with early-onset Alzheimer’s can qualify earlier. If a person has received Social Security Disability Insurance (SSDI) for 24 months, they become eligible for Medicare regardless of their age. You can find more details on these specific requirements in our Medicare Eligibility Guide. Once you’re in the system, medicare coverage for dementia and alzheimer’s care provides the same level of medical support for everyone.

The key to unlocking the most helpful benefits is a formal medical diagnosis. Once a doctor confirms the condition, Medicare covers a comprehensive care planning session. This isn’t just a quick check-up. It’s a deep dive where a specialist helps you create a roadmap for the future. During this session, your team will:

- Evaluate home safety to prevent falls or wandering.

- Review all medications to check for drug interactions or side effects.

- Identify community resources like support groups and local respite care.

We’re here to help you navigate these initial steps with patience and expertise. We believe that when you have the right information, the “crazy maze” of the insurance system becomes much easier to manage.

Medical vs. Custodial Care: What Original Medicare Covers

We often see families breathe a sigh of relief when they learn Medicare covers the doctor. But that relief quickly turns to worry when they realize it doesn’t pay for the daily help their loved one needs. It’s vital to understand the “care gap” early so you aren’t caught off guard. Medicare is health insurance, not a long-term care program. It’s designed to treat medical conditions, not to provide a personal assistant for daily life. While this distinction can feel frustrating, knowing the rules helps us build a plan that protects your family’s savings.

Medical care includes things like brain scans, specialist visits, and hospital stays. Custodial care, on the other hand, refers to help with “activities of daily living” like getting dressed, bathing, or eating. Original Medicare (Parts A and B) does not cover long-term memory care, assisted living, or a home health aide who simply helps with chores. While custodial care is out, the medical treatment side of medicare coverage for dementia and alzheimer’s care is actually quite robust. We’re here to help you maximize those medical benefits while you figure out the rest.

Part A: Hospitalization and Skilled Nursing

If your loved one needs a hospital stay for a psychiatric evaluation or a related illness, Part A is there to help. In 2026, the inpatient hospital deductible is $1,736 per benefit period. If a stay lasts longer than 60 days, you’ll face a daily coinsurance of $434. For Skilled Nursing Facilities (SNF), Medicare pays for the first 20 days in full. From days 21 to 100, there’s a daily coinsurance of $217. Crucially, this SNF care must be for recovery from a specific injury or illness. It cannot be used for permanent residence in a nursing home just because someone has dementia.

Part B: Outpatient Services and Diagnostics

Part B is the workhorse for managing the ongoing medical needs of memory loss. It covers diagnostic tools like MRIs, CT scans, and neurological exams to help confirm a diagnosis. A major benefit for families is the Medicare-covered cognitive assessments that allow doctors to create a detailed care strategy. Part B also pays for physical and occupational therapy. These services are essential for helping your loved one stay mobile and safe in their own home for as long as possible. If you’re feeling stuck between these complex choices, you can always view our Medigap guide to see how a supplement plan might help fill these expensive coinsurance gaps.

Medicare Advantage vs. Medigap: Which Path Is Better for Dementia?

Choosing between Medigap and Medicare Advantage is one of the biggest decisions you’ll make for your family. It determines which doctors you can see and how much you’ll pay out-of-pocket for every specialist visit. For medicare coverage for dementia and alzheimer’s care, the right choice depends on whether you value total freedom of choice or extra support services. We know this decision feels heavy, but we’re here to help you weigh the pros and cons with total clarity.

With Medigap, also known as Medicare Supplement Insurance, you keep Original Medicare as your primary coverage. This means you can see any doctor in the country who accepts Medicare. For a family dealing with a complex neurological condition, this freedom is a massive relief. You won’t need a referral to get a second opinion from a top-tier neurologist or a specialized memory clinic. Medigap plans also step in to pay the 20% coinsurance that Original Medicare leaves behind. Without this protection, frequent office visits and diagnostic tests can quickly drain a family’s savings. While these plans don’t usually offer bells and whistles like gym memberships, they provide a level of financial stability that is hard to beat.

Medicare Advantage: Extra Support and SNPs

Medicare Advantage plans work differently. These are managed by private companies and often bundle your hospital, medical, and drug coverage into one plan. You can find a deeper explanation of how these work in our Medicare Advantage Guide. Some of these plans are called Chronic Condition Special Needs Plans (C-SNPs). These are specifically tailored for people with conditions like dementia. They might offer extra benefits that Original Medicare doesn’t, such as transportation to the doctor or meal delivery services. According to the Alzheimer’s Association guide to Medicare, these specialized plans can provide a more coordinated care experience for medicare coverage for dementia and alzheimer’s care.

However, there’s a trade-off you must consider. Most Advantage plans use networks like HMOs or PPOs. If your favorite specialist isn’t in that network, you might pay much more or have no coverage at all. You also have to deal with “prior authorizations,” where the insurance company must approve a treatment before they pay for it. This can add a layer of stress when you’re already managing a difficult diagnosis. We help you look at your specific doctors and medications to see which path offers the most peace of mind for your unique situation.

Managing Prescription Costs and Care Planning Services

One of the biggest fears families face is the rising cost of specialized medications. In the past, a single prescription for a breakthrough Alzheimer’s drug could cost thousands of dollars, leaving families to foot the bill. Thankfully, medicare coverage for dementia and alzheimer’s care has seen a major upgrade in 2026. This year, the Inflation Reduction Act has fully kicked in. It provides a safety net that simply didn’t exist a few years ago. We’ll help you look at your specific prescriptions to ensure you’re getting every penny of help available.

Beyond the pharmacy, Medicare recognizes that the family needs support too. The Care Planning benefit, often referred to by doctors as billing code G0505, is specifically for people with cognitive impairment. It covers a dedicated session with a specialist to discuss treatment options and caregiver support. This benefit is a vital tool for moving from a state of worry to a clear, actionable plan for the future. We’ve seen this session change everything for families who were previously feeling lost in the system.

Navigating the 2026 Part D Changes

For 2026, the most significant change is the $2,100 annual out-of-pocket cap on prescription drugs. This cap specifically helps dementia patients on high-tier medications by ensuring they never pay more than $2,100 in a calendar year for their covered drugs. You can also take advantage of the Medicare Prescription Payment Plan (M3P). This program allows you to spread your drug costs out into monthly installments rather than paying a huge sum all at once at the pharmacy counter. We compare drug lists across more than 40 different carriers to find the one that fits your budget best. You can learn more about how these tiers work in our Medicare Part D Guide.

Support for the Caregiver

Caring for a loved one is a full-time job. Medicare has started to recognize the physical and emotional toll it takes on the family. In 2026, Medicare now pays for caregiver training sessions in certain situations. These sessions teach you how to manage medications and keep your loved one safe at home. If the condition progresses to the final stages, hospice care through Part A provides incredible support. This includes respite care, where your loved one can stay in a Medicare-approved facility for up to 5 days at a time to give you a much-needed break. If you aren’t sure which drug plan covers your specific medications, schedule a call with us to review your options for 2026.

Choosing the Right Plan for Your Family’s Peace of Mind

We understand that there is no “one-size-fits-all” plan when it comes to medicare coverage for dementia and alzheimer’s care. Every family has different doctors, specific pharmacies, and unique financial goals. That’s why we don’t just hand you a brochure and walk away. We use a proven 5-step process to move you from “Confusion to Confidence.” This methodical approach ensures we look at every angle of your loved one’s health needs before we make a single recommendation. We want you to feel certain that the plan you choose today will still protect you tomorrow.

We are independent brokers, which is a vital distinction in the insurance world. It means we don’t work for the big insurance companies; we work for you. While a “captive agent” is limited to selling plans from just one company, we have the freedom to compare options from over 40 different carriers. This unbiased approach is the only way to ensure you aren’t missing out on benefits or paying for coverage you don’t need. We are your advocates, and our only goal is to find the best fit for your family’s budget and health requirements.

Avoiding Costly Enrollment Mistakes

Missing an enrollment window isn’t just a minor headache. It can lead to lifelong late enrollment penalties that increase your monthly premiums forever. We help you steer clear of these expensive traps by tracking your deadlines and ensuring your paperwork is perfect. Another common mistake is choosing a plan that doesn’t include your specific neurologist or the high-tier medications required for memory care. You can read more about why choosing the right partner matters in our Medicare Broker Guide. We make sure the plan you choose actually works in the real world, not just on paper.

Your Next Steps: Schedule a Call

The path forward is simple and stress-free. Your first step is to gather a list of current medications and your preferred doctors. Then, we invite you to schedule a no-pressure consultation with Paul Barrett. We’ll sit down with you, listen to your concerns, and answer every question until you feel completely secure. Our services come at no cost to you. We are compensated by the insurance companies, but our loyalty remains strictly with your family. We are never rushed, and you will never feel pressured to make a quick decision. We are here to protect your health and your peace of mind as you manage medicare coverage for dementia and alzheimer’s care in 2026.

Move from Confusion to Confidence Today

Managing a diagnosis of memory loss is enough of a challenge without having to fight the insurance system at the same time. We’ve shown you how to distinguish between covered medical services and the gaps in custodial care, as well as how the new 2026 $2,100 out-of-pocket cap on medications can protect your family’s savings. Securing the right medicare coverage for dementia and alzheimer’s care doesn’t have to be a source of constant anxiety. When you have a clear plan, you can stop worrying about the bills and focus on what truly matters: spending quality time with your loved one.

Since 2010, we’ve provided unbiased, independent guidance to families across the country. We represent over 40 insurance carriers and are licensed in 34+ states, giving us the freedom to find the exact plan that fits your unique needs. You don’t have to navigate this “crazy maze” alone. We’re here to be your advocate, ensuring you never feel rushed or pressured into a decision. Schedule a Call With Paul today for a free, no-pressure consultation. We’re ready to help you find the peace of mind your family deserves.

Frequently Asked Questions

Does Medicare pay for memory care facilities or assisted living?

No, Medicare does not pay for the room and board costs at memory care facilities or assisted living. These services are considered “custodial care” rather than medical treatment. While Medicare continues to pay for your doctor visits, diagnostic tests, and medications while you live there, the monthly rent for the facility remains a personal or private expense.

How much does Medicare cover for home health care for dementia patients?

Medicare covers 100% of the cost for part-time skilled nursing care or physical therapy at home if a doctor certifies that it is medically necessary. However, it does not pay for 24-hour-a-day care or for home health aides who only help with daily chores like meal preparation and cleaning. To qualify for this benefit, the patient must be considered homebound and require skilled services that cannot be provided by family members.

Will Medicare Part D cover the new Alzheimer’s drugs like Leqembi in 2026?

Yes, most Medicare Part D plans in 2026 cover FDA-approved Alzheimer’s medications, and the new $2,100 out-of-pocket cap makes these high-cost treatments much more affordable. Some of these newer medications are administered via infusion in a doctor’s office, which means they may be covered under Part B instead of Part D. We always check the specific drug list, or formulary, for every plan to ensure your medications are covered at the lowest possible cost.

Is a cognitive assessment covered by Medicare Part B?

Yes, medicare coverage for dementia and alzheimer’s care includes a cognitive assessment as a standard part of your Annual Wellness Visit. If your doctor identifies any signs of impairment, Medicare Part B also pays for a more comprehensive care planning session. This allows you and your family to work with a specialist to create a medical roadmap, discuss treatment options, and identify local support resources.

What is a Dementia Special Needs Plan (C-SNP)?

A Chronic Condition Special Needs Plan, or C-SNP, is a type of Medicare Advantage plan designed specifically for people with certain illnesses like dementia. These plans often feature a network of doctors who specialize in memory loss and provide extra care coordination to help manage the condition. We help you compare these specialized options to see if they offer more value than a standard plan for medicare coverage for dementia and alzheimer’s care.

Can I switch Medicare plans if my dementia progresses?

You can typically switch your Medicare plan during the Annual Enrollment Period, which runs from October 15th to December 7th. If you are already enrolled in a Medicare Advantage plan, you have an additional window to switch or drop your plan from January 1st to March 31st each year. We help you monitor these dates so you can adjust your coverage as your health needs change without facing a gap in care.

Does Medicare cover adult day care for those with Alzheimer’s?

Original Medicare does not cover adult day care services because they are classified as custodial care. However, some Medicare Advantage plans in 2026 have added supplemental benefits that may provide limited coverage for adult day care or respite services. It is important to look closely at the specific Evidence of Coverage for each plan, as these extra benefits vary significantly by insurance company and location.

What happens to my coverage if I move into a nursing home?

Medicare continues to cover your medical needs, such as hospital stays and doctor visits, even if you move into a nursing home. However, Medicare will not pay for the long-term room and board costs of the facility. The only exception is a short-term stay in a Skilled Nursing Facility for rehabilitation after a qualifying hospital stay, which is covered for up to 100 days per benefit period. For permanent residency, families often rely on private funds or Medicaid.