What if relying solely on your VA health care is actually the riskiest move you can make for your future? Many veterans we speak with believe their VA coverage is all they need, only to face a lifelong Part B penalty later because they misunderstood the rules. We understand why you might feel frustrated with 28 day wait times for specialty care or anxious about potential funding shifts. It’s confusing to hear that VA coverage isn’t always considered “creditable” for Part B, especially when you’ve earned those benefits through years of service.

We’re here to show you exactly how medicare and VA benefits how they work together to give you the freedom to choose your own doctors without breaking your budget. In this guide, we’ll simplify the 2026 enrollment rules, explain why the $202.90 standard Part B premium is often your best insurance against the unknown, and help you build a plan that offers total confidence. You’ll learn how to protect yourself from future penalties while ensuring you never have to wait weeks for the care you deserve. We’ll move you from confusion to a clear plan that secures your health for years to come.

Key Takeaways

- Understand why having both systems is the gold standard for your health, giving you more doctor choices and shorter wait times than the VA alone.

- Learn the truth about medicare and VA benefits how they work together as separate programs that don’t share costs or coordinate billing.

- Protect your retirement savings by discovering why VA coverage isn’t “creditable” and how to steer clear of the 10% lifetime Part B penalty.

- Explore how specialized 2026 Medicare Advantage plans can actually put money back in your pocket through Part B premium giveback features.

- See how our simple 5-step process removes the stress by comparing over 40 different carriers to find your perfect fit.

Do You Really Need Medicare if You Have VA Benefits in 2026?

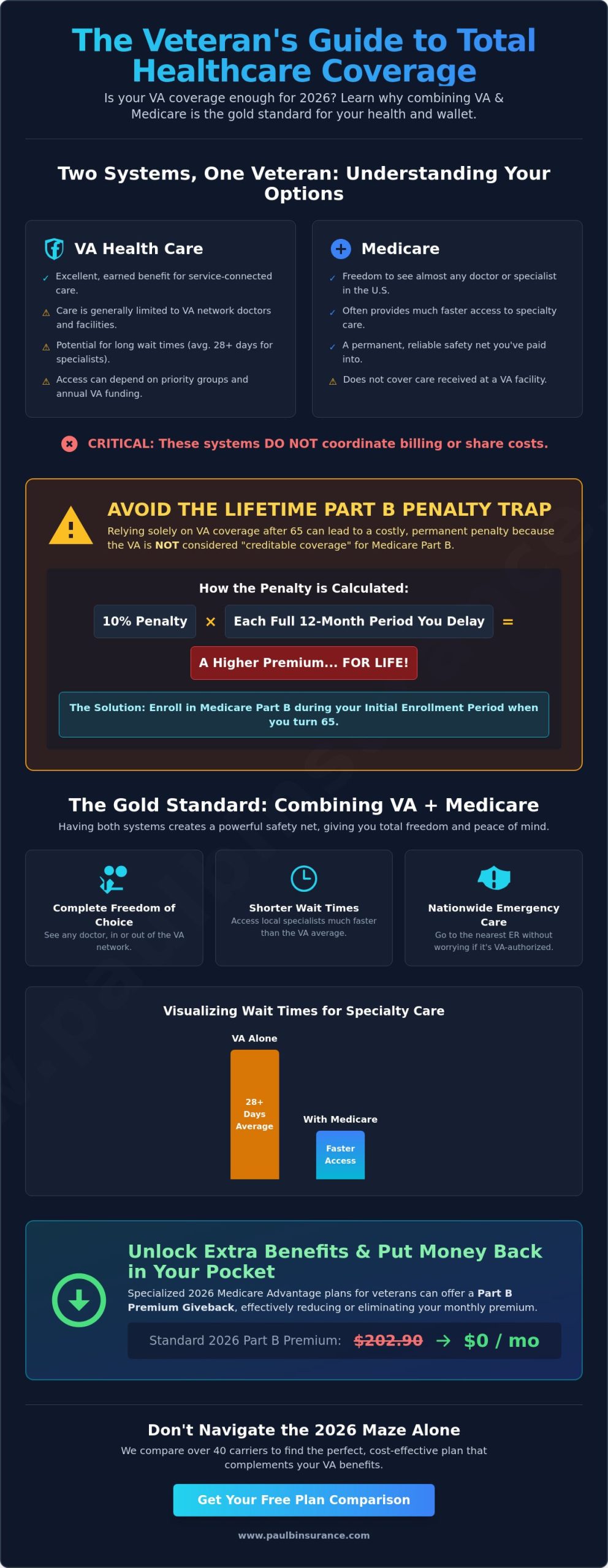

We often hear veterans say, “I’ve got the VA, so I’m set.” We truly honor that service, but the reality of healthcare in 2026 is complex. The VA and Medicare are two entirely separate systems. They don’t speak to each other, they don’t share medical records, and they don’t coordinate billing. If you’re looking for an overview of veterans benefits, you’ll see that while the VA offers incredible support, it’s designed to function as a closed loop. Enrolling in both is the gold standard because it fills the gaps that one system alone leaves behind. Knowing medicare and VA benefits how they work together is about creating a safety net that protects your health and your wallet. We don’t want you to feel stuck in a maze where you’re forced to choose between your earned benefits and the care you actually need.

Medicare isn’t a replacement for your VA care. It’s a strategic layer of protection. Think of it as an earned secondary layer of security that you’ve paid into throughout your working life. Having both means you have two different ways to get the care you need, ensuring that you’re never left without options if one system is overwhelmed or unavailable.

The Freedom of Choice: Beyond VA Facilities

VA benefits are excellent, but they generally only cover care within the VA network. If you need a specialist who isn’t at your local facility, or if you want a second opinion from a top-tier civilian hospital, your VA coverage likely won’t pay the bill. Medicare acts as your personal passport to nearly any doctor in the U.S. In 2026, wait times for specialty care at some VA facilities still average over 28 days for an appointment. With Medicare, you can often see a local specialist much faster. It gives you the power to choose the best care for your specific needs, whether that’s inside the VA system or at a private clinic down the street. It’s about having options when your health is on the line. Imagine the peace of mind knowing you can head to the nearest emergency room without worrying if it’s a VA-authorized facility.

Protecting Your Future: The Reality of VA Funding

VA priority groups determine who gets care first, and these rankings can shift based on government budgets. If you’re in a lower-priority group, your access isn’t always guaranteed if funding levels change. Medicare provides a permanent, reliable safety net that doesn’t depend on annual congressional appropriations for the VA. It’s a benefit you’ve earned through years of working, just like you earned your VA status through service. If you’re feeling a bit lost on the basics, our guide on what Medicare is offers a great starting point. Having both systems ensures you’re never at the mercy of a single budget or a single facility’s schedule. When you understand medicare and VA benefits how they work together, you realize you’re building a plan that protects your future from every angle.

How Medicare and VA Health Care Coordinate (and Where They Don’t)

We often see veterans surprised that they can’t use Medicare at the VA clinic. It’s a common point of confusion that we help clarify every day. The most critical rule to remember about medicare and VA benefits how they work together is that they do not coordinate payments. The VA won’t pay for your Medicare Part B deductible, which is $283 in 2026. Conversely, Medicare won’t pay for your VA copayments, such as the $50 charge for specialty care visits. Each system is its own island, and they don’t share the bill. You’re either using one or the other, depending on where you are standing when you receive care.

However, the VA is legally required to bill any private health insurance you carry for care related to non-service-connected conditions. While they cannot bill Original Medicare, they can and will bill a Medicare Supplement plan. This helps the VA recover costs and can sometimes count toward your private plan’s out-of-pocket limits. Following the official VA guidance on Medicare ensures you stay compliant with these rules. If you’re feeling overwhelmed by these details, you can reach out to us for a simple explanation tailored to your situation.

Service-Connected vs. Non-Service-Connected Care

The distinction between service-connected and non-service-connected care is the pivot point for your coverage. If you’re treated for a disability linked to your service, the VA generally handles the cost. For everything else, Medicare is your primary safety net if you step outside the VA system. We recommend keeping your cards separate to avoid any mix-ups at the front desk. Using your Medicare card at a VA facility won’t work, and presenting your VA ID at a civilian hospital won’t guarantee payment without prior authorization. Medicare ensures that “non-service” doesn’t mean “not covered” when you’re at a local clinic.

The Role of Medigap for Veterans

A Medicare Supplement plan provides the predictability that many veterans crave. While the VA offers great care, it can’t be everywhere. If you see a civilian doctor, Medicare Part A and B leave you with out-of-pocket costs like the $1,736 hospital deductible. Our Medicare Supplement Insurance guide details how these plans step in to pay those bills. In 2026, Plan G is a favorite because it covers the 20% coinsurance that Original Medicare ignores. It’s a simple way to ensure that your healthcare costs remain stable, no matter where you choose to receive treatment. We focus on making these choices clear so you can feel confident in your coverage.

The Part B Penalty Trap: Why 65 is the Magic Number

Many veterans we talk to are shocked to learn that VA health care is not considered “creditable coverage” for Medicare Part B. This is perhaps the most dangerous trap in the entire system. While your service earned you access to VA facilities, the federal government doesn’t view that access as a substitute for medical insurance. If you miss your enrollment window at age 65, you’ll face a 10% lifetime penalty for every 12 month period you delayed. With the 2026 standard Part B premium set at $202.90, waiting just five years could add over $100 to your monthly bill for the rest of your life. Understanding how VA health care and other insurance interact is the only way to shield your retirement savings from these permanent costs.

We want to help you steer clear of these costly enrollment mistakes. The math is simple but brutal. If you wait until age 70 to sign up because you thought the VA was enough, your premium will be 50% higher than your peers. This penalty never goes away, even if you move or change plans later. We focus on providing the clarity you need now so you don’t have to pay for a misunderstanding for the next thirty years. Knowing medicare and VA benefits how they work together starts with realizing that Medicare Part B is your primary protection against these lifelong surcharges.

Understanding Part B Enrollment Periods

Your Initial Enrollment Period is a seven month window that opens three months before you turn 65. It’s vital to remember that veterans don’t get a Special Enrollment Period just because they have VA benefits. Unless you are still working and have insurance through a large employer, 65 is your one clear shot to join without a penalty. You can find your specific deadlines on our Medicare Eligibility checklist. We make sure you know exactly when to act so you can move from confusion to confidence.

Part D and VA Pharmacy: A Different Story

The rules for prescription drugs are much more forgiving. The VA pharmacy system is considered creditable coverage, so you generally won’t face a penalty for skipping Part D. However, many of our clients still choose a Medicare Part D plan for the convenience of using a local pharmacy. By 2026, the “donut hole” has been fully eliminated, and out of pocket costs are capped at $2,000 for the year. This makes private drug coverage a great secondary option if you don’t want to rely solely on VA mail order prescriptions. It’s another example of medicare and VA benefits how they work together to give you more control over your daily life.

Medicare Advantage for Veterans: Unlocking Extra Benefits

We help you find plans that actually put money back in your Social Security check. While we’ve already discussed why enrolling in Part B is vital to avoid penalties, we know the monthly cost can feel like a burden. This is where specialized 2026 Medicare Advantage plans come into play. Many of these plans are designed specifically for veterans who already use VA pharmacy benefits. These “MA-only” plans don’t include drug coverage, which prevents any messy coordination issues with your VA prescriptions. Instead, they often feature a “Part B Giveback.” This means the insurance company pays a portion of your $202.90 monthly premium for you. It’s a powerful example of medicare and VA benefits how they work together to lower your out of pocket costs while expanding your care options.

In 2026, we’re seeing a significant trend where these plans offer even more robust “extra” benefits. Because the plan isn’t spending money on drug coverage, they can redirect those funds toward things the VA might not provide. We focus on simplifying these choices so you can see exactly how much you could save each month. If you want to see which plans offer the best giveback in your zip code, schedule a call with Paul today for a personalized review.

Dental and Vision: The VA’s Missing Pieces

Many veterans are surprised to find they don’t automatically qualify for VA dental care. Usually, you need a 100% disability rating or a specific service-connected dental injury to get coverage. A Medicare Advantage plan can bridge this gap by providing comprehensive dental insurance for cleanings, crowns, and even implants. Similarly, getting a vision exam or a new pair of glasses through the VA can involve long wait times. These plans allow you to visit a local optometrist in your neighborhood, often with little to no copay. It’s about making your daily life easier and more affordable.

TRICARE for Life and Medicare Advantage

If you have TRICARE for Life (TFL), you already know that Part B is a requirement. TFL is an incredible benefit, but in some specific cases, adding a Medicare Advantage plan can still make sense. This is typically for veterans looking for those extra dental or vision perks that TFL doesn’t prioritize. However, this is a delicate balance, and we want to ensure you don’t accidentally disrupt your existing coverage. You can read more about these nuances in our Medicare Advantage 2026 guide. We’re here to help you weigh the pros and cons without any pressure, ensuring your medicare and VA benefits how they work together perfectly for your unique situation.

Choosing Your Path: How We Help Veterans Navigate the 2026 Maze

We know that figuring out how your earned benefits fit into the larger healthcare puzzle can feel like a full-time job. Our mission is to take that weight off your shoulders. We use a clear 5-step process to ensure your medicare and VA benefits how they work together is a source of strength, not a headache. First, we listen to your specific health goals. Second, we review your VA priority group. Third, we verify your civilian doctor preferences. Fourth, we compare options from over 40 independent carriers. Finally, we help you implement a plan that offers total peace of mind. We’re never rushed and never pressured. We’re here to provide honest guidance that puts your needs first.

Many veterans ask us if the $202.90 monthly Part B premium is truly worth the cost. We look at it as an investment in your freedom. While the VA provides vital care, the ROI on Medicare is found in the ability to skip the 28 day wait times for specialists and the 60 minute drives to VA facilities. It’s about having a backup plan that works anywhere in the country. We help you weigh these costs against the potential for lifelong penalties to ensure you’re making the most ethical choice for your future self.

Personalized Plan Comparison

Doctors often change their network affiliations, especially with the significant plan shifts we’ve seen in 2026. We take the time to check if your preferred civilian specialists are still in-network before you make any decisions. An annual review is essential because what worked last year might not be the best fit today. We invite you to Schedule a Call with Paul for a stress-free consultation. We’ll look at the data together and find a path that keeps your favorite doctors accessible and your costs predictable.

The Modern Medicare Agency Advantage

There’s a big difference between a captive agent and an independent broker. A captive agent works for one insurance company and can only show you their products. As independent brokers, we work for you. We fight to find the best value across dozens of carriers because we don’t have a horse in the race. Our support doesn’t end once your plan is active, either. We provide year-round guidance to help you handle billing questions or network changes. Let us help you move from confusion to confidence today.

Take Control of Your Healthcare Future

You now have a clear picture of why relying on one system alone leaves you vulnerable. You’ve seen that the VA and Medicare are separate islands, and you know how to avoid the permanent financial sting of a lifelong penalty. Most importantly, you understand that having both systems gives you the freedom to choose your own doctors and skip the frustration of long wait times. This knowledge is your first step toward true security. Understanding medicare and VA benefits how they work together isn’t just about insurance; it’s about making sure you have the best care available when you need it most.

We’re here to help you navigate this maze with confidence. As independent brokers licensed in 34+ states, we provide unbiased guidance by comparing options from 40+ different carriers. We’ve been dedicated advocates for veterans since day one, and we promise to never rush or pressure you. Move from confusion to confidence; schedule your free veteran Medicare review with Paul today. You’ve spent your life serving others. Now, it’s our turn to help you protect the retirement and health you’ve worked so hard to earn.

Frequently Asked Questions

Do I have to sign up for Medicare if I have VA benefits?

No, the VA doesn’t require you to sign up for Medicare to keep your veterans benefits. However, we strongly advise enrolling in Part A and Part B as soon as you’re eligible. Relying only on the VA means you’re limited to their facilities and wait times, which can exceed 28 days for specialty care. Medicare gives you the freedom to see nearly any civilian doctor in the country.

Is VA health care considered creditable coverage for Medicare Part B?

No, VA health care is not considered creditable coverage for Medicare Part B. This is a common trap that leads to lifelong financial stress. While VA coverage is creditable for Part D prescription drugs, it doesn’t count for Part B. If you skip Part B at age 65, you won’t get a special enrollment period to join later without a penalty.

Can I use Medicare at a VA hospital or clinic?

No, you cannot use Medicare at a VA facility. Medicare and the VA are separate systems that don’t share costs or coordinate billing. If you’re at a VA clinic, the VA handles the bill. If you’re at a civilian hospital, Medicare is the primary payer. Understanding medicare and VA benefits how they work together means knowing which card to show depending on where you are standing.

What happens if I delay Medicare Part B because I have VA benefits?

If you delay Part B, you’ll face a 10% lifetime penalty for every 12 month period you were eligible but didn’t enroll. In 2026, with the standard premium at $202.90, a three year delay would add over $60 to your monthly cost forever. We want to help you avoid this permanent surcharge so your retirement income stays in your pocket where it belongs.

Does Medicare Part D work with my VA prescription drug coverage?

They don’t work together directly, but they can complement each other. Since VA drug coverage is creditable, you don’t need a Part D plan to avoid penalties. However, many veterans choose a Part D plan to get medications from a local pharmacy instead of waiting for VA mail-order. By 2026, the $2,000 out of pocket cap makes Part D a very attractive secondary option.

What is a “Part B Giveback” plan for veterans?

A Part B Giveback is a feature in certain 2026 Medicare Advantage plans designed specifically for veterans. These plans often don’t include drug coverage to avoid interfering with your VA pharmacy benefits. Instead, the insurance company pays a portion of your $202.90 monthly Part B premium for you. It’s a simple way to increase your monthly Social Security check while gaining extra benefits.

If I have 100% VA disability, do I still need Medicare?

Yes, we recommend Medicare even for veterans with a 100% disability rating. While your VA care is comprehensive, it’s still restricted to VA facilities. Medicare provides a vital safety net for emergency care at civilian hospitals and gives you the option to see specialists outside the VA system. It also ensures you won’t face penalties if VA funding or priority rules change in the future.

How do I coordinate TRICARE for Life with Medicare in 2026?

To keep your TRICARE for Life (TFL) coverage in 2026, you must be enrolled in Medicare Part B. Medicare acts as your primary insurance for civilian care, and TFL acts as the secondary payer to cover your deductibles and coinsurance. This combination is the gold standard for coverage, as it typically leaves you with zero out of pocket costs for most medical services. Knowing medicare and VA benefits how they work together with TFL is the key to total peace of mind.