Last week, a client named Mary sat in my office in tears because her husband’s HR department gave her one set of instructions, while the Social Security office gave her another. She was terrified that a simple misunderstanding about how to coordinate medicare with my spouse’s insurance would lead to a lifetime of financial penalties. This kind of stress is far too common in 2026, but it doesn’t have to be your reality. You aren’t alone in this, and the fear of making a permanent mistake is completely valid when the advice you’re getting feels so contradictory.

We’ll clear up that confusion right now. This guide will show you exactly how to blend Medicare with your spouse’s employer coverage to maximize your benefits and avoid costly mistakes. We’ll explain the “20-employee rule” for 2026, clarify which insurance pays your bills first, and give you a straightforward “yes or no” on whether you need to enroll today. By the end of this article, you’ll have the peace of mind that comes from knowing you’re following the rules and protecting your health.

Key Takeaways

- Understand how the “billing order” works so you know exactly which insurance company pays your medical bills first.

- Learn why the 20-employee rule is the most important factor in deciding if you can safely delay Medicare Part B in 2026.

- Discover exactly how to coordinate medicare with my spouse’s insurance to avoid the 10% lifetime penalty for late enrollment.

- Explore three common paths that help you decide whether to keep your spouse’s plan, switch to Medicare, or use both as a safety net.

- Find out why employer HR departments often provide incomplete advice and how an independent expert can compare your total costs side-by-side.

Understanding the Basics: What Does “Coordination of Benefits” Mean in 2026?

If you’ve ever felt like insurance companies speak a different language, you aren’t alone. The term “Coordination of Benefits” sounds like something from a legal textbook, but it’s actually just a simple set of rules for who pays your doctor first. Coordination of Benefits is the system that prevents double-payment of medical claims. In 2026, understanding this process is the key to making sure your medical bills don’t end up sitting on your kitchen table unpaid while insurers argue over who is responsible.

When you’re trying to figure out how to coordinate medicare with my spouse’s insurance, you’re really just trying to establish a “billing order.” Think of it like a line at a grocery store. One insurance company stands at the front of the line (the Primary Payer) and pays what they owe based on your plan’s coverage. The second insurance company (the Secondary Payer) stands behind them and only steps in to cover what the first one didn’t pay. If you get this order wrong, it can lead to delayed claims, rejected bills, and a lot of unnecessary out-of-pocket stress.

Before diving into the specifics of your situation, Understanding the Basics of Medicare can help you see how the different parts of the program, like Part A and Part B, were designed to work alongside other types of coverage. Our mission at The Modern Medicare Agency is to make this transition feel like a relief rather than a burden.

The Primary vs. Secondary Payer Dynamic

The most important rule is this: don’t cancel your spouse’s insurance plan until you are 100% certain of the billing order. In many cases, Medicare acts as a “backup” to employer plans, but this isn’t always true. If your spouse works for a small business, Medicare might actually be the one that needs to pay first. If you don’t sign up for Part B because you assumed the employer plan was primary, the secondary insurance might refuse to pay their portion. This leaves you responsible for the entire bill. We’ve seen this happen to many folks who didn’t get clear advice, and it’s a situation we want to help you avoid entirely.

Why 2026 is a Unique Year for Coordination

While Medicare rules have remained relatively stable, 2026 has brought changes to many employer-sponsored plans, specifically regarding premiums and what they are willing to cover for dependents. This makes it more important than ever to check your spouse’s “Summary of Benefits” document every year. You might find that how to coordinate medicare with my spouse’s insurance changes if their company changes insurance carriers or adjusts their plan levels.

At The Modern Medicare Agency, we help you look at your spouse’s current costs and compare them side-by-side with options like Medigap plans or Medicare Advantage. Sometimes, keeping both is the right move. Other times, moving fully to Medicare saves you thousands. We take the guesswork out of that decision so you can move forward with certainty.

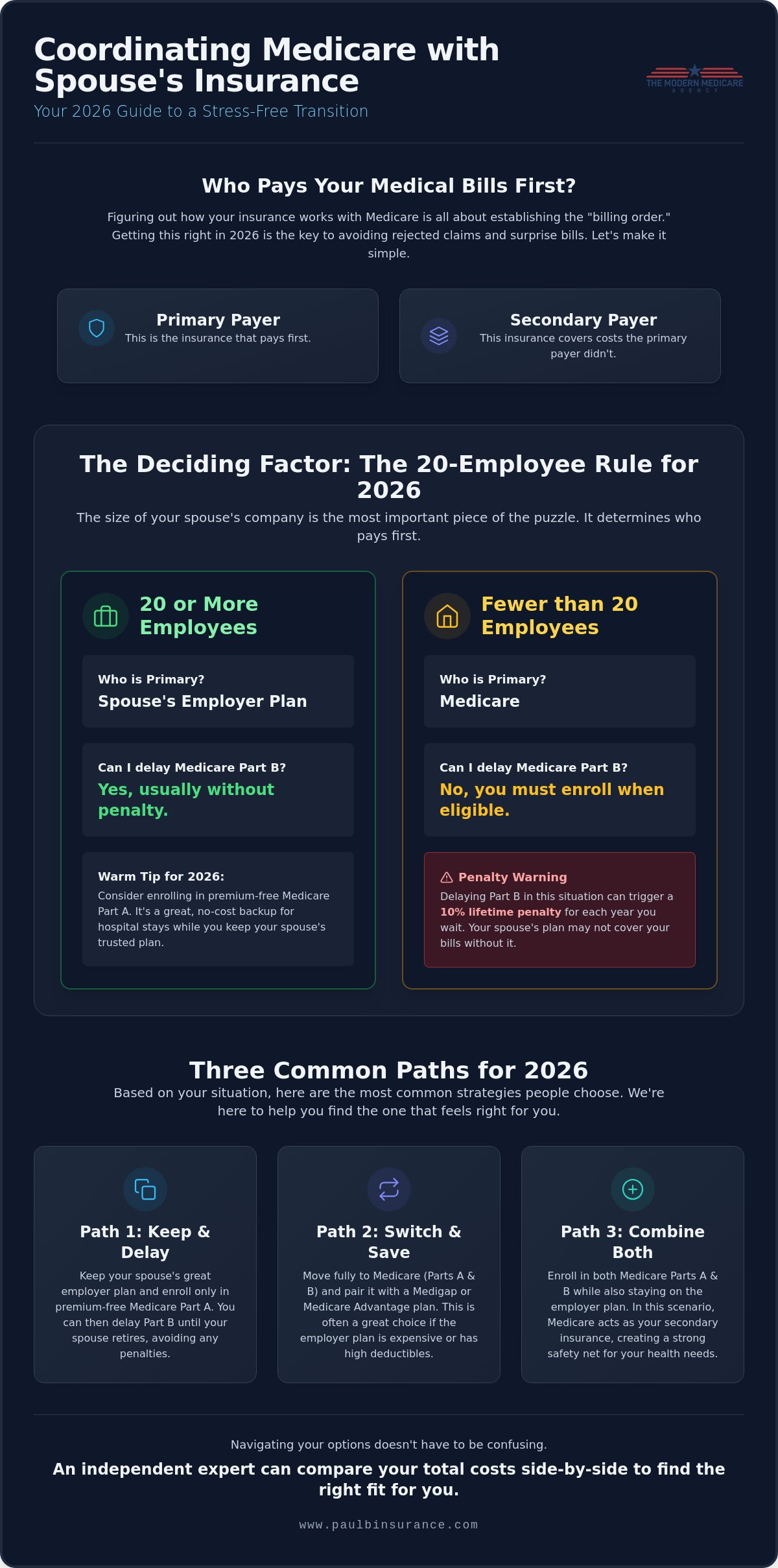

The 20-Employee Rule: Does Your Spouse’s Employer Size Matter?

The magic number is 20. If you’re trying to figure out how to coordinate medicare with my spouse’s insurance, this single number will dictate your entire strategy. In 2026, the federal government uses the size of your spouse’s employer to decide who is responsible for your medical bills first. It isn’t just a minor detail; it’s the foundation of your enrollment timeline. If the company has 20 or more employees, the employer plan usually stays primary. If the company is smaller than that, Medicare typically takes the lead the moment you turn 65.

There is a nuance called the “multi-employer” exception that sometimes catches people off guard. If your spouse works for a small local branch that only has five people, but that branch is part of a much larger corporation with hundreds of employees, you’re usually treated as being part of a large group. However, you should never guess on this. A quick, formal check with the HR department is the only way to be sure where you stand before you make any decisions about Part B.

Working for a Large Company (20 or More Employees)

If your spouse’s employer is large, you have a lot of flexibility. You can often delay Medicare Part B without worrying about a late enrollment penalty later. Many of our clients choose to sign up for “Part A only” while staying on their spouse’s plan. Since Part A is usually premium-free, it acts as a zero-cost backup for hospital stays. It’s a great way to get your foot in the door with Medicare while keeping the coverage you already know and trust. If you’re feeling overwhelmed by these choices, comparing your current costs to a Medicare Advantage guide can help you see if switching entirely might actually save you money in 2026.

The Small Business Trap (Under 20 Employees)

Working for a small business requires much more caution. In this scenario, Medicare MUST be your primary insurance. If you miss your enrollment window because you thought the small business plan would cover you, you’re walking into a “penalty trap.” We’ve seen cases where an employer plan pays a claim by mistake, realizes later that the person should have been on Medicare, and then “takes back” the payment. This can leave you with thousands of dollars in debt.

Because these rules are so strict, The Modern Medicare Agency helps you verify these tricky requirements so you don’t have to guess. We look at the specific 2026 regulations to ensure you aren’t leaving yourself vulnerable to a gap in coverage. If you aren’t sure how your spouse’s specific plan fits into these rules, reaching out for a quick review can give you the clarity you need to move forward safely.

Avoiding the “Penalty Trap”: Part B and Part D Timing

The biggest fear many of our clients share is accidentally triggering a penalty that follows them for the rest of their lives. When you’re looking at how to coordinate medicare with my spouse’s insurance, you must understand the concept of “creditable coverage.” This is simply insurance that the government considers at least as good as Medicare. If your spouse’s plan is creditable, you can usually delay Part B without a worry. If it isn’t, the clock starts ticking the moment you turn 65. You need to verify this status every year because employer plans can change their coverage levels without much warning.

Learning how to coordinate medicare with my spouse’s insurance means staying ahead of these deadlines so you never feel rushed or pressured into a bad decision. Getting your “Notice of Creditable Coverage” from your spouse’s insurance carrier is the most important step in this process. This document is your proof that you had acceptable insurance, which allows you to skip the penalties when you eventually join Medicare.

The Lifetime Cost of Waiting Too Long

The Part B late enrollment penalty is a 10% price hike for every 12-month period you were eligible but didn’t sign up. If you wait two years, you’ll pay 20% more for your Part B premium every single month. The Part B penalty is added to your monthly premium for the rest of your life. Social Security is very strict about these rules. Telling them you didn’t know or that an HR representative gave you bad advice won’t get the penalty waived. You need that written notice from the insurer to protect your savings. We recommend keeping these notices in a dedicated folder so they’re ready when you need them.

Part D and the 63-Day Rule

Drug coverage has its own set of rules and its own separate penalty. In 2026, Medicare Part D has become much more attractive because of the new $2,000 annual cap on out-of-pocket prescription costs. You might find that your spouse’s employer drug plan is actually more expensive or offers less protection than a standalone Part D plan now. If you decide to leave your spouse’s plan, you only have a 63-day window to find a new drug plan before penalties start to accrue. Learn more about Medicare Part D options to see how the 2026 changes might benefit your specific situation.

At The Modern Medicare Agency, we help you look at the “creditable” status of your current plan so you can make a choice based on facts, not guesswork. We’ve helped thousands of people navigate this exact transition, ensuring they never pay a penny more than they have to. We can compare your spouse’s 2026 premiums against Medicare’s current rates to see which path protects your wallet better.

Three Common Paths: Which One Fits Your Life?

Every family has a different health history and a different budget. When we sit down with folks to figure out how to coordinate medicare with my spouse’s insurance, we usually find that their situation fits into one of three distinct paths. Choosing the right one isn’t about following a trend; it’s about looking at your 2026 “Total Cost.” This means adding up your monthly premiums, your annual deductibles, and your estimated co-pays to see which option keeps more money in your pocket.

- Path 1: The “Double Up.” You enroll in Medicare while keeping your spouse’s plan. Medicare usually acts as a secondary payer here. It’s a great safety net for people with high medical needs, but you’ll be paying two sets of premiums.

- Path 2: The “Part A Only” approach. You sign up for Medicare Part A (Hospital Insurance) but delay Part B. This is the most common choice for people still covered by a large employer.

- Path 3: The “Full Transition.” You leave your spouse’s plan entirely and move to Medicare. If your spouse’s employer has high premiums for dependents, moving to a Medicare Advantage Plan might actually be the most budget friendly choice in 2026.

Our team at The Modern Medicare Agency can help you run these numbers side by side. We look at the 2026 costs for your spouse’s specific plan and compare them to the top carriers in your area. If you want to see how these options stack up for your specific doctors, you can request a personalized cost comparison today.

When Path 2 (Part A Only) is the Smartest Move

Since Medicare Part A is usually $0 for most people, it’s often a “no brainer” to sign up at age 65. It acts as a backup for hospital stays that your spouse’s insurance might not fully cover. However, there is one major exception. If you or your spouse contribute to a Health Savings Account (HSA), you cannot have any part of Medicare. Even signing up for “free” Part A will stop your ability to put tax free money into that account. If you’re weighing these costs, you might wonder, is Medigap a better fit than an Advantage plan for your long term needs?

Transitioning Successfully with a Special Enrollment Period (SEP)

If you decide to leave your spouse’s plan later, you’ll use a Special Enrollment Period. This allows you to join Medicare without any late penalties. You’ll need to coordinate with your spouse’s HR department to fill out Form CMS-L564. This form is your proof that you had group coverage. We always recommend timing your transition for the first of the month. This ensures you don’t have a single day where you’re unprotected. Getting the timing right removes the stress and ensures a smooth journey into your new coverage.

How The Modern Medicare Agency Simplifies Your Journey

HR departments are excellent at managing company benefits, but they aren’t Medicare specialists. Often, they give “safe” advice that focuses on protecting the company’s liability rather than your personal savings. They might suggest you stay on the employer plan simply because it’s the default option, without realizing that a Medicare plan could offer better coverage for a lower cost in 2026. This is where an independent advocate makes all the difference. We don’t work for a single insurance company; we work for you.

At The Modern Medicare Agency, we have the tools to compare your spouse’s current employer plan against more than 40 different Medicare options in just a few minutes. We look at the total picture, from your monthly premiums to your specific prescriptions and doctor preferences. Learning how to coordinate medicare with my spouse’s insurance shouldn’t feel like a second job. We take that burden off your shoulders so you can enjoy the peace of mind you’ve earned after years of hard work. We’re committed to being your partner for 2026 and every year that follows.

The Modern Medicare Advantage: Personal, Unbiased, and Free

Our services won’t cost you anything. We’re compensated by the insurance carriers, which means you get expert guidance and personalized research at no extra charge. We handle the confusing paperwork and the back-and-forth with Social Security that often leads to so much frustration. If you’ve been looking for a trusted Medicare broker near you, you’ve found a team that will stand by you. We don’t just sign you up and disappear. We’re here every time your spouse’s plan changes or your health needs evolve, ensuring you’re always on the best possible path.

Your Next Steps to Peace of Mind

Moving from a lifetime of employer coverage to Medicare is a big shift, but it’s much easier when you have a map. To prepare for your first talk with us, it’s helpful to have a list of your current medications and a copy of your spouse’s 2026 Summary of Benefits. Paul Barrett and our dedicated team are ready to review your situation and help you decide how to coordinate medicare with my spouse’s insurance without the stress. We believe that everyone deserves a guide they can trust to protect their health and their wallet. When you’re ready to move from uncertainty to a clear plan, we’re here to help. Schedule your simple, stress-free Medicare review today.

Step into Your Medicare Journey with Certainty

You’ve worked hard for your benefits; you shouldn’t have to spend your retirement worrying about whether you’ve filled out the right form. By now, you understand that the size of your spouse’s employer and the “creditable” status of their plan are the two most important factors in your 2026 strategy. We’ve seen how a simple mistake in how to coordinate medicare with my spouse’s insurance can lead to lifelong penalties, but we’ve also seen how a clear plan can save families thousands of dollars every year.

At The Modern Medicare Agency, we’re licensed in 34+ states and offer access to 40+ top insurance carriers. Our mission is to provide expert, unbiased guidance at no cost to you. We take the stress out of the process by comparing your current employer costs against every available Medicare option side-by-side. You don’t have to do this alone. Take the first step toward total peace of mind by requesting your Get a Free, No-Obligation Spousal Coordination Review. We’re here to protect your health and your future so you can focus on what really matters.

Frequently Asked Questions

Do I need Medicare Part B if I am on my spouse’s employer plan?

You don’t always need Part B immediately if you have coverage through a large employer. If your spouse’s company has 20 or more employees, Medicare allows you to delay Part B without a penalty. This is a common part of how to coordinate medicare with my spouse’s insurance. However; if the company is smaller than that, you must sign up for Part B at age 65 to avoid massive coverage gaps and future penalties.

What happens to my Medicare if my spouse retires or loses their job?

You have a safety net called a Special Enrollment Period. If your spouse stops working or the insurance ends, you have eight months to sign up for Part B. Don’t wait until the last minute. Most people find it’s best to have their new Medicare plan ready to start the very first day the old coverage ends so there is no gap in protection.

Can I keep my HSA if I sign up for Medicare Part A?

You can keep the money already in your account, but you cannot add new money to it. The IRS rules for 2026 state that once you enroll in any part of Medicare, your HSA contributions must stop. It’s often smart to stop contributing at least six months before you apply for Medicare to avoid tax headaches. This rule applies even if you only take the premium-free Part A.

Is my spouse’s retiree insurance considered “creditable coverage”?

No, retiree insurance is almost never considered “creditable” for Part B purposes. Even though it might be excellent coverage, the government doesn’t count it as active employment insurance. If you rely on retiree insurance and skip Part B, you’ll likely face a lifetime late enrollment penalty. Always check your specific plan’s annual notice to be 100% certain of its status.

How do I tell Medicare that my spouse’s insurance is my primary payer?

You’ll need to complete a Coordination of Benefits survey. Medicare usually sends this to you when you first join the program. You can also call the Benefits Coordination and Recovery Center to update your records directly. This ensures that the right company gets the bill first, which prevents those 2026 medical claims from being rejected or stuck in a billing loop.

What is the “20-employee rule” and how does it affect my Medicare enrollment?

This rule determines who pays your medical bills first. If the employer has 20 or more workers, their insurance is the primary payer and Medicare is secondary. If there are fewer than 20 employees, Medicare becomes primary. Knowing this rule is a vital step in learning how to coordinate medicare with my spouse’s insurance so you don’t get stuck with a bill the employer plan refuses to pay.

Will I be penalized if I wait to join Medicare until my spouse stops working?

You won’t be penalized as long as your spouse’s coverage meets the government’s standards for creditable coverage. Most large group plans qualify. When your spouse eventually stops working, you’ll have a window of time to join Medicare without any 10% price hikes. Just make sure you get written proof of that coverage from the employer or the insurance carrier every single year.

Can I switch from my spouse’s plan to a Medicare Advantage plan anytime?

You can’t switch at just any time. You generally need a Special Enrollment Period, which is triggered when you lose your spouse’s employer coverage. Otherwise, you’ll have to wait for the Annual Enrollment Period that happens every fall. Planning your exit from an employer plan requires careful timing to ensure you aren’t left without any insurance for a month or more during the transition.

Article by

Paul Barrett

Paul Barrett, CMIP is the founder of The Modern Medicare Agency, an independent Medicare-only brokerage based in Melville, NY. With 18 years of Medicare-exclusive experience, a CMIP designation, and more than 5,000 clients served across 37 states, Paul is one of the most credentialed independent Medicare specialists on Long Island — and one of the most direct.

He represents 40+ carriers with no quotas and no allegiances, which means his recommendations are based entirely on what fits each client's specific situation. He is the author of Medicare Mastery Unlocked and host of the Wise Guys Retirement Talk podcast. His content is grounded in primary sources, real carrier intelligence, and 18 years of watching what happens when people get Medicare right — and when they don't.

📞 631-358-5793 | paulbinsurance.com