What if the health history you can’t change becomes the reason you’re stuck with thousands of dollars in medical bills? It’s a question that keeps many people up at night, especially as we look at the rising costs of care in 2026. You might be wondering, “can i be denied a medigap policy because of a past illness?” The short answer is yes, but only in certain situations. We know how stressful it feels to worry about being rejected when you just want the peace of mind that comes with reliable coverage.

We’re here to clear up the confusion between your one-time enrollment window and the yearly sign-up periods so you don’t miss your best chance at a plan. In this guide, we explain exactly when insurance companies can deny you coverage and how to protect your right to a Medigap plan. We’ll also cover the 2026 rule changes, including shifts in Plan N availability and state-specific protections that could be your “Golden Ticket” to securing the security you deserve.

Key Takeaways

- Understand the specific legal situations where you can i be denied a medigap policy and how to avoid these common pitfalls.

- Identify your six-month “Golden Ticket” window to guarantee your acceptance into any plan regardless of your medical history.

- Learn about “Guaranteed Issue” rights that protect you during major life changes, ensuring you aren’t left without coverage.

- Explore how state-specific rules and expert guidance can help you find a plan even if you have pre-existing conditions.

- Get clarity on 2026 changes to popular plans so you can make an informed choice before your options become more limited.

Can You Be Denied a Medigap Policy? The Short Answer for 2026

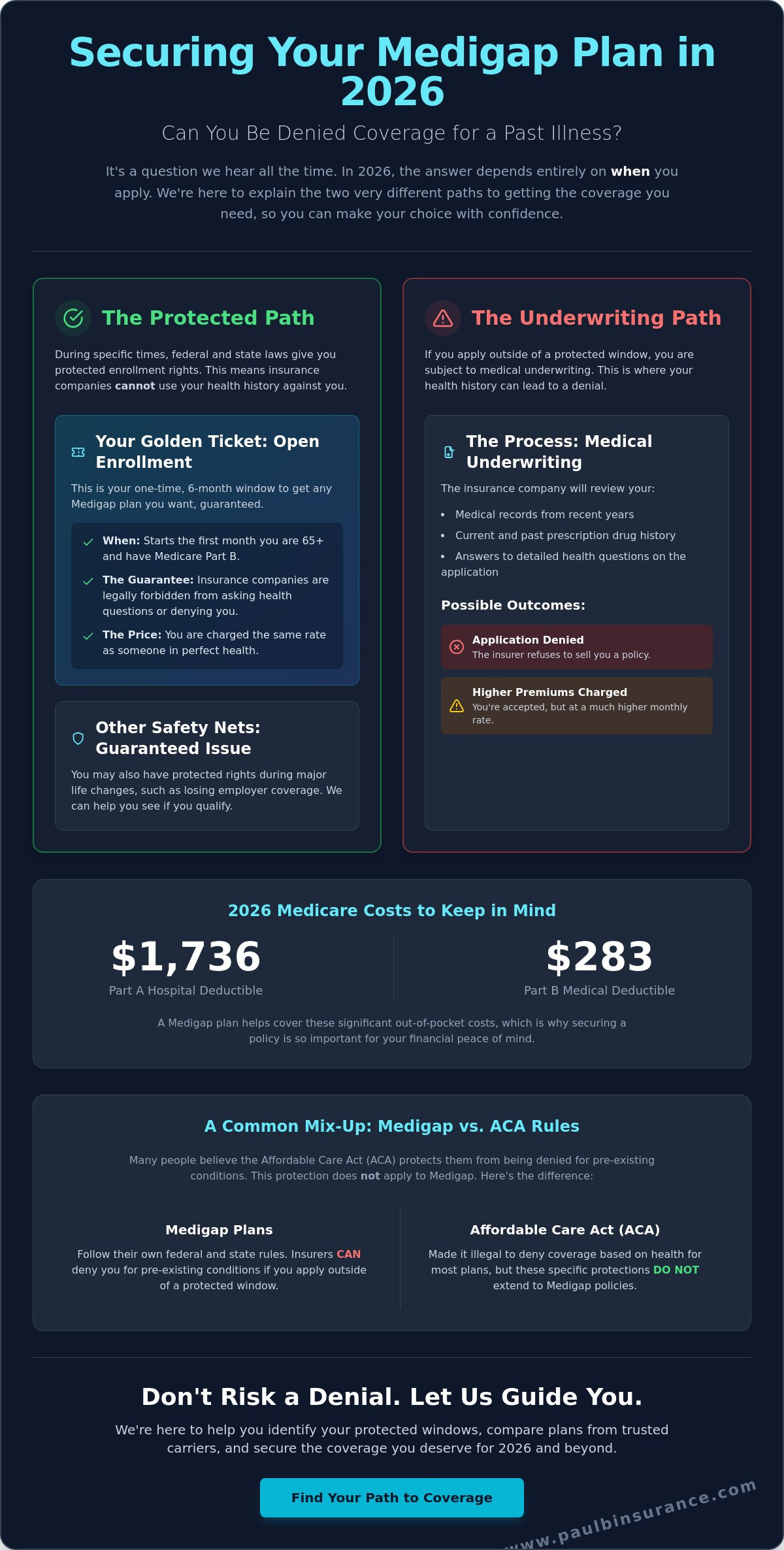

Many people assume that because they are on Medicare, their supplemental coverage is guaranteed. Unfortunately, that isn’t always the case. In 2026, private insurance companies still have the legal right to deny your application based on your health status in many situations. It’s a reality that can feel overwhelming, especially when you are trying to manage your budget against the $283 Part B deductible or the $1,736 Part A hospital deductible. We want to help you understand these rules so you never feel stuck without the protection you need.

If you are asking, “can i be denied a medigap policy,” the answer depends almost entirely on when you apply. Your health history only matters if you submit an application outside of specific protected windows. We spend a lot of our time helping clients identify if they are currently in a “safe zone” where denial is legally impossible. When you work with us, we look at your specific situation to ensure you don’t face an unnecessary rejection. You can learn more about how these plans work on our Medigap page.

The Reality of Medical Underwriting in 2026

When you apply for a Medigap plan outside of a protected window, you go through medical underwriting. This is a process where the insurance carrier reviews your medical records and your current prescriptions. They use this data to decide if they will accept you as a policyholder. In most states, if you don’t meet their health standards, they can either charge you a much higher premium or refuse to sell you a policy at all. It feels personal, but for the insurance company, it’s a cold calculation of risk. We help you navigate this by finding carriers that may have more lenient standards for your specific health history.

Medigap vs. The Affordable Care Act (ACA)

A common reason for confusion is the Affordable Care Act (ACA). The ACA changed the rules for most health insurance, making it illegal to deny coverage for pre-existing conditions. However, those specific protections don’t apply to Medigap. Because Medigap is a private contract designed to supplement Original Medicare, it follows a different set of federal and state rules. Many seniors miss their enrollment windows because they believe the ACA rules protect them. We want to make sure you don’t fall into that trap. Understanding that Medigap remains a private contract is the first step toward protecting your right to coverage. We are here to act as your advocate, making sure you understand the rules before you ever fill out an application.

Your Golden Ticket: The Medigap Open Enrollment Period

We often call this six month window your “Golden Ticket” because it’s the only time in your life when the answer to “can i be denied a medigap policy” is a definitive no. It’s a period of absolute certainty in a system that can often feel unpredictable. During these six months, private insurance companies are legally forbidden from looking at your medical records or asking about your prescriptions. They must sell you any plan they offer at the same price they would charge someone in perfect health. We want you to feel the relief of knowing that, for this brief time, your health history simply doesn’t matter.

Missing this window is the primary reason people face stressful denials later in life. Once these six months pass, the “shield” of federal protection drops in most states. Carriers can then use medical underwriting to decide if they want to take you on as a client. If you’re approaching age 65 in 2026, we can help you map out your timeline so you don’t miss a single day of this vital protection. Taking action early ensures you aren’t left scrambling at the last minute.

When Exactly Does Your Window Start?

Your enrollment window is a one-time event. It begins on the first day of the month you are 65 or older and enrolled in Medicare Part B. For most people, this happens the month they turn 65. If you delayed Part B because you were still working, your window starts the moment your Part B coverage finally begins. This window lasts for exactly six months. It cannot be paused, and it cannot be restarted. We recommend starting your search at least three months before your Part B effective date. This gives you plenty of time to compare options without feeling rushed or anxious.

Why This Window Is Your Best Protection

The beauty of this period lies in its simplicity. You can choose any plan available in your area, such as the comprehensive Plan G or the cost-effective Plan N, without worrying about a single health question. If you have “creditable coverage” from an employer or another source before joining, companies cannot even make you wait for coverage of pre-existing conditions. These guaranteed issue protections are the strongest tools you have to secure your financial future. You can find more details on how these specific plans work on our Medigap information page. It provides the peace of mind that your physical health will never stand in the way of your medical care.

Guaranteed Issue Rights: Times When They Must Accept You

Life is full of changes, and sometimes those changes are beyond your control. If your current health plan ends or you move to a new state, you might feel a surge of anxiety. You may ask yourself, “can i be denied a medigap policy if my current plan disappears?” Fortunately, federal law includes “Guaranteed Issue” (GI) rights. These rights act as a powerful shield, forcing insurance companies to accept your application even if you have a serious chronic illness. We spend our days helping people identify these moments so they can move forward with confidence and clarity.

To exercise these rights, timing is everything. You usually have exactly 63 days from the day your previous coverage ends to buy a Medigap plan. When these specific rights apply, the answer to “can i be denied a medigap policy” becomes a firm no. We walk beside you through the paperwork process, helping you gather the “Notice of Termination” letters required by carriers. Without this proof, a company might try to put you through medical underwriting. We ensure your documentation is perfect so the insurance company has no choice but to say yes. Understanding the official Medigap enrollment rules is the best way to protect your future security.

Common Situations That Create GI Rights

Many people find themselves in a GI window without even realizing it. In 2026, we see many Medicare Advantage plans leaving specific counties or stopping service altogether. If your plan is exiting your area, you have a right to buy a Medigap policy. Moving is another common trigger. If you move out of your current plan’s service area, such as moving from New York to Florida to be closer to family, you gain a window to switch. Additionally, if your employer-sponsored retiree health coverage is ending, federal law protects your right to transition into a supplemental plan without health questions.

The “Trial Right” for Medicare Advantage

Perhaps the most helpful protection is the “Trial Right” for those new to Medicare. If you joined a Medicare Advantage plan when you first became eligible at 65, you have a 12-month window to change your mind. This “Trial Right” allows you to switch back to Original Medicare and buy a Medigap plan without any health questions. It serves as a vital safety net for those who realize an Advantage plan isn’t the right fit for their needs. If you are currently in an Advantage plan and considering a change, our Medicare Advantage guide can help you understand how these systems work together to protect you.

What Happens If You Apply Outside a Protected Window?

Applying for coverage when you aren’t in a protected window can feel like walking into a maze without a map. If you missed your initial six month window or don’t have a specific life event that triggers a “Guaranteed Issue” right, you will likely face medical underwriting. This is the moment when many of our clients ask, “can i be denied a medigap policy because of my health?” The answer is yes; private companies can look at your history and decide not to offer you a plan. However, a “no” from one company does not mean everyone will reject you. We help you look at the different “look-back” periods carriers use for conditions like heart disease or cancer, which often range from two to five years.

We believe that knowledge is the best cure for anxiety. Every insurance company has its own set of rules for which health risks they are willing to take. Some might be very strict about a recent surgery, while others are more focused on long-term chronic issues. We work to find the right fit for your specific health profile so you don’t accidentally trigger a denial that could have been avoided. If you are worried about your current health status, you can contact us today to review your options before you submit an application.

Common Health Questions You Might Face

When you apply “late,” the insurance company will ask detailed questions about your health. Most applications in 2026 focus on hospitalizations or major surgeries within the last two years. They will also run what is known as a “prescription drug hit.” This is a digital report that shows the medications you have filled in the recent past. Carriers use this to identify chronic conditions that might not be mentioned elsewhere. Some common reasons for denial include:

- Chronic Obstructive Pulmonary Disease (COPD) or other chronic respiratory issues.

- Insulin-dependent diabetes, especially if combined with heart or kidney problems.

- Recent treatments for internal cancer or heart-related procedures.

- Current use of certain high-cost specialty medications.

Denial vs. Pre-existing Condition Waiting Periods

It is vital to understand the difference between a denial and a waiting period. A denial is a flat rejection; the company refuses to sell you the policy. A pre-existing condition waiting period is different. If a company accepts your application but you have a health issue, they may refuse to pay for care related to that specific issue for up to six months. During this time, the policy still covers everything else. In 2026, with the Part A hospital deductible at $1,736, even a policy with a waiting period can provide significant financial security for new health issues. We help you weigh these options so you can plan your healthcare budget for that first transition year. You can find more details on how these rules apply to different plans on our Medigap information page.

How We Help You Find a Path to Coverage

Where you live is just as important as when you apply. While the federal rules provide a baseline of protection, many states have passed their own laws to give you even more security. We know that the fear of a rejection can be paralyzing, especially if you have been managing a health condition for years. You might still be asking yourself, “can i be denied a medigap policy if my health has changed?” The answer often depends on the specific zip code you call home. We make it our mission to understand these local nuances so we can guide you to the best possible outcome.

We don’t work for the insurance companies; we work for you. As independent brokers, we have the freedom to look at the entire market rather than being restricted to a single carrier’s offerings. This independence is your greatest advantage. We help you move from a state of uncertainty to a place of complete confidence. Our goal is to ensure that by the time we submit an application, we already have a very good idea of what the answer will be. You can explore the different types of Medigap plans we compare to see which one fits your needs for 2026.

State-Specific Protections (NY, CA, FL)

Some states offer incredible protections that bypass standard underwriting altogether. In New York, for example, Medigap is “Continuous Guaranteed Issue.” This means you cannot be denied at any time of the year, regardless of your health history. Other states like California and Florida have specific “Birthday Rules” or unique guaranteed issue events that we can leverage for you. These rules allow you to switch plans or join a new one during specific windows without answering a single health question. We ensure you are taking full advantage of these local laws so you never pay more than necessary.

The Value of an Independent Expert

We compare over 40 different carriers to find the one with the most lenient underwriting for your specific condition. This is a level of support you simply won’t get from a restricted representative who only sells one brand. We help you avoid the “trial and error” approach that leads to multiple denials on your record. Instead, we use our expertise to identify the carrier most likely to say yes to your specific health profile. We want to remove the stress from this process and give you peace of mind for 2026 and every year that follows. Our step-by-step path turns a difficult journey into a simple, successful transition to the coverage you deserve.

Secure Your Peace of Mind for 2026

Getting the right coverage doesn’t have to be a source of stress. We’ve explored how your initial six month window and specific life changes act as a shield against medical questions. You now know that while the answer to can i be denied a medigap policy can be yes in some cases, there are many legal “safe zones” designed to protect you. Whether you’re navigating the unique rules in New York or leveraging a birthday rule in California, your location and timing are your greatest assets.

We’re here to help you navigate these choices with clarity. Our team of independent brokers offers unbiased guidance and access to over 40 insurance carriers. We have deep expertise in 34 states, including Florida and New York, ensuring you get the most from your local laws. You don’t have to do this alone. Let our experts help you find a Medigap plan you can count on. You deserve to move into 2026 with a plan that gives you certainty. We’re ready to help you take that next step toward total peace of mind.

Frequently Asked Questions

Can I be denied Medigap if I have cancer?

Yes, you can be denied coverage if you apply during a time when medical underwriting is required. However, if you are in your initial six month Open Enrollment window, the company must accept you regardless of your diagnosis. We help you look for specific windows where your history won’t be a barrier to getting the care you need. Timing is the most important factor in protecting your right to a plan.

Does the Annual Enrollment Period (AEP) let me switch to Medigap without health questions?

No, the Annual Enrollment Period does not waive health questions for Medigap. This is a very common point of confusion for many seniors. AEP allows you to change your Medicare Advantage or Part D plan, but it doesn’t give you a free pass into a Medigap policy. If you want to switch from Advantage to Medigap during this time, you will usually have to pass a health check and answer medical questions.

What are the states that don’t allow Medigap companies to deny you?

Connecticut, Massachusetts, Maine, and New York offer the strongest protections against being rejected. In New York, you cannot be denied a policy at any time of the year because of the state’s continuous enrollment rules. You might still wonder, “can i be denied a medigap policy in other states?” Most other states allow underwriting after your initial window ends. We make sure you understand the specific laws in your zip code to find your best options.

Can a Medigap company cancel my policy if I get sick later?

No, your policy cannot be canceled because of your health as long as you pay your premiums on time. Medigap plans are guaranteed renewable. This means even if you develop a serious condition like heart disease or Alzheimer’s after your policy starts, the insurance company must continue your coverage. This rule provides the long term security and peace of mind we want all our clients to have when navigating the healthcare system.

Is there a difference in denial rates between Plan G and Plan N?

The health questions are typically the same for both plans, but some carriers are becoming more restrictive with Plan N availability. Starting in April 2026, some major companies will no longer offer Plan N during certain guaranteed issue periods. While the denial rates for underwriting are similar, the availability of these plans is shifting. We help you compare these options to find the most stable path forward for your healthcare budget and coverage needs.

How far back do Medigap companies look at my medical records?

Most insurance companies look back at your medical records and prescription history for the last two to five years. They are specifically looking for chronic conditions or recent major surgeries that might indicate future risk. Every carrier has a different list of conditions they are willing to accept. We help you navigate these look-back periods by finding companies that have more lenient standards for your specific health history so you can avoid unnecessary denials.

Can I be denied a Medigap policy if I am under 65 and on disability?

Yes, you can be denied a medigap policy in many states if you are under 65, as federal law does not require carriers to sell to those on disability. While some states have passed laws to protect younger beneficiaries, many have not. This often leaves people in a difficult position where they are stuck with high out of pocket costs. We can help you check your state’s specific 2026 rules to see if you have a path to a plan.