You can expect Medicare Part B to cover most outpatient care you get from doctors, clinics, and outpatient hospitals, plus many preventive services, tests, and medically necessary supplies like durable medical equipment.

Part B pays for doctor visits, outpatient procedures, lab tests, mental health services, and certain injections and durable equipment when they’re medically necessary or preventive.

This post will walk you through what counts as covered care and what might not be.

If you want help sorting your options, The Modern Medicare Agency makes it simple: licensed agents you can talk to one-on-one review your needs, match you to plans, and do not add hidden fees.

Keep reading to see which doctor visits, tests, therapies, and supplies Medicare Part B typically covers and how to verify coverage for your situation.

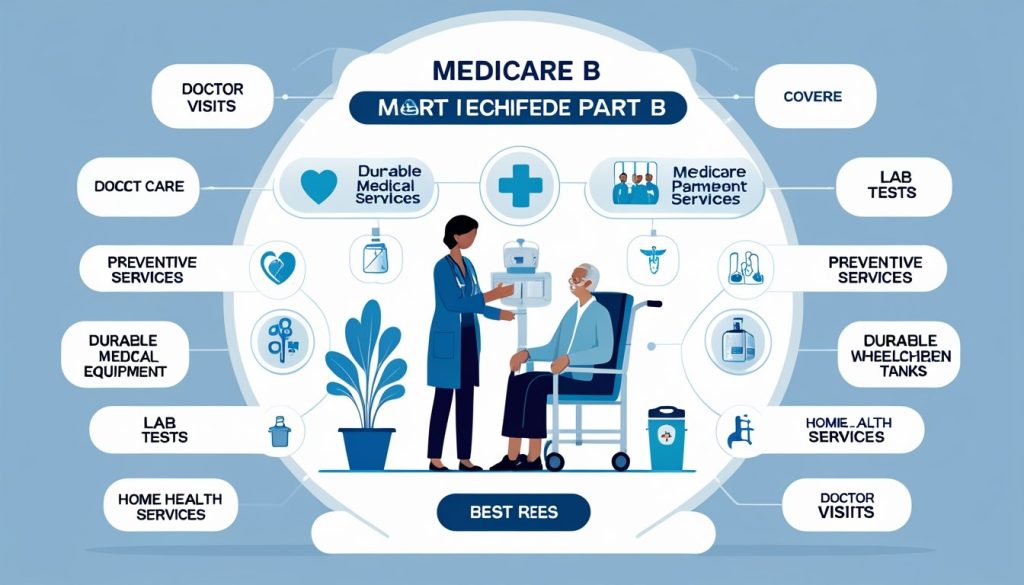

Overview of Medicare Part B Coverage

Medicare Part B pays for many outpatient services you get from doctors and clinics.

It covers preventive care, tests, medical equipment, and some home health services, with costs shared between you and Medicare.

Eligibility Requirements

You qualify for Part B if you are age 65 or older and either already receive Social Security or Railroad Retirement Board benefits, or you enroll during your initial enrollment window.

Younger people with certain disabilities or those with end-stage renal disease may also qualify.

If you live in the U.S. as a legal resident and meet the work-history requirements tied to Social Security credits, you will typically be eligible for Part B.

You must have Part A coverage or be eligible for it; Part B stands alone but normally pairs with Part A for full Original Medicare benefits.

The Modern Medicare Agency can check your specific eligibility in minutes and explain exceptions, such as special enrollment periods after employer coverage ends.

Our licensed agents speak with you 1-on-1 to confirm when and how to enroll.

Enrollment Process

You usually enroll in Part B during your Initial Enrollment Period: the three months before your 65th birthday, the month you turn 65, and the three months after.

If you miss that window, you can sign up during the General Enrollment Period from January 1 to March 31 each year, but coverage starts July 1 and you may pay a late-enrollment penalty.

If you have active employer coverage at 65, you can delay Part B and use a Special Enrollment Period when that job-based coverage ends.

To enroll, you can sign up online at Social Security or call Social Security directly.

The Modern Medicare Agency helps you pick the right time to enroll and avoids penalties.

Our agents walk you through forms and deadlines so your start date and coverage match your needs.

Monthly Premiums and Costs

Part B has a monthly premium that most people pay.

In 2026 the standard premium is $202.90 per month; higher-income beneficiaries may pay an Income-Related Monthly Adjustment Amount (IRMAA).

You also owe an annual deductible—$283 in 2026—then typically 20% coinsurance for most services after Medicare approves the cost.

Costs vary by year and by your reported income from two years prior.

If you get Social Security benefits, your premium may be deducted from your benefit check.

Durable medical equipment, outpatient tests, and many doctor services all follow the 20% coinsurance rule unless supplemental coverage or a Medicare Advantage plan covers more.

The Modern Medicare Agency explains how premiums, IRMAA, deductibles, and coinsurance will affect your budget.

Our licensed agents compare options that fit your finances and won’t charge extra fees for this guidance.

Doctor and Outpatient Services

Medicare Part B pays for many visits, tests, and outpatient treatments you get from doctors and clinics.

It helps cover regular checkups, specialist care, outpatient procedures, and second opinions before surgery.

Primary Care Visits

Part B covers medically necessary visits with your primary care doctor.

This includes office visits for illness, chronic condition management like diabetes or high blood pressure, and preventive visits such as yearly wellness exams.

You pay the Part B deductible first, then usually 20% of the Medicare-approved amount for each visit unless you have supplemental coverage.

Your primary care provider can order lab tests, X-rays, and certain outpatient services that Part B also covers.

They can also refer you to specialists when needed.

If you want help choosing plans that lower out‑of‑pocket costs for regular doctor visits, The Modern Medicare Agency offers licensed agents who speak with you 1 on 1 and find Medicare options that match your needs without extra fees.

Specialist Consultations

Part B covers consultations with specialists when a doctor refers you or when care is medically necessary.

This includes visits to cardiologists, neurologists, orthopedists, and other specialty doctors for diagnosis and treatment.

You are responsible for the Part B coinsurance after meeting the deductible, typically 20% of the approved cost.

Specialists can perform diagnostic tests during visits, and Part B covers those tests when ordered by a doctor.

If you need help finding plans that reduce coinsurance or connect you with in‑network specialists, The Modern Medicare Agency’s licensed agents can review your options and explain costs clearly.

Outpatient Medical Procedures

Outpatient procedures done in a clinic or hospital outpatient department fall under Part B when they are medically necessary.

Examples include minor surgeries, certain biopsies, endoscopies, and wound care.

Part B covers the doctor’s service and usually part of the facility fee; you pay the deductible and the coinsurance portion.

Durable medical equipment and certain injectable drugs you receive during outpatient visits can also be covered by Part B.

If you want to lower facility or procedure costs, an agent at The Modern Medicare Agency can help compare Medicare plans and explain which coverages reduce your share of expenses.

Second Opinions for Surgery

Part B covers second‑opinion visits when you want confirmation that surgery is necessary or to explore less invasive options.

A covered second opinion must be with a qualified doctor and deemed medically appropriate.

You pay the same Part B cost-sharing as with other doctor visits.

Getting a second opinion can affect whether Medicare approves or helps pay for planned surgery.

The Modern Medicare Agency can connect you with licensed agents who help you understand coverage rules, find participating doctors, and choose plans that support access to second opinions without hidden fees.

Preventive Services Covered

Medicare Part B pays for many services that help find health problems early, prevent disease, and keep you healthy.

You get screenings, shots, and an annual visit that sets up a personalized prevention plan.

Screenings and Tests

Medicare Part B covers many screening tests to detect cancer, heart disease, diabetes, and other conditions early.

Commonly covered tests include mammograms for breast cancer, colon cancer screenings (like colonoscopy or stool tests), and Pap tests plus pelvic exams.

You also get screening for cardiovascular disease risk with blood tests and EKGs when appropriate, and diabetes screening for those at risk.

Most screenings are free if you use a provider who accepts Medicare and meet program rules.

Some tests require a doctor’s order or have specific frequency limits—mammograms yearly or every two years, colon cancer screening intervals vary by method.

Ask your provider if a test needs prior approval or if a copay applies for follow-up care.

Vaccinations and Immunizations

Part B covers several vaccines that protect you from serious illnesses.

Medicare pays for flu shots each year and one dose of the pneumococcal vaccines that help prevent pneumonia.

Part B also covers the COVID-19 vaccine and certain hepatitis B vaccines when you’re at medium or high risk.

You usually pay nothing for these vaccines if the provider accepts Medicare assignment.

Keep records of which vaccines you’ve had; timing matters—for example, flu shots are annual while pneumococcal shots follow a specific schedule.

If a vaccine is covered under Part D instead of Part B, ask your agent or provider which plan pays so you won’t get unexpected bills.

Annual Wellness Visits

Medicare Part B covers a yearly “Welcome to Medicare” and an Annual Wellness Visit (AWV) after the first year.

These visits focus on prevention, not treatment.

During an AWV, your provider creates or updates a personalized prevention plan based on your medical history, current health, risk factors, and screening schedule.

The visit includes measuring height, weight, blood pressure, and cognitive assessments when needed.

You’ll discuss vaccines, screenings, and steps to reduce health risks.

There’s no charge for the AWV if your provider accepts Medicare, but tests or services ordered during the visit might carry separate charges.

Medically Necessary Services and Supplies

Medicare Part B pays for items and services that a doctor says you need to treat an illness or injury.

You should expect coverage only when a licensed provider documents medical necessity and uses a Medicare-approved supplier.

Durable Medical Equipment

Durable Medical Equipment (DME) includes items you use at home to manage a health problem.

Examples are oxygen equipment, hospital beds, wheelchairs, walkers, and certain nebulizers.

To get DME covered, your doctor must write a prescription that shows why the item is medically necessary.

The supplier must be enrolled in Medicare.

Medicare typically pays 80% of the Medicare-approved amount after your Part B deductible, and you pay the remaining 20% unless you have other coverage.

Check whether the supplier accepts Medicare assignment.

If they do not, you may face higher out-of-pocket costs.

Your supplier should document the need and keep records to support coverage.

Ambulance Transportation

Medicare Part B covers ambulance rides when other transport is unsafe and EMS care is essential.

Covered trips often include emergency transport to the nearest appropriate facility and non-emergency transport when your condition requires ambulance-level care.

A doctor or other qualified provider must certify that ambulance transport is medically necessary.

Medicare pays its approved amount, leaving you responsible for 20% and any Part B deductible, unless you have secondary insurance.

Keep detailed records and ask the ambulance provider if they accept Medicare assignment.

If air transport is needed, Medicare covers it only when ground transport cannot meet your medical needs.

Home Health Care

Home health services cover skilled nursing care, physical therapy, speech therapy, and some medical supplies when you are homebound and a doctor certifies ongoing skilled care.

Medicare Part B pays for outpatient therapy services provided at home and some home health services when they are not covered under Part A.

A doctor must create and review your plan of care regularly.

Services must be provided by Medicare-certified home health agencies or qualified clinicians.

Medicare generally pays the approved amount for covered services; you may owe 20% for some outpatient therapy costs and any applicable deductible.

Mental Health and Therapy Services

Medicare Part B helps pay for many outpatient mental health and therapy services.

You’ll find coverage for therapy visits, certain substance use treatments, and therapy aimed at improving daily function after injury or illness.

Outpatient Mental Health Visits

Medicare Part B covers psychotherapy, psychiatry visits, and diagnostic assessments when a Medicare-approved provider gives them in an outpatient setting.

This includes individual and group therapy, family counseling when needed for your treatment, and annual depression screenings performed by a qualified clinician.

You pay the Part B deductible first, then typically 20% of the Medicare-approved amount for each covered visit if your provider accepts Medicare assignment.

If you see a non-participating provider, costs can be higher.

Telehealth mental health visits are usually covered if the provider follows Medicare rules.

To get covered care, choose providers enrolled in Medicare or participating in Medicare Advantage networks.

The Modern Medicare Agency can help you find in-network mental health providers and explain cost-sharing for visits.

Substance Use Disorder Treatment

Part B covers outpatient treatment for substance use disorders, including counseling and visits with psychiatrists or addiction specialists. Coverage applies to medically necessary services like medication management for addiction, psychotherapy, and certain office-based treatment programs.

You pay the Part B deductible and generally 20% coinsurance after the deductible. Inpatient detox and rehab may fall under Part A or need separate coverage, so confirm settings and billing before treatment.

Medicare requires services to be provided by eligible, credentialed providers for coverage to apply.

Occupational and Physical Therapy

Part B covers outpatient occupational therapy (OT) and physical therapy (PT) when they are medically necessary to improve or restore your ability to function. Covered services include evaluations, therapy sessions, and equipment needed during therapy, such as walkers or braces used in treatment.

You pay the Part B deductible first, then usually 20% of the Medicare-approved amount for each therapy visit. Medicare has limits on therapy “cap” amounts in some cases, but many services are covered if a doctor documents medical necessity and reviews progress periodically.

Make sure therapists are Medicare-enrolled or in your Medicare Advantage network so visits count toward coverage.

Laboratory and Diagnostic Tests

Medicare Part B pays for many tests your doctor orders to diagnose or treat health problems. You will usually need a provider’s order and the provider must accept Medicare assignment for Part B to cover the cost.

Blood Tests

Medicare Part B covers medically necessary blood tests ordered by your doctor. This includes basic panels like complete blood count (CBC), basic metabolic panel (BMP), and tests for blood sugar (glucose) or cholesterol.

It also covers many specialized tests used to monitor chronic conditions, such as hemoglobin A1c for diabetes or tests that track kidney and liver function. If the lab accepts assignment, Medicare pays its approved amount and you pay any Part B coinsurance or deductible that applies.

Preventive blood tests that Medicare specifically lists—such as certain screenings—may be covered with no cost-sharing when you meet eligibility rules. Always confirm the test is ordered by an authorized provider and that the lab files claims to Medicare.

X-rays and Imaging

Part B covers diagnostic X-rays and many outpatient imaging services when your doctor orders them. Covered items include standard X-rays, CT scans, MRI scans, and certain ultrasounds used to diagnose injury or illness.

The test must be medically necessary and performed by a Medicare-approved facility or provider. You normally pay the Part B coinsurance after Medicare pays its share.

Some advanced imaging may require prior authorization based on Medicare’s rules or local coverage determinations. Ask your provider to verify that the imaging center accepts Medicare assignment to avoid unexpected bills.

Pathology Screenings

Pathology services under Part B include tissue analysis, biopsies, and cytology tests used to identify cancer, infections, and other diseases. Medicare covers lab processing, pathology interpretation, and related technician services when ordered by your treating physician and tied to diagnosis or treatment.

Certain screening tests—such as some cancer screenings—have specific coverage criteria that can reduce or eliminate your out‑of‑pocket cost if you meet the rules. Make sure your provider documents medical necessity and that the lab is Medicare‑approved.

Medications and Injections Covered

Medicare Part B pays for a narrow set of outpatient drugs when they are given in a medical setting or are tied to other covered services. You’ll mainly see coverage for drugs given by a clinician, certain vaccines, and specific post-transplant medications.

Limited Outpatient Drugs

Part B covers outpatient drugs only in specific situations, not routine prescriptions you fill at a retail pharmacy. Examples include drugs that are:

- Given as part of a physician’s service (infusions, injections, or drugs “incident to” a doctor’s care).

- Used with covered durable medical equipment (like certain drugs for infusion pumps).

Coverage often depends on medical necessity and the drug being administered in a clinic, office, or outpatient facility. You may still pay coinsurance and a provider-administered drug may be billed separately from the office visit.

Administered Injections

Medicare Part B covers many injectable and infused drugs when a clinician gives them in an outpatient setting. This includes cancer chemotherapy drugs, some biologics, and other physician-administered meds.

If the injection is typically self‑administered at home, Part B usually won’t cover it unless there’s a specific exception. When a provider gives the injection, billing goes through Part B and you may face a 20% coinsurance after the Part B deductible.

Ask your provider to confirm that the drug is billed under Part B and whether any prior authorization or step therapy rules apply.

Certain Immunosuppressive Drugs

Part B covers some immunosuppressive drugs for patients who have received a Medicare-covered organ transplant. These drugs help prevent organ rejection and must be medically necessary and tied to the covered transplant.

If you qualify, Part B may cover the medications for a defined period after the transplant. You should verify eligibility and coverage details with your provider and Medicare to avoid unexpected costs.

Exclusions and Limitations

Medicare Part B does not pay for everything. Some services, supplies, and settings are specifically excluded or limited, and you usually share costs for covered items.

Non-Covered Items

Medicare Part B generally excludes routine dental care, most eyeglasses and contact lenses for vision correction, and routine podiatry services. Cosmetic surgery and most long-term care or custodial care — like help with bathing or dressing — are not covered.

Services that Medicare considers experimental or not medically necessary also get denied. Some items are statutorily excluded by law; when that happens, you may get a voluntary Advance Beneficiary Notice (ABN) and be billed directly.

Always check before care: ask your provider whether Medicare will pay and request pre-authorization when available.

Coverage Restrictions

Many Part B benefits come with limits. Durable medical equipment (DME) must meet specific medical criteria and often requires a signed order and supplier enrollment.

Imaging, lab tests, and some outpatient procedures may need prior authorization or frequency limits. Home health coverage requires a doctor’s plan of care and intermittent skilled need.

Services provided “incident to” a physician’s service follow strict rules for payment. If a provider or supplier isn’t enrolled or if documentation is missing, Medicare can deny the claim.

Ask providers about medical necessity, documentation, and any prior authorization steps before receiving care.

Cost-Sharing Responsibilities

With Part B, you typically pay the monthly premium, an annual deductible, then 20% coinsurance for most approved services. For certain preventive services, Medicare may pay 100% if you meet criteria.

If you receive care from an out-of-network provider without proper enrollment or billing, you could face full charges. When Medicare denies coverage, you may be billed for the full cost unless you signed an ABN.

Keep records: get itemized bills, ask for Medicare billing codes, and request an explanation of benefits (EOB).

How to Verify Medicare Part B Coverage

Start by checking your Medicare card. It shows whether you have Part B and your effective date.

Keep the card handy when you call or check online.

Use your MyMedicare.gov account to see covered items and claims. Sign in to review services, durable medical equipment, and preventive care records.

The site updates regularly after a provider submits a claim.

Call Medicare at the number on your card if you need a live answer. Have your Medicare number, date of birth, and service details ready.

The representative can confirm coverage and explain any cost sharing.

Ask your provider to verify coverage before services or equipment are ordered. Your doctor or supplier can submit a pre-claim or prior authorization request when needed.

This step helps avoid unexpected bills.

Contact The Modern Medicare Agency for one-on-one help from licensed agents. Our agents speak with you directly to review your needs and check Part B coverage details.

We match Medicare plans to your situation without charging extra fees.

Keep a record of all calls and authorizations. Note dates, names, and confirmation numbers.

These records simplify disputes or appeals if a coverage question arises.